NNGRY - NN Group: The Drop In Sovereign Bond Yields Is Good News

2023-03-16 05:58:52 ET

Summary

- NN Group is a large Dutch insurance company with in excess of 200B EUR in assets. It also operates a (small) bank.

- The insurance company had in excess of 100B EUR in the securities available for sale portfolio in 2021, this dropped to 81B EUR in 2022.

- About 10% will mature this year and should carry little valuation risk.

- The flight to safety actually reduced government bond yields this week, and this could potentially result in a revaluation gain in Q1.

- That's not a guarantee: we don't know how the corporate bonds are performing and whether or not NN held onto its entire government bond portfolio in Q1.

Introduction

NN Group (NNGPF) (NNGRY) is a Dutch insurance company with in excess of 200B EUR in assets on the balance sheet. The company's main issue lately has been the revaluation of the portfolio of securities available for sale. As an insurance company generally matches the duration of its investments with anticipated liabilities there shouldn't be a liquidity crunch. But the main element I'm interested in is the erosion of the book value as the unrealized losses don't have to be reported in the income statement but do have an impact on the equity value of the balance sheet.

{kind=link}

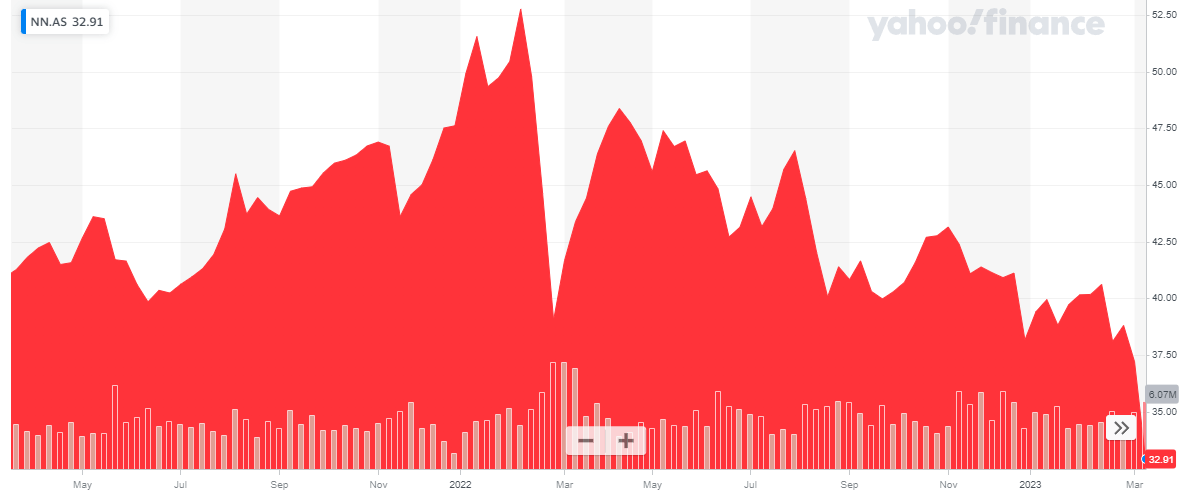

NN Group has a very liquid listing on Euronext Amsterdam where it's trading with NN as ticker symbol . The average daily volume is approximately one million shares. As there are approximately 280 million shares outstanding, the market capitalization is just over 9.2B EUR using a share price of 33 EUR per share. As NN Group trades and reports its financial results in Euro, I will use the EUR as base currency throughout this article.

All relevant information can be found here (the website contains download-only links).

The recent fallout on the financial markets is also hitting this insurance company

Investors liked to point at the book value and tangible book value of financial companies to figure out what the value of a stock is. But as the rapidly increasing interest rates have shown: an aggressive rate hike pattern erodes a lot of value as the market value of debt securities rapidly decreases as interest rates increase.

With banks, it's mainly an issue for the securities available for sale. Those tend to be held on the balance sheet in order to backstop any reasonable cash needs from customers. The key word here is 'reasonable'. While in normal times it is great to see a lot of cash, securities available for sale and securities held to maturity on the balance sheet (as it indicates the bank is running a liquid balance sheet) it does become a pain when the value of those securities has to be marked down based on the true market value of said securities.

