NREF - NexPoint Real Estate Finance And The Dondero Complex

2023-03-23 16:09:09 ET

Summary

- This article takes a look at mortgage REIT NexPoint Real Estate Finance and their focus on multi- and single-family rentals.

- Specifically, I'll provide reflections regarding the value of their Series A preferred shares NREF-A. We'll review the company's finances and portfolio overall.

- James Dondero is an outsized figure in this story. We will get to him. And in the course of it, there's another name you might recognize.

- Read on for why I'm avoiding.

Another commercial mREIT that I have not covered yet is NexPoint Real Estate Finance Trust (NREF). Their primary focus is in multifamily and single family rental with life science, hospitality, and office sectors thrown in. The REIT is managed by NexPoint Real Estate Advisors as part of the overall NexPoint alternative investment platform .

Besides the common stock, this REIT also has a preferred stock: NREF.PA . My focus will be on this security, but we will discuss the company broadly including the portfolio and management.

Structure Of The NREF-A Preferred Shares

There are 1.645 million shares outstanding of these cumulative preferreds. They were originally issued at par value of $25.00 with an 8.50% coupon. Today this annual dividend amounts to $2.13.

At the time of writing NREF-A is trading at a price of $20.05 meaning the annual dividend yield is 10.62%. Across a universe of nearly 700 preferreds the average dividend yield is 8.03% with a standard deviation of 3.20%. That suggests this preferred is trading in the upper end of this range with the double digit yield.

These dividends are paid out quarterly.

Shares were originally issued in July 2020 and have no maturity. But they can be redeemed after their first call date in July 2025.

| NREF-A |

| Type |

| Cumulative Redeemable |

| 1st Call Date |

| July 2025 |

| Price |

| $20.050 |

| Coupon |

| 8.50% |

| Current Yield |

| 10.62% |

Overview Of NexPoint Real Estate Finance Trust's Finances

On February 23, 2023 the company announced fourth quarter and full year earnings for 2022 which saw them bring in $61.8 million ($2.75 per share) in distributable earnings for the year. This established a two year trend of double-digit distributable EPS growth.

| Distributable EPS |

| YoY Growth % |

| 2023 |

| $2.75 |

| 45.50% |

| 2022 |

| $1.89 |

| 29.45% |

| 2021 |

| $1.46 |

Strength of earnings drove management to announce a Special Dividend on the common shares totaling $0.74 for the year paid out in $0.185 per share increments each quarter this year. This is on top of the standard $0.50 quarterly dividend representing a 37% increase for this cycle.

| Common Dividend |

| $2.00 |

| Special 2023 Dividend |

| $0.74 |

| Total Expected 2023 Dividends |

| $2.74 |

If there is enough cash and cash flow that they are able to pay a special dividend on top of their standard common dividend, it stands to reason that the preferred dividend is not at risk here. With the 1.645 million in preferred shares paying $2.13 annually this comes out to an expense of $3.5 million. Earnings available for distribution in this case covers the preferred dividend by a whopping 17x.

Taking the three-year average of distributable earnings between 2021-2023 we'd get a value of $2.03 per share or around $46 million. With this estimate the preferred dividend is covered a mere 13x.

Let's turn to the balance sheet though. While their earnings announcement happened a month ago, the company has not yet filed their related 10-k. But we can use the data provided in their investor presentation to get the picture of it.

NREF February 2023 Investor Presentation: Balance Sheet.

The company has Total Stockholders Equity reported at $384.7 million. Preferred equity is $41.1 million leaving common stock equity at $343.6 million - this translated to a Stock Equity/Preferred equity coverage over 7x. It's another measure which suggests support for the preferred's value.

I'm calculating total debt at $1,263 million by excluding the accounts and bonds payable line items from liabilities. Total book value of the company inclusive of the Operating Partnership interests but excluding the preferreds is $444.8 million. That brings my calculation of debt-to-equity to 2.84x which is not as levered as some in this space.

Stockholder equity value looks a bit thinner from this perspective yet the strength of earnings over the recent path has more than supported these debt levels. One way we can think about this is the distributable earnings return on equity. Book value per share is $20.11 which they generated $2.75 in distributable earnings from translating to an ROE of 13.67%.

