NIE - NIE: I Want To Like This Convertible CEF But I'm Not Sure It's Worth The Risk

Summary

- Convertible securities offer the best of fixed-income securities and common equities to investors.

- AllianzGI Equity & Convertible Income Fund is heavily invested in technology and healthcare companies, which is not unsurprising but resulted in horrible performance when the bubble popped last year.

- The closed-end fund is more heavily invested in convertible securities than might be expected, which should allow it to muddle through the bear market.

- The fund is struggling to maintain its distribution and will almost certainly have to cut it.

- The fund is trading at a very attractive valuation right now but I am not sure that it is worth the risk.

One of the more interesting asset types in the market is convertible securities. These assets are not particularly well-followed by investors, likely because they are somewhat uncommon. This should not really be the case, though, since they have a great many benefits to offer to traditional fixed-income investors. Basically, they are fixed-income securities that still have much of the upside potential with stocks.

In previous articles, I mentioned that income-focused investors frequently have to sacrifice some upside in order to get their income so convertible securities offer one possible solution to this problem. As these securities are somewhat uncommon though, it can be difficult to construct a diversified portfolio of them. Fortunately, there is a solution to this problem and that is to invest in a closed-end fund that specializes in convertible securities.

There are a few of them in the market, but this article will focus specifically on the AllianzGI Equity & Convertible Income Fund ( NIE ), which yields an attractive 10.86% as of the time of writing. This fund offers more than simply an impressive yield, however, as it is trading for an incredibly attractive price. As these two factors are both very appealing to closed-end fund ("CEF") investors, let us investigate further and see if this fund could be a worthy addition to a portfolio today.

About The Fund

According to the fund’s webpage , the AllianzGI Equity & Convertible Income Fund has the stated objective of providing its investors with a high level of total return, focusing specifically on current income, capital appreciation, and capital gains. This is hardly unusual for an equity fund because equities are a total return instrument. After all, we purchase equities primarily because we want to obtain both dividend income and capital gains from the security. The fund does invest in common equities but it also goes further and purchases convertible securities. This is something that sets it apart from many other closed-end funds as there are scant few of them that actually purchase these assets.

As some readers may be aware, a convertible security is a preferred stock or bond that can be converted into equity under certain conditions. In exchange for this conversion feature, the security will have a lower yield than an ordinary bond issued by the same company. However, the fact that it can be converted into common equity works out pretty well for investors if the common stock of the issuing company skyrockets in value as then the fixed-income investor can receive substantial capital gains from the conversion. In the absence of such common stock appreciation, it provides the safety of a normal fixed-income security.