It becomes an even bigger pain when a bank actually has to tap into those securities to boost its liquidity and cash profile, for instance in the case of a run on the bank. Then additional losses will likely be generated as those securities would have to be sold right away in order to satisfy these needs.

The banks have been in the spotlights the past few days, but investors tend to forget there's another sub-sector in the financial sector where the exposure to securities available for sale is even higher: insurance companies. But insurance companies usually have an important thing going for them: unless there is a sudden flurry or insurance claims, there is no real need to unwind the portfolio of securities available for sale, and that portfolio becomes de facto a portfolio with securities held to maturity, but classified with a for sale status.

The main issue insurance companies are facing is the erosion of book value. And although that shouldn't really come as a massive surprise, it did and does surprise investors.

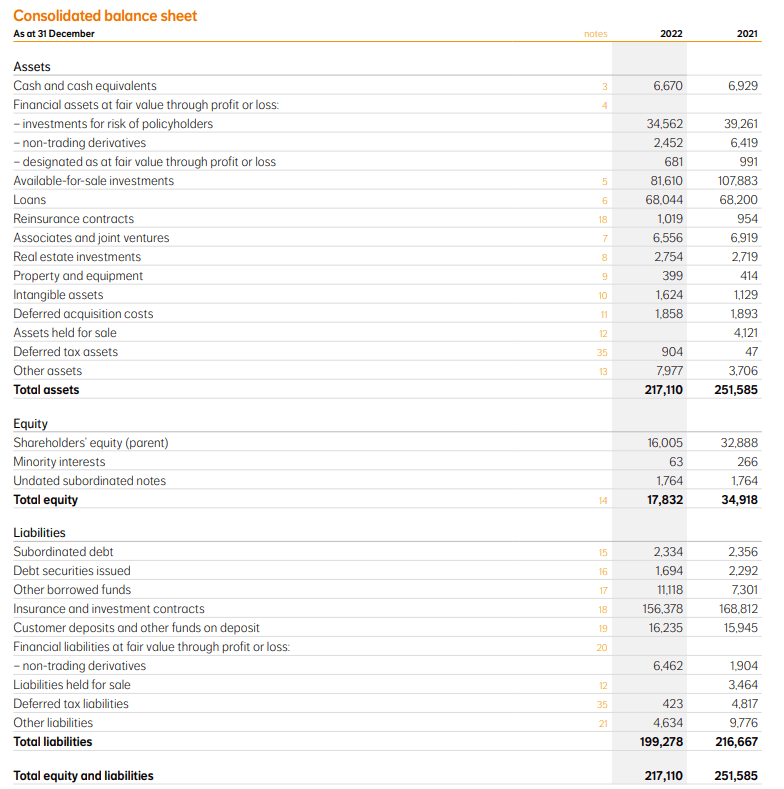

Although most investors outside of Western Europe likely won't have heard of NN Group, it is a very sizeable insurance company with a total balance sheet size of 217B EUR (down from almost 252B EUR). But as you can see below, the total amount of equity on the balance sheet was pretty much cut in half: there was a decrease from almost 35B EUR to just under 18B EUR.

