NLLSY - Nel ASA: Higher Execution Risks

2023-03-23 21:54:56 ET

Summary

- Largest projects also mean higher execution risks.

- The company is still unprofitable with an unsuccessful track record.

- Nel ASA is still priced at a premium valuation and we still believe that consensus downgrades are still likely.

Nel ASA (NLLSF) (NLLSY) is a company that we closely follow and here at the Lab, we are still waiting for The Turnaround Moment . In our previous publication, we emphasized many times the following statement: " Revenues up. Costs up. When will this end? " And also, we reported our negative comments on how 1) the former Nel ASA's CEO and current board member Jon Lokke disinvested almost 75% of their stocks during 2022, 2) given the current cash burn, we are forecasting an additional equity raise and 3) we were lowering Nel ASA's average selling price by almost 30%, forecasting a break-even EBITDA point in 2026 from the previous estimates in 2025. Today, we would like to report additional risks to take into account.

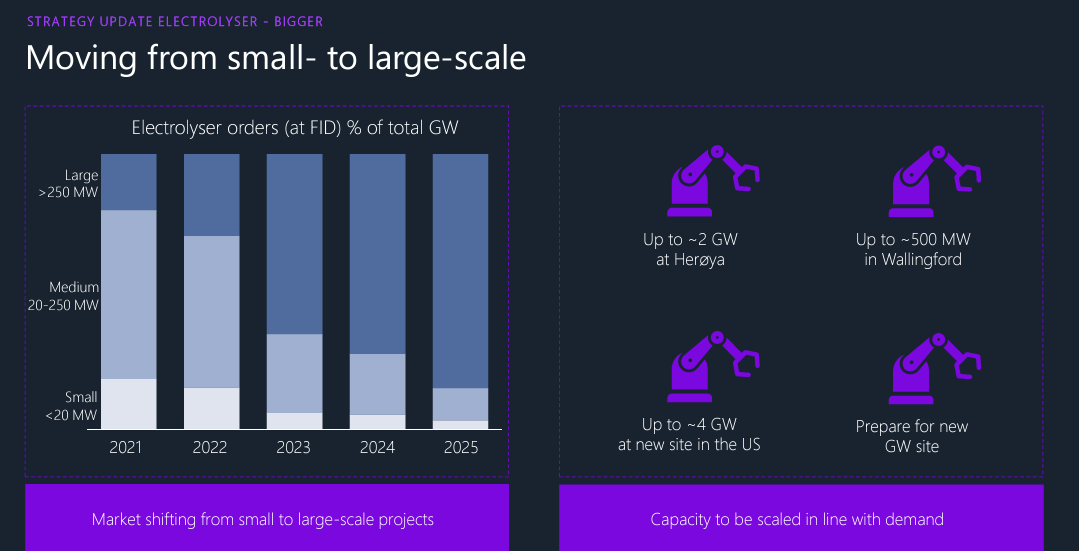

Although the company has delivered solid order book momentum in the last 2022 two quarters, which may have led to Wall Street optimism on the company outlook, our internal team still highlights that our Norwegian hydrogen player is in its infancy and there is a high risk of business execution on their scale-up. At the moment, Nel ASA's largest project was an electrolyzer of ~20MW, and investors should have confidence that the company can deliver a project ten times this scale by 2024.

{kind=link}

Looking at the company's press release, Nel ASA's EBITDA reached NOK -216 million from NOK -168 in Q4 2021 and was mainly due to higher losses in the fueling division and low margins on electrolyzer projects signed in the 2020-2021 period. Despite that, during the year, we should report that the company increased its personnel costs to prepare for large-scale projects. As a reminder in Q3, the company disclosed " execution issues ".

In Q4, Nel disclosed a joint agreement with General Motors (GM) and signed two additional contracts with Statkraft and Woodside Energy. However, we should also report another risk, in Q3, the company secured a record size 200 MW order from a US client but is still undisclosed (as a reminder, this is the biggest contract for Nel ASA).

{kind=link}

Additional risks include clients' projects delay or final investment decision pushback. This might delay Nel ASA's top-line sales recognition in 2023 and also in 2024 estimates. Aside from the 200 MW undisclosed US order, two clients now account for approximately 50% of Nel ASA backlog. Even though the company is trading at a higher price from the October low, we still believe that consensus downgrades are still likely.

Last time, we downgraded our internal estimates and we believe that EBITDA will not materially improve in the current year. The company will continue to execute lower-margin contracts in the Electrolyser division and the Fueling segment was recently impaired by NOK 31 million. In addition, the company's margins were also impacted by a lower product mix.

Valuation and Conclusion

At year-end, the company had a record-high backlog of approximately NOK 2.61 billion and was up 112% on a yearly basis, and 24% up versus the Q3 end. Despite that, Nel is trading at >10x its 2024 EV/sales compared to its peers such as De Nora at 2x. Last time, we already downgraded our target price to NOK 12 per share ($35 in ADR) and we continue to believe that it is a fair estimate for the next twelve months. The current stock price would require the company to take more than 20% of the electrolyzer market by 2050 and we believe it is unachievable. Aside from De Nora, we also like Ceres Power which is trading at a premium compared to Nel, but given its asset-light business model should reach a better EBITDA margin. Regarding Nel, here at the Lab, we remain cautious and we forecast a capital increase by 2024.

For further details see:

Nel ASA: Higher Execution Risks