MDV - Net Lease REITs: Fighting The Fed

2023-09-28 09:00:00 ET

Summary

- Net Lease REITs - one of the most "bond-like" and interest-rate-sensitive property sectors - have lagged in recent months as investors come to grips with a potential "higher-for-longer" interest rate environment.

- Thriving in the "lower forever" environment, the industry has been reluctant to acknowledge the higher-rate regime, keeping private-market values and cap rates surprisingly "sticky" and resulting in compressed investment spreads.

- Despite the tighter investment spreads, acquisition activity has slowed only modestly for some REITs - paying top-dollar for recent purchases - a strategy that could prove costly if rates remain elevated.

- Strong balance sheets and limited variable rate debt exposure had afforded these REITs the ability to be patient until the price is right. While some REITs have exhibited prudence, others have initiated seemingly impulsive pivots, discarding decades of hard-fought progress.

- Don't Fight The Fed: We continue to see the best value in REITs that focus on “middle-market” tenants and the middle-tier of cap rates where inflation-hedging lease structures and initial yields grant more breathing room for higher financing costs.

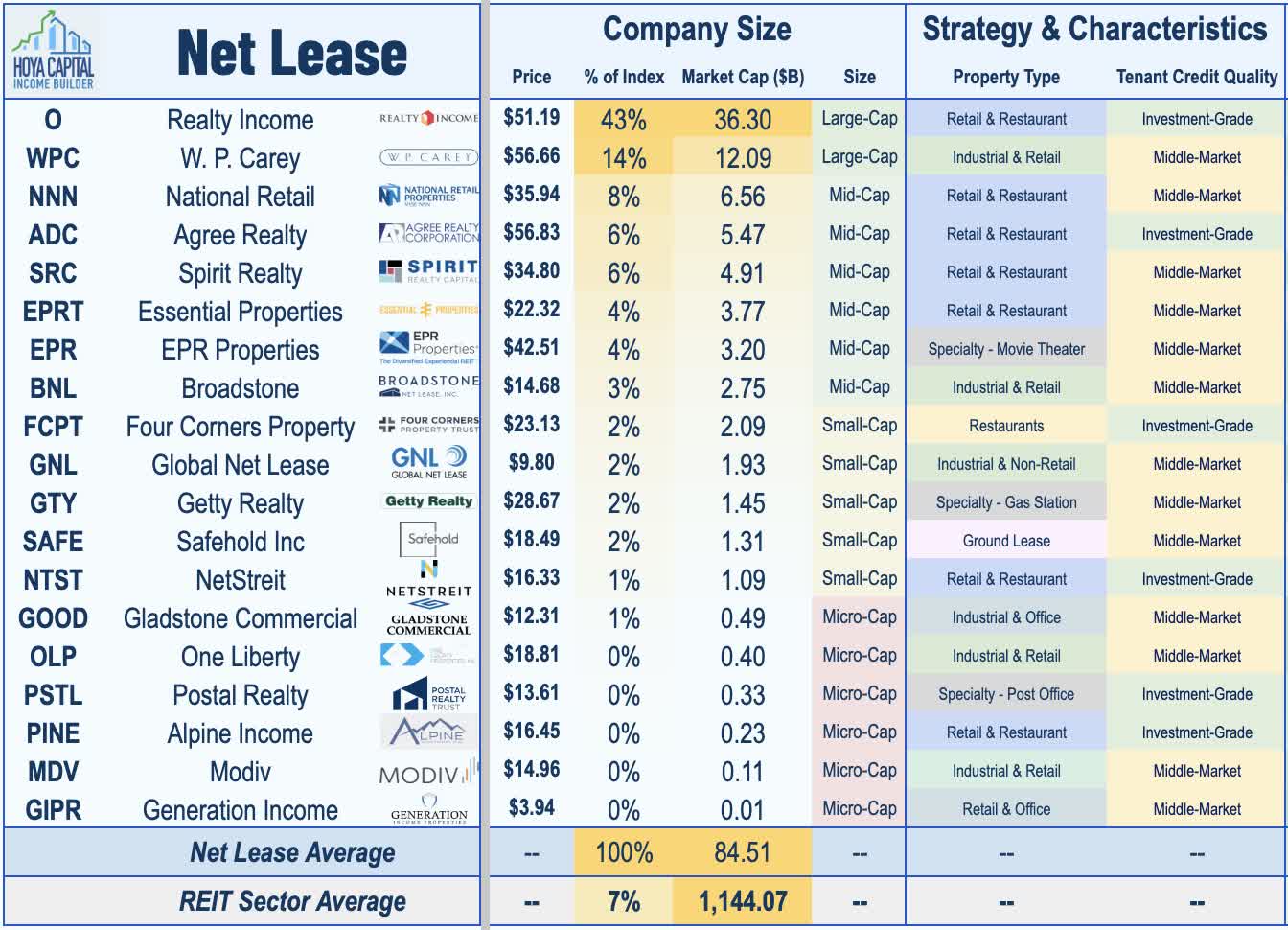

REIT Rankings: Net Lease

{kind=link}

Within the Hoya Capital Net Lease Index , we track the eighteen net lease REITs and one ground lease REIT, which account for roughly $100 billion in market value. These net lease REITs generally own single-tenant properties leased to high credit-quality tenants under long-term leases, focused primarily on retail, restaurant, and industrial properties. Historically one of the more interest-rate-sensitive property sectors, the net lease had surprisingly been among the best-performing property sectors in early 2023 amid signs of receding inflationary pressures and expectations of a pending pivot but have slumped in recent months amid a resurgence in benchmark yields through fresh multi-decade highs, raising fresh questions about how the industry will adapt to a potential "higher for longer" interest rate regime.

{kind=link}

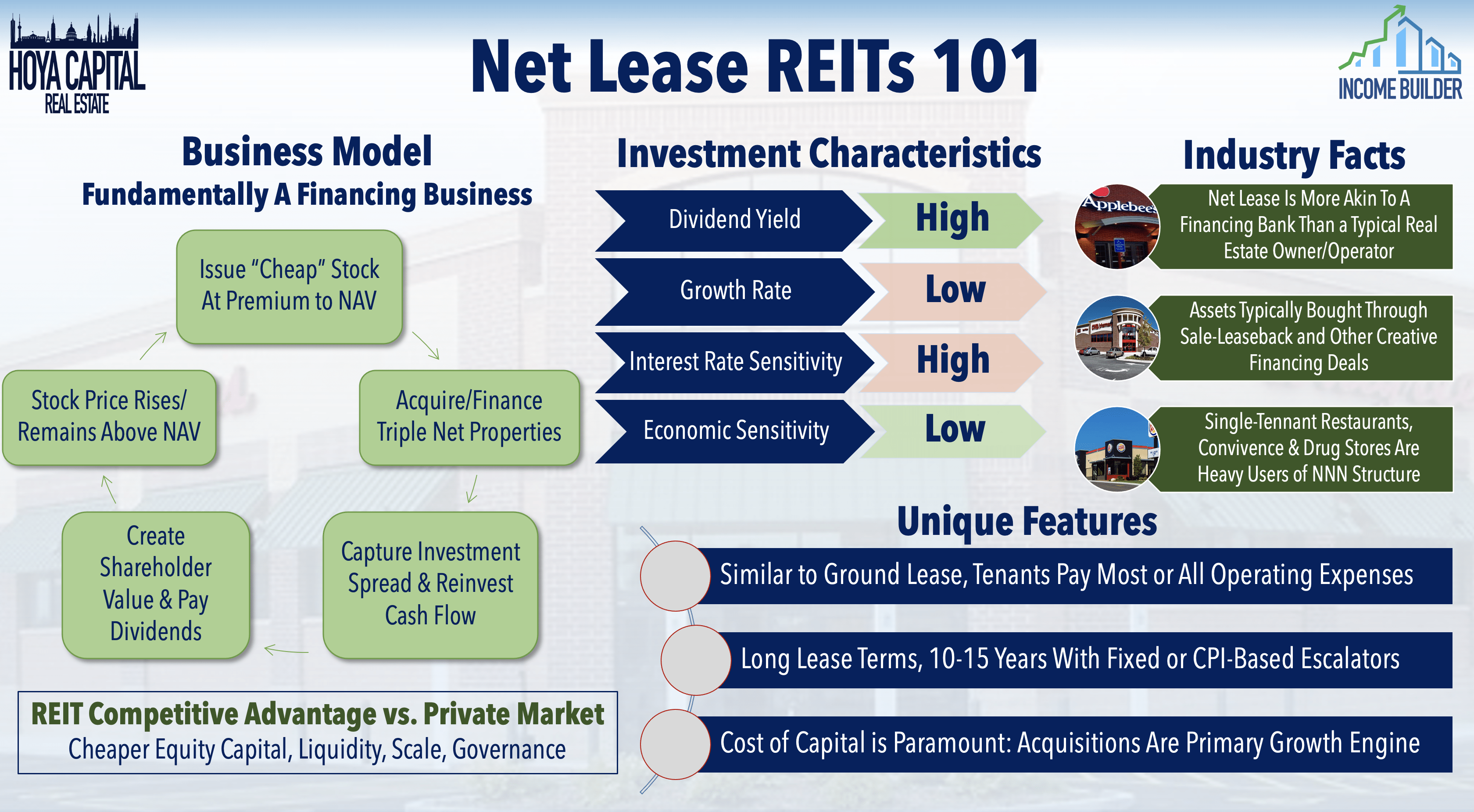

"Net lease" refers to the triple-net lease structure, whereby tenants pay all expenses related to property management: property taxes, insurance, and maintenance - a structure similar to a ground lease. As a result, net lease REITs tend to operate more like a financing company than a property manager, effectively capturing the spread between the acquisition capitalization rate ("cap rate") and their cost of capital. Net lease REIT investment characteristics are similar to corporate bonds due to the long-term nature of leases and the underlying "credit" exposure through their tenants' ability to pay rent. Unlike corporate bonds, however, net lease REITs have the ability to grow distributions through a combination of organic (rent escalations) and accretive external growth (acquisitions). Lease terms average 10-15 years and typically include fixed-rate contractual rent escalations at 1-2% per year.

