NRDY - Nerdy Stock: Q2 Results Make The Honor Roll

2023-08-21 17:25:08 ET

Summary

- Nerdy reported its Q2 results highlighted by strong operational momentum and firming margins.

- The introduction of a new subscription product has helped drive stronger financials and keep students engaged for longer.

- We are bullish on the stock and expect shares to climb higher.

Nerdy, Inc. ( NRDY ) is penciling in an impressive turnaround with shares nearly doubling this year. The online learning platform recognized by its "Varsity Tutors" brand connecting students with live one-on-one classes has found success with the addition of new learning formats and even AI tools.

We last covered the stock back in 2022 highlighting the company's "learning platform-as-a-service " model which we believe represents a significant long-term growth opportunity. Indeed, a key development has been the introduction of a new subscription product working to keep students engaged for longer while driving stronger financials.

Nerdy's latest Q2 report confirms the trend of solid operational momentum and firming margins. Our update today reaffirms a bullish view on NRDY with an expectation for more upside going forward.

NRDY Q2 Earnings Recap

The first point here is that Nerdy remains technically unprofitable given its ongoing investment spending. That said, the underlying trends are moving in the right direction.

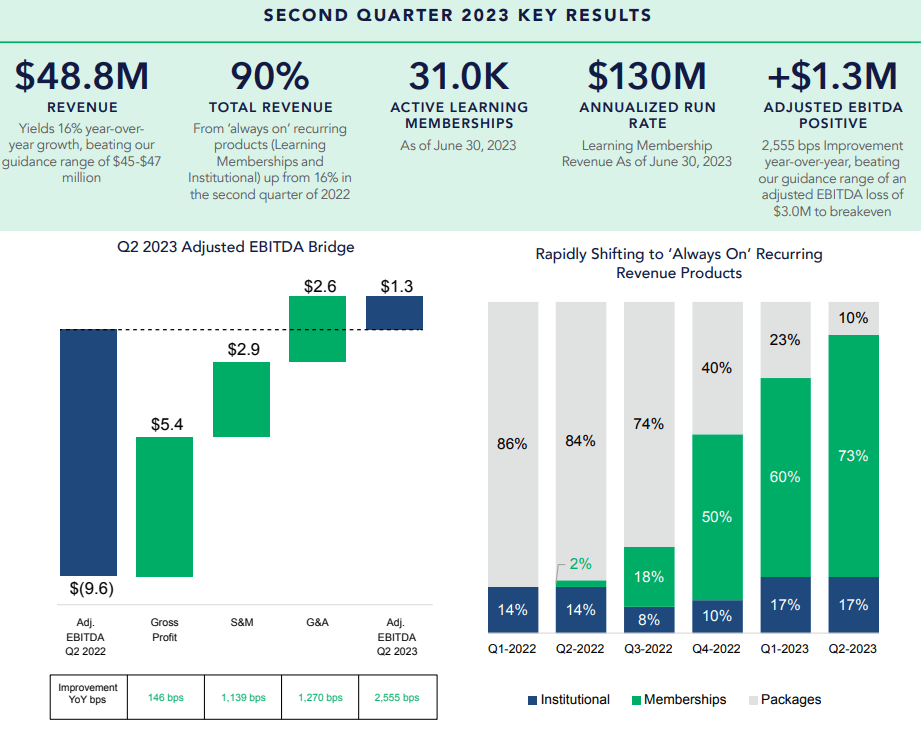

NRDY reported a Q2 GAAP net loss of -$5.5 million including $10.1 million in stock-based compensation expense. More importantly, the adjusted EBITDA reached $1.3 million, reversing a loss of -$9.6 million in the period last year, also coming in above previous management guidance.

Revenue of $48.8 million climbed by 16% year-over-year which reflects the ongoing shift into the "Always On" subscription model, which is essentially the membership where students get access to the full learning tools with an allocated number of personalized tutoring hours per month.

{kind=link}

For example, quoted packages for high-school students range between $199 to $579 per month compared to the previous system where Nerdy was simply charging per hour of tutoring. There are also plans for college-level and professional certificates. Separately, Nerdy secures deals with school districts for supplemental learning like test-prep and after-school programs.

The proportion of revenue based on memberships has reached 90% between institutional and consumer segments compared to 50% to just 16% in Q2 2022.

The result here is that the gross margin at 69.8% is up from 68.2% in the period last year with the new cohort of members setting up a growth run expected to continue going forward.

