NYT - New York Times: Undeserving Of Its Premium Valuation

2023-12-14 12:05:00 ET

Summary

- The New York Times Company has built a successful digital business with over 9.4 million subscribers, accounting for 60% of total revenue.

- NYT trades at a premium valuation to the broader market and in line with Netflix.

- NYT has struggled to grow digital ARPU over the past few years suggesting the company has limited pricing power.

- The company's print business still contributes a significant portion of revenue and is facing secular challenges.

- I am initiating NYT with a sell rating as I do not believe it is worth its premium valuation.

The New York Times Company ( NYT ) has weathered challenges to the traditional print media business far better than most peers. The company has built an impressive digital business with over 9.4 million subscribers.

Digital revenue now accounts for ~60% of the company's total revenue and primarily consists of subscription based revenue up from 45% a decade ago. Success in the digital business has allowed NYT to deliver solid returns for investors. Over the past 10 years, NYT shares have delivered a total return of 273% compared to a total return of 205% delivered by the S&P 500.

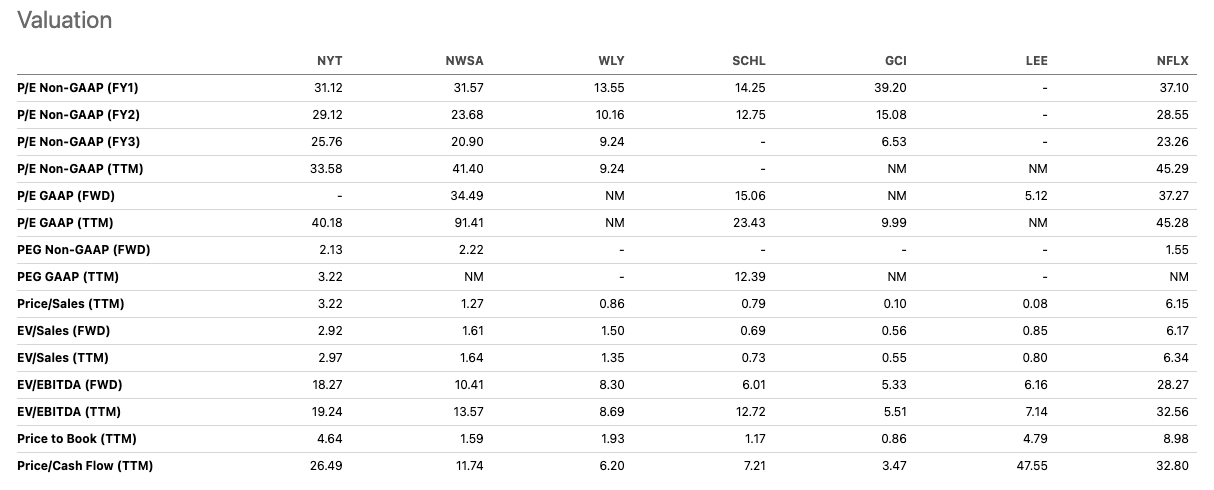

NYT currently trades at 29x consensus FY 2024 EPS estimates and 25.8x consensus FY 2025 EPS estimates. Comparably, Netflix ( NFLX ) trades at 28.5x consensus FY 2024 EPS estimates and 23.3x consensus FY 2025 EPS estimates.

While NYT and NFLX both are subscription based businesses, I do not believe NYT deserves to trade at a similar valuation to NFLX. NYT faces more competition than NFLX, offers subscribers a less compelling value proposition, has lower growth potential, and remains heavily exposed to a declining print business.

I believe NYT should trade more in line with peers such as News Corp ( NWSA ) and Gannett ( GCI ) which trade at 23.7x and 15x forward EPS respectively. Thus, I believe NYT is not a compelling investment at current levels.

The News Business Is Highly Competitive

NYT operates in a highly competitive business. Beyond peers Gannett and News Corp, competitors include the Washington Post, The Financial Times, and many other local smaller players. NYT also competes with traditional video and digital news service providers such as CNN, Fox News, BBC News, NBC, and others.

In addition to these competitors, NYT also faces competition from social media products such as Meta Platforms, X, LinkedIn, and others which allow individuals and companies to share news directly with followers.

