XLF - New York Community Bancorp: Deal-Breaker Deep Overview Of Risk Profile And Valuation

2023-05-30 07:16:51 ET

Summary

- New York Community Bancorp (NYCB) has emerged as a strong regional banking opportunity due to its acquisition of assets and liabilities from the failed Signature Bank, diversified portfolio, and solid liquidity and capital ratios.

- The bank's risk profile is considered safe, with no red flags in liquidity and capital buffer analysis, making it undervalued compared to its peers.

- Investors should consider the bank's growth potential, strengthened balance sheet, and improved risk profile when evaluating regional banks for investment opportunities.

- The bank is cheap and healthy based on its risk profile-adjusted valuation, whereas other banks in the sector could carry significant risks.

- Due to lower requirements, regional banking bears a greater risk. The analysis provides a comprehensive overview of regional banks based on my assumptions regarding liquidity and capital buffers.

The financial strain in regional banking continues to be justified. Despite the fact that many regional banks fall below the mandatory and Basel III requirements, it should not be sufficient, leaving regional banking in the United States vulnerable. Nevertheless, my bank stock screener revealed a tremendous opportunity in regional banking, a sector I intend to investigate further due to the possibility of solid long-term opportunities. New York Community Bancorp, Inc. ( NYCB ) was the winner of my regional banking stock screener based on the extremely stringent balance sheet criteria, liquidity and capital buffer dashboard, and valuation criteria. I find it extremely intriguing because the company made a shrewd selection of the assets and liabilities of the failed Signature Bank ( OTC:SBNY ). It does not acquire risky private equity loans or crypto-based liabilities. The balance sheet improved significantly as a result of the P&A transaction, making the company more immune to the regional banking stress in the future. Liquidity is very robust, Basel III ratios are satisfactory and provide a buffer, and the company's decline is unjustified despite its recovery. Investors should evaluate regional banks from a risk perspective, and its valuation profile should be modified accordingly. Given that NYCB's balance sheet and long-term growth prospects have vastly improved, the company's stock has become undervalued.

FDIC takeover of Signature Bank

First and foremost, I believe it is crucial to comprehend the nature of the "FDIC takeover" policy. It is crucial for a banking investor to understand how this can occur, what the investor should be aware of, and the state of the regulatory framework.

The issue is more complex, but on a very basic level, bank failures are more prevalent on Fridays. FDIC's primary responsibility is to identify bank problems. Regarding the Silicon Valley Bank, I am of the opinion that insufficient management steps were taken to adequately hedge its portfolio against duration risks and cash outflows from VC firms. The Signature Bank, which is also impacted by crypto-related liabilities, faces similar ongoing issues. However, the issue is more macro-related, as I discussed a few weeks ago in the bearish analysis, as short-term yields on MMF are significantly higher than those on bank savings accounts. Additionally, it relies on substantial and ongoing Fed tightening to combat inflation. Banks with a weak balance sheet and a risky loan and asset allocation may experience significant stress in the event of a bank run.

However, it is crucial for FDIS to examine the individual conditions of banks under financial stress, where the regulator can take corrective action, such as requiring the bank to raise capital, attempt to manage risky loans (by reducing its exposure or selling them on the secondary market), etc.

Mandatory capital ratios are under scrutiny

If the bank did not take immediate steps to improve its balance sheet, it is imperative that the FDIC closely monitor its financial condition. When FDIC decides to "take over," they seek a more nuanced perspective than a single criterion. It is for this very reason that we cannot rely on a single ratio to evaluate the financial health of a bank:

Common Equity Tier 1 Ratio. It incorporates common equity, retained earnings, and high-quality capital into its risk-weighted assets (RWA). According to Basel III, an adequate or "safe" bank must have a capital ratio of 6.5% or more in order to be deemed adequately capitalized. There are also different criteria described later, which needs to be examined. The FDIC may intervene if a bank's requirement criteria fall below mandatory 4.0%. In the event that the Tier 1 Capital Ratio falls below 2%, regulatory intervention may be triggered due to the bank's critical undercapitalization. In this situation, federal law mandates that the bank to be closed and the FDIC appointed as receiver.

If the Total Capital Ratio (Tier 1 and Tier 2) falls below 8%, banks are severely undercapitalized; consequently, the regulator may take action. Monitoring the LCR ratio or Liquidity Coverage Ratio is essential from a liquidity perspective. Significantly more ratios, such as loan-to-deposit, cash-to-deposit, nonperforming assets, and other, are utilized to provide a comprehensive perspective. In addition to these general guidelines, there are additional conditions that, if not met, can result in a bank being taken as receiver by the FDIC, including noncompliance with regulations, poor management practices, ongoing liquidity issues, and failure to meet regulatory obligations.

The problem in regulatory banking is that rules are somewhat less stringent than for GSIBs. Regional banking does not include the treatment of accumulated other comprehensive income, which includes unrealized gains and losses on AVS (available-for-sale) securities. Regional banks have the option to exclude such a requirement (unlike GSIBs), with no impact on CET 1 and mandatory ratios. As an alternative, these banks may utilize the rules from Basel I, where other comprehensive income is generally not included in these ratios.