{kind=link}

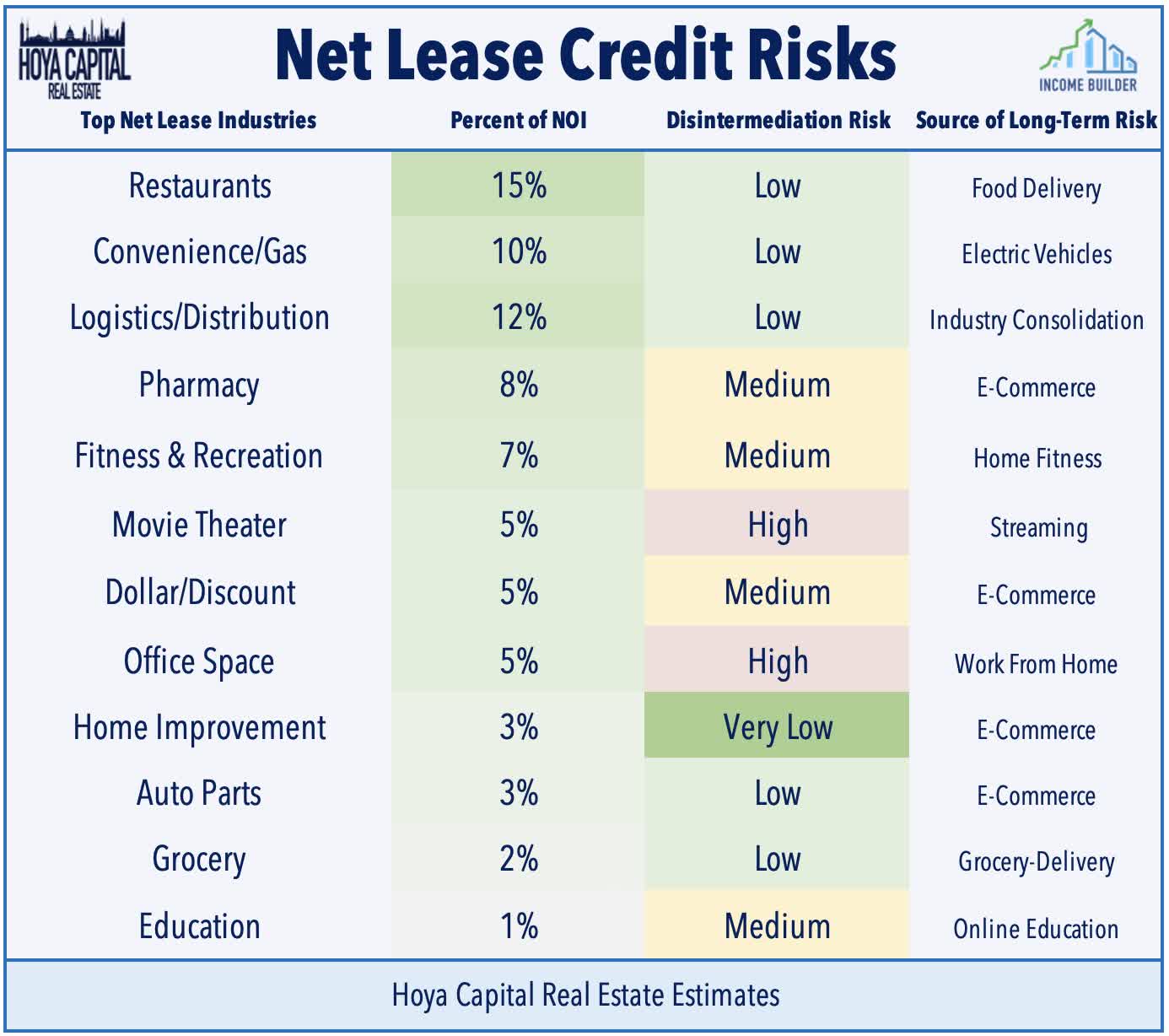

Triple net leases are used to varying degrees across the REIT universe - including the Casino and Healthcare REIT sectors - and proved to be particularly durable throughout the pandemic-related turmoil regardless of the headwinds endured by their tenants. While nearly every property sector uses the triple-net lease structure to some degree, we focus this report primarily on the "free-standing" net lease REITs and diversified REITs which make heavy use of the net lease structure that don't otherwise fall neatly into one of the other property sectors. Some net lease REITs focus their strategy on investment-grade tenants with near-zero credit risk, while others focus on "middle-market" or smaller tenants with higher potential credit risk levels. Currently, the most significant sources of credit risk are movie theaters (roughly 3% of rent), offices (5% of rent), and specialty retail (5% of rent).

{kind=link}

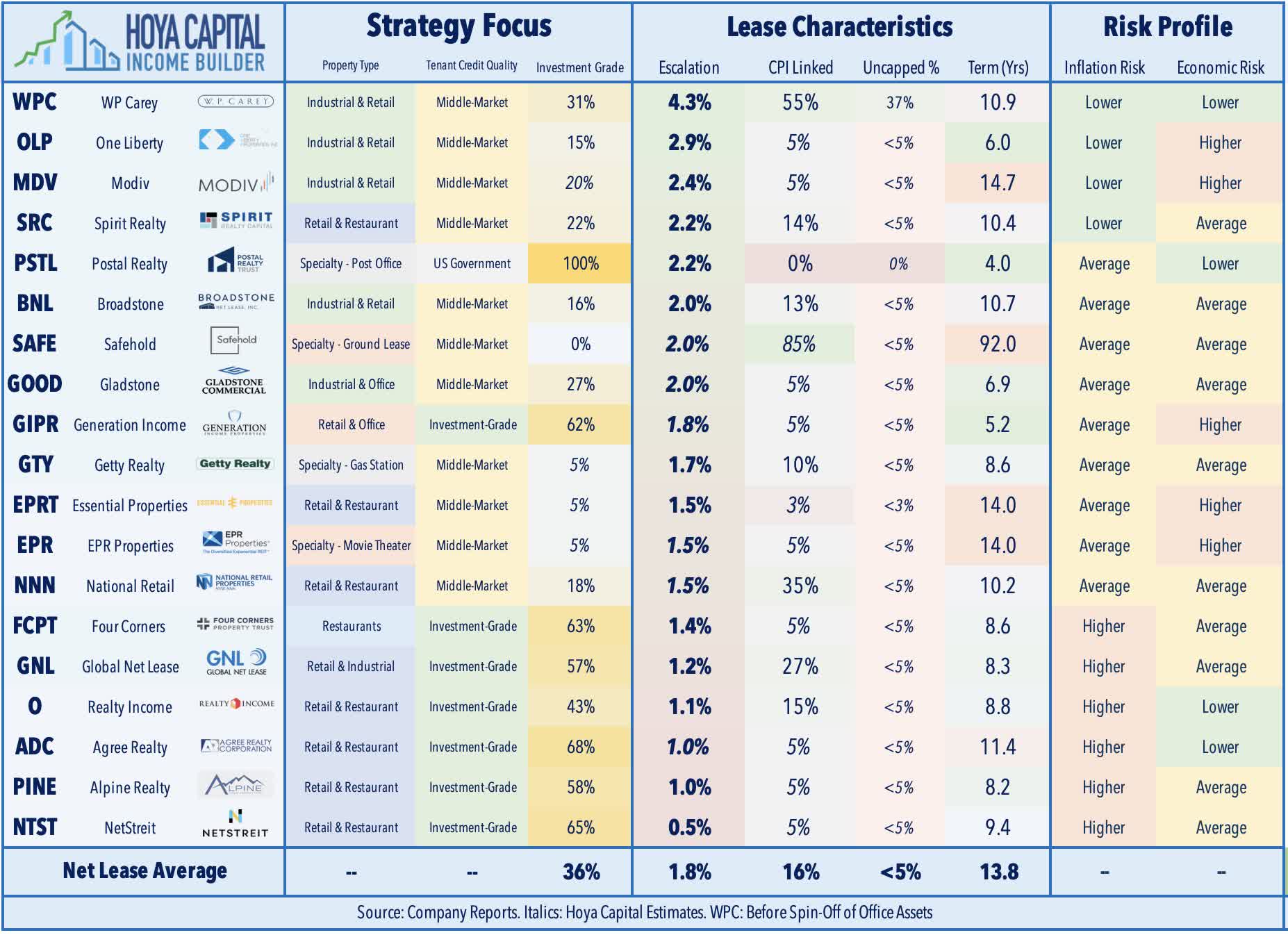

With this bond-like lease structure, naturally, comes bond-like risks - notably a high sensitivity to inflation and interest rates. Inflation-sensitivity and rate sensitivity are driven by several interacting factors, including lease structure and term, external growth potential, tenant credit quality, and the cyclicality of the underlying property type. Investment Grade ("IG") tenants - often retail tenants like Walgreens ( WBA ), CVS ( CVS ), Home Depot ( HD ), and FedEx ( FDX ) typically have minimal credit risk, but lease terms generally grant less potential upside or inflation protection to the property owner with fixed-rate or zero rent escalations. Only a handful of net lease REITs include explicit CPI linkages in their rent escalators - namely W. P. Carey , which has a sector-high 55% of its leases calculated using a CPI-based formula. Among the top ten largest net lease REITs, Broadstone and Spirit Realty are the only other net lease REITs to report average escalations of at least 2% thus far in 2023.

