NTES - NetEase: Masked Margin Miss

Summary

- My most important takeaway from NetEase's Q4 FY22 earnings call yesterday is on the margin dynamics:

- The headline ~300bps gross profit margin miss vs consensus is understandable as it is due to a one-time effect.

- But a favorable mix effect toward PC games - which have materially higher margins than mobile games - failed to translate into higher margins.

- Based on this, I deduce that NetEase is seeing a 360bps margin headwind in its core online gaming business. I expect this weakness to continue as the underlying drivers look weak.

- Technical analysis supports my view, which is a 'Sell' stance on the stock.

Thesis

NetEase (NTES) (NETTF) reported yesterday with headline revenues in-line with consensus expectations and a 301bps gross profit margin miss due to a one-time impact. At face value, this does not warrant much concern. But deeper analysis into the details of the numbers suggests a more persisting margin weakness brewing in the background. I believe the market is missing NetEase's true margin weakness, which is more structural. This leads me to have a bearish view on the stock.

The headline gross profit margin miss is understandable

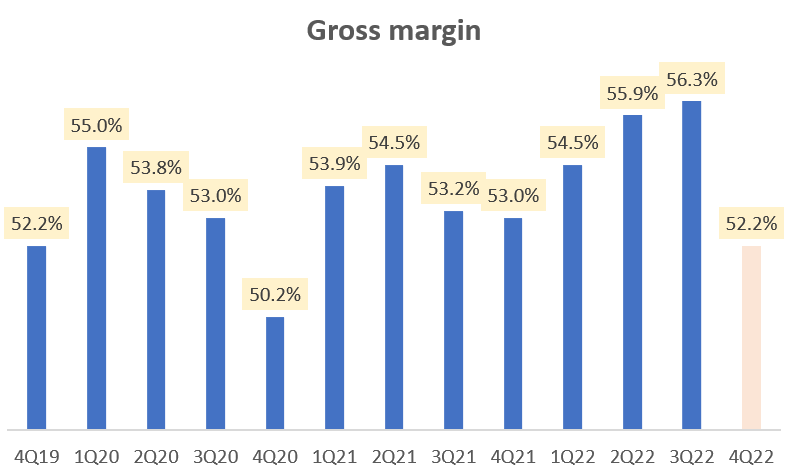

Gross Margins (Company Filings, Author's Analysis)

{kind=link}

NetEase reported overall gross margins of 52.2% , corresponding to a ~300bps miss vs consensus estimates of 55.3%. This was due to a one-time impact of royalty fees from the termination of their games publishing agreement with Blizzard Entertainment ( ATVI ) that was announced in Q3 FY22 and implemented in January 2023.

This is not representative of future business performance, and hence it is important to adjust for this one-time impact when analyzing the core business performance:

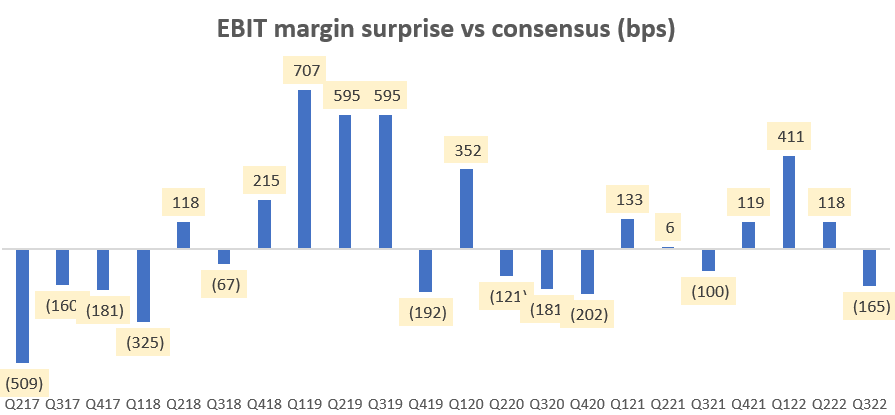

During the current CFO Charles Yang's tenure since June 2017, NetEase has had mixed surprises vs consensus expectations before the last quarter:

EBIT margin surprise vs consensus (bps) (Company Filings, Capital IQ, Author's Analysis)

{kind=link}

The median EBIT margin surprise vs consensus is -31bps. If I conservatively give the company the benefit of the doubt and assume the company met gross margins of 55.2% ex of the one-time royalty fees impact, the normalized gross margins come out to be 55.2%:

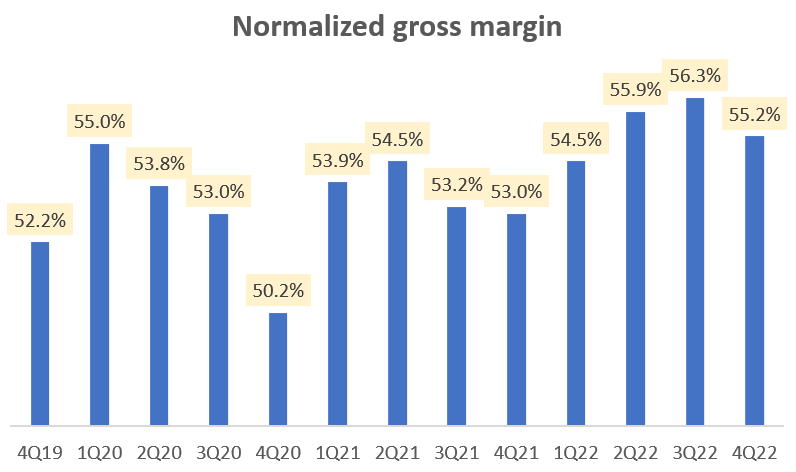

Normalized Gross Margin (Company Filings, Author's Analysis)

{kind=link}

Optically, this looks more in-line. But...

A favorable mix effect not translating to higher margins is worrying

The performance of the online games segment is the most important driver for NetEase as that makes up 75.3% of overall revenues and the majority of the margin profile as well. Within this segment, PC games made up 33.6% of overall revenues in Q4 FY22 compared to 31.4% in Q3 FY22, with the balance coming from mobile games.

This higher PC games mix effect is important because PC games have a higher gross margin profile than mobile games. From NetEase's annual reports during the 2017 - 2021, you can observe that PC games averaged 85.7% in gross margins compared to only 53.0% for mobile games; a 32.7% increment difference. Thus, I would have expected the 220bps higher revenue contribution from PC games to have translated into a 70bps (2.20%*32.7% = 0.7% = 70bps) increase in gross margins for the online gaming segment. But this did not happen:

As I explained in the section prior, if I add back the ~300bps adjustment to get a normalized gross margins figure, the online gaming's normalized gross margins come in at 62.1%. Last quarter , the online games' gross margins came in at 65.0%. Thus, this corresponds to a 290bps decline. A 290bps decline when there was supposed to be a 70bps benefit from a favorable mix shift results in a genuine 360bps margin miss in the online gaming segment .

Management did not offer any comments on this implied weakness in the gaming margin profile. Unfortunately, neither was there was any question to probe on this matter further by the analyst community in the Q4 FY22 earnings call .

My guess is there is a mix of downward pricing pressures and a fall in in-game purchases. I believe consumers and gamers' in-game purchasing behavior is akin to the response to advertisements, since both in-game collectibles and real-world advertisements have the same mantra of "Buy X to improve your life/in-game life". With this context, I find it unsurprising that gaming is likely seeing weakness given the global slowdown in ad spends , in both the US and China, driven by reduced impact conversions .

Moreover, according to media-buying firm GroupM, global ad spend growth is expected to slow down in 2023 with a 5.9% YoY growth; lower than the 6.4% YoY growth in the prior year. Hence, I would not be surprised to see NetEase's gaming revenues and margins continue to see headwinds in Q1 FY23 and even beyond.