As we have seen in recent years, avoiding such calculations when presenting capital ratios in a bank's quarterly report can be a matter of moral hazard. Because, if the bank is not adequately hedged, problems may arise. This was the situation with Silicon Valley Bank. From this perspective, regional banking is more susceptible to misinformation than GSIBs, and investors must delve deeply into the bank's financials to comprehend the potential outcomes and risks. In addition, in this article I will attempt to provide extremely in-depth research on NYCB, which I consider to be safe, strengthened by a great transaction, and regulatory compliant.

Examine the transaction

Cherry-picking process

In the second half of March, Flagstar Bank, a wholly-owned subsidiary of NYCB, acquired from the FDIC, in its capacity as receiver, a substantial portion of the assets and liabilities of failed bank Signature Bank.

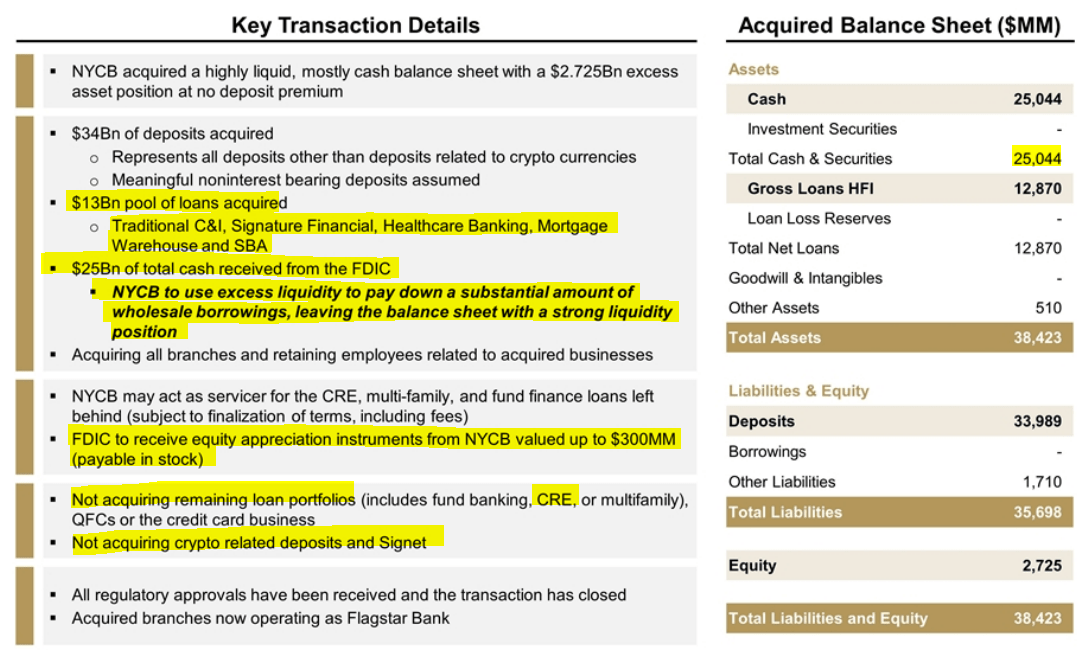

Initially, it is prudent to analyze how the overall P&A transaction evolves. Yes, there is a bidding process for the assets and liabilities of failed banks, but the FDIC must identify a financially sound and secure institution. If the acquirer selects solid assets after completing these steps, these types of transactions can result in significant growth for the acquirer. Typically, the bank obtained a large proportion of healthy assets and liabilities at a substantial discount. That is precisely what occurred :

The Bank acquired only certain financially and strategically complementary parts of Signature that are intended to enhance our future growth. Purchased assets of approximately $38 billion, including cash totaling approximately $25 billion and approximately $13 billion in loans. Included in the $25 billion of cash is $2.7 billion arising from a discounted bid to net asset value. Assumed liabilities approximating $36 billion, including deposits of approximately $34 billion and other liabilities of approximately $2 billion.

{kind=link}

Transaction details (NYCB, SEC)