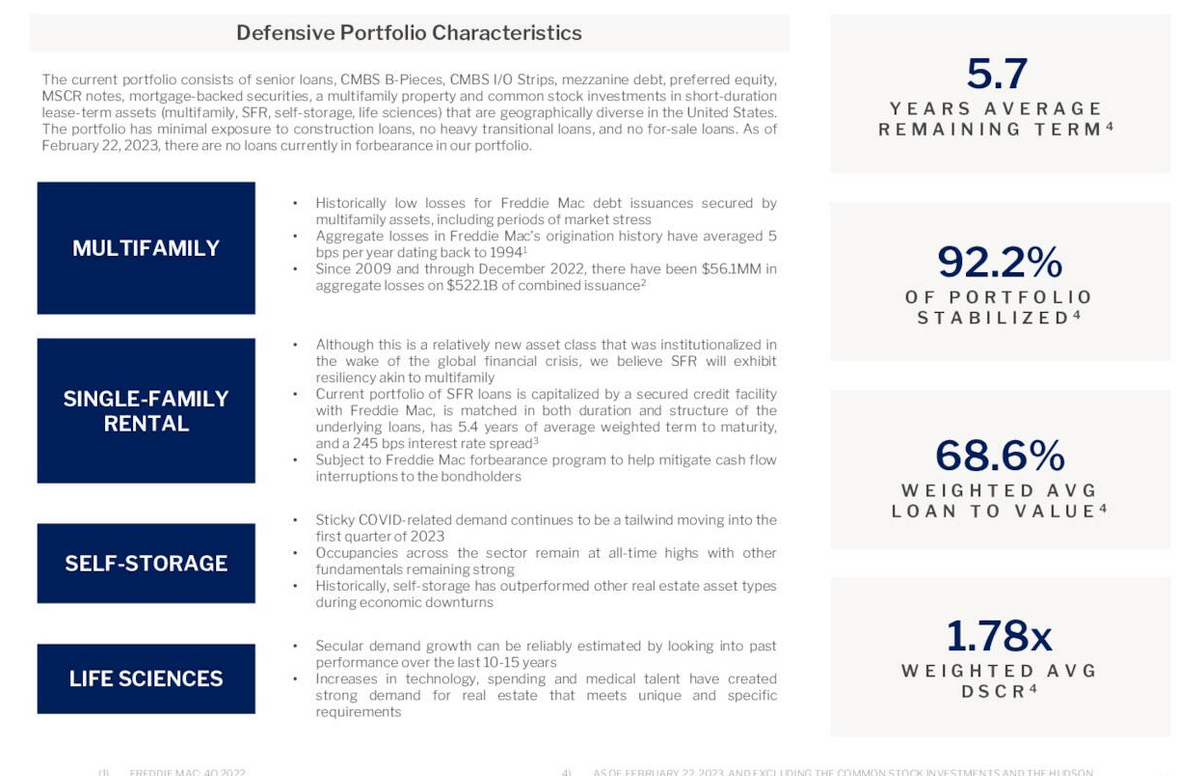

Portfolio Characteristics

Weighted average loan-to-value in their portfolio is 68.6% with $1.7 billion in current principal. Geographically this portfolio is diverse with a slight bias toward the Southeast and Southwest markets.

NREF February 2023 Investor Presentation: Portfolio Highlights.

From this we can see that primarily the REIT is invested in multifamily (53%) and single family rentals (43%) accounting for 96% of the portfolio. Both of these sectors have seen sustained growth recently with inflation driving rental increases. Management is opportunistic about the vehicle they invest through as evidenced by their broad range of investment types. Senior loans account for the bulk (40.8%) with CMBS B-Pieces (34.8%) coming in second. Then there are five other classes of investments from preferreds to mezzanines to IO strips.

Management believes this to be a defensive portfolio. They note " the portfolio has minimal exposure to construction loans, no heavy transitional loans, and no for-sale loans. As of February 22nd, 2023, there are no loans currently in forbearance in our portfolio. "

NREF February 2023 Investor Presentation: Portfolio Highlights.

{kind=link}

The Dondero Complex

All the financials look in decent order and the portfolio indeed seems defensively positioned amidst a likely downcycle. My stumbling block is over the Dondero Complex.

