TYNPF - Nippon Sanso Is Very Undervalued Compared To Western Peers

2023-03-10 07:00:00 ET

Summary

- If you've heard of Air Liquide or Air Products & Chemicals, you should know about Nippon Sanso Holdings Corporation because it's valued substantially lower.

- While industrial figures remain strong considering the economic environment, there are some volume pressures, but most end-markets are resilient.

- Moreover, the industry allows for pricing ahead of inflation, so incomes have grown across Nippon Sanso's geographies.

- They also own the Thermos brand, which is huge in sports bottles, camping, and other thermal retention equipment, the same way Hoover is dominant in vacuums.

- Nippon Sanso is a pretty clear buy to those who already have positions in this space. However, we still have better ideas than this that we'd allocate to fully first.

Published on the Value Lab 03/8/23.

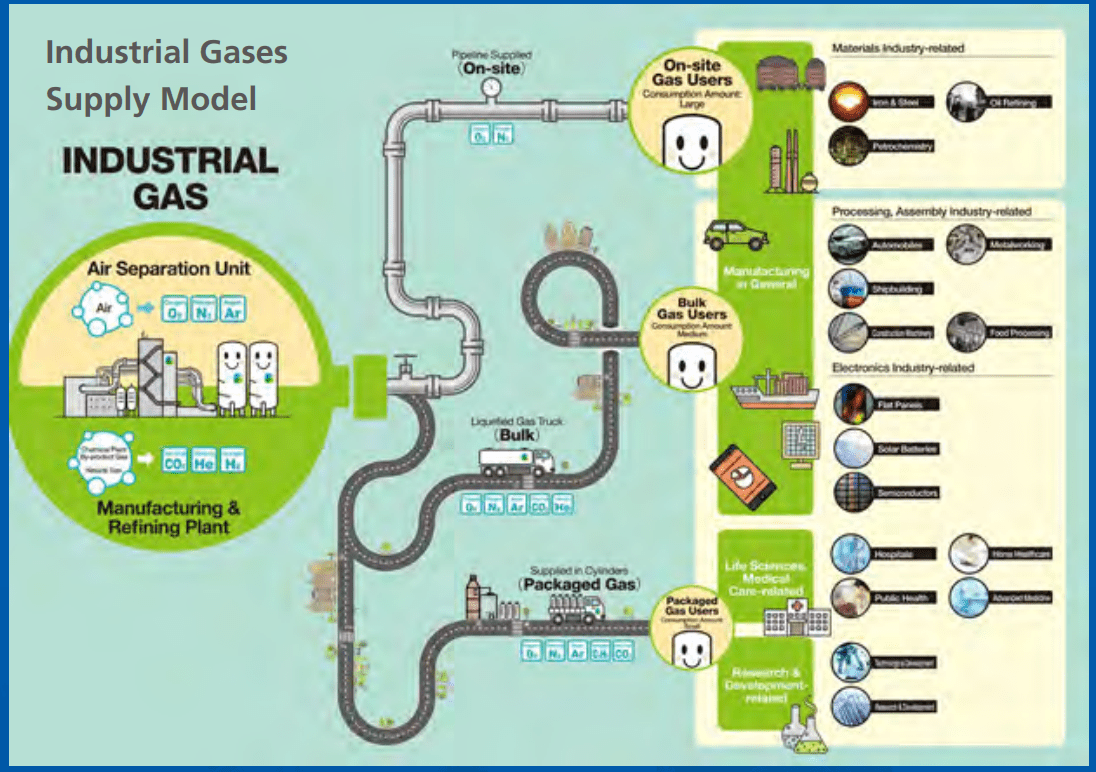

Nippon Sanso Holdings Corporation ( TYNPF ) is an industrial gases producer that operates in several geographies, and they call each of those geographies their segments. Much of their capacity is for air separation gases, and ultimately their end-markets are across industries including chemicals, refinery, steel and medical applications, but also electronics. They sell a lot of the same products as L'Air Liquide S.A. ( AIQUF ) and Air Products and Chemicals, Inc. ( APD ) at a much smaller valuation. They are clearly the best pick among them for less than 9x EV/EBITDA.

Nippon Sanso Q3

They produce gases like nitrogen, oxygen , argon etc. for uses in many industrial processes including refinery, petrochemicals, steelmaking, but also lots of other pretty heavy industry like automotive and electronics, but also the medical industries.

The electronics exposures are pretty big in Japan, as well as automotive, and they operate in Oceania, the U.S., Japan, and Europe as their four geographic segments by which they report.

The company also sells equipment, and they own the Thermos brand for sports bottles and camping equipment. This is their only B2C segment and accounts for about 5% of operating income.

{kind=link}

The big cost inputs are electricity, and this has been the main source of input inflation for them, but they are staying ahead of the price increases with their own pricing initiatives, and broadly speaking volumes remain healthy and incomes are clearly rising.

Comprehensively, operating income grew 10% , and the only segment that saw declines was Japan by 10%, and this is only because of some technical lags between input inflation and output pricing, so this decline will be reversed soon as end-prices catch up.

Air separation gases are the main product, so the gases are ones that come from separating the individual gases that you find in the air. Volumes were down in Japan, flat in the U.S., fell in Europe, and were flat in Asia & Oceania. The sales of equipment actually increased in all geographies, which is a good leading indicator for industrial investment cycles which remain bullish on the value of industrial products. Electronics was generally a strong market across segments including Japan, due to the release of some of the pressures on the supply chain. Moreover, automotive was strong, too, with good car sales volumes out of Japanese and global manufacturers as pent-up demand liquidates.

LP gas is a bigger market in Asia & Oceania, and these markets remained strong in terms of volumes with some growth, and of course in terms of pricing and marginality. Europe saw problems due to the proximity to the energy crisis, which has muted the industrial picture there, since energy intensity characterizes industrial businesses, but the benefits in pricing in that dislocated market were clear and contributed to 30% operating income growth, the highest of all the segments.

Generally, the depreciation of the yen was good for the company, as some of the input costs were brought relatively down in the fixed cost base.

Thermos saw good revenue growth thanks to reduced global restrictions on mobility and activity, but inflation and higher local costs due to a depreciating yen has hit margins meaningfully and operating income decreased 10%.

Bottom Line

While some of the Nippon Sanso Holdings Corporation end-markets are more exposed, as seen in Japan where lacking consumer sentiment is hitting industrial volumes, there are plenty of more resilient markets, medical exposures among others, which are pretty important, considering these are some of the key markets for companies like Air Liquide.

Despite similar resilience to its industrial gases peers, Nippon Sanso trades at a substantially lower valuation. APD and Air Liquide are >15x and >11x EV/EBITDA respectively, while Nippon Sanso is lower than 9x. There's no good reason to pick anything other than Nippon Sanso in this space, considering a minimal 20% discount in multiple.

The only reason we can think of for the lower valuation is the controlling interest from Mitsubishi Chemical (MTLHF) ( MTLHY ), which limits opportunities for activism and acquisition. Still, this isn't a great reason since Air Liquide and APD aren't acquisition or activist targets anyway, since they're pretty big now. Nippon Sanso Holdings Corporation is the better buy.

For further details see:

Nippon Sanso Is Very Undervalued Compared To Western Peers