The loan portfolio becomes more diversified

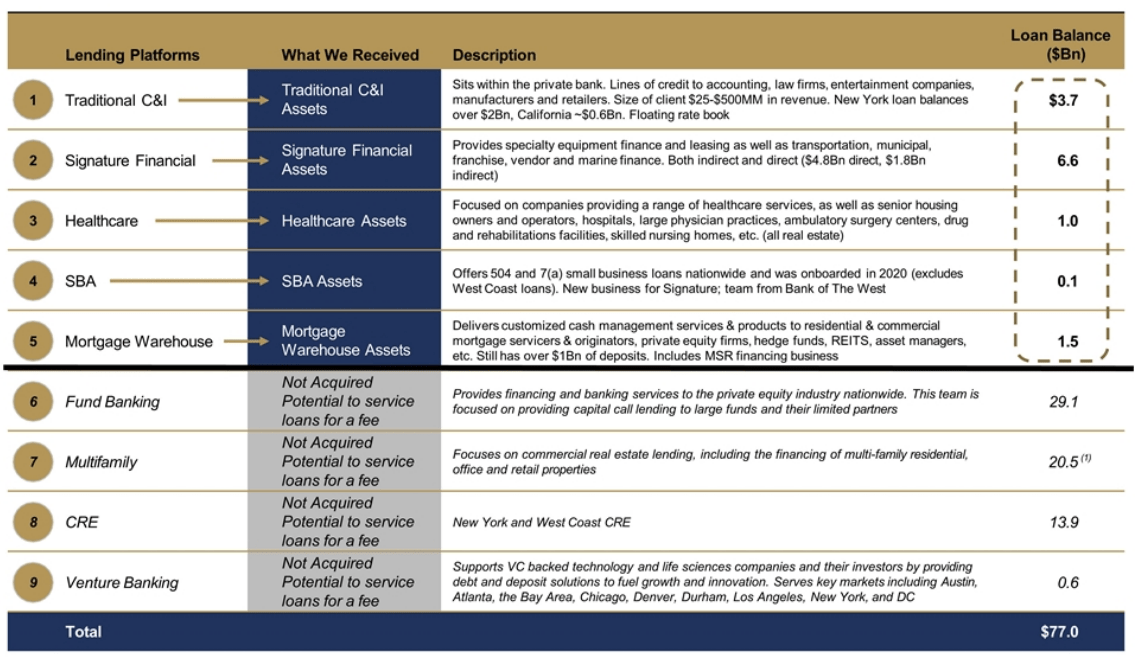

This transaction is absolutely monumental for Flagstar. FDIC receives ridiculous non-cash equity appreciation instruments with a maximum value of $300 million. I am convinced that such a deal-breaker can open up many more opportunities in the future, allowing a company to grow vertically within its former core business - CRE (commercial real estate) and multifamily divisions. These assets were acquired at a substantial discount, totaling $2.7 billion.

Prior to the current macroeconomic cycle, the vast majority of NYCB loans were secured by commercial real estate, making them extremely vulnerable. Now, the overall loan portfolio is less concentrated on CRE, but the diversification gained a new dimension with the addition of key employees, making the transaction even more ideal. NYCB acquired $3.7 billion in traditional C&I, $6.6 billion in Signature financial assets, and other assets.

{kind=link}

Transaction details for loan portfolio (NYCB, SEC)

The next task for management will be to determine how to handle such growth without consuming cash, while maintaining a strong liquidity position and avoiding making new errors. The logical question for management would be whether or not they could replace some employees and use synergy to save money and reduce their workforce. In my opinion, it could be a grave error, as the NYCB lacks experience in the new business segment, and such efforts could impede growth in the very near future.

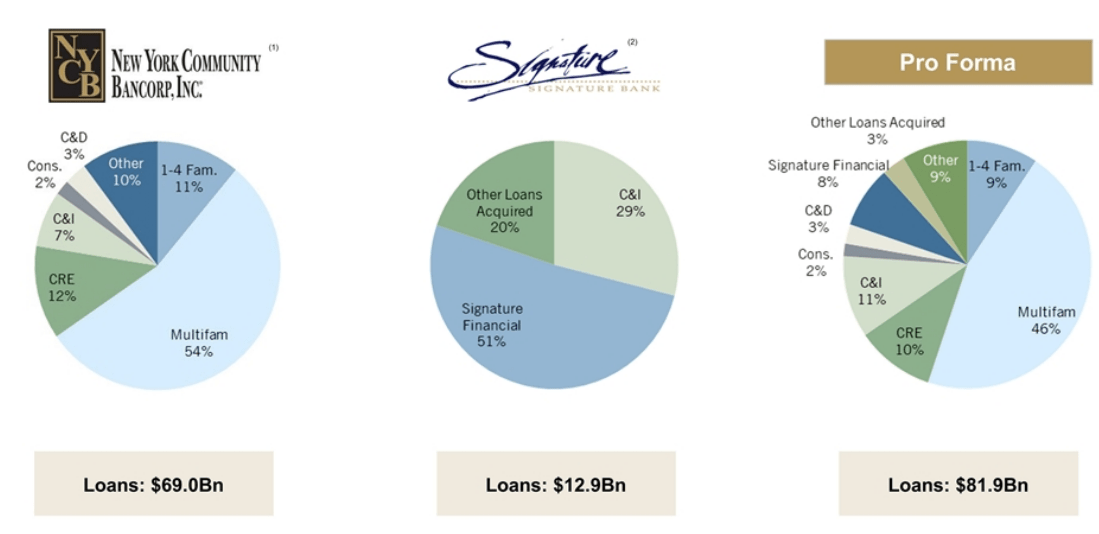

As previously stated, the portfolio becomes more diversified and less reliant on CRE and Multifamily, whose proportion decreased from 64% before the transaction to 55% after the transaction.