James Dondero is the President and Chairman of NREF. He's also the President of the LP which owns the external manager of NREF. Then there's NexPoint Residential Trust ( NXRT ) which he is similarly President and Chair of the board, and NexPoint Hospitality Trust where he's CEO.

That's a lot of positions to juggle.

Earlier in Dondero's career he founded Highland Capital Management in 1993. The firm is credited with designing the first software to electronically track loan portfolios in the early aughts. They shifted into the mutual fund space around this time where they ended up with the Highland Global Allocation Fund ( HGLB ).

Highland Capital Management filed for Chapter 11 bankruptcy protection in October 2019 amidst a legal battle with investors. Ironically for a man who has a history of buying distressed credit, his own LP apparently owed a $189.3 million debt to investors in its own shuttered Highland Crusader Fund which folded in 2008.

Reorganization efforts resulted in a corporate governance settlement agreement to remove Dondero as director and officer of Highland Capital in January 2020. He remained on as an unpaid portfolio manager. Here's a little color from Dondero's own behavior subsequent to that:

"Throughout summer 2020, Dondero proposed several reorganization plans, each opposed by the Committee and the Independent Directors. Unpersuaded by Dondero, the Committee and Independent Directors negotiated their own plan. When Dondero's plans failed, he and other creditors began to frustrate the proceedings by objecting to settlements, appealing orders, seeking writs of mandamus, interfering with Highland Capital's management, threatening employees, and canceling trades between Highland Capital and its clients. See Highland Cap. Mgmt., L.P. v. Dondero (holding Dondero in civil contempt, sanctioning him $100,000, and comparing this case to a "nasty divorce"). In Seery's words, Dondero wanted to " burn the place down " because he did not get his way. The Independent Directors insisted Dondero resign from Highland Capital, which he did in October 2020."

A " nasty divorce " indeed. Which reminds me of another thing I heard about Dondero once. Something to do with his actual wife (don't worry, Highland's still involved). This is from a Dallas Observer article dated November 2013.

"Last we checked some 17 months ago, Dondero was legal-feuding with two people . One was his wife, whom he accused of infidelity and was in the process of divorcing. The other was a former Highland Capital Management business partner named Patrick Daugherty, who was booted from Highland in September 2011 for being " megalomaniac ," and who was " unmanageable, erratic and insubordinate " and went on abusive tirades against employees, according to court filings.

Things got very weird very quickly. Dondero reportedly believed his wife was cheating on him with Daugherty . Daugherty, in turn, accused his former business partner, whose income was $36 million in 2010, of hiding assets to avoid paying his wife spousal support, a claim he first unveiled in a legal filing describing a very weird dinner scene in which Dondero said he had 20,000 emails and texts, obtained from sources in " certain branches of the intelligence community, " proving his wife was being unfaithful."

Dondero went on to tell a judge that he was unable to pay divorce proceedings claiming he was insolvent and only makes " a million, two " a year.

The Institutional Investor produced an excellent piece reporting on this Hedge Fund Soap Opera in April 2020. It paints a damning portrait of the man.

Institutional Investor: A Damning Portrait.

Consider this tidbit offered in the article:

"Almost no one contacted by Institutional Investor would speak on the record for this story, for fear of legal reprisal. Those fears are well founded: Thousands of pages of legal documents show that Highland's co-founder and current chief executive, James Dondero, is not afraid to wage the legal equivalent of war - and doesn't back down when the courts don't rule in his favor."

This man is the one managing your money if you are invested in NREF. And he's been amidst legal war with Highland Capital Management over an issue that dates back to 2008. What's really alleged in that court case is that Dondero and management at Highland never paid their investors what they were owed.

The bankruptcy effort of Highland Capital may be a self-preserving tactic in-and-of-itself. Recall that they filed for Chapter 11 due to the $189 million they owed creditors from 2008 because it may not have enough liquid assets to cover the judgment. Yet Highland operates over billions in capital in other entities on their platform (like NREF, NXRT, HGLB, and HFRO), none of which were filing for bankruptcy.

But what this means is that management contracts and capital involved around NREF are engulfed in the matters of Dondero. So much so with Highland that they specifically note it in the company's risks as " Risks associated with the Highland Capital Management, L.P. ("Highland") bankruptcy, including related litigation and potential conflicts of interest ." This was as of their Q3'22 filing in November .

