NBB - NBB: A Few Reasons Why I'm More Bullish Going Forward (Rating Upgrade)

2023-08-30 21:23:24 ET

Summary

- Nuveen Taxable Municipal Income Fund is currently undervalued with a discount to NAV of almost 9%.

- Taxable munis offer higher income compared to tax-exempt munis, making them attractive for investors in lower tax brackets.

- NBB has maintained its distribution in the short-term, providing reassurance to investors despite the challenges posed by the inverted yield curve.

Main Thesis & Background

The purpose of this article is to evaluate the Nuveen Taxable Municipal Income Fund ( NBB ) as an investment option at its current market price. This fund is run by Nuveen and its primary objective is "current income through investments in taxable municipal securities".

When 2023 was getting underway I was cautious on this particular investment. My followers know I was generally recommending to avoid leveraged CEFs (save for floating rate funds) because the inverted yield curve was hammering away at expenses. I saw NBB's forward outlook as not very bright as a result and, in hindsight, this was the correct assessment:

Fund Performance (Seeking Alpha)

In fairness, some of the macro-risks facing NBB remain present today. However, there are now enough positive attributes that I think the risk-reward proposition is quite favorable at these levels. Enough so that I believe a rating upgrade to "buy" is warranted. I will discuss each of the factors behind this decision in detail below.

Valuation Getting Enticing

The first metric that gets me excited is the fund's valuation. Back in April NBB looked attractive enough, with a discount to NAV above 4%. However, I saw other factors that outweighed that discount. Today, the difference is stark. The discount spread has widened to almost 9% on the open market - making me reluctant to overlook this compelling metric:

{kind=link}

NBB's Metrics (Nuveen)

Of course, a wider discount does not necessarily translate to forward gains. So understand this is just one aspect to consider. But it helps to understand that NBB's loss since my last review is almost entirely due to discount widening. While not "good" for prior investors, it really opens up an attractive opportunity for new money going forward. The fund's underlying securities have held up reasonably well, yet the fund is much cheaper today. That is a win-win in my book and central to supporting my rating upgrade.

Taxable Munis: Relative Value In Terms Of Income

A reminder on this particular fund is that it invests mostly in taxable muni securities. This is in stark contrast to tax-exempt offerings that I mostly write about. The taxable corner of the muni market is much smaller (although it has been growing) and options to buy in to it via CEFs is quite limited. NBB is one of just a few funds offering this exposure.

While taxable munis do not have the same tax benefits of their counterparts, there are reasons to buy them all the same. One is diversification. Another is that the absolute yield tends to be higher. This can often make them more attractive for those in lower tax brackets because the savings from tax-exempt securities may not be enough to cover the difference for those individuals. It all depends on one's personal income and unique circumstances.

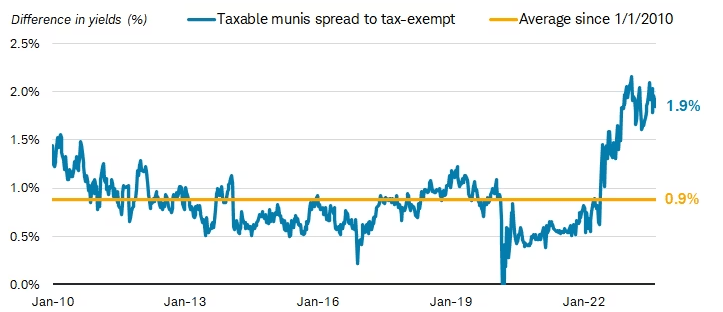

With this in mind, it is worth asking how taxable munis compare to tax-exempt munis at this juncture. Is there a case for buying one over the other right now?

Again, this is highly dependent on each individual, but a look at historical norms suggests the bull case is firmly in the court of taxables. This is because taxable munis are offering much higher streams of income by comparison - and this level is not only high in absolute terms but also when compared to the usual spread between the two over time:

{kind=link}

Historical Yield Spread (taxable munis vs. tax-exempt munis) (Charles Schwab)

What this boils down to for me is that taxable munis look quite attractive right now. History has a way of repeating itself and I would expect this spread to narrow to historical norms eventually - and probably sooner than later. This tells me the time is ripe to buy a fund like NBB, as it will benefit from a rotation in to the sector as investors realize the value. Buying in now will offer an opportunity to front-run this eventuality.

Distribution Has Held Steady

Another aspect I view positively is that NBB has held its distribution steady since my last review. Again, the inverted yield curve remains a major hurdle for this fund and all fixed-income leveraged CEFs. So I will not rule out the possibility of another income cut and urge readers to be well aware of this risk.

However, when I wrote about the fund in April it had experienced three income cuts in a short period of time. This was too much for me to bear and resulted in my cautious guidance. Fortunately, since that time NBB has kept the payout constant, a reassuring measure to say the least!