{kind=link}

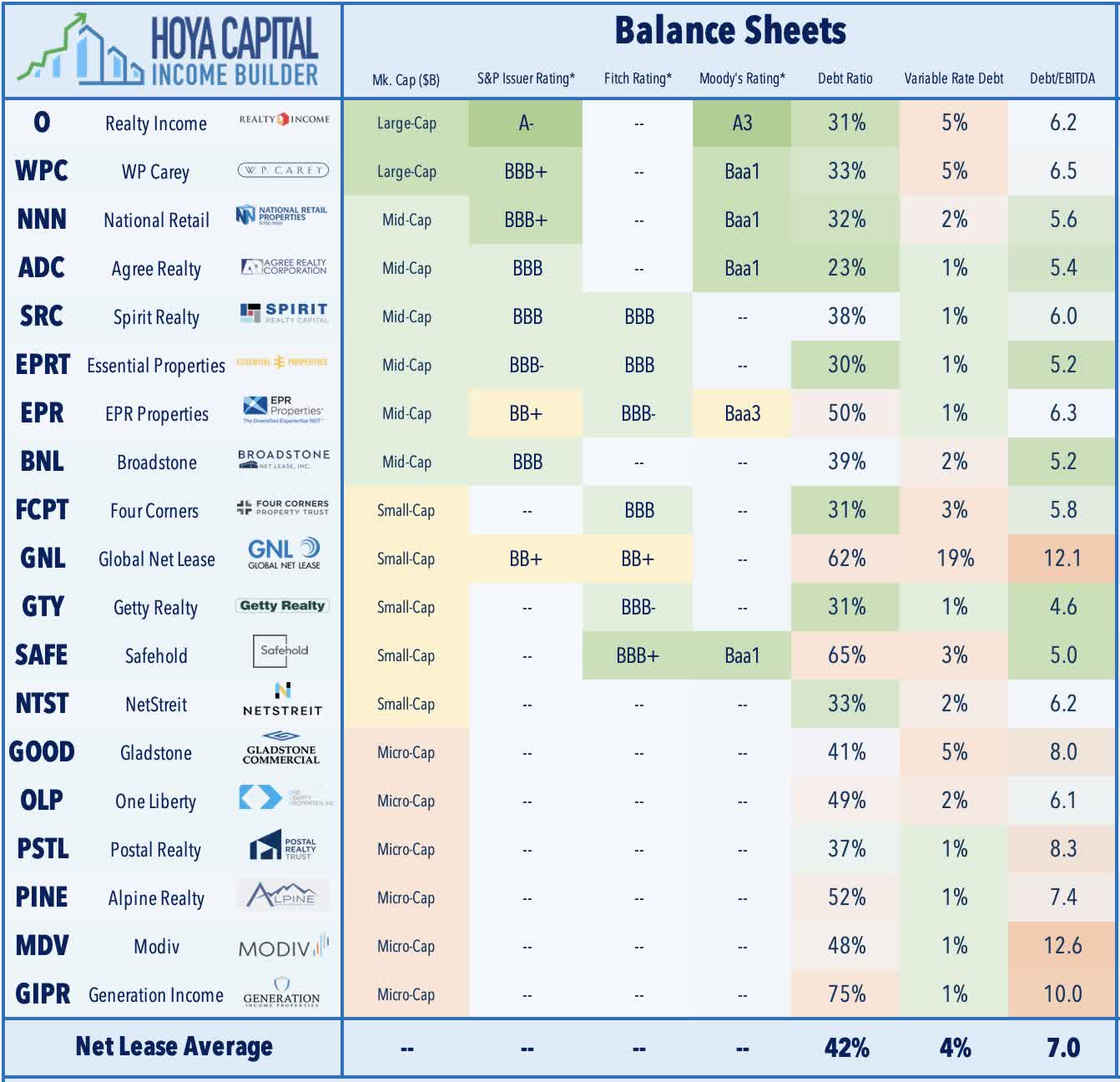

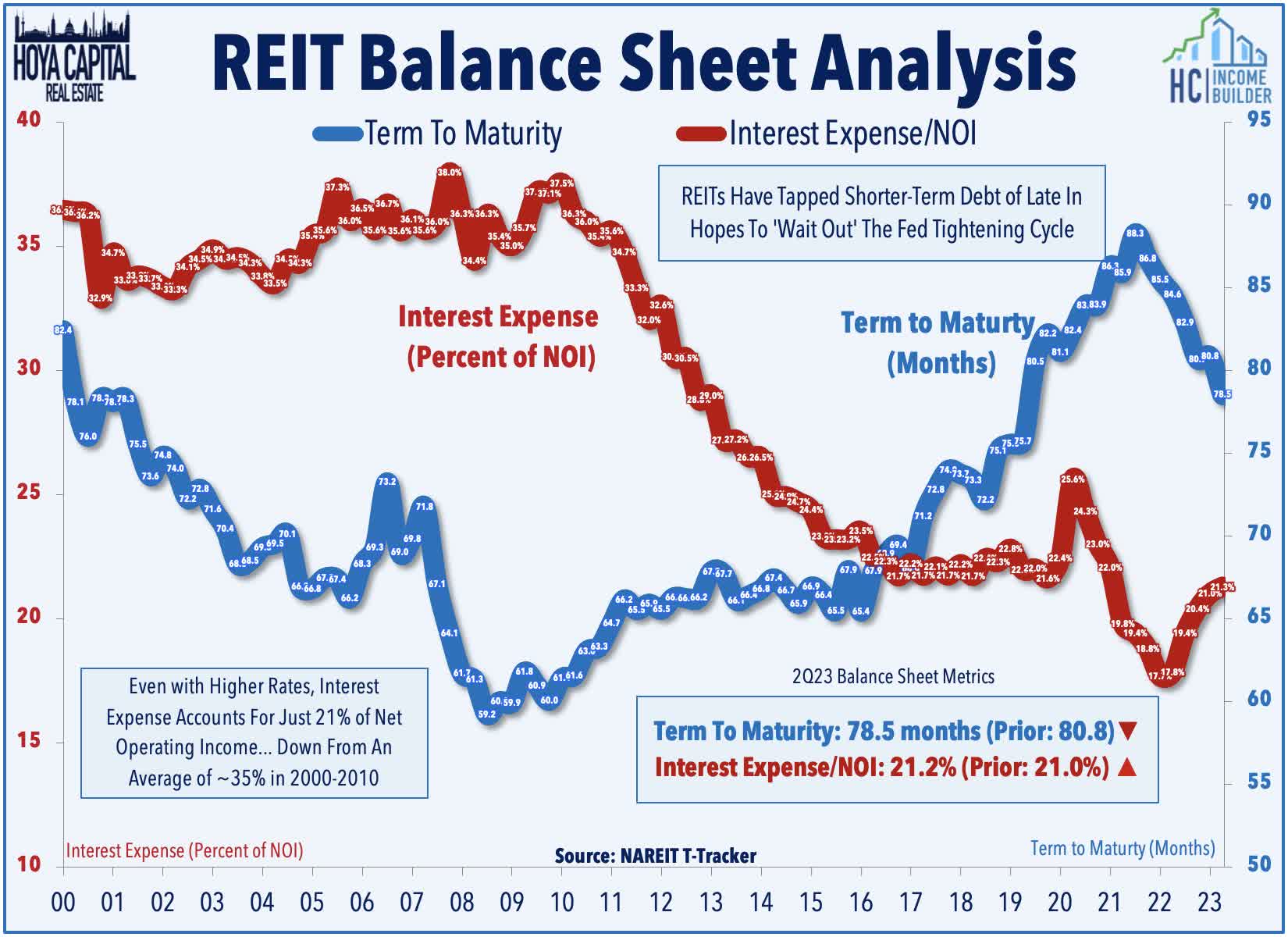

Balance sheet quality also plays a critical role in the degree of risk - and the "cost of capital" more broadly - and the net lease REITs that have lower leverage and more long-term fixed-rate debt should be able to maintain accretive investment spreads in a variety of macroeconomic environments - assuming that acquisition cap rates eventually "catch up" to the rise in cost of capital. Strong balance sheets and lack of variable rate debt exposure have positioned these REITs to be aggressors as over-levered private players seek an exit, but these REITs can afford to wait until the price is right. While many REITs have exhibited prudence by scaling back the pace of acquisitions in response to these dislocations, others have been perhaps overly aggressive in their recent acquisitions - often paying "top dollar" with razor-thin investment margins - while a handful of others have initiated seemingly impulsive pivots, potentially discarding decades of hard-fought progress. We continue to see the best value in net lease REITs that focus on "middle-market" tenants and the middle-tier of cap rates where inflation-hedging lease structures and initial yields grant more breathing room for higher financing costs.

