NNGPF - NN Group: Still An Exceptional Dividend Growth Investment Opportunity

2023-09-03 05:31:49 ET

Summary

- NN Group is a Dutch insurance company that offers an attractive total shareholder return of around 10% annually.

- The fundamentals of the company have significantly improved due to a higher than expected operating capital generation and a better solvency ratio.

- Due to the improved financials, it shouldn’t be a problem for NN Group to stay committed to their dividend growth policy.

- Based on the dividend discount model, the fair value of NN Group is €44.77 per share, which is significantly undervalued.

Investment thesis

On the 27th of June I wrote an article about NN Group (NNGPF) as an attractive dividend growth investment. Since then the stock price of €33.32 per share went up a decent amount.

This week NN Group has released its 1H23 results. The results were very well received with an 10% increase in share price on the 29 th of August. Since then the share price dropped again to €35.84, this also had to do with the fact that the company went ex-dividend on the 31st of August.

{kind=link}

Share price NN Group (Google Finance)

Despite the increase in share price I think NN Group still has much more left in the tank to make it a worthy long-term investment. In this article we’re going to take a deeper dive in the 1H23 results and I want to show you why NN Group is still a valuable addition to a well-balanced dividend growth portfolio.

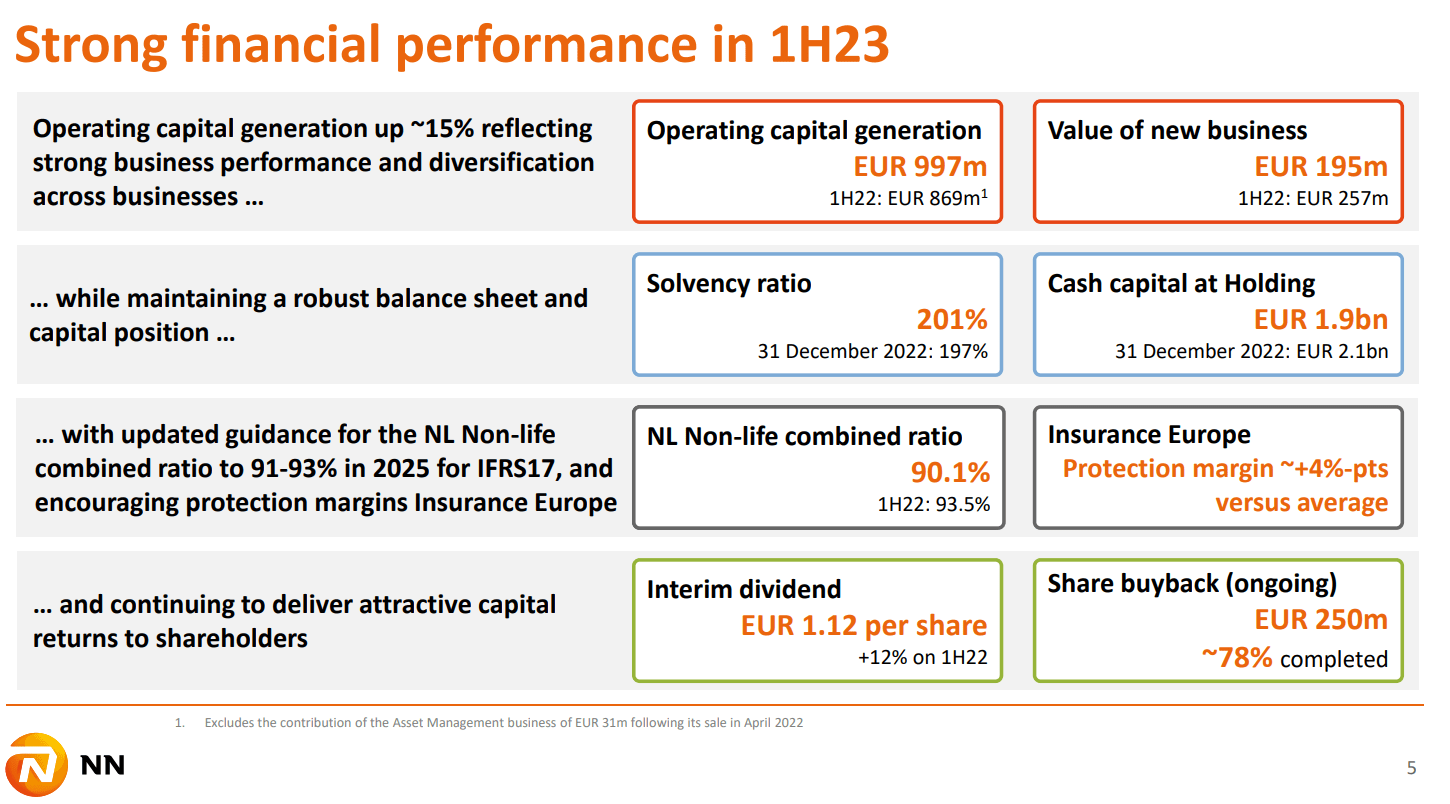

1H23 results

The slide below shows a clear picture of the strong performance.