And those matters magnified even further in February 2023 when the Swiss Bank UBS ( UBS ) brought a suit alleging Dondero and Highland's former chief legal officer have " conspired for over a decade to frustrate UBS's ultimate recovery by systematically draining the judgment debtors' assets. " They are looking to recover more than $1 billion.

I'll be clear in stating I do not believe that NREF's assets are at risk amidst this -- I'm more noting that the stock price may be whimsy to potential forced selling if Dondero needs to pay out something.

Insider Ownership Review

I don't typically spend this much time detailing the history of a single person. Nonetheless, Dondero had a biography worth reading. For those interested in owning the preferred shares of NREF I find some things perhaps illuminating from this review.

For one, I trust something Warren Buffett said when he thinks about hiring, " In looking for people to hire, you look for three qualities: integrity, intelligence, and energy. And if they don't have the first, the other two will kill you. "

Buying stock in a company is in part hiring a management team with the task of growing your capital. Integrity is the litmus test - Dondero seemingly possesses little.

What he does possess, on the other hand, is 29,810 shares of NREF-A which he's been accumulating since June 2022 where he started with just 5k. Here's some data pulled from Fintel .

| Trade Date |

| Insider |

| Ticker |

| Code |

| Price |

| # of shares |

| Remaining Shares |

| 2022-09-26 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.50 |

| 4,463 |

| 29,300 |

| 2022-09-26 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.50 |

| 537 |

| 19,511 |

| 2022-09-23 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.70 |

| 6,111 |

| 24,837 |

| 2022-09-23 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.70 |

| 734 |

| 18,974 |

| 2022-09-22 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.77 |

| 1,280 |

| 18,726 |

| 2022-09-22 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.77 |

| 154 |

| 18,240 |

| 2022-09-21 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.70 |

| 237 |

| 17,446 |

| 2022-09-21 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.70 |

| 29 |

| 18,086 |

| 2022-09-20 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.75 |

| 585 |

| 17,209 |

| 2022-09-20 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.75 |

| 70 |

| 18,057 |

| 2022-09-19 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.75 |

| 652 |

| 16,624 |

| 2022-09-19 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.75 |

| 78 |

| 17,987 |

| 2022-09-16 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.85 |

| 1,428 |

| 15,972 |

| 2022-09-16 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.85 |

| 172 |

| 17,909 |

| 2022-09-15 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.83 |

| 1,757 |

| 14,544 |

| 2022-09-15 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.83 |

| 211 |

| 17,737 |

| 2022-09-14 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.90 |

| 4,287 |