{kind=link}

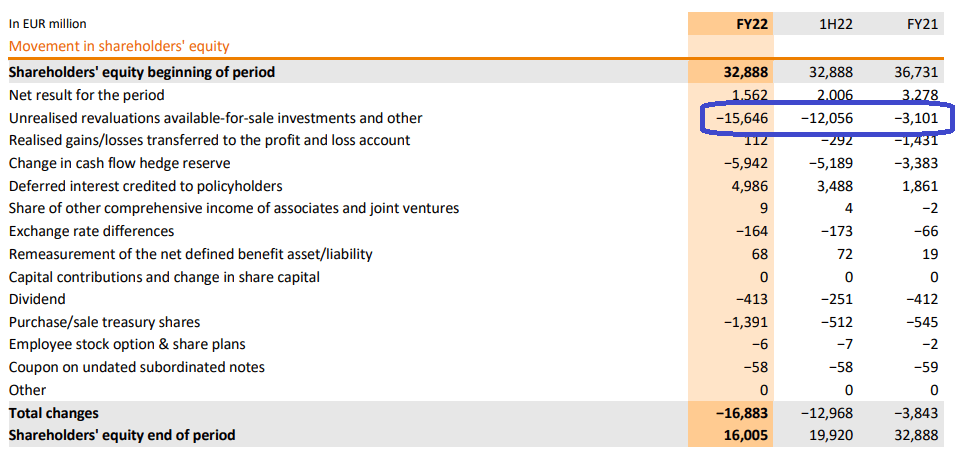

The image above also shows that almost 40% of the assets is held in securities available for sale, and that the value of those securities decreased by about 26B EUR during 2022. This does not mean NN Group recorded a 26B EUR loss on those assets, but the image below shows there was a rather substantial unrealized loss of 15.6B EUR on those securities in 2022.

{kind=link}

Perhaps even more surprising is the fact that almost 80% of the full-year loss was generated in the first half of the year, while the benchmark interest rates only started to increase in the second half of this year. This for sure does not mean the pain is over as additional rate hikes are to be expected, but I do think the risk should be manageable for NN Group.

As mentioned above, an insurance company has the luxury of treating the securities AFS as HTM as there usually is no urgent need to get liquidity and the main parameter we will have to keep an eye on is the equity value on the balance sheet as insurance companies likely won't be hit with a liquidity crisis but with a solvency crisis.

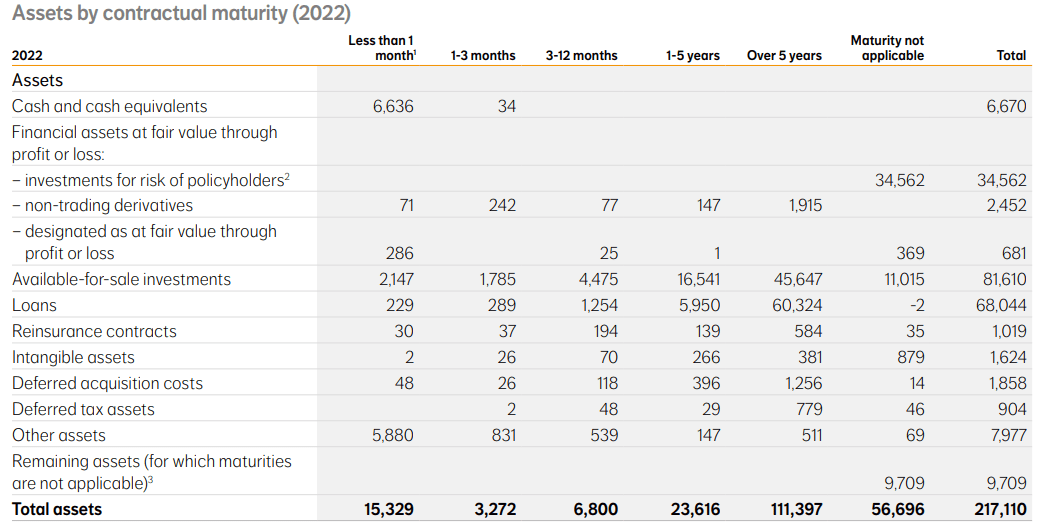

First of all, it is important to understand the duration of the sums invested in the securities AFS. Footnote 39 to the annual report provides an excellent overview. As you can see below, about 2.15B EUR of the portfolio has already matured in January while a cumulative 3.9B EUR will mature by the end of this quarter. That's about 5% of the portfolio. That doesn't sound like much, but that 5% will be recouped at 100% of the principal value.