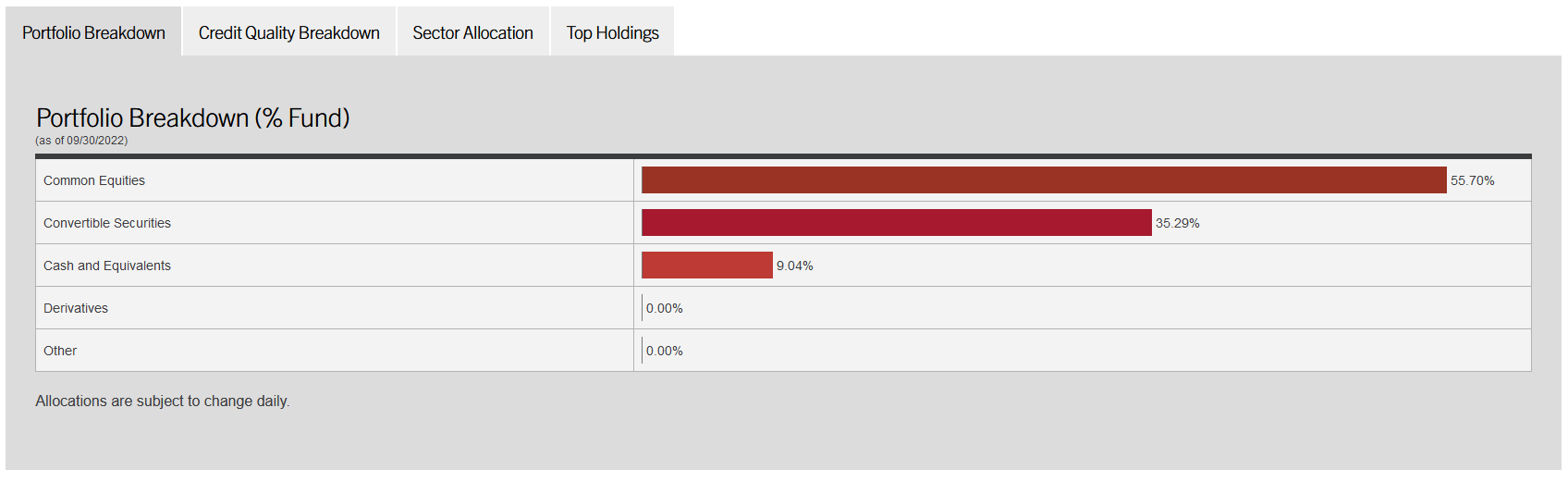

Convertible securities are commonly issued by start-up firms or other high-risk but potentially high-reward companies like Tesla ( TSLA ) in their early days as a way to entice some risk-averse investors into financing the company. Despite the general appeal of convertible securities to most investors, the fund is invested primarily in common stock:

{kind=link}

I will admit, though, that the 35.29% common equity allocation is more than I expected to find in the fund. Convertible securities are somewhat uncommon so even those funds that specialize in the asset class frequently have a difficult time filling up more than 20% of their portfolio with them. It is nice to see that this fund does manage to have a fairly high exposure to convertibles though considering that they can provide us with the best of both worlds, so to speak.

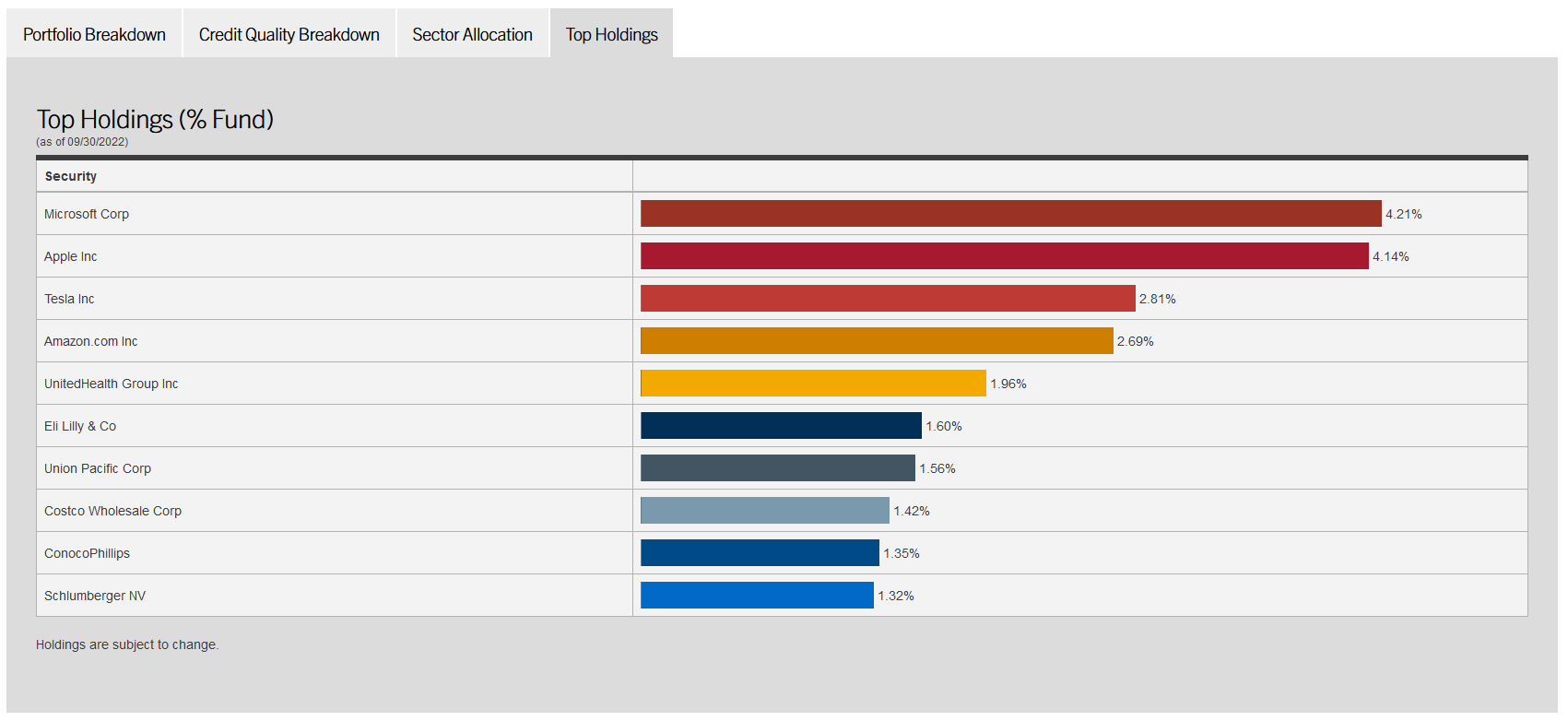

The largest positions in the fund will undoubtedly be familiar to most investors. Here they are:

{kind=link}

I very highly doubt that any reader has not heard of every company on this list. We see here three of the mega-cap technology companies in the form of Apple ( AAPL ), Amazon ( AMZN ), and Microsoft ( MSFT ). Apple and Microsoft are also arguably the most “blue chip” of the technology companies as well due to their high degree of recurring revenue and the fact that they are much more aggressive about returning money to shareholders than their other mega-cap peers, such as Amazon. We also see Tesla, which was a stock market darling during the free money era that ended last Spring.

United Healthcare ( UNH ) and Eli Lilly ( LLY ) are among the largest healthcare firms in the world. Healthcare has a lot going for it right now as its inelastic and recession-resistant nature should position the sector well to weather the likely economic challenges that we will face in 2023. We also have here two major energy company companies in the form of ConocoPhillips ( COP ) and Schlumberger ( SLB ), which is also appealing due to the fact that energy was by far the best-performing sector in 2022 and it looks positioned to have a similarly strong year in 2023. Finally, we have a retail giant and a transportation company. Costco ( COST ) may be a decent play in the retail sector given that many households will want to tightly budget their expenses following nineteen straight months of negative real wage growth. Overall, this looks like a fairly reasonable portfolio as we enter 2023.

Another nice thing to see here is that the fund’s portfolio is reasonably diversified. As my long-time readers on the topic of closed-end funds are no doubt well aware, I do not generally like to see any single position in a fund account for more than 5% of the fund’s assets. That is because this is approximately the point at which an asset begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification but if the asset accounts for too much of the portfolio, then this risk will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market does not, and if that asset accounts for too much of the portfolio, then it may end up dragging the entire fund down with it. As we can see above, though, there is no asset that accounts for more than 5% of the portfolio so we seemingly do not need to actually worry about this. Of course, Microsoft and Apple are fairly close so if you are also invested in other funds that have a high allocation to these stocks then you should ensure that you are willing to be exposed to the risks of holding these stocks individually. This fund in isolation appears just fine, though.