{kind=link}

New portfolio allocation (NYCB, SEC)

Financial buffers and crucial ratios

The most important factor to consider when contemplating a possible investment in bank shares is the aforementioned ratios.

{kind=link}

NYCB - Capital ratios (NYCB, SEC)

Considering the following ratios, the company is unquestionably in a comfortable position:

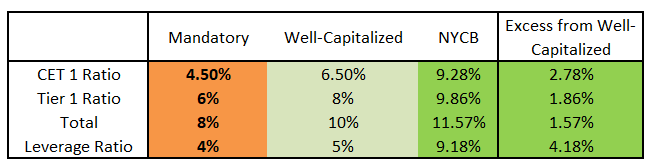

- CET 1 Ratio - Mandatory at 4.5%, more than 6.5% for well-capitalized banks. NYCB has 9.28%. We can consider this a formidable figure.

- Tier 1 Ratio - Required at 6%, well-capitalized banks exceed 8%. NYCB got 9.86%. Additionally, you have a solid appearance.

- Total Ratio - Required 8%. There is room for CCB (Capital Conversation Buffer), which can have additional form of 2.5% if the company has excess capital. It should be created when there is no stress and implemented when potential losses are imminent. As NYCB withholds 11.57 percent, 2.5% is also fully implemented. Therefore, above 10% is highly satisfactory.

- The leverage ratio is also quite robust.

{kind=link}

NYCB - Excess capital from well-capitalized bank (NYCB,SEC)

These ratios are quite impressive, but they are not the best in the industry. However, NYCB provides a substantial buffer or excess from the category "well-capitalized" bank, providing a solid and logical belief that the bank is able to withstand any potential headwinds in the banking industry. Based on the current macro cycle and extremely tight monetary policy, there may still be pressure on businesses and individuals, which could damage the bank's loan portfolio and lead to continued deposit withdrawal.

Previously, I stated that some regional banks can easily avoid certain capital ratios if their AFS portfolio's other comprehensive income is negative. It is not required to be included in capital ratios, unlike GSIBs. However, this is not the case for NYCB at present, as the total comprehensive income is only slightly below net income and the change in net unrealized gain (loss) is only -$7 million (60 million gain from AFS and -67 million USD losses from CF hedges). Even if the group decided to exclude unrealized gains and losses, it would not be a material loss in this instance.

{kind=link}

NYCB - other comprehensive income (NYCB, SEC)

Competition: NYCB is not the one and only

Capital buffers

Regarding these ratios, I would like to note that NYCB is not the holy grail. There are also numerous solid regional banks that are even more secure and have a significantly larger capital cushion than NYCB. Comparing capital ratios revealed a substantial number of banks that are more secure. But these details must be considered in context. I am convinced that there are strong and even better opportunities from a valuation and safety standpoint. However, the majority of regional banks lack the same growth potential and valuation metrics as NYCB.

As previously stated, capital ratios for well-capitalized banks in the United States are

- CET 1 at 6.5% or higher,

- Tier 1 at 8.0% or higher,

- and the total capital ratio at 10%.

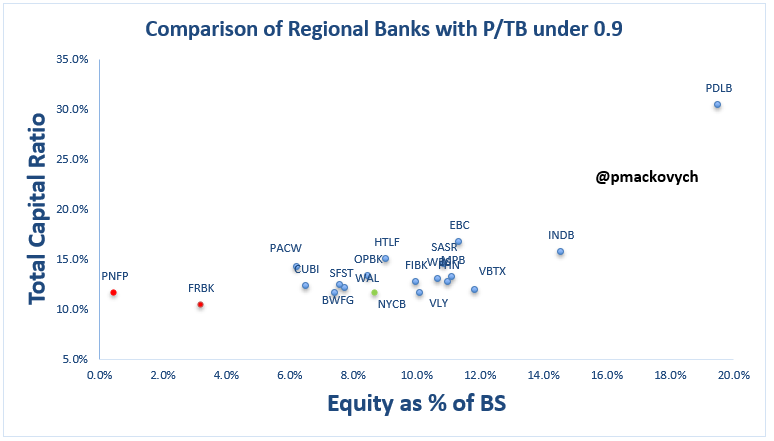

In these times, I would greatly appreciate some sort of positive buffer. I researched "cheap" picks with a price-to-tangible-book ratio of less than 0.90 in an effort to identify undervalued banking stocks. I discovered that there are great companies with excellent ratios.

I initially compared Equity as % of BS and Total Capital ratio as regulatory ratios with a high level of equity. It must be stated that these ratios do not include losses from other comprehensive income, specifically unrealized loss from AFS portfolio. Nonetheless, I do not consider it crucial at this time, as a review of each company reveals only minor changes (losses) resulting from AFS portfolios in selected banks. Nothing that could significantly affect the capital reserves. However, for better and more conservative purposes, I chose my own appropriate ratios, deviating from Basel III and U.S. requirements, described later.

