NXGN - NextGen: Potential Thoma Bravo Deal Inching Closer - A Look At The Moving Parts

2023-09-06 09:40:10 ET

Summary

- Private equity firm Thoma Bravo is reportedly nearing a deal to acquire NextGen Healthcare, Inc.

- NextGen Healthcare is a platform company that helps healthcare providers with patient documentation and revenue cycle management.

- Wall Street analysts have been bullish on NXGN stock, with revisions higher to revenues and earnings in the last 3 months.

NextGen Healthcare investment summary

Since the last publication on NextGen Healthcare, Inc. ( NXGN ) in May, there have been multiple investment updates. Chief among these, private equity firm Thoma Bravo is reportedly moving closer to a potential deal to acquire NXGN. While no official announcement has been made, discussions have intensified and may lead to a formal agreement as early as this week. Here I'll cover all the relevant details and what to make of the investment case going forward. I would stress, given the lack of financial details surrounding the potential transaction, that I am retaining my previous rating on the company as a buy. However, this may be subject to change depending on what Thoma Bravo puts forward, if anything at all.

Critical facts to investment debate

As mentioned, Thoma Bravo is said to be nearing a deal with NXGN. I would point out that no final decision has been reached, and the private equity player has kept its reservations on any talks of the deal. Discussions could still fall through, but based on what's been reported to date on several wires, on a bounce of probabilities, it looks as if an offer will be made. Critically, NXGN brought onboard Morgan Stanley ( MS ) in late August to arrange options for a potential sale, so this has been on the cards for a few weeks now.

As a reminder, NXGN is positioned as a platform company to help healthcare providers in patient documentation and revenue cycle management, among other software applications. As of its first quarter in fiscal '24 , ~92% of its c.$179mm in quarterly revenues were booked as recurring in nature, and management raised its FY'24 top line forecasts to $722mm at the upper end of range. Moreover, $52mm of Q1 sales were from subscription services (up 23% YoY), and non-recurring sales were up 13% to $35mm.

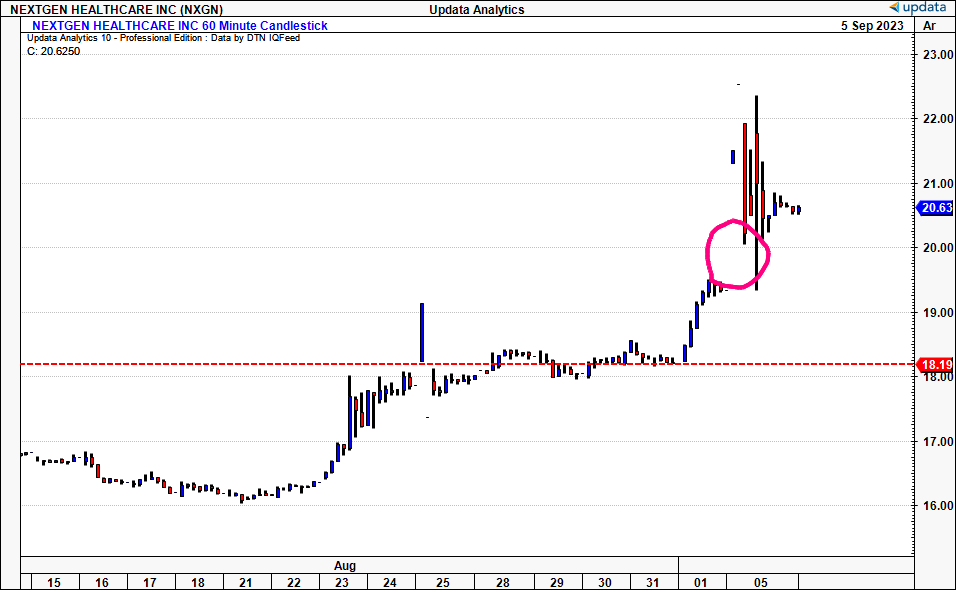

Following reports of the potential deal yesterday, NXGN's stock price has rallied 6.3% from the open as I write and trades a shade off 52-week highs. You can see the gap higher once the market digested the announcement in Figure 1, that shows the 60-minute chart from August rolling into September.