{kind=link}

NN Group financial performance (NN Group analyst presentation 1H23)

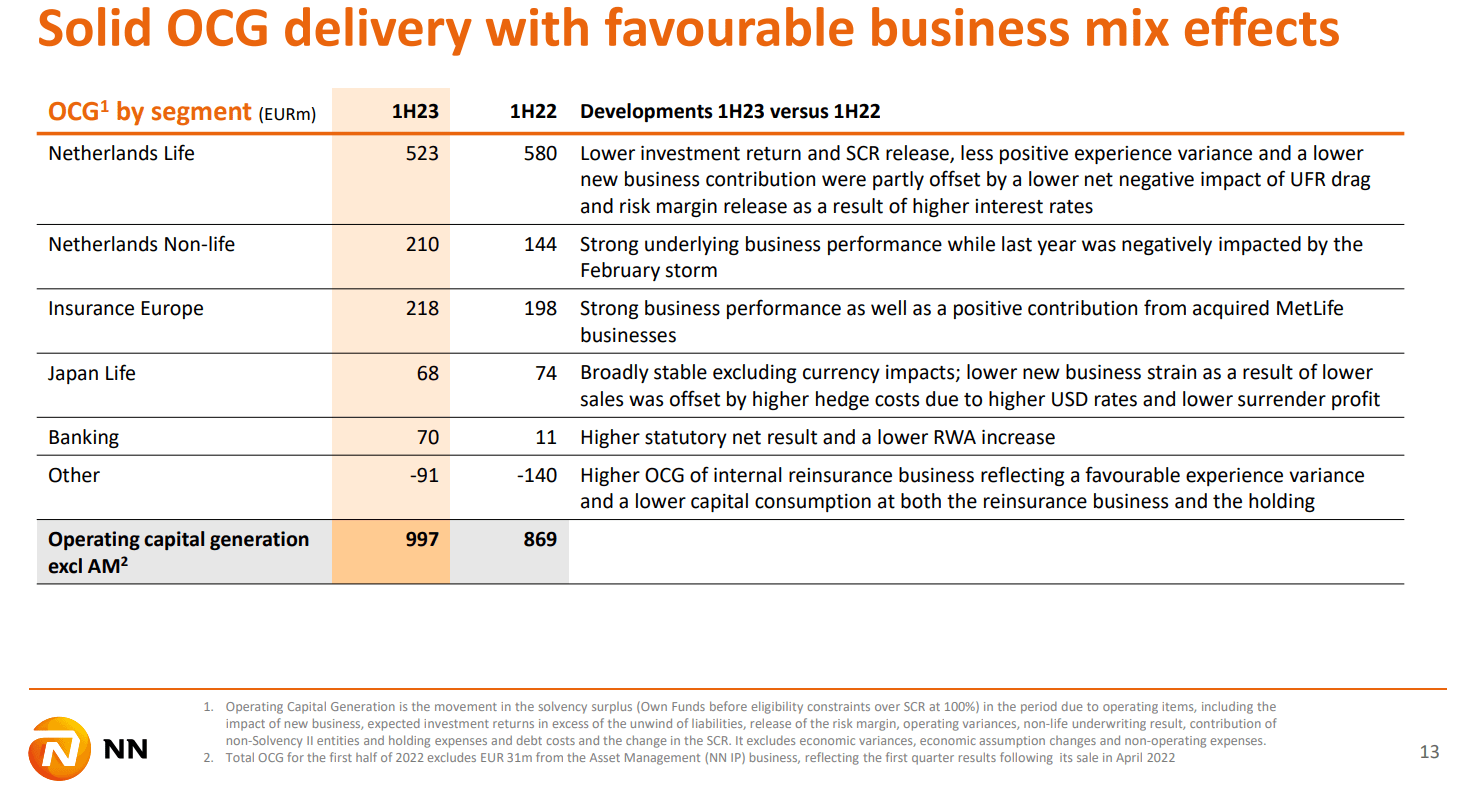

Operating capital generation

Operating capital generation ((OCG)) is one of the most important metrics for measuring the performance of NN Group.