{kind=link}

Comparison of regional banks with P/TB under 0.9 (Author´s calculation. Seeking Alpha)

While none of the selected banks are subject to the "mandatory ratios" I described, Republic First Bancorp, Inc. ( FRBK ) is reaching the exact level of "well-capitalized" at 10% and has been subjected to significant pressures. From this perspective, I also emphasize the importance of analyzing a complex picture, namely the table examined below. Nonetheless, as you can see from the comparison of capital ratios, I consider NYCB to be in good health. However, there are a large number of banks with an even safer capital buffer, the vast majority of them, according to the comparison used. Some of them are well-known institutions, while others are relatively obscure. In the preceding chart, comparisons are displayed, which may be useful for investors in gaining a better understanding of comparison outlook. I would say that there are two possible extremes. The first is low capital ratios, but FRBK and Pinnacle Financial Partners, Inc. ( PNFP ) are the only two banks that do not meet my quite conservative criteria for capital ratios.

However, the opposite extreme occurs when banks have extremely high capital ratios. Even in the event of a recession, total capital ratios greater than 18-20% can be wasteful. It may indicate that banks are unable to utilize their funds and assets in the most effective manner, resulting in a lower return (compared to their peers). It may be the case of Ponce Financial Group ( PDLB ), Independent Bank Corp. ( INDB ), or Eastern Bankshares, Inc. ( EBC ), but I cannot guarantee it. However, additional and extensive research should be conducted to confirm that.

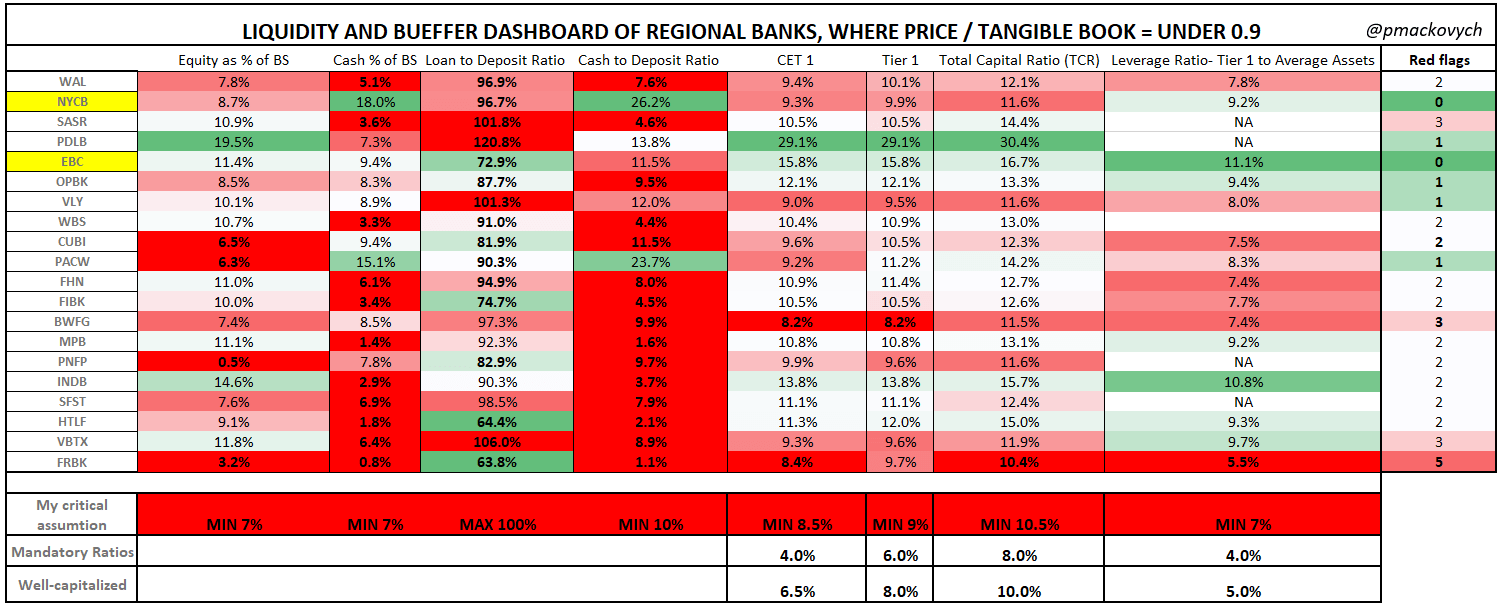

Evaluating the liquidity and buffers dashboard of peers

First of all, I would like to inform you that we must consider more than just the capital ratio. We must also consider additional conditions in the case of liquidity, including my conservative conditions:

- Equity as a proportion of the balance sheet (at least 7%).

- Cash as a percentage of the balance sheet (I want greater than 7%).

- I desire a loan to deposit ratio below 100%.

- My minimum requirement is a 10% cash-to-deposit ratio. This is a bit more complex and dependent on many factors. If the ratio of loan to deposit is lower, there is less need for the ratio of cash to deposit to be higher, and vice versa. When I want to be precise, I would say 20%, but this ratio is so complex that a more general and useful ratio is "cash as a percentage of the balance sheet" in this case.