NYT has been able to succeed despite high levels of competition due to its strong brand and high quality content. However, competition remains a constant treat and limits NYT's pricing power as consumers have so many alternatives.

As shown by the chart below, NYT has been able to generate high single digit profits margins. This compares favorably to peers such as NWSA and GCI which have struggled to post positive profit margins. However, NYT's margins remain well below NFLX which has been generating a mid-teens level of profit margin.

While NFLX also faces a significant amount of competition the degree of competition is somewhat lower than the degree of competition facing NYT as players must have massive scale to effectively compete. NFLX's primary competitors are large platforms operated by Disney ( DIS ), Comcast ( CMCSA ), Paramount ( PARA ), and Warner Bros. Discovery ( WBD ). NFLX has an estimated ~20% market share of the streaming market. Comparably, NYT faces competition from both large and small media news organization as the benefits due to scale and barriers to entry are more limited in the news business.

Axios represents an excellent example of how a news media company can rapidly enter the market and gain share from entrenched players. Axios was founded as an online news platform focused on politics in 2016. In 2022, the company was sold to Cox Enterprises for $525 million.

While low margins are sometimes views as a positive in that they offer potential for improvement, I believe that argument applies mostly to companies with margins well below peers. Currently, NYT has much better profit and EBITDA margins compared to peers NWSA and GCI. Thus, I am skeptical that NYT will find it easy to improve margins from current levels as they are already best in class. To the contrary, in a market which continued to become increasingly competitive I believe NYT may find it difficult to maintain margins above industry peers.

Strong Q3 Results But Pricing Power May Be Limited

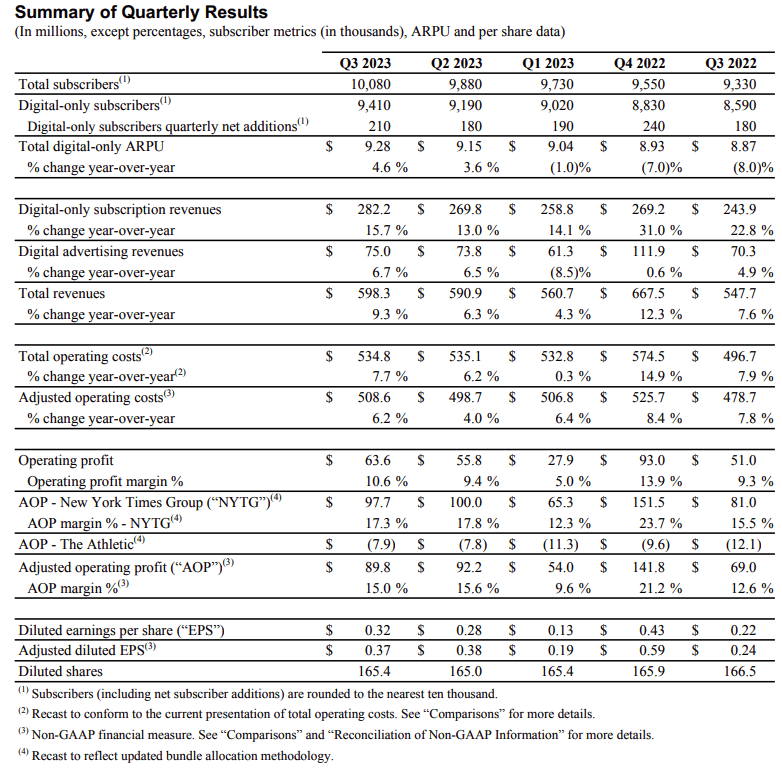

On November 8, 2023 NYT reported better than expected results. The company reported Adjusted EPS of $0.37 which beat estimates by $0.08 and represents a $0.13 increase from the same period a year ago. Revenues came in at $598.3 million, up 9.2% compared to the same period a year ago, and $8.9 million better than consensus estimates.

