NNGRY - NN Group: Capital Generation Will Alleviate Requirement Concerns

Summary

- Lower Solvency II requirements will be compensated by cash flow generation.

- Wall Street expectations on higher buyback is not the solution. In the long run, we prefer tactical M&A and a progressive dividend policy.

- NN Group offers an interesting entry point both at valuation and also in terms of yield (considering both dividend and buyback).

After our comps analysis between Aegon (NYSE: AEG ) and NN Group NV ( OTCPK:NNGPF ), today we are back analyzing the Dutch insurance sector. When we released our analysis in April 2020, our preference was for Aegon, which delivered a stock price appreciation of more than 200% compared to NN Group which was up by only 43%. At that time, Aegon was also offering a better dividend yield with a lower payout ratio whereas, as mentioned, NN was looking safer

from a solvency ratio perspective, but from a shareholder remuneration policy perspective and considering long-term earnings power, Aegon is not only cheaper but more vigorous of a pick in this sector, and for that reason, it's our Dutch insurance pick.

It was definitely a good call; however, here at the Lab, we believe that now NN offers an interesting entry point. We also follow up on Aegon's latest quarterly results - Q1 performance and half-year account . Here below we explain our main key takeaways:

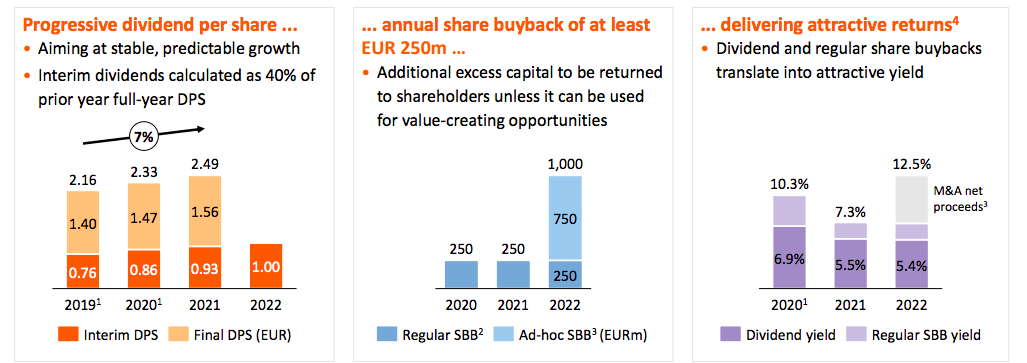

- First of all, NN hosted a capital market day in mid-November. This was not favored by the Wall Street investor community, and the company's long-term objectives were lower than analyst expectations. More importantly, the €250 million share repurchase agreement was lower than anticipated. Looking at the consensus, on average, they were pricing €500/€550 million. Our readers know that we prefer a dividend per share increase versus a buyback; however, NN Group explicitly said that the annual buyback was " at least €250 million " and additional excess cash might be returned to shareholders (Fig 1). Indeed, we believe is a fair amount considering the fact that the buyback is financed by net proceeds (€1.7 billion);

- Secondly, the company is progressing on its DPS commitment. Despite a Pro-forma dividend for the EIPOA decision in 2020, this year, the interim dividend per share was up by 7% (Fig 1). To sum up, buyback and dividend yield, the company is trading at 12.1% and we do believe that these returns are attractive within the financial sector;

- Still related to point 1) and 2), we should also price in NN Group M&A optionality. Indeed , the company will engage in acquisition only if there is a clear strategic rationale and more importantly if financial hurdle rates will be met. Just last week , the company announced the merger completion of the former MetLife businesses in Greece and Poland for a total consideration of approximately €584 million investment;