- I favor higher capital ratios as an additional buffer against the possibility of unrealized losses:

- CET Minimum of 8.5% (200 basis points above "well-capitalized").

- Tier 1 at 9.0% (100 basis points more than "well-capitalized").

- Total Capital Ratio of 10.5% (50 basis points higher than "well-capitalized").

- Minimum leverage ratio of 7.0% (200 basis points above "well-capitalized").

Using a Seeking Alpha filter, I present a comprehensive dashboard of each regional bank's liquidity and capital ratios where price to tangible book (P/TB) is less than 0.90. I'd much rather find a diamond in severely undervalued regional banks that have taken a significant hit and have tremendous potential. For higher image quality, please visit my Twitter .

{kind=link}

Liquidity and buffer dashboard of regional banks with P/TB under 0.9 (Author´s calculation)

My criteria are much more conservative than regulatory ones, and if a bank has 0-1 red flags, liquidity and capital stress should not occur even during a recession or deposit withdrawal. The specifics of the banking sector, however, prevent me from ever being a strong buyer of bank stocks. It is because of its business model and where I always want to explain that even the most well-capitalized bank should not survive a strong bun run. However, creating such a dashboard gave me a great deal more confidence to consider some regional banks to be extremely secure for the first quarter of 2023 (data for 1Q2023), though this could change throughout 2023.

When banks fail to meet some of the aforementioned criteria, a red flag is raised. As I consider eight critical ratios, the bank may receive up to eight red flags. Let's begin with a summary:

- According to my rules, a bank with four or more red flags is uninvestable, and I strongly advise avoiding such stock. It is likely to be a speculative play with a high risk of stock dilution or even bankruptcy in times of economic stress. Moreover, from the selected dashboards, only one bank received this rating: FRBK, which received five red flags. Such a bank has significant equity, liquidity, and capital ratio problems.

- If a bank receives three red flags, additional and in-depth research may be necessary. This bank carries its own risks and must be examined. It is a less speculative play, and there should be no issues during favorable times. Even a sluggish deposit withdrawal or a decrease in pressure could necessitate additional capital funding. Investors should concentrate on their loan portfolio and potential threats. Bankwell Financial Group, Inc. ( BWFG ) and Veritex Holdings, Inc. ( VBTX ) serve as examples.

- If a bank receives two red flags, it may be reasonable to conclude that it is merely healthy (but must fulfil the well-capitalized criteria), with sufficient resources to withstand a potential economic downturn or weak deposit pressures. With strong ones, it could be questionable. It shouldn't be a speculative play, but additional research is also required. Western Alliance Bancorporation ( WAL ), Webster Financial Corporation ( WBS ), and Customers Bancorp, Inc. ( CUBI ) are examples of regional banks with recognizable names.

- If a bank has fewer than one red flag, it is likely that it is healthy, and further research should concentrate on profitability, asset growth, and portfolio. New York Community Bancorp, Inc. is a great example of a company with no red flags and substantial liquidity buffers. The majority of competitors have superior capital ratios, but it and Eastern Bankshares, Inc. ( EBC ) both meet my criteria with zero flags. A potentially troubled bank, PacWest Bancorp ( PACW ), has only one red flag. It appears that the stock market decline has been exaggerated, but a comprehensive analysis of the company's loan portfolio is required to be certain of its future dangers. Some loan segments are more sensitive to interest rates than others and carry greater risk.

The reasons behind my bullish stamp on NYCB Stock

Increased profitability

As stated in the analysis's introduction, NYCB performed admirably during the recent storm and grew significantly stronger. However, it is a fantastic combination:

- Stunning acquisition,

- diversified portfolio,

- expanding asset base,

- solid management steps,

- safe capital ratios,

- solid liquidity ratios,

- attractive valuation relative to its peers,

- and expectation of future profit growth make a group very appealing to me.