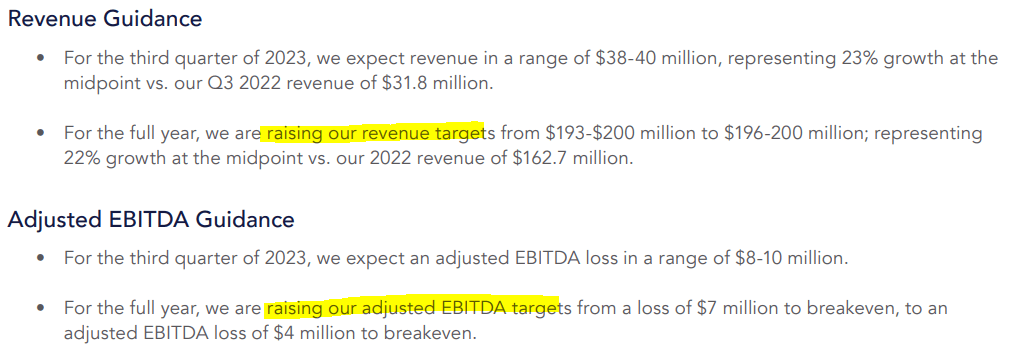

Looking ahead, based on the stronger-than-expected operating trends from Q2, management is raising its full-year guidance. Nerdy now expects 2023 revenue between $196 to $200 million representing an increase of 22% over 2022. The company is narrowing the range of its adjusted EBITDA target from a loss of -$7 million to breakeven, to an adjusted EBITDA loss of -$4 million to breakeven. This compares to an adjusted EBITDA loss of -$36 million in 2022.

Finally, we note that the company ended Q2 with $91 million in cash against effectively zero debt. We believe the balance sheet liquidity position represents a strong point in the company's investment profile.

{kind=link}

What's Next For NRDY?

