ECF - NCV And NCZ: Discounts Narrow For Both But One Looking More Appealing

Summary

- NCV and NCZ have seen their discounts narrow from the wide discount we saw several months ago.

- NCZ presents a potentially better opportunity with a larger discount compared to NCV.

- Both of these funds carry some elevated leverage levels, but the recovery in the broader market since our last update has helped these funds rebound.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on February 22nd, 2023.

Virtus offers a platform of several convertible-focused funds that are managed by Voya, which were previously managed by Allianz. Two of these could be considered sister funds, with nearly identical investments leading to similar performance results. That would be the Virtus Convertible & Income Fund (NCV) and Virtus Convertible & Income Fund II (NCZ).

These funds also had a bit of their own drama last year, with NCZ delaying their distributions due to being over the leverage limit. They both utilized preferred for leverage, and NCZ breached the 50% limit of leverage. NCV was flirting with the limit level but didn't have the same delay. Despite that, NCV simultaneously deleveraged anyway. As they were quite close to breaching the limit, it seemed to make sense.

We discussed more of that topic recently, but a good reminder of just how leveraged these funds are and what sort of negatives can happen during bear markets.

Today, I wanted to highlight a potential opportunity for investors that want to invest in these funds, despite their potential risks. A difference in valuation provides for a swap opportunity.

The Basics

NCV Basics

- 1-Year Z-score: 1.90

- Discount: 2.85%

- Distribution Yield: 13.60%

- Expense Ratio: 1.35%

- Leverage: 42.29%

- Managed Assets: $680.251 million

- Structure: Perpetual

NCV's objective is to "seek total return through a combination of capital appreciation and high current income."

To achieve this, the fund will "invest in a diversified portfolio of domestic convertible securities and high-yield bonds rated below investment grade." They add that "at least 80% of its total assets in a diversified portfolio of convertible securities and non-convertible income-producing securities and seeks to invest at least 50% of its total assets in convertible securities, but determines its allocation based on changes in equity prices, changes in interest rates, and other economic and market factors."

NCZ Basics

- 1-Year Z-score: 1.15

- Discount: 8.45%

- Distribution Yield: 14.33%

- Expense Ratio: 1.40%

- Leverage: 42.50%

- Managed Assets: $638.41 million

- Structure: Perpetual

NCZ's investment objective is to "seek total return through a combination of capital appreciation and high current income."

To achieve this, the fund will "invest in a diversified portfolio of domestic convertible securities and high-yield bonds rated below investment grade." From there, they also include the parameter that they will "invest at least 80% of its total assets in a diversified portfolio of convertible securities and non-convertible income-producing securities and also seek to invest at least 50% of its total assets in convertible securities, but determines its allocation based on changes in equity prices, changes in interest rates, and other economic and market factors."

As we can see, the investment objective and the investment policy to achieve that are copy-paste of each other. That's how we end up with such similar portfolios when the same manager runs them.

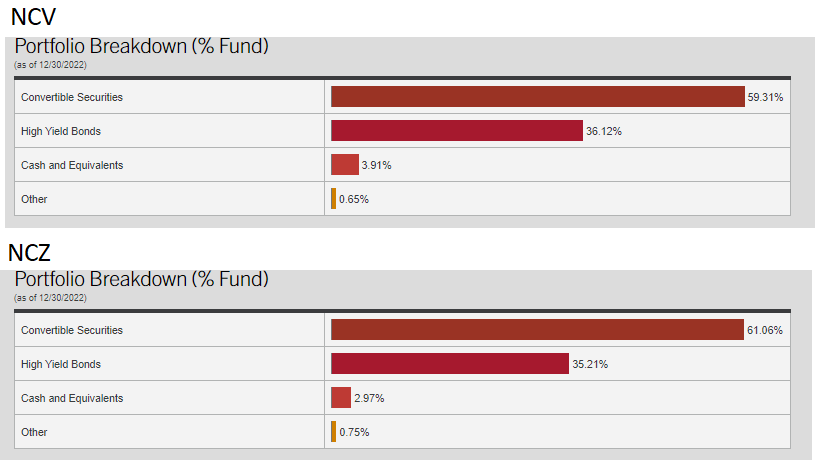

The breakdown of their portfolio stands nearly identical. Convertible securities make up the majority of their underlying holdings, with high-yield bonds also making up a meaningful allocation.

