NBB - NBB: Still A Reasonable Option In 2023 But Income Cuts Hurt (Rating Downgrade)

2023-04-13 03:30:28 ET

Summary

- NBB has had a pretty strong 2023 so far and is in positive territory since my last bullish review.

- The fund did see an income cut in January, which was not a great sign. Then this month, we were hit with another cut announcement. This makes me less bullish on the fund.

- Still, the broader muni sector has its advantages. So there is merit to monitoring this fund. But I would be very selective with entry points and/or look elsewhere for more value.

Main Thesis & Background

The purpose of this article is to evaluate the Nuveen Taxable Municipal Income Fund ( NBB ) as an investment option at its current market price. This fund is run by Nuveen and its primary objective is "current income through investments in taxable municipal securities."

It has been a while since I wrote about NBB. But when I last did, about ten months ago, I was bullish on the fund. The good news is it has indeed performed well since that time:

Fund Performance (Seeking Alpha)

With Q2 underway, I thought now was a good time to take another look at this fund. This is especially true given the recent distribution cut announcement that came out last week. On the backdrop of this, and other factors, I think the time is ripe for a rating downgrade on this fund. Therefore, I am in a "hold" state of mind for NBB, and will explain why below.

Income Cuts Galore

To start the review let's discuss income. This is a key consideration when evaluating any muni play - especially a leveraged one like NBB. With a current market price yield near 5%, it seems like a good option. While some savings accounts can rival this at the moment, NBB offers the potential for capital appreciation too. So there is logic to buying it.

The problem is this 5% mark is not especially comforting given the short-term history of the distribution. To start off April there was a distribution cut and, while modest, it is the third cut in less than a year:

Recent Income Cuts (NBB) (Nuveen)

Quite frankly this is a terrible history for a CEF. The fund managers overseeing NBB have not done a very good job at managing leverage, the inverted yield curve, and the broader muni backdrop. While those factors all pressure what the fund is able to pay, we have to also consider that higher rates keep refinancings low, which means the underlying bonds are still offering income streams at a constant rate. The fact NBB has seen consistent cuts means other factors - like leverage costs and management expenses - are eroding the income. That is not something I am impressed buy.

For this reason alone I find it hard to rate this fund a buy. While three income cuts in such a short time period suggests the worst is probably over, I would have said the same after the second one in January. The fact is the yield has been punished to a level where I really need to see other compelling reasons to buy this one besides the yield. At the moment, I'm just not there.

Valuation A Mixed Bag

I will now turn to the fund's valuation - always a critical element when evaluating any CEF. On the surface, this may seem like a screaming buy. The fund sits with a discount to NAV in excess of 4%. This is generally a good sign:

Current Valuation Metrics (Nuveen)

{kind=link}

In addition, this price trades favorably to its closest competitor, the BlackRock Taxable Municipal Bond Trust ( BBN ). At time of writing, this CEF sits with a discount to NAV just under 3%:

{kind=link}

So NBB is cheaper and has a sharp discount on the surface. What's the problem? There is no real "problem", as these metrics do speak favorably. But the reason this is not an outright buy signal to me is that NBB often trades for even cheaper prices. So patient investors, if they remain patient now, may actually be able to get this fund even cheaper than its current price. There is no guarantee, of course. But for perspective consider NBB had a discount just under 8% when I wrote about it last June. That's a much wider than it is now and hopefully illuminates readers on a reason why I am leaning towards a "hold" on this fund, rather than a buy.

Compared To Corporate & Treasuries, Munis Look Good

I have so far laid out a couple reasons why I am less than enthusiastic about NBB right now. But I continue to have a positive outlook on the broader muni sector. This is not meant to be contradictory. I tend to like munis over time, including now, especially in relation to their taxable counterparts in the corporate and government (treasury) sectors. I own very little corporate debt and zero treasuries, but munis have been and continue to be a fundamental part of my portfolio.