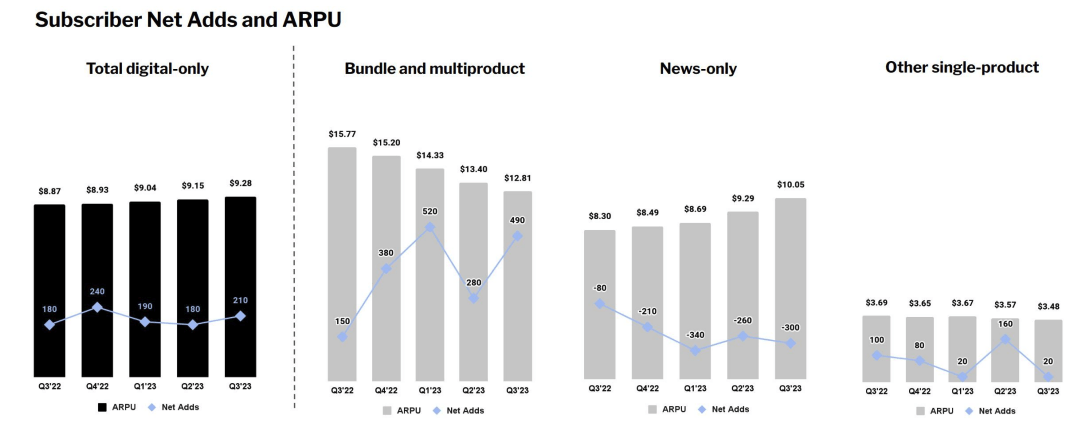

The strong results were driven by solid digital subscriber growth, digital advertising growth, and digital ARPU growth. Digital-only subscribers increased by 210,000 or ~2.4% compared to Q2 2023 and by 820,000 or 9.5% compared to Q3 2023. Digital ARPU increased by 4.6% on a year-over-year basis to $9.28.

The improvement in digital ARPU is noteworthy as the company had reported declines in digital ARPU during Q1 2023, Q4 2022, and Q3 2022. That said, digital ARPU still remains below 2021 levels. Thus, I am concerned that the company may have a limited ability to raise prices from here.

Currently, NYT offers its online all access subscription for $6.25 per week. However, the company's current promotion offer allows new users to sign up and pay just $1 per week for the first 6 months. The fact the digital ARPU remains at just $9.28 compared to a full monthly subscription cost of $25 is somewhat concerning given the maturity of the service. The significant difference suggests that a high percentage of users are signing up for promotional offers and not converting to full paying users.

It is interesting to point out that NFLX reported similar subscriber growth during Q3 2023 of 10.8% on a year-over-year basis. NFLX reported average revenue per membership of $16.29 for its U.S. and Canada business. Given the significant amount of content available on NFLX, I think it is difficult to argue that the NYT subscription for $25 per month is extremely compelling given that it offers a much smaller amount of content.

{kind=link}

NYT Q3 Earnings Release

{kind=link}

NYT Q3 Earnings Release

Seeking Alpha

Significant Exposure To The Print Business

Despite its evolution to become a digitally focused company, NYT still derives significant revenue from its print based business. Print subscription revenue accounts for ~23% of the company's revenue and declined by 1.8% during Q3 2023 on a year-over-year basis. Print advertising revenues account for ~7% of the company's total revenue and increased by 4.8% during Q3 2023 on a year-over-year basis. Thus, performance of the company's print business has been fairly resilient despite industry headwinds.

However, I believe the print business will continue to experience secular challenges over the next few years and will serve as a challenge for the company to navigate.

While NYT does not report a separate profit margin for its digital vs print business, current levels of profitability are roughly in line with historical averages. Thus, this data point suggests that as the company becomes more digitally focused profit margins may not expand significantly. I believe the reason for this is that the print newspaper business actually has much higher barriers to entry then the digital news business. For this reason NYT has better pricing power in its print business compared to its digital offering though the cost in the print business are higher. Currently a full price print + all access subscription costs $10 per week or $40 per month compared to the all-access digital only offering which costs $6.25 per week or $25 per month.

Growth Potential

Wall Street Analysts expect NYT to grow EPS at a rate of 6.9%, 13%, and 7.6% for FY 2024, FY 2025, and FY 2026 respectively. Comparably, NFLX is expected to grow EPS at a rate of 30%, 22.7%, and 18.8% for FY 2024, FY 2025, and FY 2026 respectively.