{kind=link}

NN Group OCG targets (NN Group analyst presentation 1H23)

NN Group has the goal of making €1.8 billion in OCG in FY 2025 and based on the results of the report there is a possibility that the company can already achieve it this year. However, NN Group doesn’t want to raise their OCG outlook yet due to some potential one-offs, which I will explain later.

Their OCG was nearly 15% higher (€997 million) compared to the results of 1H22 (€869 million).

What I like about NN Group is their diversified business mix, which is the one of the reasons why the numbers were better than expected. Their best performing segments were the Netherlands Non-life, Insurance Europe and the Banking activities.

{kind=link}

Business mix (NN Group analyst presentation 1H23)

Firstly, There was a big difference in the Netherlands Non-life segment compared to last year (€210 million vs €144 million).

The Non-life insurance market in the Netherlands is quite consolidated, because all the big insurance companies, such as NN Group and ASR (ASRNL.AS), made some acquisitions in the past years. This has led to improved pricing and higher operating results. What is also good to mention is the growth was also driven by the weather environment. This was better compared to last year, because back then they had to deal with the February storm. This could be a one-off, however there is still improvement in profitability in the long term and the combined ratios are still getting better. What is good to see is that they’re well on track to achieve their own FY 2025 goal of €325 million in OCG.

{kind=link}

NN Group non-life market (NN Group analyst presentation 1H23)

Secondly, Insurance Europe is also making progress. This is in my opinion one of the more important growth divers for NN Group. Compared to the Dutch insurance market in central and southern Europe the markets aren’t fully penetrated. The company is really experiencing a shift towards protection products in these countries, so NN Group can take advantage of this. They also try to integrate MetLife and they are seeing the first results of it. The CEO David Knibbe said in the 1H23 earnings call it is likely that NN Group will achieve the gradual OCG increase to €50 million already this year, so they’re a year ahead of plan.

Insurance Europe OCG growth (NN Group analyst presentation 1H23)

The Netherlands life insurance business has resulted in lower contribution in OCG due to the negative impact of the financial markets. However there was still a strong net inflow of assets which is a good sign for future cash generation.

Net inflows (NN Group analyst presentation 1H23)