NCV/NCZ Portfolio Breakdown (Virtus)

{kind=link}

Leverage Discussion

This remains one of the key factors and key risks for these funds. There have also been a lot of moving levers here with these funds, so breaking it down in their own section for both of these funds is important.

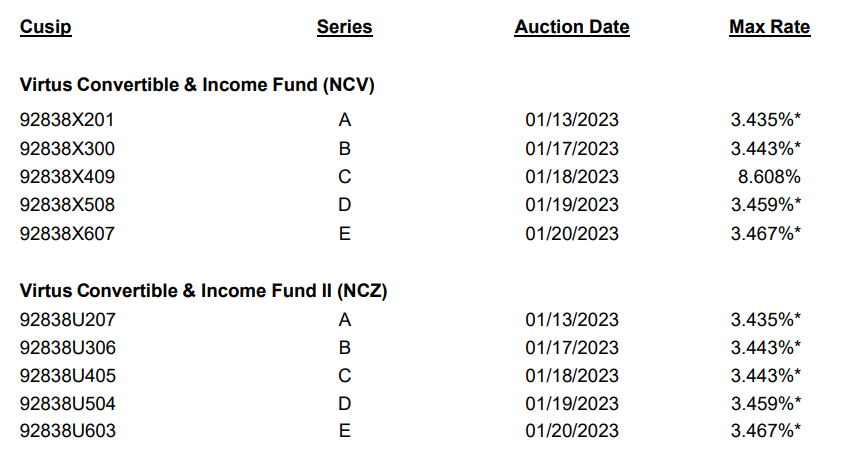

Since our last update, they've continued to reduce their auction rate preferred leverage by redeeming the rest of the preferreds that were outstanding.

NCV/NCZ Redeeming ARPS (Virtus)

The final redemption date for all of their preferred leverage was set to be January 27th, 2023, as we've seen listed above.

However, each fund has still retained the Series A Cumulative Preferred Shares. This series of preferred can be more ideal than the ARPS during a time when interest rates are rising as they are fixed costs. However, the fixed rate for NCZ is 5.5%, and for NCV, they are 5.625%. When interest rates were low, or if they ever reach lows again, this would be considered expensive.

For those interested, the preferreds are publicly traded as well; 5.625% Cumulative Preferred Shares ( NCV.PA ) and 5.5% Cumulative Preferred Shares ( NCZ.PA ). Both of these become callable in September 2023 (the 20th for NCV and the 11th for NCZ.)

Perhaps more interestingly, is that the last of the ARPS showed us that the max rates on most of these were still cheaper than these fixed-rate costs except for the Series C for NCZ.

{kind=link}

Additionally, they were also quick to increase their borrowed debt to offset the ARPS they were redeeming. This isn't necessarily bad as it means they stay invested, but it was replacing one variable rate form of leverage for another. A benefit can be that going forward, borrowings are more flexible. They can reduce borrowings quicker than preferreds would allow going through the redemption process.

Through March 31, 2022, interest was charged at 3-month LIBOR plus an additional percentage rate on the amount

borrowed. Effective April 1, 2022, interest is charged at the Overnight Bank Funding Rate plus an additional percentage rate on the amount borrowed.

For the period ended July 31, 2022, the weighted average daily balance outstanding was $25,000 at the weighted average interest rate of 1.85%. With

respect to the margin loan financing, loan interest expense of $229 is included in the Diversified Income & Convertible Fund's Statement of Operations.

The average borrowings might have been 1.85% throughout their semi-annual report period, but the actual interest rate at the end was 2.64%. That was also all the way back in July 2022; interest rates have only risen even further, which means these costs are increasing.

Ycharts

Overall, here's a look at the total breakdown for NCV's total capital structure:

NCV Capital Structure (Virtus)

{kind=link}

Here is the breakdown for NCZ:

NCZ Capital Structure (Virtus)

{kind=link}

Which still means that their leverage overall remains quite elevated. Thanks to a strong rebound in the markets since the October lows of 2022, that certainly helped too.

The Opportunity For A Swap

We last covered NCV in October; since then, the fund has done quite well in terms of returns. The discount at that time was sitting at just over 10%.

NCV Performance Since Prior Update (Seeking Alpha)

It has been quite some time since I've touched on NCZ, but we've seen similar results. In fact, it looks like NCZ's results have been a touch better than NCV's.