{kind=link}

For Net Lease REITs, It's Business As Usual

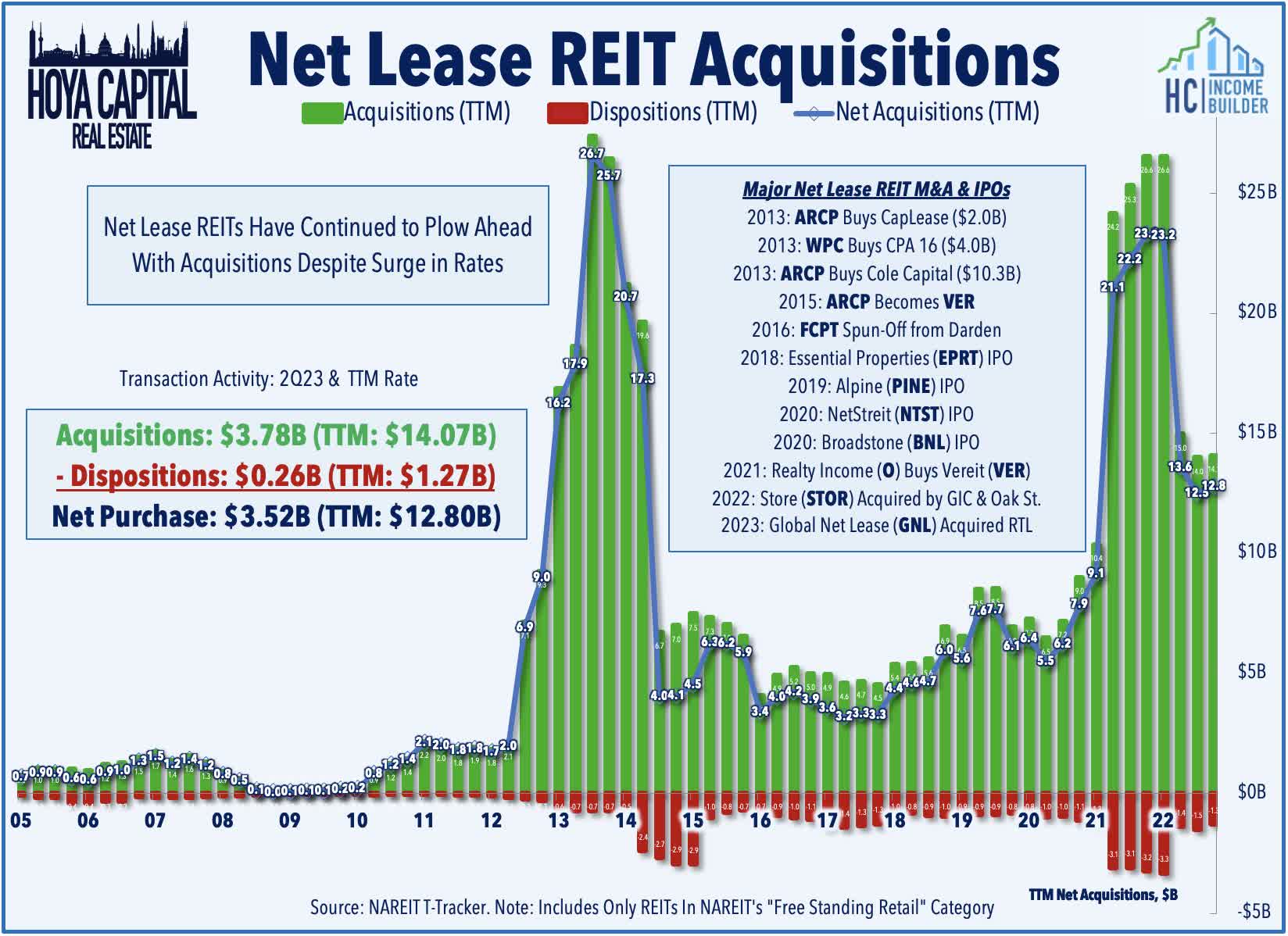

Acquisition-fueled external growth has historically been the "bread and butter" of the net lease sector's strategy, explaining the vast majority of the sector's FFO ("Funds From Operations") growth over the last two decades. Despite narrower investment spreads resulting from the significant increase in benchmark interest rates over the past year, net lease REITs completed $4B in property purchases in the second quarter, raising their twelve-month haul to over $14B. Notably, while net lease REITs account for just 7% of the Equity REIT Index - they accounted for nearly 50% of total REIT acquisitions so far in 2023. Surprisingly, three of the four largest net lease REITs - Realty Income ( O ), Agree Realty ( ADC ), and NNN REIT ( NNN ) actually raised their full-year acquisition targets in the most recent quarter, taking a surprising "business as usual" approach that could prove costly if rates remain elevated.

{kind=link}

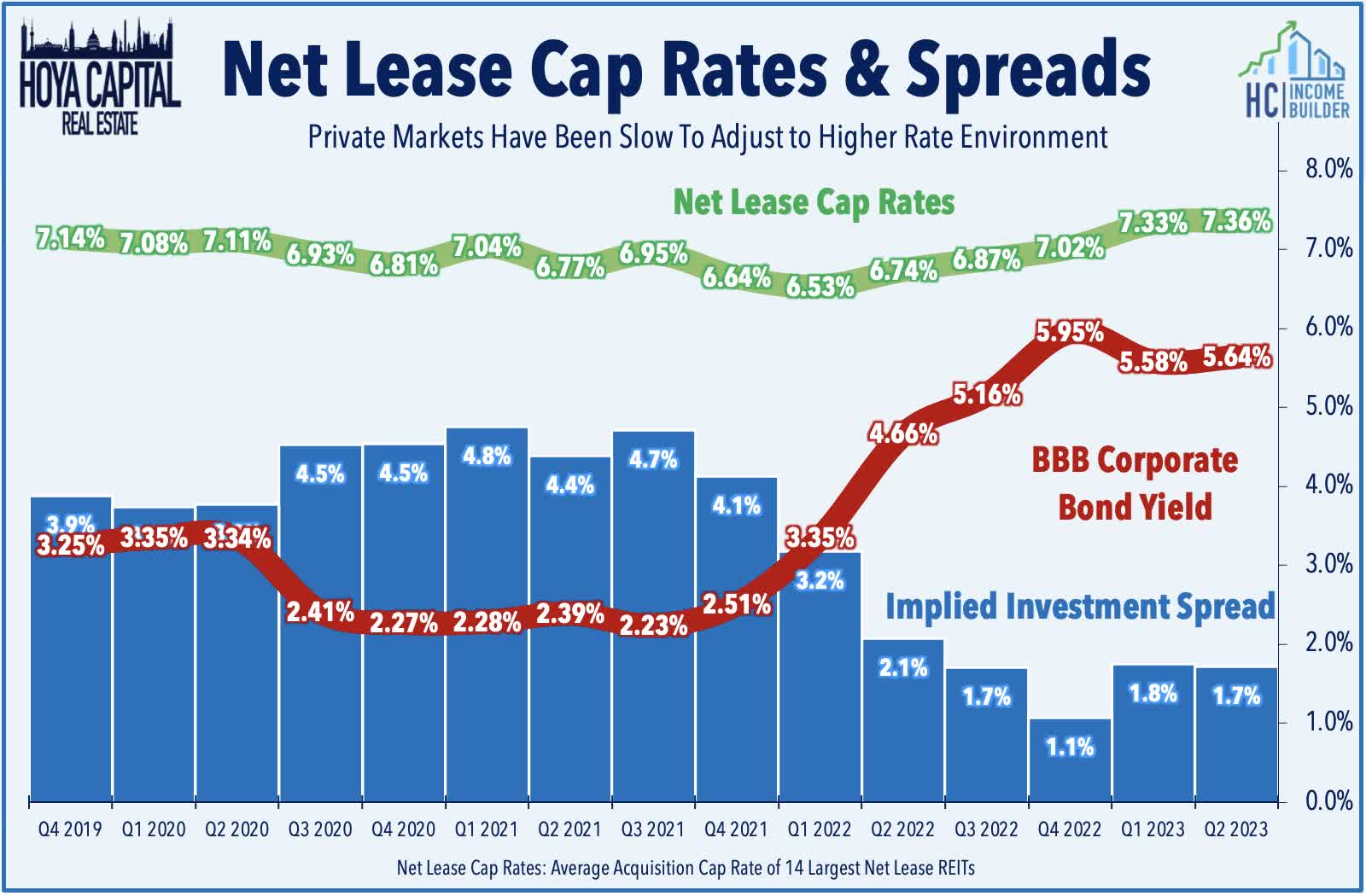

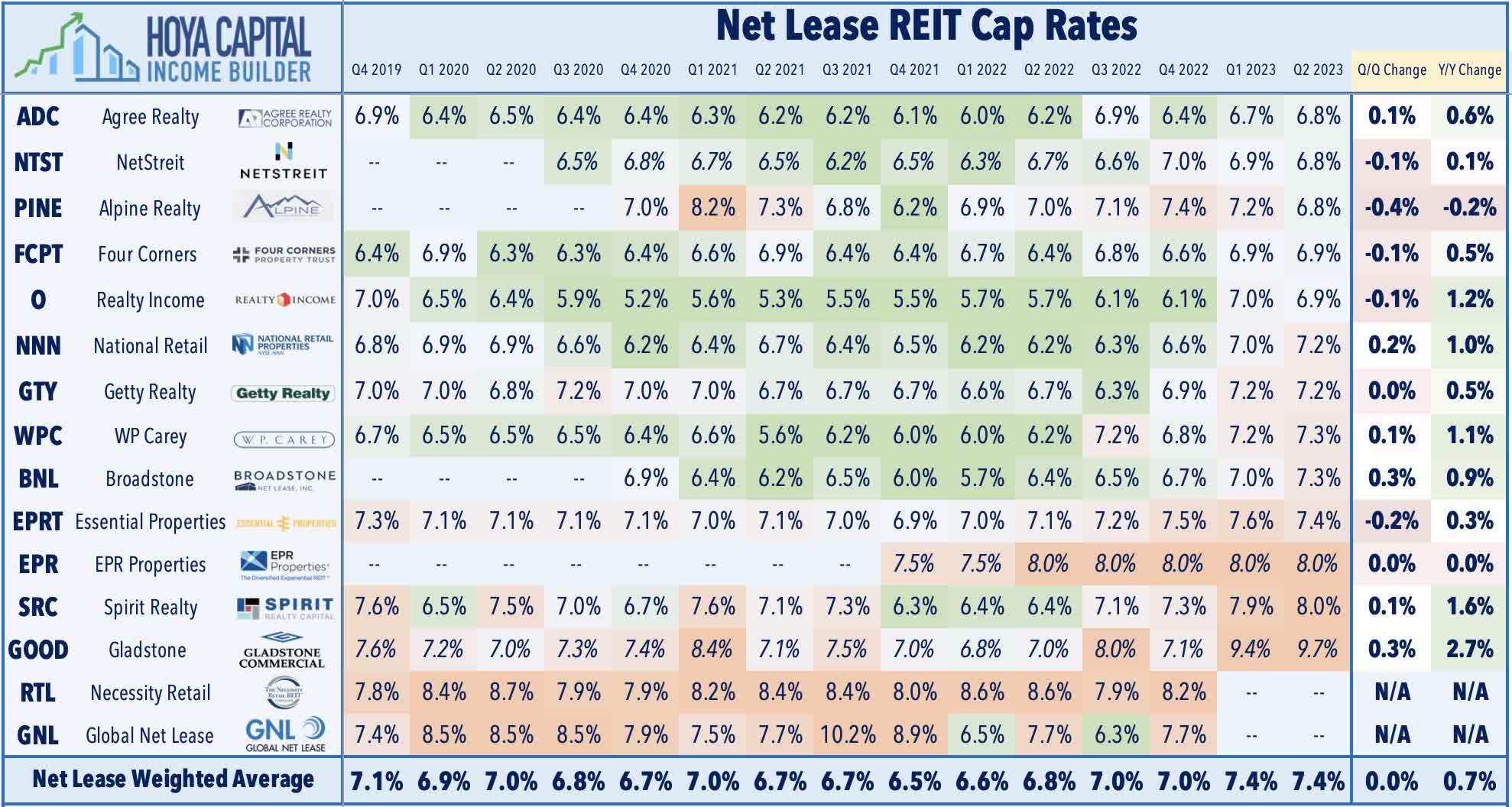

Curiously, private market real estate valuations of net lease properties have been far "stickier" than other comparable public market assets, underscoring our sense that net lease REIT investors, executives, and asset owners have seemingly never bought into the idea of a "new normal" of sustained higher interest rates. As noted in our Earnings Recap , net lease REIT acquisition cap rates increased 60 basis points from last year to roughly 7.4% in Q2, during which time benchmark financing rates (as implied by the BBB Corporate Bond Yield a useful proxy to approximate a Net Lease REITs' long-term cost of capital) increased by over 100 bps. The compression in investment spreads is more significant when compared to the prior year: since Q2 2021, net lease REIT acquisition cap rates have increased by 60 basis points, during which time the BBB Corporate Bond Yield has increased by 325 basis points.