Given these growth rates, I believe it is clear that NFLX is a faster growing company than NYT.

NYT's traditional media p eer NWSA is also expected to grow EPS at a rate of 41.8%, 33.3%, and 13.3% for FY 2024, FY 2025, and FY 2026.

Based on these comparisons, I do not find NYT to be a highly compelling earnings growth story. While the digital business presents a growth opportunity, I believe the price point limits potential future growth for the stock. NYT may be able to grow earnings in line with current estimates but this level of growth is not dissimilar to the level of earnings growth I expect from the S&P 500 over the next few years.

Valuation

NYT trades at 29x consensus FY 2024 earnings. Even after backing out the company's $587.8 million in cash, NYT still trades at ~26.7x consensus FY 2024 earnings.

Comparably, the S&P 500 trades at ~18.9x consensus FY 2024 earnings. Simply put, I do not believe NYT is worth the premium.

Historically, over the past 10 years NYT has grown EPS at a 0.2% CAGR. More recently, over the past 3 years the NYT has grown EPS at a 7.3% CAGR. The company is expected to grow FY 2024 earnings at 6.9%. Comparably, the S&P is expected to grow earnings at ~12%. Thus, I do not find NYT compelling relative to the broader market.

NYT's current valuation puts it in line with NFLX on a forward P/E basis. I believe this highlights how overvalued NYT currently is as NFLX represents a higher quality business. At its core, I believe NYT's subscription offering is a less compelling value proposition than NFLX's suite of offerings. Moreover, NYT continues to have significant exposure to the print media business which is in secular decline.

I believe NWSA and GCI represent more reasonable comparable companies for the NYT. NWSA trades at 23.7x forward earnings while GCI trades at 15x forward earnings. Thus, the average of these suggests that NYT could trade at ~19.3x earnings and be roughly inline. Based on FY 2024 EPS estimates of $1.60 I believe a reasonable valuation for NYT is ~$31 per share, versus it's recent trading price of $47.

{kind=link}

Seeking Alpha

Potential Upside Catalysts

Perhaps the biggest upside catalyst for NYT would be if the company is able to bridge the gap between its current digital ARPU of $9.28 and the cost of its core online digital offering of $25 per month. A convergence of these two numbers would suggest that NYT has a reasonable degree of purchasing power which could allow for long-term earnings growth.

While I believe it is possible that NYT is able to increase ARPU from current levels, I am skeptical that is has substantial pricing power given the value offered by NFLX for a substantially lower cost.

Another potential upside catalyst could emerge if the company were to explore a sale. NYT remains a highly valuable brand and could attract significant interest if it were to be put up for sale. However, I view this as highly unlikely given the fact that the controlling Ochs Sulzberger family has ~90% of Class B shares which allows for the election of 70% of the company's board.

Finally, a more aggressive share repurchase program would also be a potential upside catalyst. In February 2023, NYT Board of Directors approved a $250 million increase in the repurchase authorization bringing the total authorization to $250.5 million. This authorization represents ~3.2% of shares outstanding at current levels and thus is fairly modest. Additionally, the company has been slow to repurchase shares historically despite carrying a relatively high cash balance. This suggests that management does not view the stock as undervalued at current levels. I would view a more aggressive repurchase program as a positive.

Conclusion

NYT has done an excellent job in managing a substantial disruption of its core print media business. The company has built a strong online subscription based business with solid growth potential. However, the print media business remains a significant part of the company's business and is exposed to further weakness due to secular challenges.

Growth potential for the company's digital offerings may be somewhat limited due to fierce competition in the news media business which limits NYT's pricing power.

NYT is trading at a fairly high valuation which is in line with NFLX and substantially above the S&P 500. I do not believe this valuation is warranted given the fact that the company has only moderate growth prospects.

I am initiating the stock with a sell rating and would consider upgrading the stock if the valuation picture improves and the company shows sustained growth in ARPU. I would also consider upgrading the stock if the controlling Ochs Sulzberger family were to consider putting the company up for sale.

For further details see:

New York Times: Undeserving Of Its Premium Valuation