Ycharts

Helping to drive those results was the discount now narrowing to around 2% for NCV since our prior update. At the same time, NCZ's discount came in at a whopping 16.38% on the closing for that same day. At the same time, NCZ's discount is still wider than NCV's for now, and that is what could be creating the opportunity for a potential swap.

Perhaps worth noting, though, is that both funds are trading below their long-term historical average. This can often indicate that a fund could be ready for mean reversion. That being said, I believe these are riskier funds being highly leveraged.

If we look back at the historical performance of the funds. We can see that, ultimately, the total NAV returns of these two are quite similar. That's what presents the perfect opportunity for swap pairs - as one shouldn't expect to see their underlying portfolio significantly deviate in terms of total results. Thus, allowing closed-end fund investors to exploit the opportunities between discount/premium valuations.

Ycharts

Distributions Looking Enticing, But Stretched

Despite needing to deleverage throughout last year, these funds have maintained their elevated distributions.

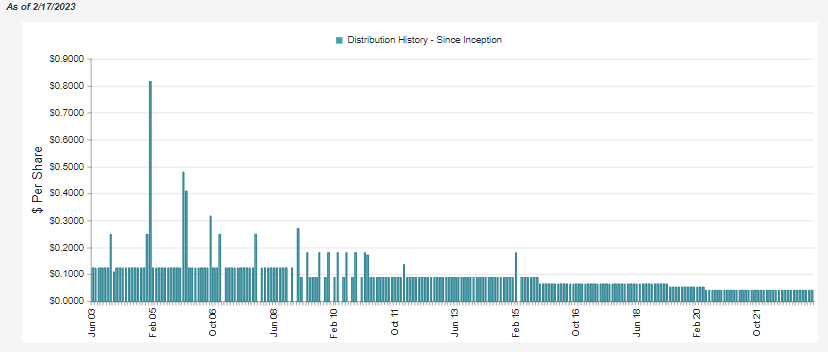

NCV carries a 13.60% distribution yield on share price and 13.21% based on the NAV.

NCV Distribution History (CEFConnect)

{kind=link}

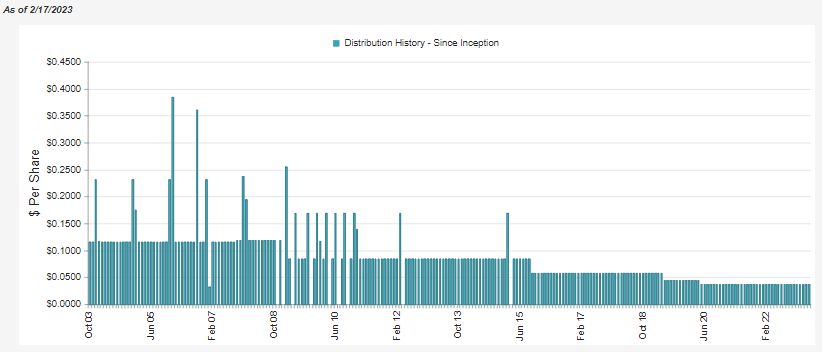

NCZ gives us a similar elevated distribution yield at 14.33%. However, that's thanks to the slightly larger discount. The actual NAV rate comes in closer and is actually a touch lower at 13.12%.

NCZ Distribution History (CEFConnect)

{kind=link}

As we can see, historically, both of these funds have cut their distributions but haven't elected to do so at this time despite the volatility we've experienced. Generally, the larger the yields, the more these funds can generate interest, and that's what can provide shifts in their discounts/premiums.

By maintaining these distribution levels, it's likely being priced in by these narrowing discounts. However, that can be one of the additional risks. When funds cut their distributions, we can see their valuations drop. We've seen that be the case with these funds.

Each cut brought the discount/premium down quite dramatically. Although investors eventually started pooling back in during the 2016-2019 period, the correlation is mostly quite apparent. Cut happens, value drops.

Conclusion

NCV is trading at a richer valuation and has rebounded significantly since our last update. They are providing outsized distribution rates with high leverage; those are the main risks going forward for these two. Still, NCZ now presents a fairly interesting alternative if one wants to remain invested in one of these sister funds. A slightly lower discount could present a bit more downside protection.

If you aren't concerned with the upfront yield, I believe that Ellsworth Growth and Income Fund ( ECF ) and Bancroft Fund ( BCV ) in the convertible space remain more interesting convertible plays.

For further details see:

NCV And NCZ: Discounts Narrow For Both, But One Looking More Appealing