{kind=link}

One such acquisition that may look particularly dubious if we've indeed entered a "higher for longer" period of sustained mid-single-digit benchmark rates is Realty Income's deal to acquire a 22% stake in The Bellagio casino from Blackstone Real Estate in a $950M deal which values the property at $5.1B with an implied capitalization rate of 5.2%. Notably, VICI Properties ( VICI ) indicated in its earnings call that it had discussed a deal for The Bellagio but determined that the asking price represented a "dilutive yield." The triple net lease structure with MGM includes 2.0% annual rent escalators for the next six years, with capped CPI-based increases from 2030 through 2050 - a rent escalation that is actually far better than Realty Income's existing portfolio, which has average rent escalators around 1%. Other net lease REITs have appeared more price-conscious in their recent acquisition strategy. Spirit Realty , for instance, noted that its average acquisition cap rate climbed to 8.0% in Q2 - up 160 basis points from last year. Broadstone , meanwhile, reported that its acquisition cap rate climbed to 7.3% in Q2, up 90 basis points from last year and 160 basis points from the lows in Q1 2022.

{kind=link}

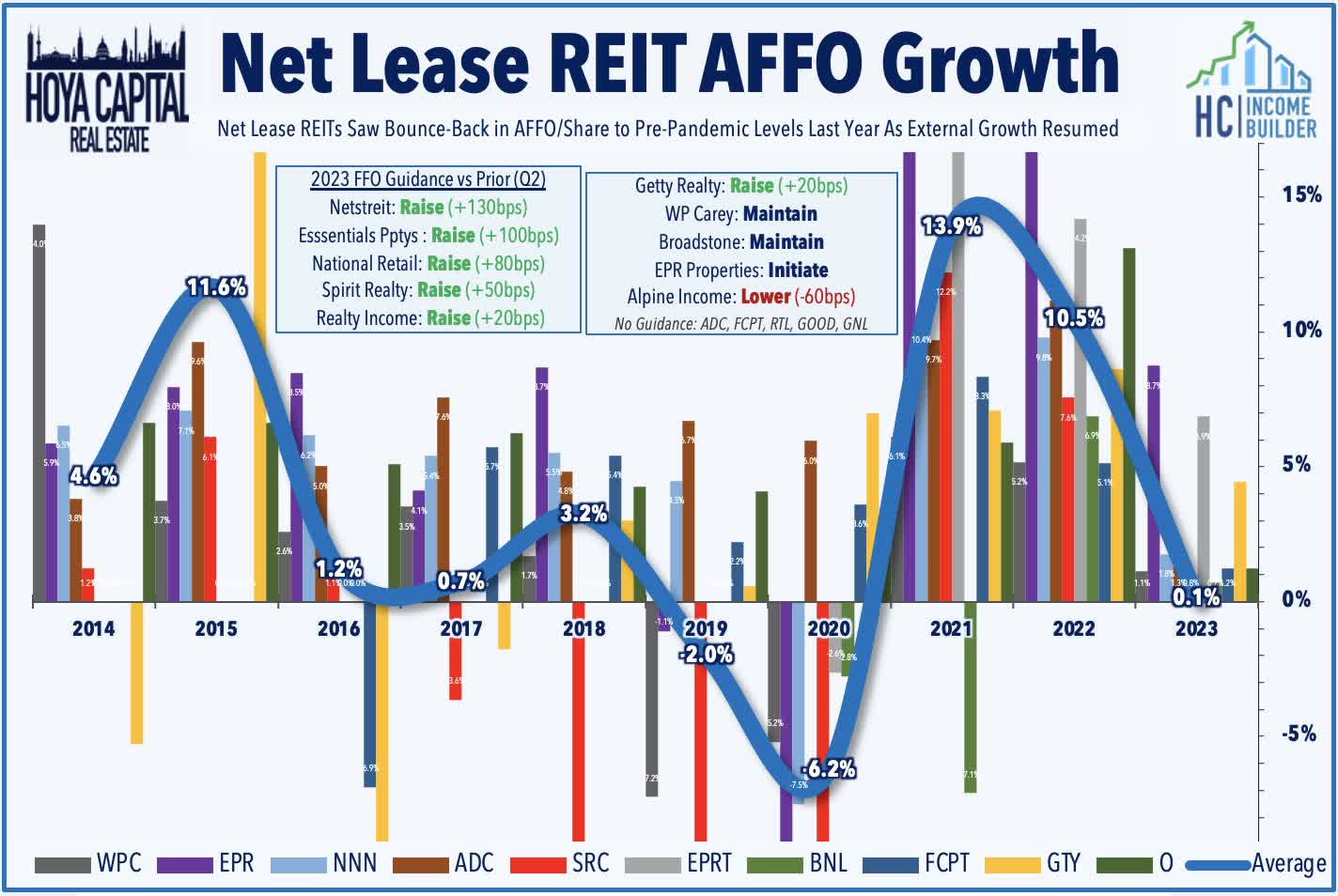

The overall "business as usual" approach had been working just fine for the past several quarters, but the resurgence in interest rates has raised fresh questions about the ability to finance some of these recent acquisitions at accretive spreads. Six of the ten net lease REITs that provide guidance raised their full-year FFO outlook in the second quarter, as strong underlying retail performance has helped to offset this more challenging acquisition and financing environment. Upside standouts on the earnings front included NETSTREIT ( NTST ), which raised its full-year FFO outlook to 4.7% (up 130 basis points from last quarter), and Essential Properties ( EPRT ), which raised its full-year FFO growth outlook by 100 basis points to 6.9%. Four other net lease REITs raised their full-year outlook - NNN REIT , Spirit Realty ( SRC ), Realty Income , and Getty Realty ( GTY ) - which lifted the sector's average full-year FFO growth target to 0.1% - which would be a decent showing if achieved after two years of double-digit FFO growth.

{kind=link}

Diving deeper into recent earnings results, Spirit Realty was notably able to raise its FFO target despite bucking the trend from its larger peers by trimming its full-year net acquisitions target to 400M from $450M. The only other net lease REIT to scale back its acquisition target in 2023 was Alpine Income ( PINE ). Among the nine REITs that provide full-year acquisition guidance, these REITs still expect to acquire over $13B in assets this year, led by the aforementioned Realty Income at $7B, followed by W. P. Carey at 1.65B, Agree Realty at $1.3B, and National Retail and NETSTREIT at roughly $500M each. One notable comment in recent earnings commentary came from ADC, which stated that it observed a "lack of competition amongst both public and private buyers" at the prices it was willing to pay, consistent with our concern that some net lease REITs are exhibiting a "winners curse" - potentially overpaying for recent property acquisitions.