| 12,787 |

| 2022-09-14 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.90 |

| 515 |

| 17,526 |

| 2022-09-06 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.80 |

| 2,550 |

| 17,011 |

| 2022-09-01 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.75 |

| 1,250 |

| 14,461 |

| 2022-09-01 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.80 |

| 1,637 |

| 13,211 |

| 2022-08-30 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.80 |

| 413 |

| 11,574 |

| 2022-08-08 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $23.95 |

| 4,590 |

| 11,161 |

| 2022-08-04 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $24.00 |

| 410 |

| 6,571 |

| 2022-07-06 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $24.80 |

| 1,132 |

| 6,161 |

| 2022-06-16 |

| DONDERO JAMES D |

| NREF-A |

| P - Purchase |

| $24.64 |

| 5,029 |

| 5,029 |

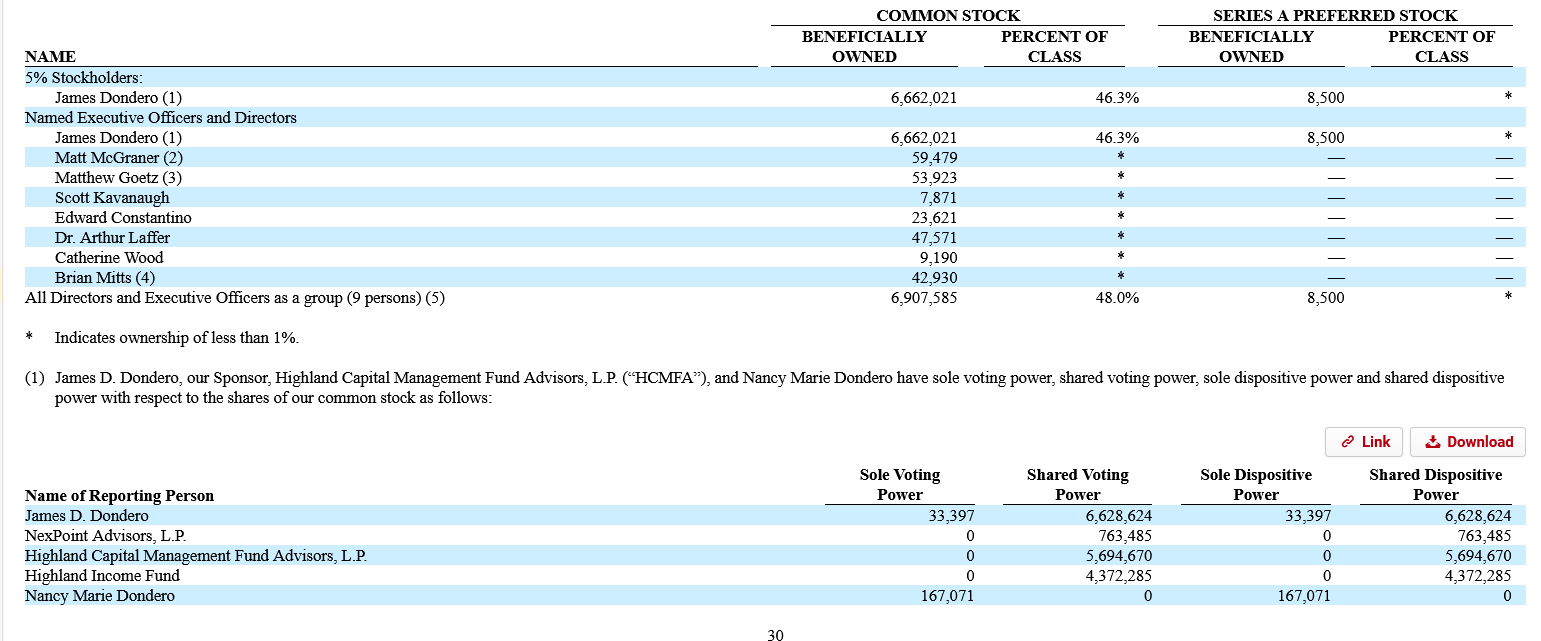

Average purchase price was $23.85 which is nearly 19% higher than current prices. When we look at the proxy from last year (which is a bit dated given it's from April 2022 ) we can see that he's tied to common ownership.

2022 Prospectus: Insider Ownership.

{kind=link}

What's of note is that the vast majority of the shares (~86%) represented as owned by Dondero are actually owned by the sponsor Highland Capital Management. A majority of that is owned directly through their traded Highland Income Fund.

Taken together they beneficially own 46.3% of NREF. With Highland Capital still caught up in litigation which could cost them, I'd be conscious of these interests and downstream impact on their holdings if they see adverse rulings.

What Does Cathie Wood Have To Do With It?

Admittedly, very little. But, keen readers will have perhaps gleaned another notable name in this drama, ARK Investment's CEO Cathie Wood ( ARKK ). Ms. Wood was brought on to NREF's board in July 2020 as an independent director. She's also a director over at NXRT - so she's tied to the broader NexPoint platform.

Investor Takeaways

What started as a rather mundane exploration of a pretty standard preferred security led me down an Alice in Wonderland type rabbit-hole. As I said, the Dondero complex is a stumbling block I could not get over because I fell into researching it. While NREF-A offers above average dividend yield, seemingly good earnings coverage, and balance sheet support it's also ultimately tied to James Dondero.

And with Highland Capital's outsized stake in the firm the stock price will likely be impacted by whatever litigation they are involved in. Everything about the last fifteen years has suggested one thing for Highland - more litigation is to come. And with UBS seeking over $1 billion in claims this is not chump change.

For those who have a bit more comfort with this situation than I do, then these preferreds may look attractive. But all I've learned about James Dondero suggested that I would not be investing alongside a trusted partner. That is enough for me to pass on the security.

For further details see:

NexPoint Real Estate Finance And The Dondero Complex