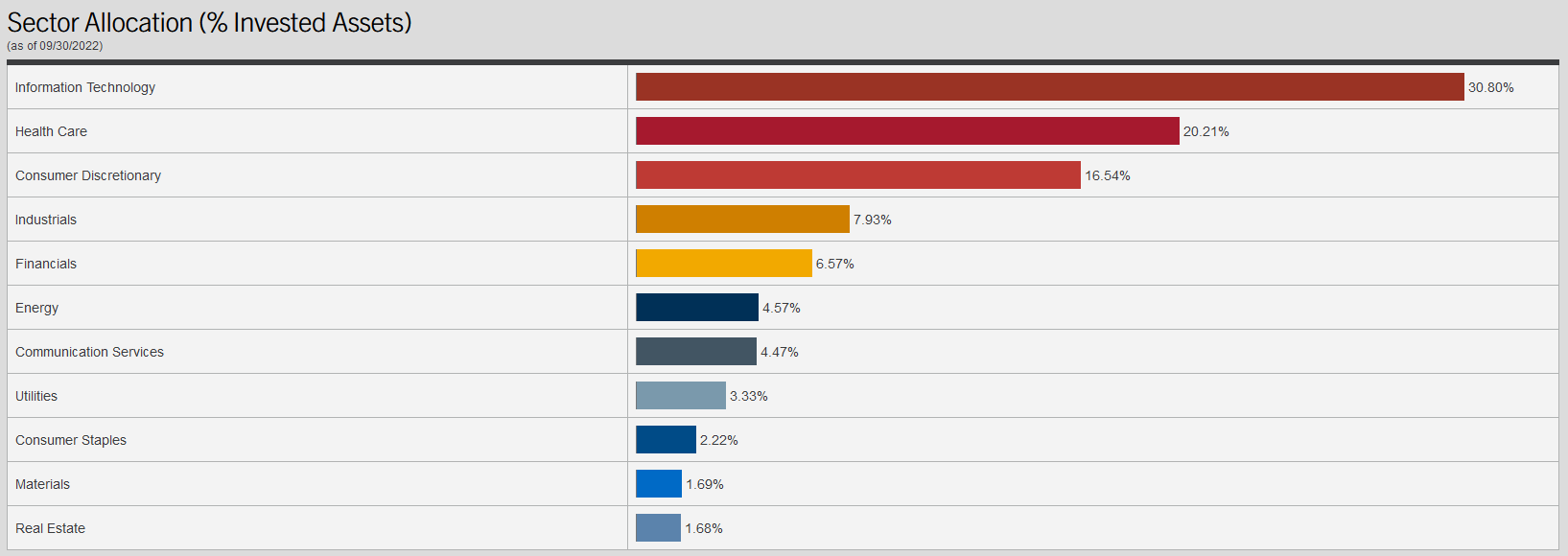

A look at the largest positions in the fund will undoubtedly lead one to believe that the AllianzGI Equity & Convertible Income Fund is heavily exposed to the technology sector. This is certainly the case as that sector accounts for fully 30.80% of the portfolio:

{kind=link}

This is substantially more than the 25.47% technology sector weighting in the S&P 500 Index ( SP500 ). However, this is not especially surprising. As I pointed out earlier in this article, convertible securities are frequently used by start-up companies to obtain financing at a more attractive price than could be accomplished with ordinary securities. As many start-up firms are in technology and healthcare, we would naturally expect to see these sectors have a larger-than-normal weighting in this fund. Unfortunately, these same companies tend to have lower dividend yields on their common stocks than financials, real estate, or energy. However, this fund is not focused on generating dividend income from common stocks. Rather, it is mostly receiving income from the convertible securities in the portfolio and then converting them to common stocks in order to generate capital gains.

As I have pointed out in the past, though, the technology sector and other high-flying stocks were punished fairly severely when the Federal Reserve began to tighten monetary policy. This applies to many of the stocks that account for the largest positions in the fund:

| Company |

| TTM Market Price Return |

| Microsoft |

| -29.04% |

| Apple |

| -27.97% |

| Tesla |

| -69.35% |

| Amazon |

| -48.79% |

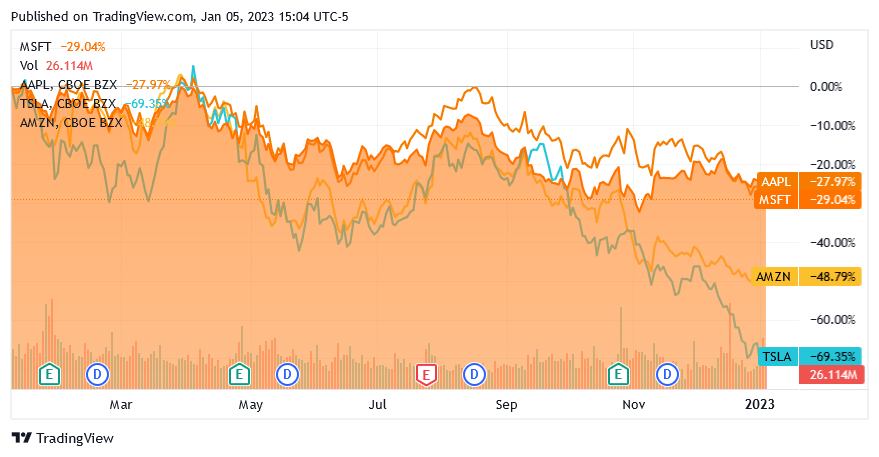

Here are the same figures in graphic form, just to show how bad it has been for these stocks:

{kind=link}

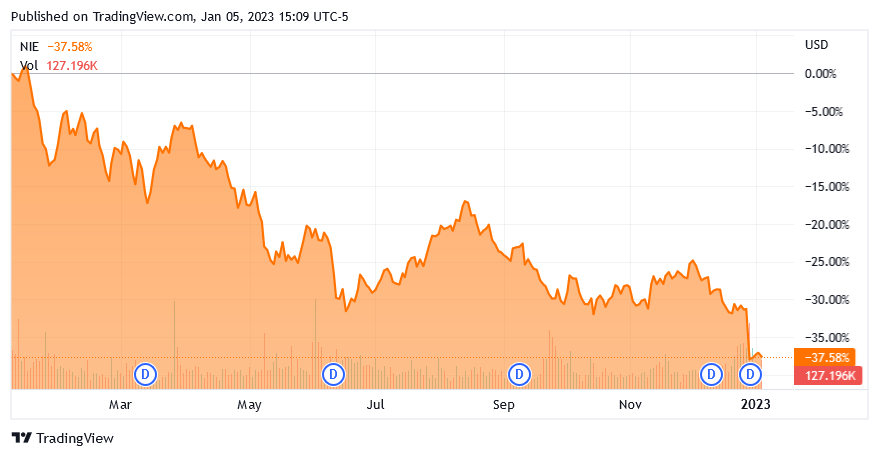

The fact that these four stocks account for 13.85% of the portfolio thus undoubtedly served as a major drag on the fund’s capital gains over the same period. This would be amplified by the fact that the stock prices of start-up technology or healthcare companies are nowhere near as high as they were during the bubble era, which means that converting the convertible securities held by the fund is not as profitable as it would have been a year ago. The market has certainly not been blind to this as the AllianzGI Equity & Convertible Income Fund is down 37.58% over the trailing twelve months:

{kind=link}

This is certainly disappointing and it could have been avoided if the fund’s management had pivoted away from the bubble-era mentality last year. An obvious strategy even back then would have been to sell the technology stocks in favor of energy and possibly healthcare as high energy prices were severely straining consumers even back in 2021 (well before the Federal Reserve began raising interest rates). I suppose it is water under the bridge now, though, and at least this fund did not have as much exposure to the high-flying bubble stocks as some other closed-end funds did. The presence of the convertible securities helps a bit here too since they will at least continue to generate income in the absence of conversion.

Distribution Analysis

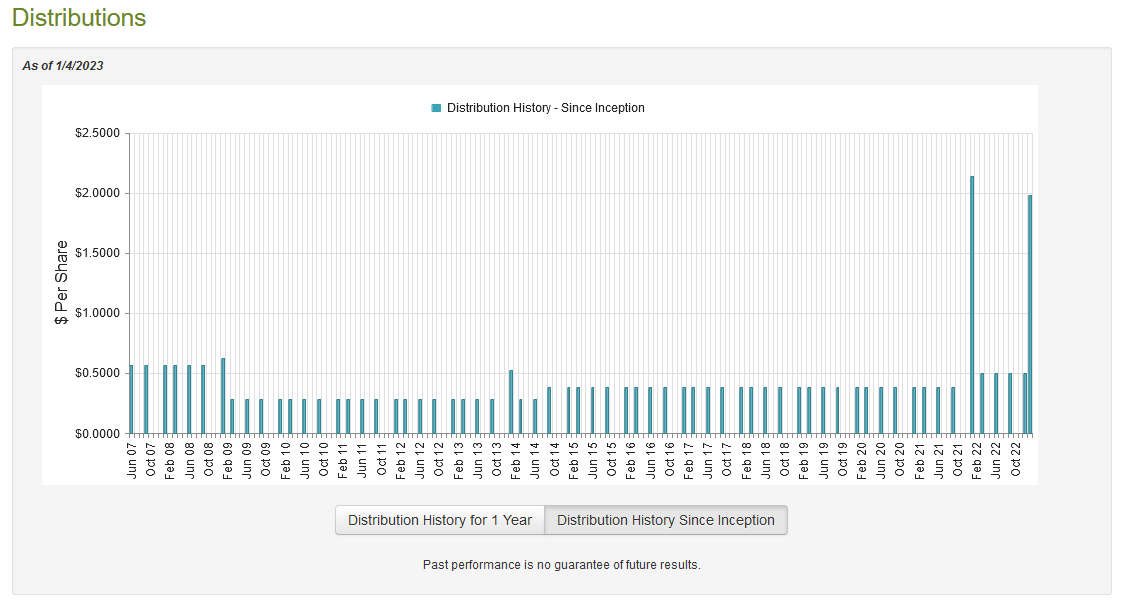

As stated earlier in the article, AllianzGI Equity & Convertible Income Fund aims to provide investors with a high level of total return, primarily through current income and capital gains. The fund will naturally be paying out its capital gains to investors through the distribution, though. In addition, more than a third of the portfolio is invested in convertible securities, which act largely as fixed-income investments that provide the fund with a high level of income. As such, we can assume that the fund itself boasts a high yield. This is certainly the case as the AllianzGI Equity & Convertible Income Fund pays out a quarterly distribution of $0.50 per share ($2.00 per share annually), which gives the fund a 10.86% yield at the current price. It is important to note though that the fund paid out special distributions in both January 2021 and January 2022 but as these are not recurring distributions, we are not including them in the calculation of the yield. The fund’s distribution history will likely be a source of comfort though as it has generally increased its payout over time:

{kind=link}

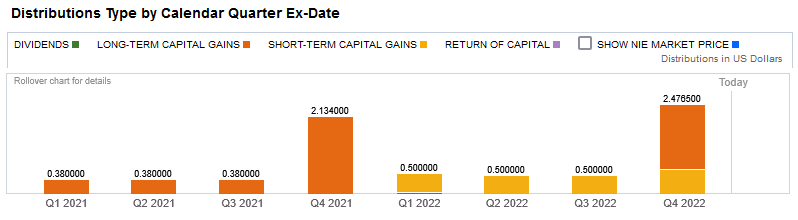

This should be at least somewhat comforting to more risk-averse investors that are seeking a secure and consistent source of income with which to pay their bills. I will admit though that I have a difficult time believing that too many risk-averse investors would be interested in a fund like this, despite the general appeal of convertible securities for any income-seeking investor. Another thing that will likely be comforting to most investors is that the distributions are entirely classified as capital gains and contain no return of capital component:

{kind=link}

The reason why the lack of a return of capital component could be appealing is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously unsustainable over any sort of extended period. A capital gains distribution implies that the fund is simply paying out its capital gains to investors while retaining its principal. The only real problem with this is that there is no guarantee that the fund will always generate sufficient capital gains in order to maintain its distribution. It is still generally preferable to paying out money that the fund never actually earned, though. For this reason, it is important that we analyze the fund’s finances in order to determine exactly how sustainable these distributions are likely to be as we do not really want to be the victims of a distribution cut.

Fortunately, we do have a somewhat recent document to consult for that purpose. The fund’s most recent financial report corresponds to the six-month period that ended on July 31, 2022. While this report will not include information from the past few months, this is still a more recent report than other funds have provided and it will give us quite a bit of insight into how well the fund handled the shift to a monetary tightening policy early in 2022. During the six-month period, the AllianzGI Equity & Convertible Income Fund received $3.874 million in interest and $29,000 in dividends from the assets in its portfolio. When we combine this with a relatively small amount of income from other sources, the fund brought in a total of $3.918 million during the period. It paid its expenses out of this amount, which left it with $2.402 million available for investors. This was obviously not enough to cover the $23.045 million that the fund actually paid out in distributions during the period, however. At first glance, this appears rather concerning as the fund clearly failed to cover its distributions.

However, there are other ways that the fund can cover its distributions, such as through capital gains. As might be expected from the market weakness in the technology sector during the first half of 2022, the fund failed miserably at this. The fund reported net realized losses of $20.587 million and net unrealized losses of $73.270 million during the period. Overall, the fund’s assets declined by $111.510 million during the six-month period. The fund did not make up for this in prior years either as its assets declined by $82.694 million during the eleven-month period that ended January 31, 2022, which is especially disappointing as that was an incredibly strong period for the market. On February 28, 2020, the AllianzGI Equity & Convertible Income Fund had total assets of $481.633 million but this was down to $389.740 million on July 31, 2022. Overall, it certainly appears that the fund is failing to cover its distribution so we should proceed cautiously as it will almost certainly have to cut in the near future.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a sure-fire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the AllianzGI Equity & Convertible Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the assets for less than they are actually worth. This is certainly the case with this fund today. As of January 4, 2023, the AllianzGI Equity & Convertible Income Fund had a net asset value of $21.16 per share but the shares only trade for $18.23 per share. This gives the fund’s shares a discount of 13.85% at the current price. This is a much more attractive price than the 12.06% discount that the shares have averaged over the past month so the price certainly appears reasonable here. However, it is important to keep in mind that the fund could cut its distribution so the price may not be quite as attractive as it first appears.

Conclusion

In conclusion, I certainly want to like the AllianzGI Equity & Convertible Income Fund. Convertible securities can be among the most attractive things to own because they offer the high yields of fixed-income securities and the capital gains potential of common equity. This is one of the few funds available on the market that heavily invests in these securities. Unfortunately, the significant exposure to a few bubble stocks that have fallen substantially over the past year has proven to be a drag on AllianzGI Equity & Convertible Income Fund’s performance, and it appears to be struggling to maintain its distribution. The price is certainly attractive here for AllianzGI Equity & Convertible Income Fund, but I am not certain that it is worth the risk.

For further details see:

NIE: I Want To Like This Convertible CEF But I'm Not Sure It's Worth The Risk