{kind=link}

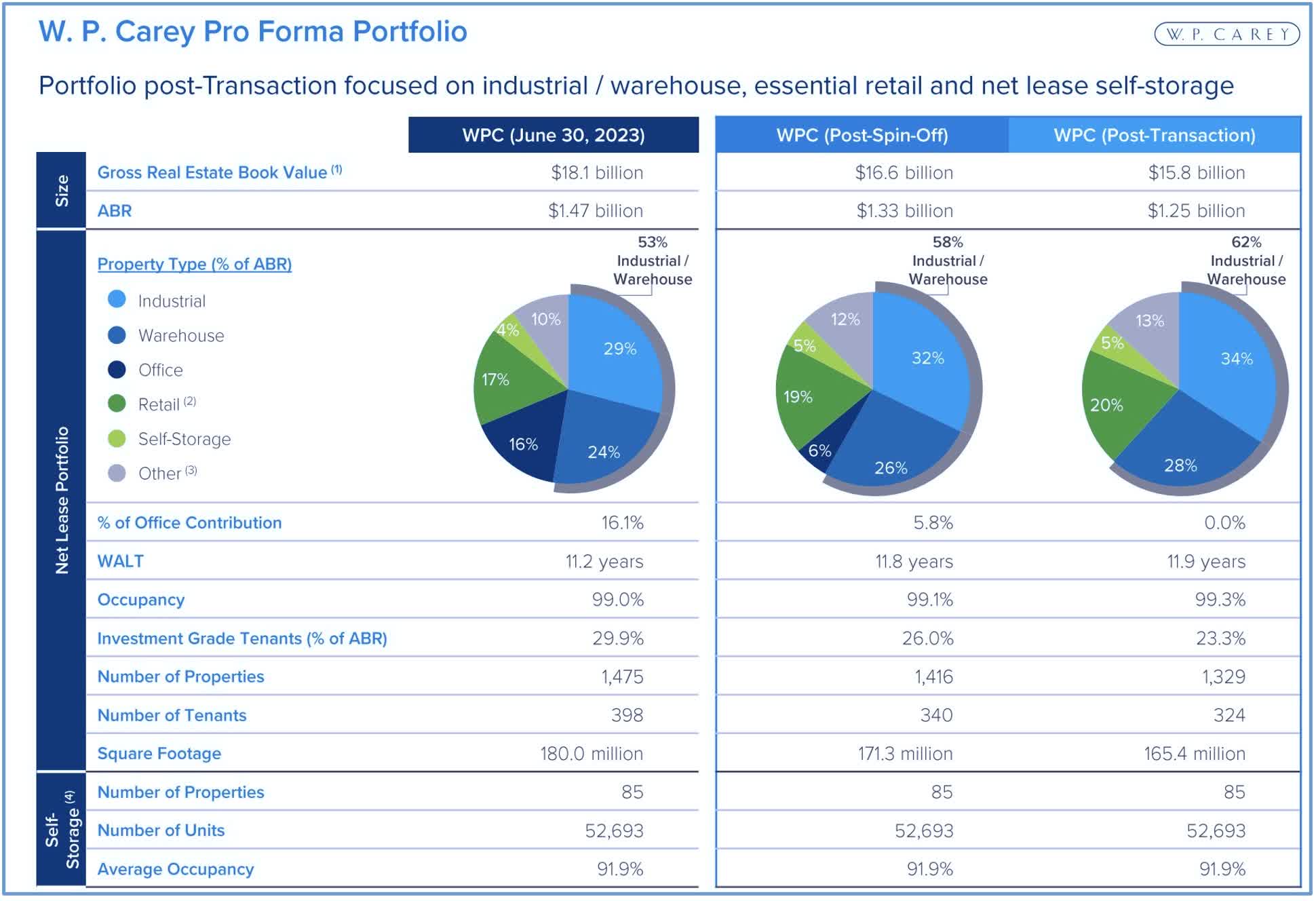

W. P. Carey ( WPC ) has been a notable laggard over the past quarter - and has been hit especially hard over the past week following its poorly-received announcement that it will sell the majority of its office assets (16% of its portfolio) aimed at driving a "re-rating" of WPC's stock price, which has traded at discounted valuations to similar-sized peers net lease and industrial peers. Post-transaction, roughly two-thirds of WPC's portfolio will be industrial net lease assets, with the bulk of the remainder in net lease retail and self-storage. WPC now trades at a roughly 10x P/FFO - a steep discount to the roughly 15x average P/FFO ascribed to comparable net lease industrial REITs. While we continue to see value in WPC's underlying portfolio and its best-in-class inflation-hedged lease structure, management has some explaining to do after this botched unveiling in which it appeared surprisingly unprepared, failing to effectively convey the strategic rationale for several abrupt and costly strategy shifts, including an indicated dividend reduction, putting at risk its hard-earned "dividend aristocrat" status.

{kind=link}

Described by the company as a "rip off the band-aid" approach, the strategy entails a spin-off of 59 office properties into a new REIT - Net Lease Office Properties - that will be completed by the end of next month - and a sale of 87 remaining European office properties, which it expects to complete by early 2024. Upon completion of the spin-off, WPC stockholders will own shares of NLOP via a pro rata special distribution, which is expected to be taxable for U.S. federal income tax purposes. Met by confusion from analysts given WPC's relatively solid operating performance in recent quarters - including sector-leading same-store NOI growth - WPC indicated that NLOP would effectively function as a liquidation company with a strategy "focused on realizing value through the strategic asset management and disposition of its assets." WPC lowered its full-year AFFO guidance to $5.24/share at the midpoint - down from its prior outlook of $5.35 - and introduced plans to "reset" its dividend policy, "targeting an AFFO payout ratio of 70%-75%." This policy would imply an 11% dividend cut to $3.80/share based on current AFFO guidance, but WPC did not provide forward guidance for post-transaction AFFO levels and provided few specifics on its anticipated use of the proceeds.

{kind=link}

Net Lease REIT Stock Performance

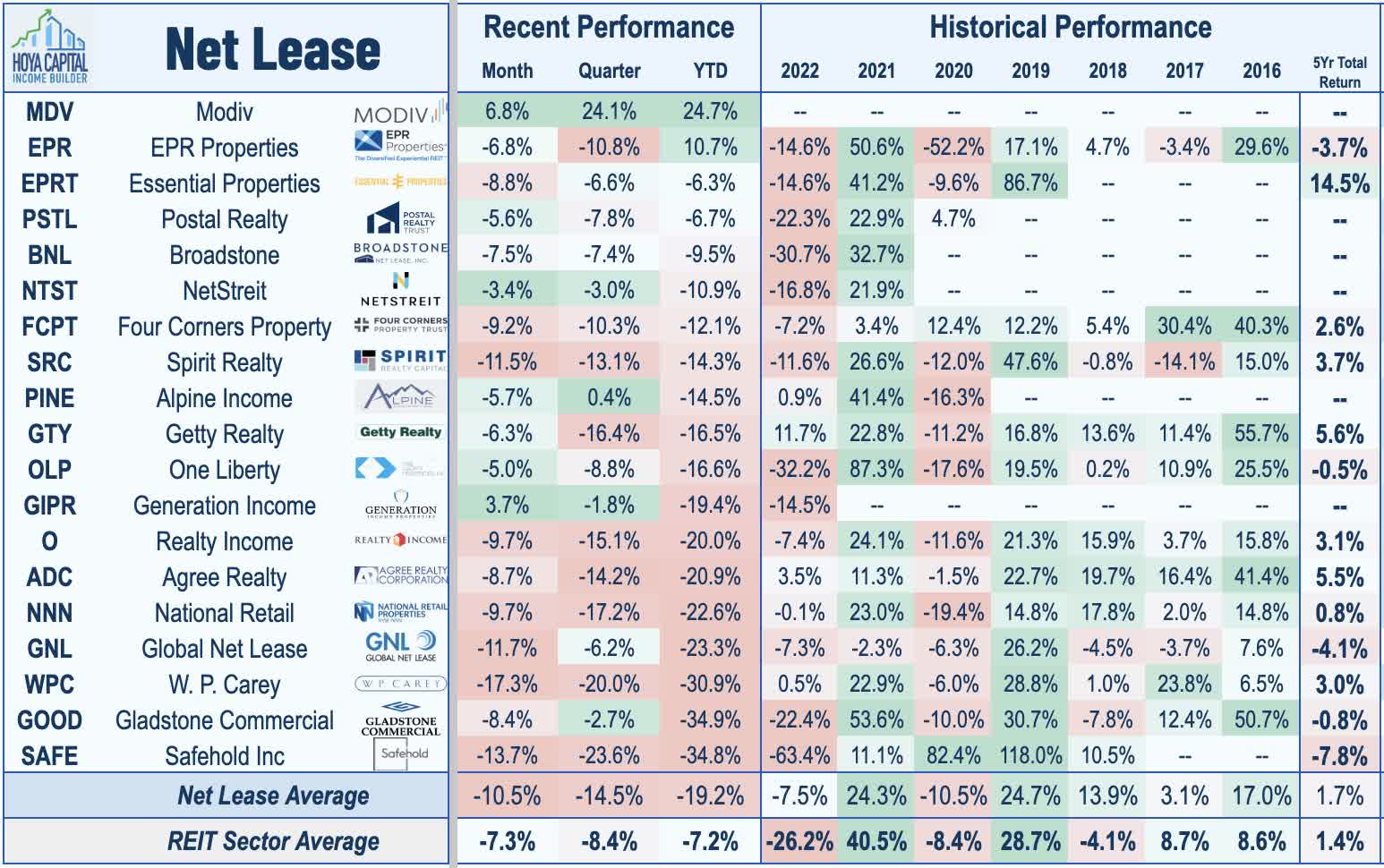

Net lease REITs were slammed early in the pandemic - plunging more than 50% at their lows in March 2020 - but began to rebound in mid-2020 and had delivered notable outperformance over the REIT Index through mid-2023 before the renewed pressure from "higher for longer" concerns. The Hoya Capital Net Lease Index - a market-cap weighted index of these 18 REITs - is now lower by nearly 20% this year, significantly lagging the broad-based Vanguard Real Estate ETF ( VNQ ) - which has dipped 7.5%, and the S&P 500 ETF ( SPY ) which has posed gains of nearly 12%. The weak performance this year, however, follows a relatively strong year in 2022 in which net lease REITs were the top-performing property sector.

{kind=link}

Seventeen of the eighteen net lease REITs are lower on the year. Newly-listed Modiv ( MDV ) - which went public last year - has been the upside standout, as its transition to focus exclusively on industrial real estate has been far better-received than the similar announcement from W. P. Carey . Movie theater owner EPR Properties ( EPR ) is the only other net lease REIT in positive-territory this year amid a recovery in movie theater attendance and after reporting progress in lease renegotiations among several struggling theater operators. Laggards this year include Safehold ( SAFE ) - the lone REIT focused specifically on ground leases - which dipped more than 60% in 2022 - and has declined another 35% this year on concerns over the outlook for its ultra-low yielding ground lease portfolio in a higher rate environment. Other laggards this year include Gladstone Commercial - which became the first net lease REIT over the past two years to reduce its dividend, and W. P. Carey - which signaled that it'll become the second.