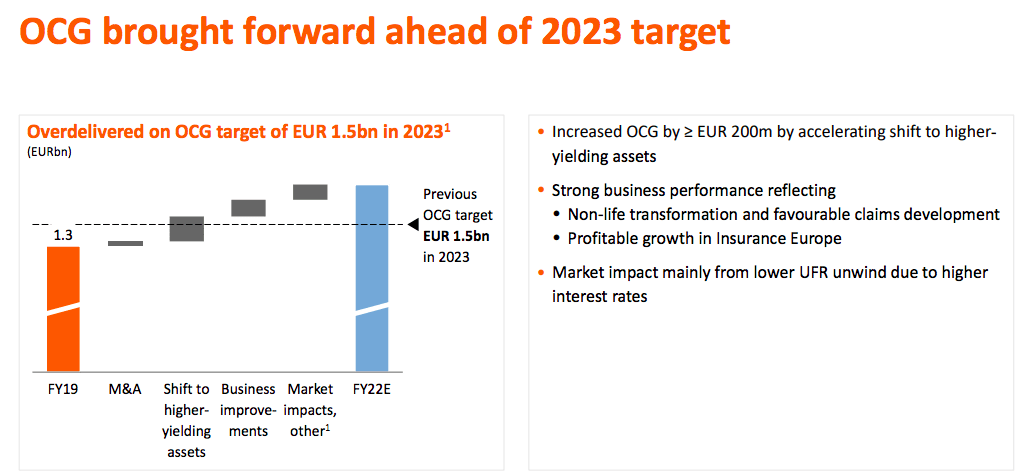

- Even if Wall Street analysts were not enjoying NN Group’s Operating Capital Generation target, we are in line with management indication forecasting in our internal number an increase to €1.8 billion in OCG by 2025 with a mid-single-digit growth. Concerning the FY 2022 results, the company exceeds its initial target and we are forecasting an OCG of €920 million for the 2022 second half-year results with managements that were suggesting €150 million higher results thanks to higher investment rates and better spreads (Fig 2);

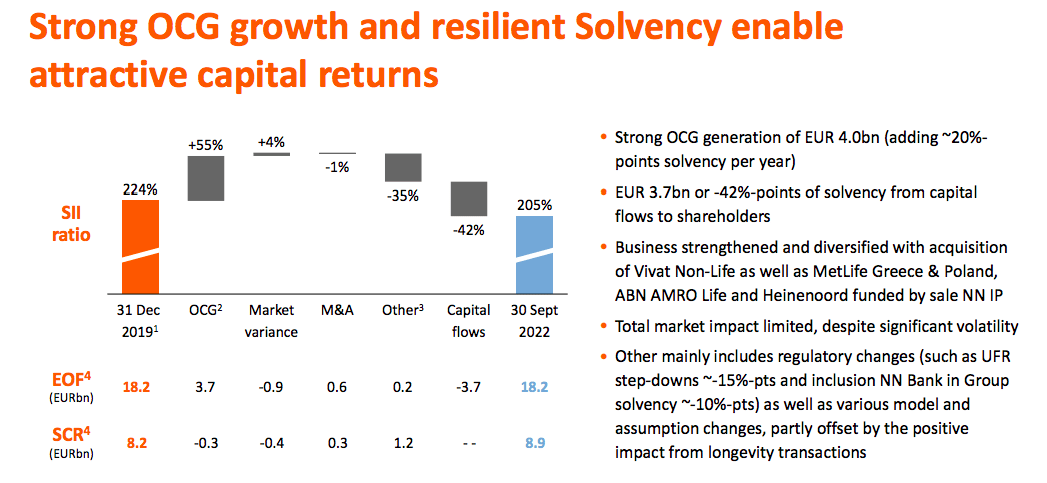

- NN Group is offering solid capital requirements in terms of the Solvency II ratio. Looking at the capital market day released, in September end, NN was standing at 205% (capital regulatory requirements set a minimum target of 180%) (Fig 3);

- Going to the valuation, the company is currently trading at 11.8% in Hold CO cash flow with a capital return potential higher than 12%. As already mentioned, this is pretty attractive. With a WACC of 6%, we derive a valuation of €16.5 billion compared to the current market cap of €11.3 billion. With 294 million shares, we have decide to increase our target price to €58.5 per share with a clear buy rating.

{kind=link}

Fig 1

{kind=link}

Fig 2

{kind=link}

Source: NN Group Capital Market Day 2022 - Fig 3

Aside from the usual insurance risk claims, our downside section includes: SII ratio deterioration from negative equity/debt capital market correction, long-lasting litigation in the insurance business which may cost €1 billion, real estate valuation decrease, and mortgage spreads widening.

For further details see:

NN Group: Capital Generation Will Alleviate Requirement Concerns