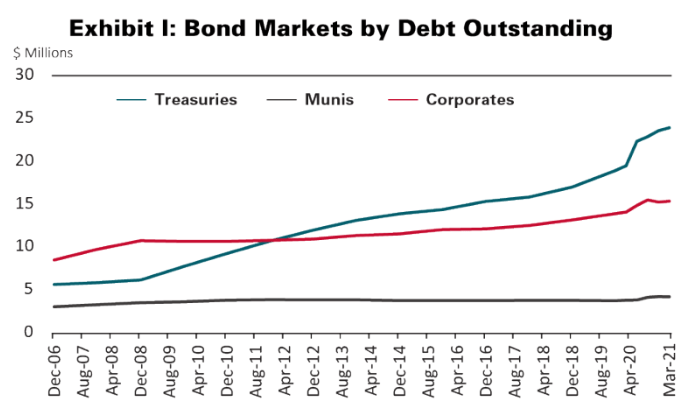

There are multiple reasons for this which I have discussed at length over the years in my reviews. One point to highlight that makes this sentiment relevant today is that state and local governments have been more prudent with borrowing than U.S. corporations and the federal government. This has kept the size of the sector more stable than corporate and treasury debt markets, which is an attribute I find appealing:

Debt Outstanding (By Sector) (Federal Reserve)

{kind=link}

I bring this up because investors have plenty of options when it comes to taxable bond funds. NBB is fairly unique in its taxable muni approach but, as the graphic above illustrates, this may give investors exposure to a sector that is fundamentally less risky.

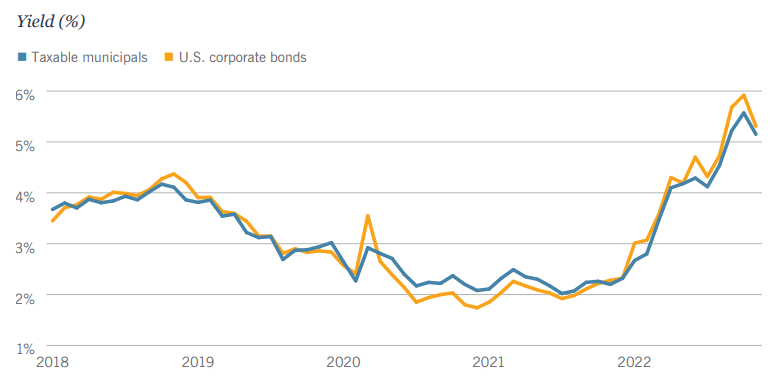

The distinction to make here is that often more risk means higher yield. But in the relative case of taxable munis versus corporates and treasuries, investors aren't sacrificing yield by taking a more conservative approach. The sector yields for taxable munis and taxable corporates have been generally the same for years:

{kind=link}

What I am getting at here is the backdrop for taxable munis is stronger than alternative sectors and the yield is the same. This extends to NBB as the fund is comprised almost entirely (about 90%) of investment-grade debt:

NBB's Credit Ratings (Nuveen)

I use this to amplify that I am not bearish on munis nor NBB. While I don't love positions at this level, there is plenty of merit to holding this fund and/or keeping in on the radar.

An Option For Those Worried About Equities

Another reason for taxables to be a part of one's portfolio is the role they serve as diversifiers. While the correlation with corporates is high, taxable munis have a fairly low correlation to most other sectors:

Taxable Muni Sector Correlations (Morningstar)

This really speaks to the resiliency of the sector and the stability of revenue streams when other areas face downturns. Taxable munis often are backed by projects that support essential services (i.e. utilities, hospitals, education, water systems, etc.) and are not prone to massive swings in revenue as a result. This makes NBB less economically sensitive and a play for someone who is worried about a recession and equity market volatility.

Bottom-line

I will continue to monitor taxable municipals and that includes NBB. I have liked the fund in the past but there are a few attributes that give me pause here and I will wait for a more compelling opportunity. Aside from the income cuts and the narrower discount than last year, readers should take note that NBB is very concentrated in just a handful of states. This concentration risk is something investors should weigh against their other holdings to ensure they are comfortable with the exposure before buying:

NBB's State Allocation (Nuveen)

On this note, I think it is clear I am no longer bullish on this fund. That could change at some point later this year, but for now a "hold" seems appropriate. As a result, I would suggest my followers approach this fund selectively going forward.

For further details see:

NBB: Still A Reasonable Option In 2023, But Income Cuts Hurt (Rating Downgrade)