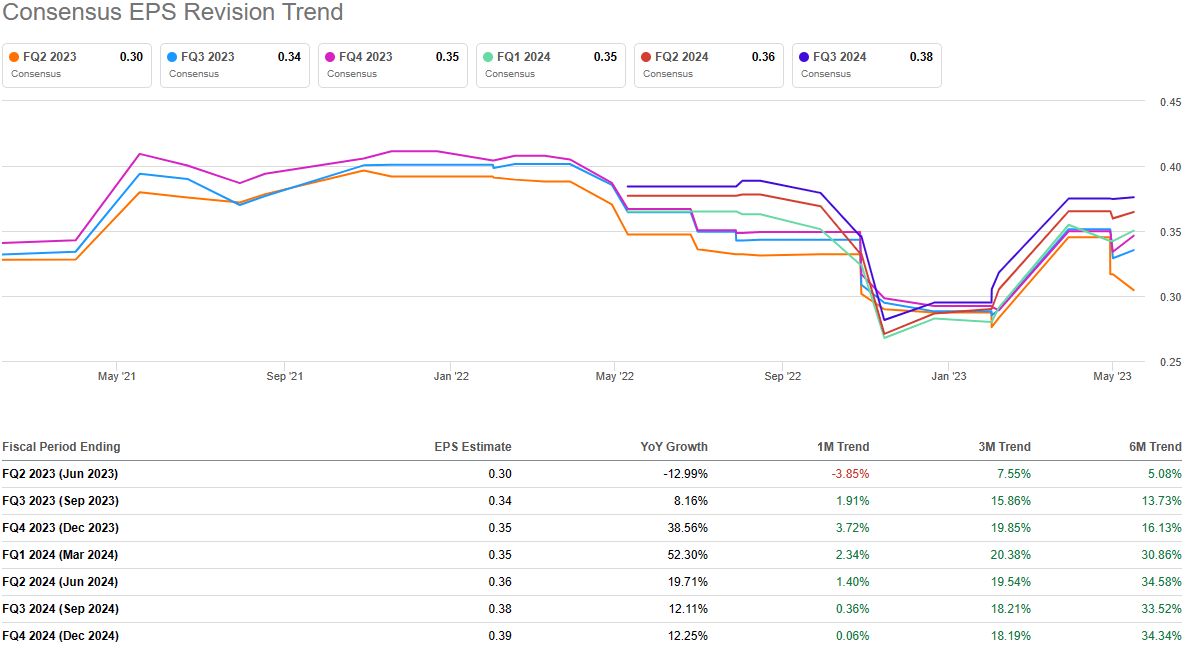

The acquisition of assets and liabilities provides a company with a revitalizing boost. It will earn a substantial amount of additional net income, which has been demonstrated and anticipated by Wall Street, as noted in the Seeking Alpha section . In my opinion, it is too early to tell what the final effect will be, but one thing is certain: the EPS trend has changed from decreasing to increasing. I am convinced that there will be volatility, but I believe it will be positive. The company's growth also received a new boost.

{kind=link}

Consensus EPS Revision Trend (Seeking Alpha)

Adjusted valuation based on risk profile

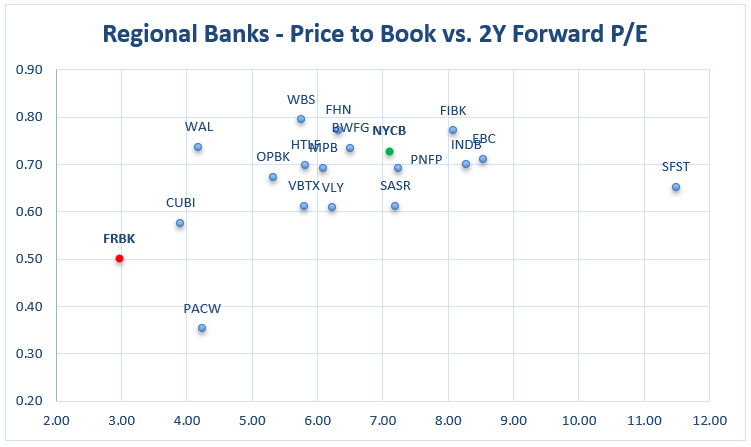

The regional banking sector has taken a hit, but there are some safe and undervalued picks. On the basis of the Seeking Alpha comparison table, I created an XY scatter plot describing 2Y Forward (Dec 2024) Price-to-earnings (P/E) and Price-to-Book. This can be a bit tricky, as I will explain below.

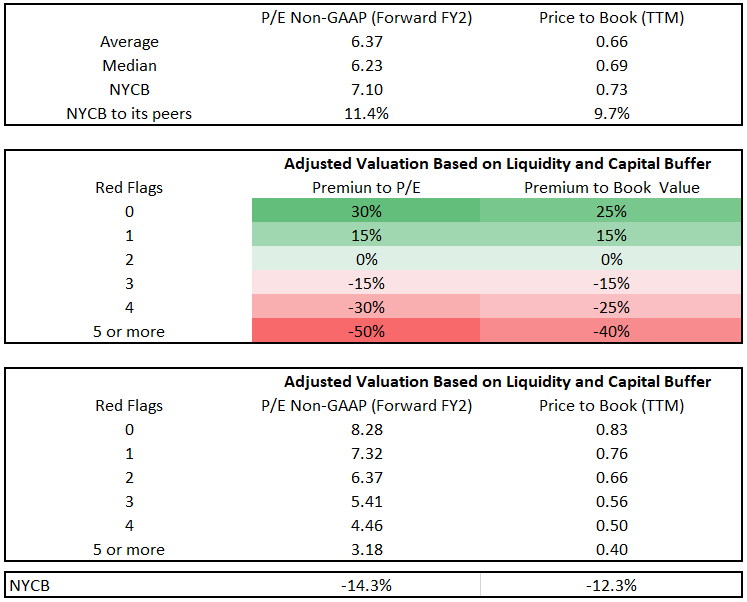

Based on the stocks of the selected regional banks, I calculated a median 2Y Forward P/E of 6.23 and an average of 6.37. The mean P/B ratio is 0.66 and the median is 0.69. The sector premium for NYCB is 11.4% (7.10) and 9.0%, respectively.