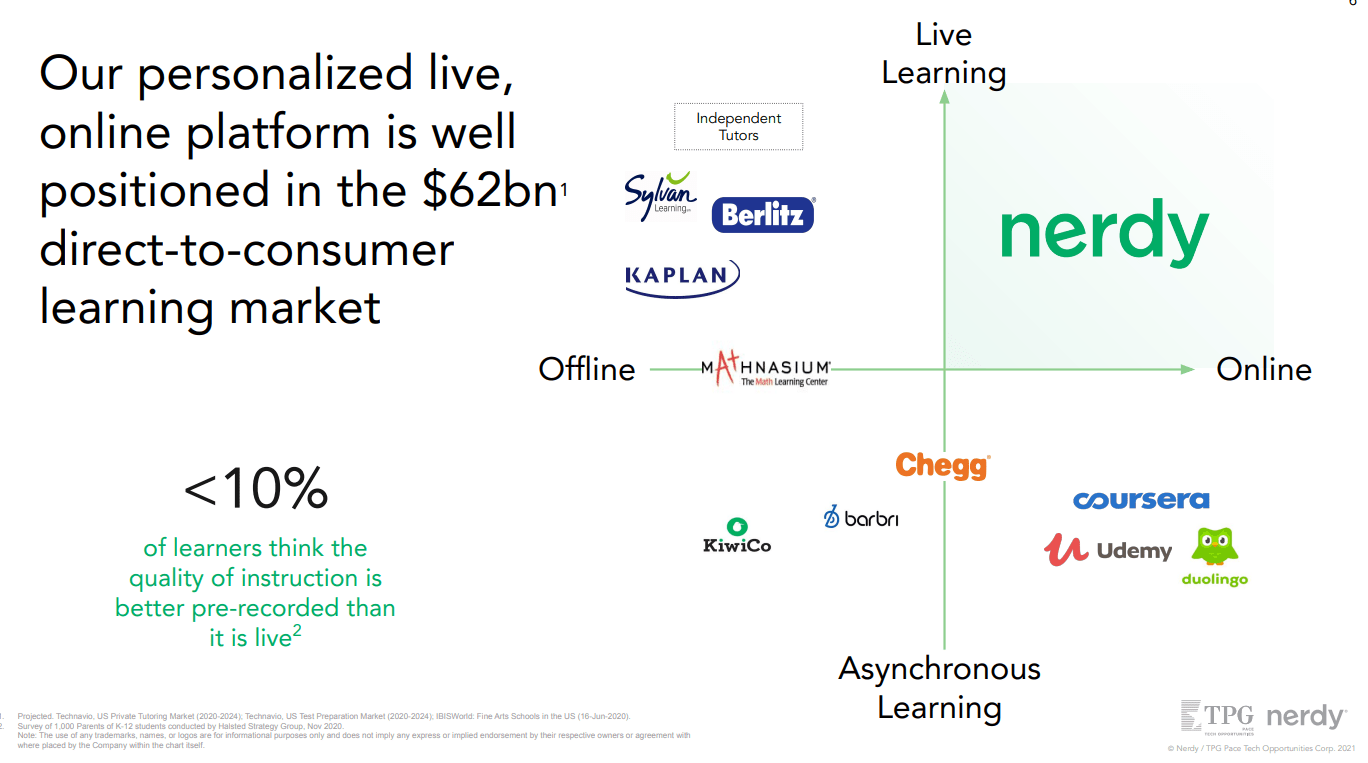

What we like about Nerdy and Varsity Tutors, in particular, is its unique market positioning and differentiated system. The live learning model counts on a network of 10,000 active "experts" that operate through a marketplace model allowing vetted tutors and teachers to generate income as a "gig" or part-time self-employment.

Over time, Nerdy can identify the top-performing experts while cutting off weaker instructors adding to the quality of the platform overall. The company shares data that this type of format leads to both better subject understanding and higher levels of satisfactio n by students.

This is in contrast to alternative learning platforms like Chegg Inc ( CHGG ), Coursera Inc ( COUR ), and Udemy Inc ( UDMY ) which focus more on "pre-recorded" courses. It depends on the subject, but the tutoring process is compelling, especially for primary-grade and college-age students that often benefit from one-on-one attention.

{kind=link}

The reason this is important is that Varsity Tutors has built a loyal following with name recognition in the segment with an expectation that current students will stick to the program throughout their academic journey. We believe there is room to grow the number of active learners with a future international expansion as an untapped market.

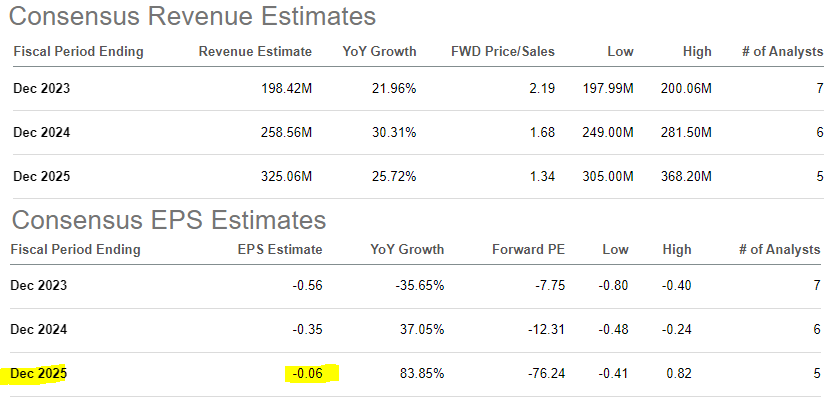

According to the consensus, the market forecast is for top-line revenue growth to average above 25% annually over the next two years. From an EPS loss estimate of -$0.56 this year, the market sees that there is room to approach breakeven with an EPS estimate of -$0.06 by 2025.

The bullish case here is simply that NRDY can reach sustained profitability, sooner rather than later, with further operating and financial momentum working as a catalyst for the stock.

{kind=link}

In terms of valuation, we view NRDY as attractively priced trading at an EV to revenue multiple under 2x. While this level is broadly in line with the segment peers we mentioned like CHGG, COUR, and UDMY; NRDY stands out with stronger expected growth this year and in 2024.

NRDY Stock Price Forecast

Following a difficult period for the company amid the post-pandemic slowdown last year, we sense that Nerdy is finally hitting its stride with a credible strategy backed by good financial execution. In our view, this is an education segment category leader, and we expect the company to continue growing and remain relevant over the long run.

We rate shares as a buy with a price target for the year ahead at $6.00 per share, representing a sales multiple of 2.5x on the current 2023 revenue guidance. In our view, the company's path to profitability alongside its solid balance sheet should support an expansion of valuation multiples.

On the downside, keep in mind that the stock remains speculative given the negative free cash flow and uncertainties of the outlook beyond the next few quarters. This means that shares will likely continue to exhibit volatility and be exposed to any negative headlines impacting its growth opportunity.

The risk here is that results disappoint forcing a reassessment of the earnings outlook, opening the door for a repricing of shares lower. The key metrics to watch include the level of active learners every quarter along with the progress in driving margins and adjusted EBITDA higher.

{kind=link}

For further details see:

Nerdy Stock: Q2 Results Make The Honor Roll