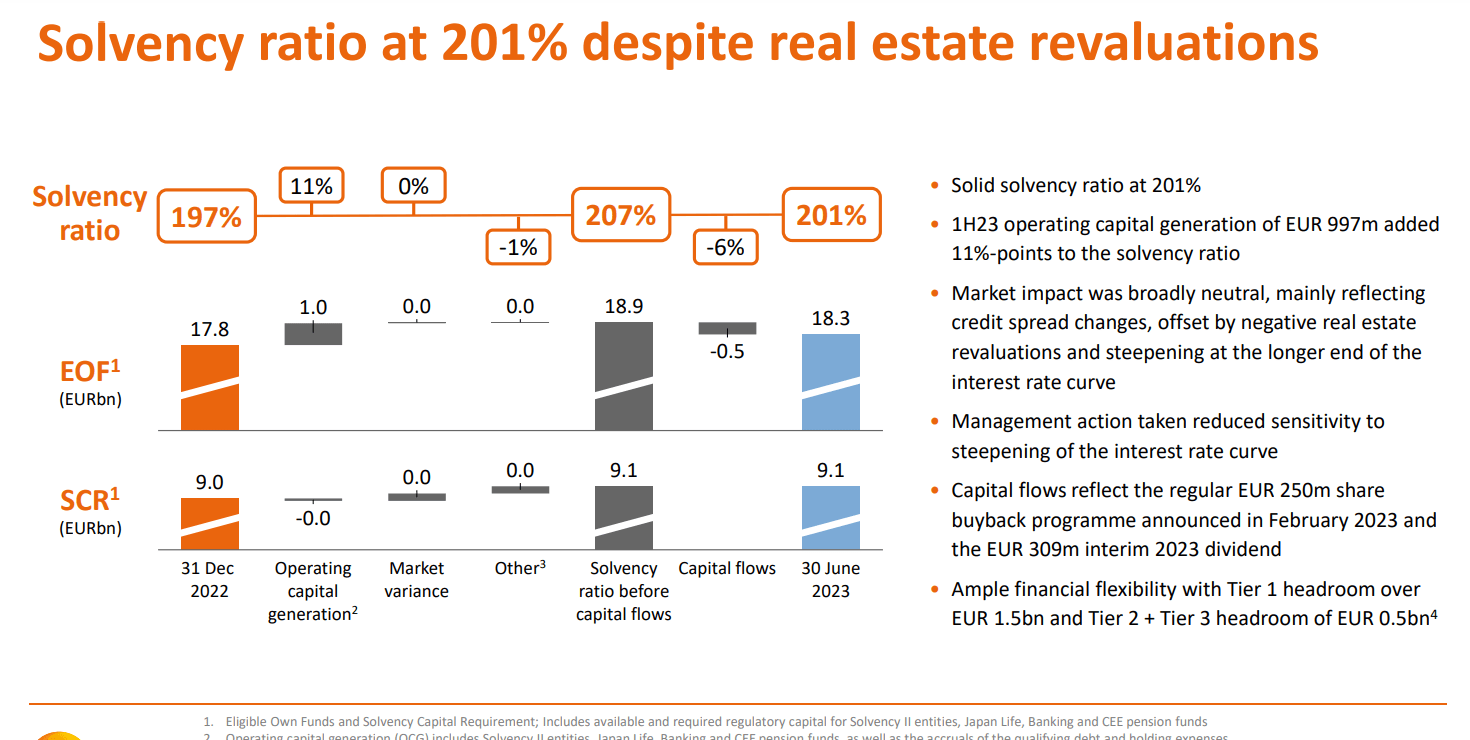

Solvency ratio

Another surprise was the increase in solvency ratio (201%) compared to the end of 2022 (197%). Analysts had expected a solvency ratio between the 190%-196% range. This was mainly due to the surprise in OCG and actions to reduce steepening risk. I think this is impressive that they were able to achieve this after 12 months of negative real estate revaluations.

{kind=link}

NN Group solvency ratio (NN Group analyst presentation 1H23)

With a solvency ratio of 201% the company has improved its financial health even more. While they already had an “A” credit rating from S&P Global, the improved solvency ratio puts NN Group in an even better position to stay financially flexible when investment in the business is needed.

In conclusion, the better than expected solvency ratio and OCG further strengthens the investment thesis, because it will be more easy for NN Group to stay committed to their capital return policy.