{kind=link}

Regional Banks - Price to Book vs. 2Y Forward P/E (Author´s calculation. Seeking Alpha)

Despite the fact that some picks are priced below the industry average, I believe that the most important factor to consider when determining valuation is safety, as reflected by the prominence of liquidity and capital buffers in my dashboard table. I am convinced that banks with zero to one red flag should trade with a much higher premium than those that are in a potential stress scenario. This effect is always reflected in the stock price, as FRBK, WAL, CUBI, and PACW appear to be extremely depressed and have experienced problems. However, I will attempt to determine if the NYCB is under- or overvalued, as it appears to be slightly so based on peer comparisons.

The results of my adjusted valuation based on liquidity and capital buffer (dashboard) are displayed below. Firstly, I'd like to note that this is my subjective opinion, but it makes a great deal of sense to me.

{kind=link}

Premium valuation of industry, based on liquidity and capital criteria (Author´s calculation)

As stated, my top priority is to find a reputable and secure regional bank, and this should be the primary objective. Second, we must adjust this valuation to its red flags criteria, so that these banks trade at a higher premium than their competitors due to their superior quality and safety. Let's assume we should disregard FRBK at this time, despite the fact that it appears to be significantly undervalued relative to its peers, because it has five red flags. Probably, investors should avoid such bank stocks, as the likelihood of dilution or bankruptcy is significantly higher (however, a speculative play would make sense).

Nonetheless, shown below are the current, unadjusted market valuations of P/B and 2Y forward P/E for each bank in the selection versus the average for the selection. According to simple metrics, you should view FRBK as significantly undervalued and NYCB as significantly overvalued relative to its peers, which I believe is incorrect because the market does not price the risks of each bank company fairly. As a result of some form of bank contagion, it is normal for some great and secure banks to still be under substantial price pressure during times of banking stress.

Current valuation vs. industry average 2Y Fwd P/E and P/B (Author´s calculation. Seeking Alpha)

I am convinced that investors should value the stocks, given the low likelihood of bankruptcy or of being appointed as FDIC's receiver, as well as stock dilution. This leads me to a straightforward conclusion. Where the risk of dilution is lower and the quality of the business model is strong, bank stocks should trade at a much higher premium than picks, where the risk of dilution is greater. On the basis of the preceding table and the calculated premium, the valuation adjusted for liquidity and capital buffer should appear as follows:

Adjusted valuation of regional banks based on its risk profile (Author´s calculation. Data from Seeking Alpha.)

On the chart, in the bottom left corner, we can consider these bank stocks to be extremely undervalued relative to their risk profile, as indicated by my dashboard. Note that my valuation metric does not take into account the business model, portfolio allocation, number of insured and uninsured deposits, and other metrics. Nonetheless, based on the criteria listed in the dashboard, I consider these bank stocks to be undervalued relative to their risk profile. Let's assume, for the sake of simplicity, that NYCB trades at a discount of 14.3% to its adjusted fair value, based on 2Y Forward P/E metrics, and at a discount of 12.0% to its adjusted book value. CUBI and PACW are grossly undervalued relative to their risk profiles; however, additional research is required to evaluate all risks and opportunities associated with the aforementioned companies. WAL should also be the following candidate.

Taking into account its risk profile, according to my calculations FRBK is significantly overvalued (+30%) relative to its adjusted price to book valuation and only very slightly undervalued relative to its adjusted 2Y Forward valuation. There is no opportunity in terms of valuation. Nevertheless, based on the current market valuation depicted in the upper chart, FRBK could be considered inexpensive. In my opinion, absolutely incorrect.

Risks and summary

Although I could be wrong, evaluating the banking industry can be somewhat difficult and is not as straightforward as many investors believe. It goes beyond P/E and P/B. I believe that each bank's risk profile should be taken into account. While I see a great opportunity in the banking industry, including regional banking, the process should emphasize business and stock selection considerably more. The banking industry is extremely fascinating to me, but as I've mentioned multiple times, even the greatest and most secure bank could experience significant difficulties during a bank run. Each investor should keep this in mind. NYCB is a very solid bank, and I would likely miss it if the acquisition did not occur. The bank would be even weaker than it is now, and its growth potential would be diminished. Currently, I view it as a solid opportunity, as its portfolio is better diversified, its balance sheet was strengthened by the acquisition, and its risk profile is very solid.

However, investors in the banking sector should monitor the stock more frequently than investors in other industries due to certain risks that are not fully present in other industries. As previously stated, I am convinced that NYCB has a great deal to offer, and based on my dashboard and risk profile, there are several other banks, including CUBI, PACW, WAL, and others, that should be the subject of additional research. I believe that this analysis assisted you in comprehending and revealing the details of NYCB and regional banking, as well as how an investor should view them. If you enjoyed my work, I would appreciate your follow or a discussion regarding potential improvements.

For further details see:

New York Community Bancorp: Deal-Breaker, Deep Overview Of Risk Profile And Valuation