Figure 1. NXGN 60–minute chart, note gap higher on news of potential Thomas Bravo takeover

{kind=link}

Data: Updata

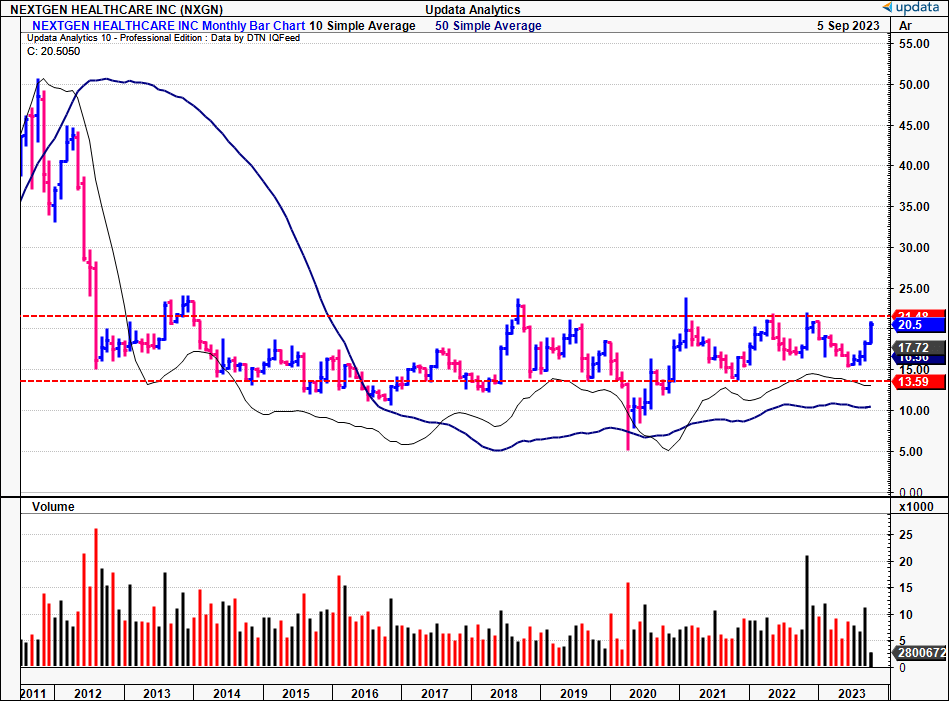

Put into perspective, the breakout is less significant. Figure 2 outlines NXGN's equity line over the past 11–12 years. Monthly returns are shown, with each bar representing 1 month's worth of trade.

NXGN has sold within a tight range for the last decade, after wiping ~$45/share in market value in mid-2012. The market has rated it poorly over this time, with NXGN missing a bid despite the tremendous run in equity benchmarks over the same period.

Figure 2.

{kind=link}

Data: Updata

Wall Street analysts have been bullish on NXGN as well. Cantor Fitzgerald recently updated its rating on the stock to a buy with a $21/share valuation, noting, “[w]e believe the company’s balanced approach to revenue and margin growth, high recurring revenue mix and well-capitalized balance sheet create an attractive investment profile”.

There have also been 4 revisions higher to revenues and earnings over the last 3 months from Wall Street analysts as well. Consensus now eyes $718mm in top-line revenues on earnings of $1.10/share.

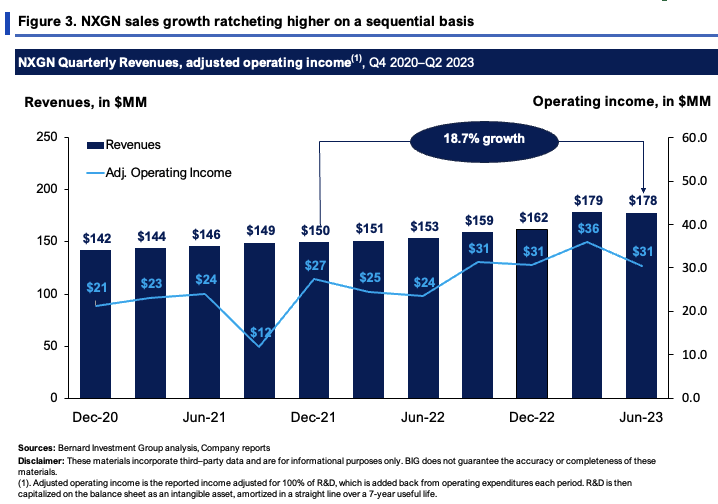

And it would appear there's good foundation for this. Figure 3 outlines the company's quarterly sales clip against adjusted operating income. Adjusted operating income is the reported income adjusted for 100% of R&D, which is added back from operating expenditures each period. R&D is then capitalized on the balance sheet as an intangible asset, amortized in a straight line over a 7-year useful life.