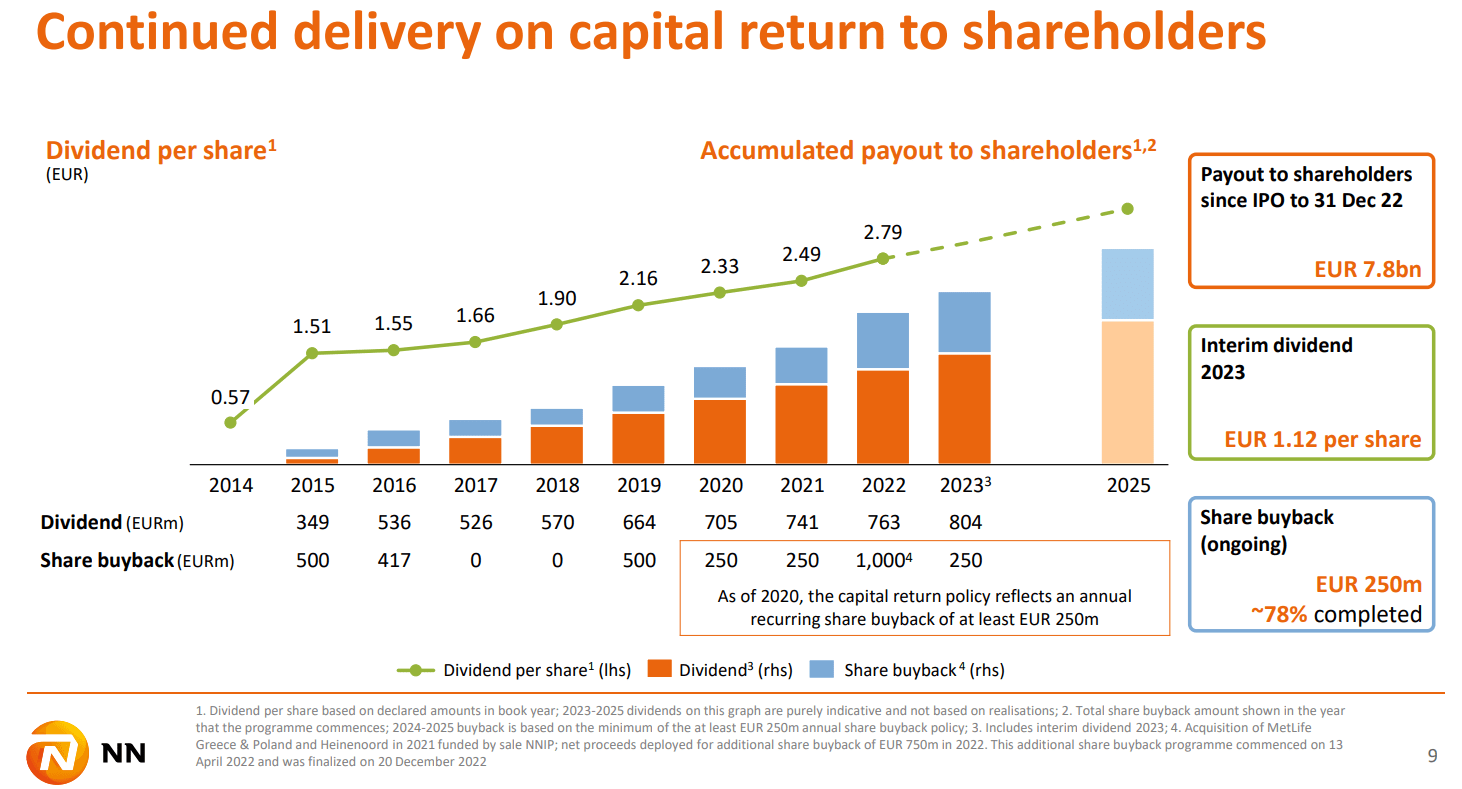

Capital return policy

As they have had mentioned it several times in the last conference call, NN Group is really committed when it comes to their capital return policy to their shareholders.

{kind=link}

NN Group Capital return (NN Group analyst presentation 1H23)

The most important goal is to pay a progressive dividend per share. NN Group has announced a 2023 interim dividend of €1.12, which is 12% higher than its previous interim dividend of €1.00 per share. Their last increase was huge compared to their own 5 year dividend growth CAGR of 7.98%.

When this article was written the stock price of NN Group was €35.84 and with a forward dividend of €2.91 (final dividend of 2022 + interim dividend of 2023) this comes down to a yield of 7.86%. The combination of dividend yield and dividend growth is in my opinion very attractive.

Based on the basic earnings per share in 1H23 (€2.01) the payout ratio was 55.8% which means the dividend should be more than safe. NN Group also should be able to grow its dividend at a nice pace for the coming years. As a dividend growth investor its sometime hard to find European companies with such a clear dividend growth policy and at this moment in time NN Group ticks all the boxes.

In addition to the dividend, an annual share buyback program can also be expected. NN Group said it would be at least €250 million until 2025. When there is excess cash the share buyback program will be bigger. With a market cap of €10.23 billion we can add up at least 2% to the total shareholder yield, which will be at least 10% annually!

Valuation

At the moment NN Group had a price-to-book ratio of 0.57, which is still far below its sector median of 1.04. This can be an indication that NN group is still attractively valued.

In my last article about NN Group I used the dividend discount model (Gordon’s Growth Model), because it fits the company's characteristics very well. I also think NN Group is capable of producing constant and predictable dividend growth.

As I said earlier the total dividend in 2023 (final dividend of 2022 + interim dividend of 2023) is €2.91 per share. I used a rate of return of 12.5%, because I want a return on investment of around 12.5% per year. Compared to the last valuation I used a higher dividend growth rate of 6% because of the better than expected 1H23 results and the extra opportunities for NN Group to further grow their OCG.

If we do the math again this comes to a fair value of €44.77 per share. Compared to the current share price NN Group is 24.9% undervalued.

Also more analysts are shifting towards a buy rating with a median stock price target of €50 per share.

Conclusion

Despite the increase in share price after the 1H23 results, NN Group still has a lot to offer as a great long-term investment. The best part of it is that the fundamentals have improved. The OCG and solvency ratio were better than expected and NN Group has managed to grow its business activities in central and southern Europe. And I haven’t even talked about the potential opportunity in the Dutch pension market. NN Group is on pole position in the defined contribution pension market and its plausible that the company can take benefit of the changing environment in the market transition period.

Due to the improved financial metrics, it shouldn’t be a problem for NN Group to stay committed to their capital return policy. Their dividend metrics are still excellent and combined with a proper share buyback program, shareholders can expect a shareholder yield of at least 10% annually. Based on price-to-book ratio and the dividend discount model valuation NN Group is significantly undervalued.

Finally, I still give NN Group a “BUY” rating. I really like the “put the money where your mouth is” approach and I am going to re-evaluate my own position of NN Group to potentially add more shares in my own dividend stock portfolio.

PS: Shares of NN Group are listed on Euronext Amsterdam (NN.AS) and their ADRs trade on the OTC markets ( OTCPK:NNGPF ). I would encourage you to buy the shares from Euronext Amsterdam for liquidity reasons.

For further details see:

NN Group: Still An Exceptional Dividend Growth Investment Opportunity