{kind=link}

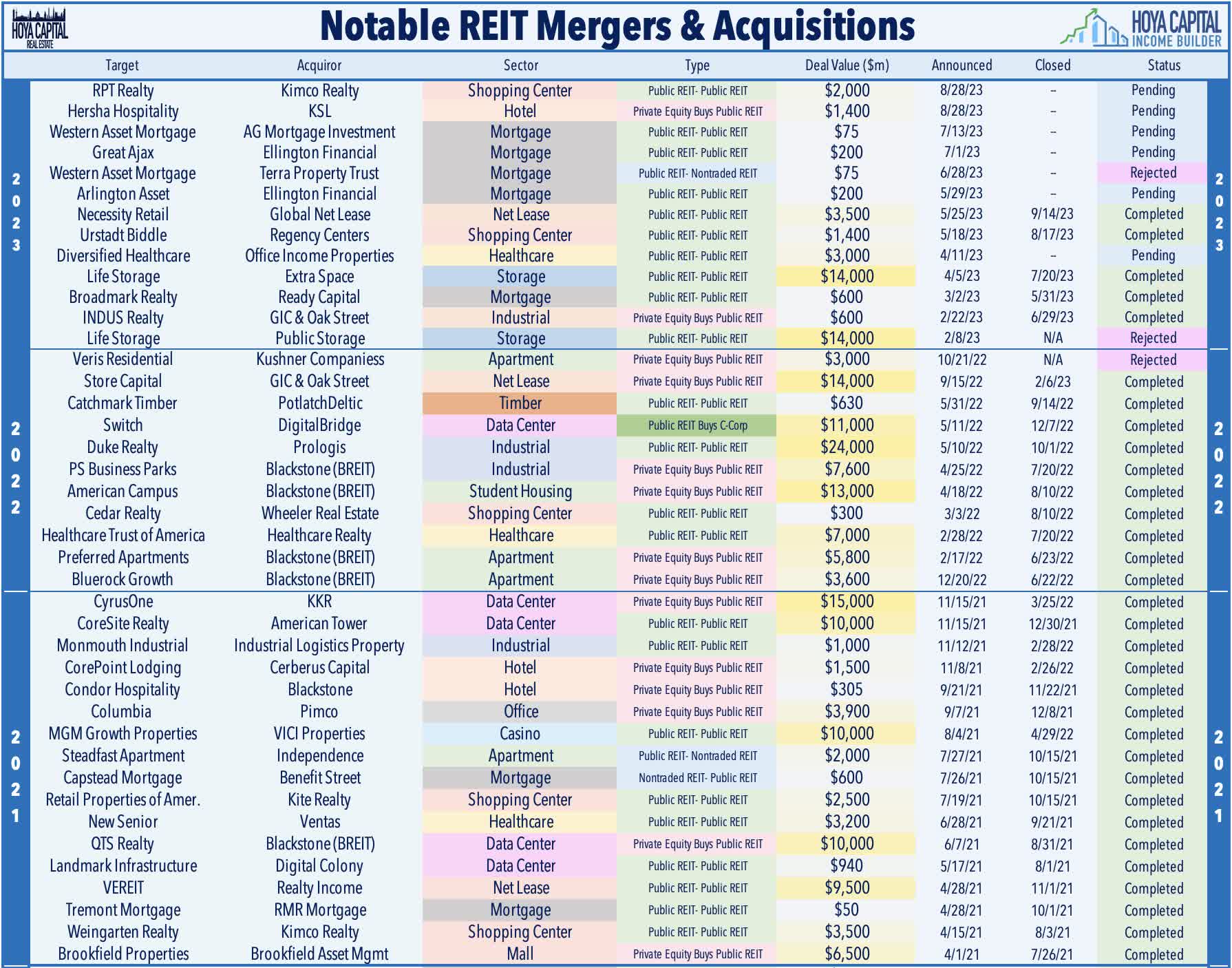

We've also seen some M&A activity in the net lease space this year. Global Net Lease ( GNL ) and Necessity Retail - a pair of externally managed REITs advised by AR Global - completed a merger that included the internalization of both GNL's and RTL's management. Shares of RTL have ceased trading on the Nasdaq. As part of the merger, GNL noted that it plans to reduce its quarterly dividend by 12% to $0.354 per share. Management cited the benefits of improved scale, reduced leverage, and operating efficiencies, noting that the combined company would own roughly 1,350 properties with an aggregate enterprise value of $9.5B - making it one of the eight largest net lease REITs by asset value. The deal follows a heated proxy battle led by activist firm Blackwells Capital, and proxy advisory firms ISS and Glass Lewis each recommended that shareholders withhold support for several of AR Global's directors and raised questions over the firms' corporate governance practices.

{kind=link}

Speaking of REITs with a history of questionable corporate governance practices, Peakstone Realty Trust ( PKST ) - formerly known as Griffin Realty Trust - began trading on NYSE earlier this year through a direct listing, and the early-goings have not been pretty. PKST currently trades at more than 50% below its self-reported Net Asset Value before the listing. Peakstone is a net lease office and industrial REIT that owns 78 properties across 24 states. Roughly 70% of PKST's Net Operating Income ("NOI") is derived from its portfolio of 55 office properties, while 30% of NOI comes from its portfolio of 23 industrial properties. Griffin Real Estate advises a collection of non-traded REITs and closed-end funds and has faced several lawsuits over its suspension of share redemptions and NAV valuations.