Critically, the company has grown its quarterly top-line by 18.7% since 2021, pulling in $178mm last quarter. On this, it booked $31mm in adj. operating income, up from $27mm in Q4 CY 2021.

{kind=link}

BIG Insights

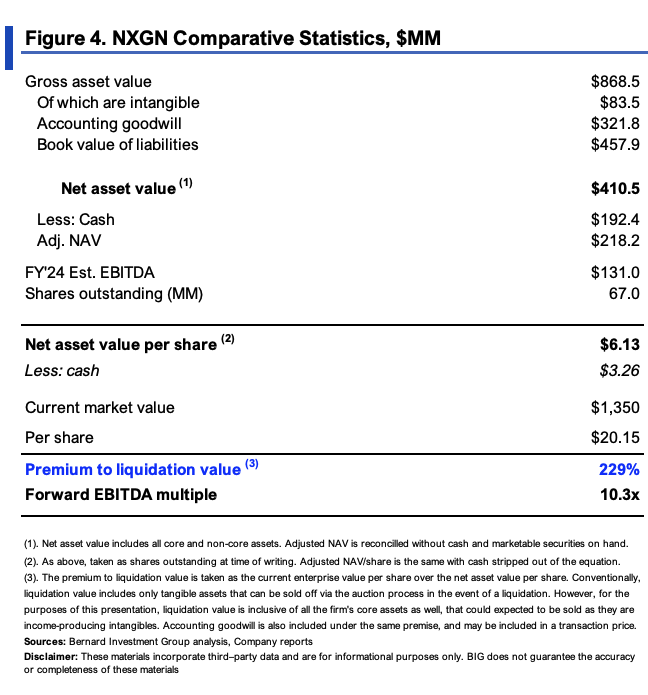

Figure 4 outlines some of the comparative statistics relevant to a potential transaction. Basic assumptions are taken in the presentation of figures. For one, liquidation value here—that typically only includes tangible assets—includes all intangibles that are considered core assets to NXGN's operations and growth. Adjustments are made for cash included and stripped out (as is often the case—you don't typically pay cash to buy cash). Consider this the 'adjusted' liquidation value for now. NXGN's net asset value comes to $6.13/share, $3.26/share less cash, on its last book values. FY'24 EBITDA estimates are NXGN's guided numbers of $131mm for the year.

At the company's $1.35Bn enterprise value, it trades at 10.3x EBITDA estimates, and a 230% premium to adjusted liquidation value (518% less cash). If a deal were made at the current market value, Thoma Bravo would theoretically be asked to pay 10.3x forward EBITDA to acquire the company based on these rudimentary assumptions.

{kind=link}

BIG Insights

Figure 5 is actually taken directly from a separate analysis performed on Abcam plc ( ABCM ) and is updated to include a potential NXGN/Thomas Bravo sale. It shows comparable transactions within healthcare/biotech this year. There have been no conclusions with the ABCM deal, hence why it is in red. Nor has anything been mentioned in the transaction value for NXGN/Thomas Bravo either. But just for perspective, say it were to pay around enterprise value for NXGN—$1.3Bn, say—this would be on the lower end of comparable healthcare M&A this year.

Figure 5.

Note: This chart is Retrieved from article: " Abcam: Further Upside Limited With Potential Acquisition In The Making, Reiterate Hold", published 26th August, 2023. ( )

In short

The market looks to have placed a premium on NXGN's potential acquisition from Thoma Bravo. I'd stress again—there have been no confirmations from the private equity firm, but given the press it has garnered thus far, there is a high likelihood of something being released as early as this week in my opinion.

The questions are: 1) what will Thoma Bravo offer up, 2) how will it structure the deal (all cash vs scrip), and 3) will NXGN even accept the offer in the first place. We shouldn't rule out competing bids either if/once the details are eventually released. Any offer also has to be approved by NXGN's shareholders, so it would have to surpass the long-term ranges outlined earlier. Net-net, without any clarifications on the deal, I'm unchanged on my last posture (which was a buy), but those in the special situations crowd would be no doubt paying very close attention to the story here. It may pay to be trigger-ready on the name if the deal particulars are attractive.

For further details see:

NextGen: Potential Thoma Bravo Deal Inching Closer - A Look At The Moving Parts