NBB's Distribution History (Nuveen)

Of course, we as investors want to generally have a longer history than that. I am not blind to this reality. NBB has faced significant income pressure and, with the yield curve inversion still at record levels, this pressure could continue:

{kind=link}

Treasury Yield Curve (CNBC)

The takeaway for me is this remains a mixed bag and should be treated as such. Still, four months ago the picture was very negative with three recent cuts so close together. Today, we are almost in September and the distribution has been steady during the past five payouts. This shows marked improvement and helps to support a more positive outlook.

Muni Issuance Is Low, Supporting Values

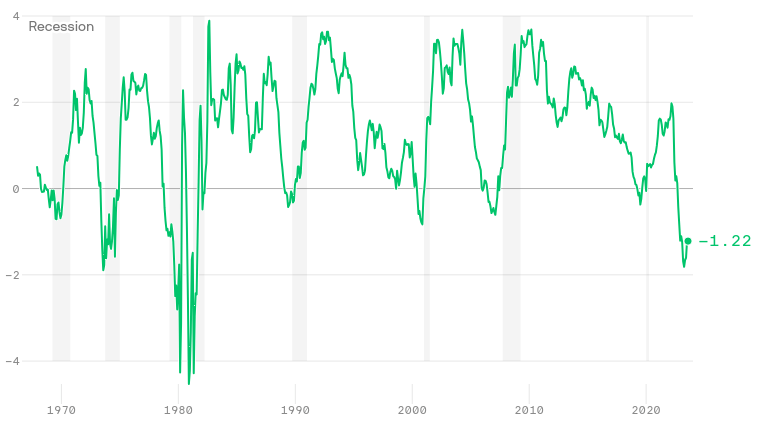

My next topic is a macro-one and relates to broader muni supply. This is relevant for both taxable and tax-exempt debt, as well as most funds that cover this space. So it is an important consideration for NBB, but just about any other muni fund by extension.

What I am referring to is the supply dynamic in this sector right now. Supply has dropped off sharply in the past few weeks and is expected to remain low for the time being:

{kind=link}

Muni Bond Sales (by week) (Bloomberg)

What this can do is boost underlying value of muni securities as long as demand stays constant (or increases). With supply tight, the number of securities available for purchase is low, prompting a natural supply imbalance based on week averages.

The conclusion I draw here is this is a favorable backdrop for munis heading in to Q4. This is likely to benefit NBB and is another reason why I like this fund more than I did earlier in the year.

NBB Is Cali Heavy, With Areas Seeing Uptick In Sales Tax Collections

Shifting back to NBB specifically, readers should bear in mind this fund is fairly top-heavy when it comes to state-specific weightings. California stands out in particular, representing almost a quarter of total fund assets:

NBB's State Allocation (Nuveen)

For this reason, one should be fairly bullish on California-focused munis before buying in to this fund - or at least not bearish on them!

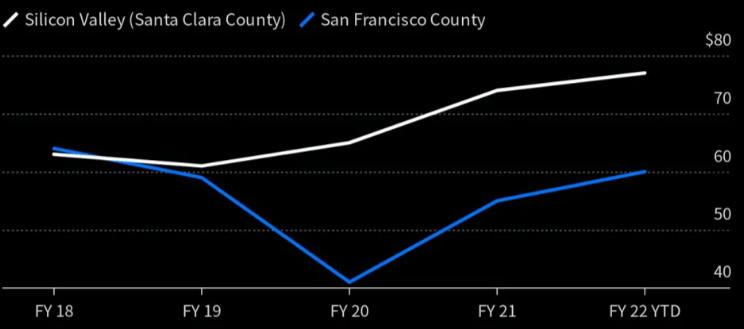

California is certainly a state that makes a lot of headlines and it can get easy to get lost in the noise (both negative and positive). But when it comes to muni investing we have to focus on facts. The state has seen a shift from a big surplus to a deficit, but it is taking action to limit the fallout going forward through some spending cuts . In addition, local tax collections has been on the rise since the worst of the lockdowns passed. This is a consistent story across multiple major metropolitan areas of the state:

{kind=link}

Per Capita Sales Tax Revenue (Yahoo Finance)

What I draw from this is that under the surface and the political headlines, states and local governments have been making progress. While keeping spending under control should hopefully be a focus going forward, local (city) tax collections are keeping pace with inflation. This bodes well for muni investors getting their interest payments timely and keeping any delinquencies minimal - as they have been in the past.

Bottom-line

NBB has had a tough go of things in 2023 and there are some headwinds to keep an eye on going forward. Leveraged funds face pressure from the yield curve and fixed-income more broadly could take a hit if the Fed keeps raising its benchmark rate.

However, I see multiple positives that suggest NBB has a brighter future ahead. The fund's discount to NAV has widened markedly, the distribution has been stable short-term, and taxable muni yields are historically high compared to their tax-exempt counterparts. That could bring in investor interest going forward. With all this considered, I see a rating upgrade as warranted here and will place a "buy" rating on NBB for now. This suggests readers should give the fund some consideration at this time.

For further details see:

NBB: A Few Reasons Why I'm More Bullish Going Forward (Rating Upgrade)