{kind=link}

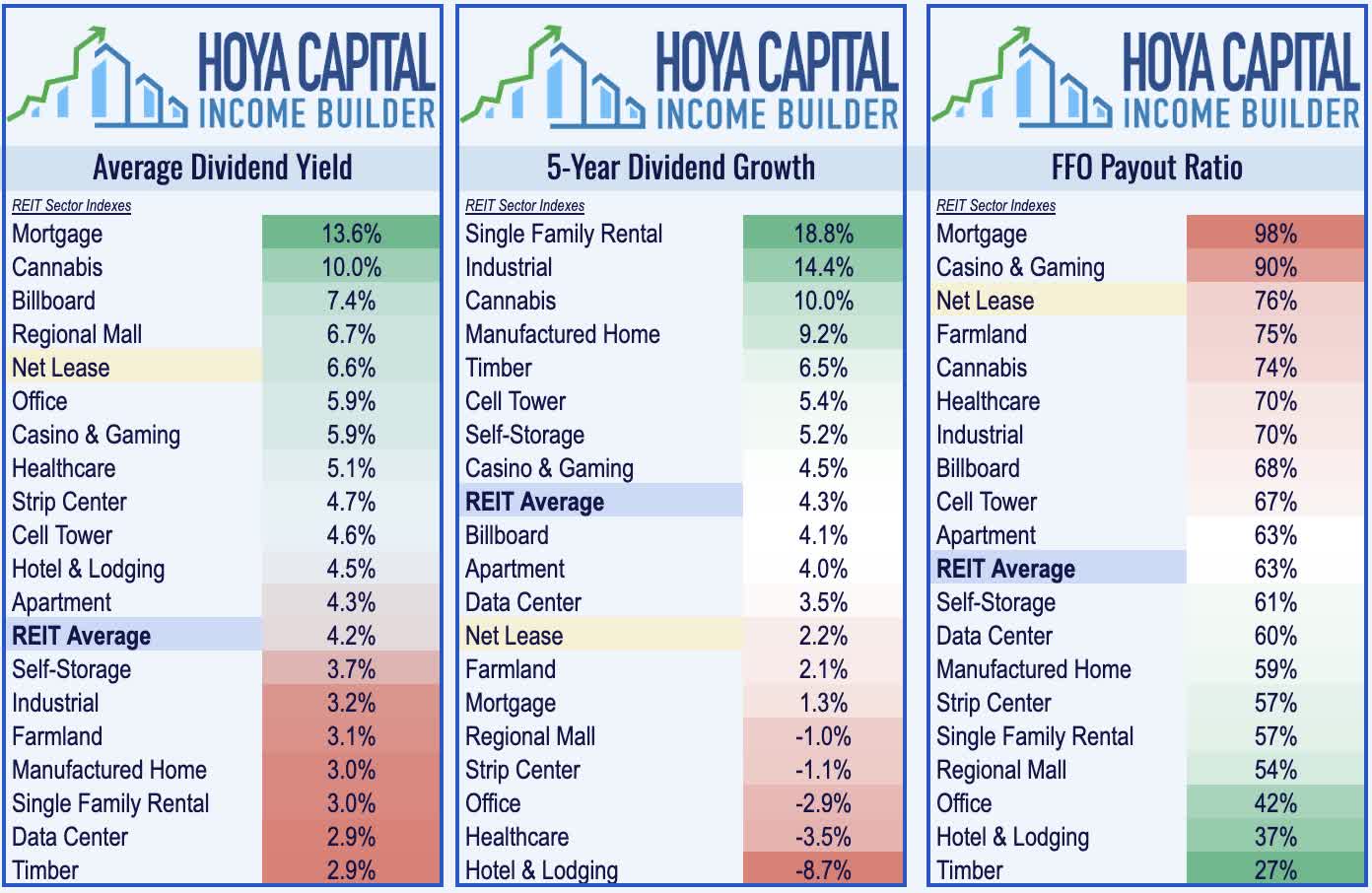

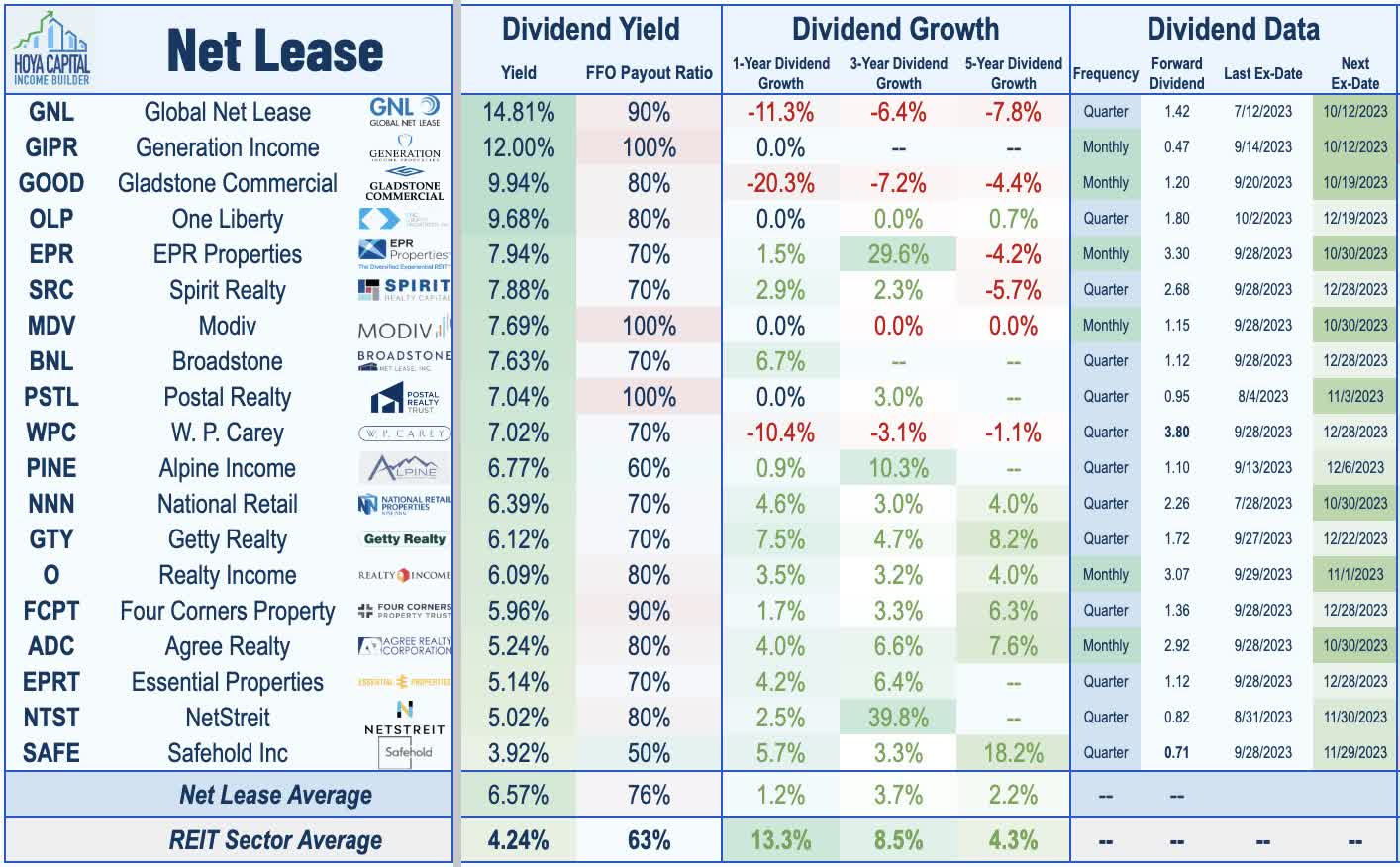

Net Lease REIT Dividend Yields

Relatively high dividend yields are one of the key investment features of the net lease REIT sector, and the resilience in maintaining or increasing dividends has helped to push dividend yields toward the top of the REIT sector. Net lease REITs now pay an average dividend yield of 6.6%, a premium of 240 basis points over the broader market-cap-weighted REIT average of 4.2%. Net lease REITs pay out roughly 75% of their free cash flow, also towards the top end of the REIT sector average, but typically make heavy use of secondary equity offerings to raise capital to fund accretive external growth.

{kind=link}

Seven net lease REITs have raised their dividend this year, led by Realty Income - the largest net lease REIT - which has hiked its monthly dividend by four times this year, representing a 3.2% year-over-year increase. Of note, a half-dozen of these REITs have delivered consistent dividend growth over the past half-decade, led by Getty Realty , Four Corners , STORE Capital, Agree Realty , and Realty Income . Ten net lease REITs are currently paying a dividend yield above 7%, led on the upside by externally managed Global Net Lease and small-cap Generation Income ( GIPR ), which each command a dividend yield above 12%.

{kind=link}

Net Lease REIT Credit Risk

At the outset of the pandemic, investors were painfully reminded of the potential credit risk faced by net lease REITs amid a wave of economic lockdowns and uncollected rents - a focus that has been renewed given the lingering recession concerns. While the triple-net lease structure has provided a strong degree of protection for most segments, some tenants in several heavily disrupted categories including movie theaters, offices, and some specialty retail segments still face an uncertain future, underscored by the recent bankruptcies of Bed Bath Beyond and Party City.

{kind=link}

At a high-level, U.S. retail fundamentals are as solid as they've been in a half-decade. Coresight Research reported that the number of store openings had outpaced closings by nearly 2x since early 2021 with particular strength in larger-format 'big box' strip centers along with free-standing retail. After surging to around 10,000 in both 2019 and 2020, just 5,000 retail stores shut down in 2021 while only 2,600 closed in 2022 - the lowest level of store closings on record. In our Earnings Recap, we noted that occupancy rates at Strip Centers are now at record-highs while Mall occupancy rates have recovered the majority of their pandemic-era declines.

{kind=link}

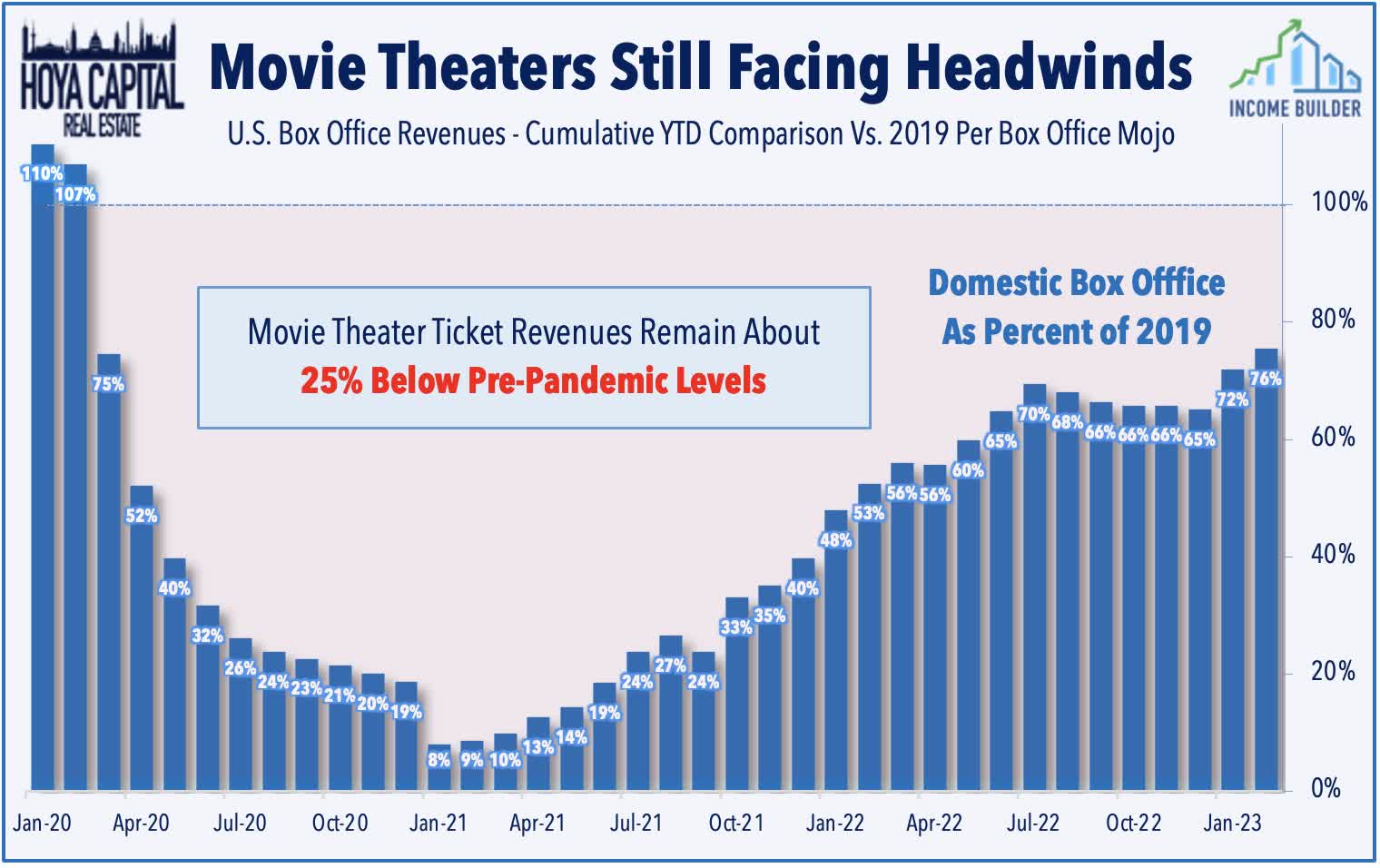

The recovery is significantly less certain for movie theaters, which represent roughly 5% of overall net lease NOI - but are the primary property type for EPR Properties . Box Office Mojo data shows that box office revenue plunged 80% in 2020 and has remained about 15% below 2019 levels thus far in 2023. A handful of other net lease REITs have between 1.5-5% of their rents coming from movie theater tenants, but these REITs have not seen a material uptick in missed rents from these theater tenants despite the apparent distress. Of note, EPR announced earlier this year that it reached a comprehensive lease restructuring deal with struggling movie theater operator Regal Cinemas which includes a new master lease for 41 of the 57 properties and the termination of operations at 16 properties. EPR expects the deal to achieve 96% of total pre-bankruptcy rent in 2024 if certain performance-based thresholds are fully met. The restructured deal will be anchored by a new master lease for 41 properties, a triple-net lease with $65 million in total annual fixed rent, which will escalate by 10% every five years.

{kind=link}

Takeaway: Don't Fight the Fed

Net Lease REITs - one of the most "bond-like" and interest-rate-sensitive property sectors - have lagged in recent months as investors come to grips with a potential "higher-for-longer" interest rate environment. Thriving in the "lower forever" environment, the industry had been reluctant to acknowledge the higher-rate regime, keeping private-market values and cap rates surprisingly "sticky" and resulting in compressed investment spreads. Despite the tighter spreads, acquisition activity has slowed only modestly for some REITs, a strategy that could prove costly if rates remain elevated. Strong balance sheets and limited variable rate debt exposure had afforded these REITs the ability to be patient until the price is right, and while some REITs have exhibited prudence, others have been overly aggressive, seemingly putting at risk decades of hard-fought progress. Don't Fight the Fed: We see the best value in net lease REITs that focus on "middle-market" tenants and the middle-tier of cap rates where inflation-hedging lease structures and initial yields grant more breathing room for higher financing costs.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Net Lease REITs: Fighting The Fed