Technical analysis

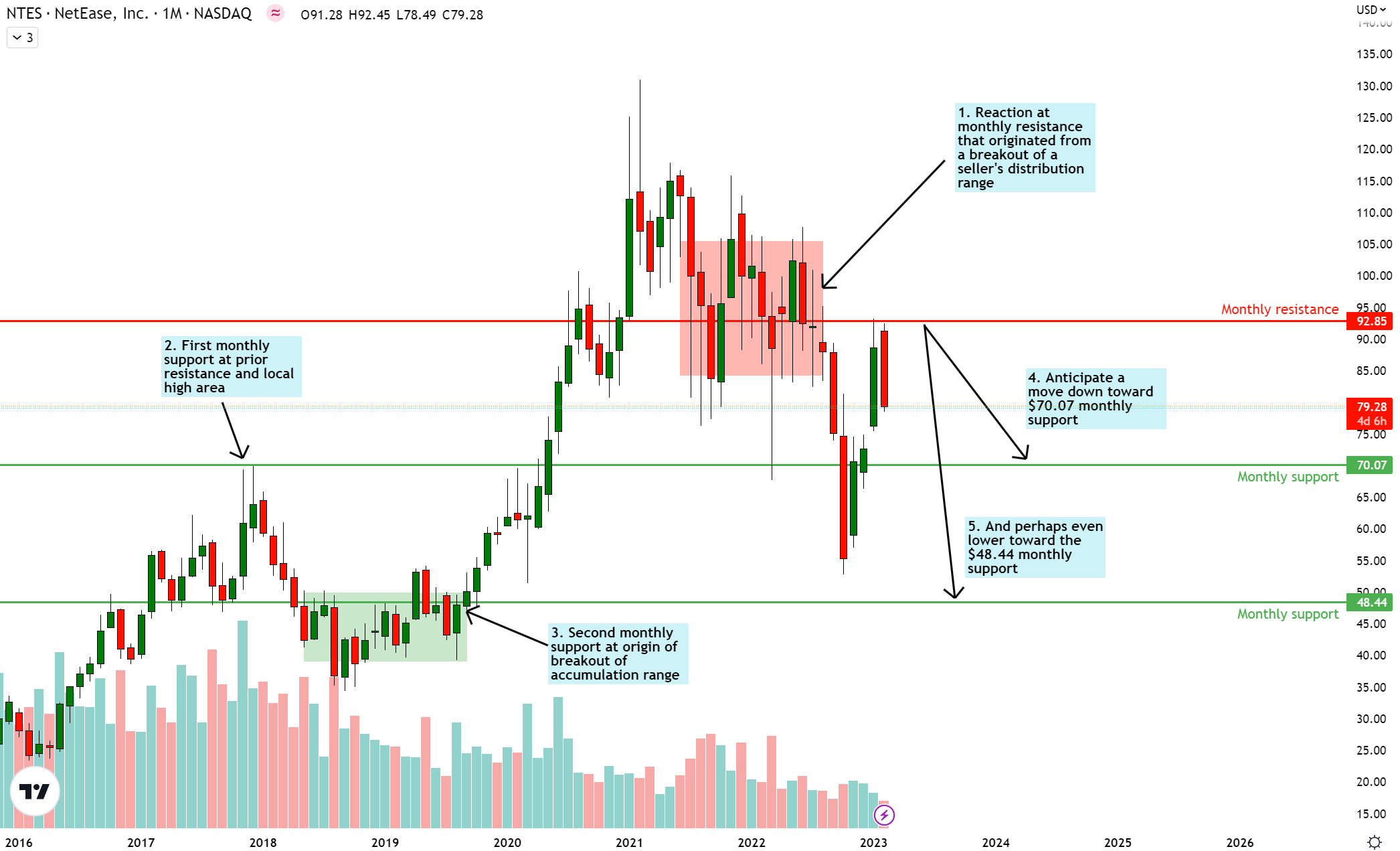

NetEase Technical Analysis (TradingView, Author's Analysis)

{kind=link}

Prices are currently reacting off a key monthly resistance level at $92.85. I anticipate a further fall toward at least $70.07, where I spot the nearest monthly support. If pricing conversions on online games continues to be weak for longer, I would watch for a return down to $48.44.

Key monitorables

To get further clarity on my thesis, I intend to follow Tencent's (TCEHY) (TCTZF) Q4 FY22 earnings call expected on 22nd March 2023, to track commentary on Tencent Gaming, which forms 31% of total revenues.

As mentioned earlier, I believe digital ads effectiveness and in-game app purchases are correlated. Hence, I am monitoring the ad spend environment in China, US, Japan, Europe and other markets where NetEase is present.

Summary

NetEase reported a 301bps miss in gross margins in the Q4 FY22 earnings call. But this is understandable since it is a one-time impact associated with royalty fees from their termination of an agreement with Blizzard Entertainment. Correcting for this impact, it would seem that NetEase met margin expectations of the street.

However, a deeper dive into the online gaming segment reveals that despite a favorable mix shift toward the higher margin PC games, NetEase's normalized online gaming margins (which does not count the 301bps one-time impact) still fell 290bps. This corresponds to a more structural 360bps margin miss vs expectations, likely due to weaker pricing and reduced in-game purchase conversions.

Reasonably assuming in-game purchase activity is correlated to advertising conversions due to similar consumer behavior, and given advertising firms' outlook of continued weakness in the advertising market in 2023, I believe NetEase is likely to see continued slowness ahead. Technical analysis also supports this view.

Hence, I rate NetEase a 'Sell'.

For further details see:

NetEase: Masked Margin Miss