{kind=link}

Over the next three quarters, an additional 4.5B EUR in securities AFS will mature which means the valuation risk on those securities will also be close to zero as every day that goes by, the bonds will trade closer to the par value. This means that with about 8.4B EUR (or 10.5% of the AFS portfolio) maturing this year, I think there's very little [re]valuation risk, which means the underlying 73B EUR carries a higher risk. Unfortunately the vast majority of those loans (about 60%) will only mature beyond 5 years from now (and likely even longer) so that is where the risk is at. I'm not worried about the 68B EUR loan portfolio (which mainly consists of residential mortgages), but the 46B EUR in securities AFS with a maturity of longer than 5 years will be the issue NN Group will have to deal with.

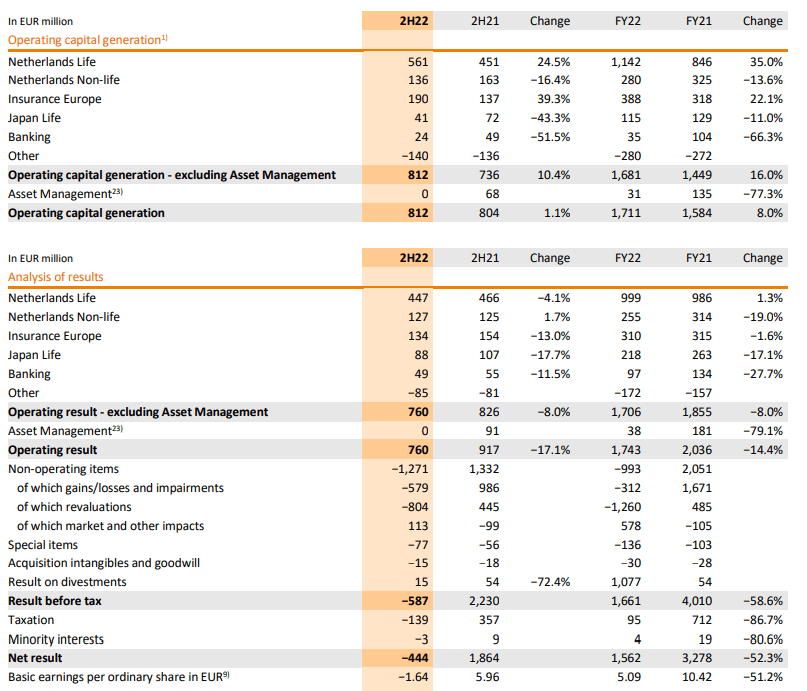

That is not 'mission impossible'. Looking at the 2022 results, NN Group is generating about 1.7B EUR in operating capital. Taxation was pretty minimal and the basic EPS was 5.09 EUR per share of 1.56B EUR as you can see below.

{kind=link}

This includes a positive 1.08B EUR contribution from selling a division to Goldman Sachs, but it also already includes about 1B EUR in non-operating items (including impairment charges and revaluations that do flow through the P&L statement). So it is reasonable to assume NN Group generates about 1.6-1.7B EUR per year in operating capital which it can use to A) cover losses and charges that are subject to the income statement reporting standards and B) add the remainder to the equity portion on the balance sheet to shore up the equity position.

There's one issue here: NN Group currently pays a dividend of 2.79 EUR per share, which results in a total cash outflow of 781M EUR using the current share count of approximately 280M shares.

While this still leaves about 1B EUR per year in capital growth on the table to strengthen the balance sheet, let's not forget NN Group also targets to repurchase 250M EUR in shares per year. But let's argue that will be put on hold. We can also expect the stock dividend to be pretty popular, so let's assume there is a take-up rate of 50%. That means the insurance group is retaining about 1.3B EUR per year in earnings. While that sounds great in absolute numbers, it's really not that high given the total size of the AFS portfolio as 1.3B EUR is just 0.6% of the entire asset base.

There may be a small silver lining here. The 8B EUR in securities AFS that will mature this year will likely be reinvested at a 300-350 basis point higher return, which will bring in about 250M EUR pre-tax and about 200M EUR in after-tax earnings. That will help to boost the potentially retained capital to 1.5B EUR per year but that still is pretty low given the 70B+ EUR of securities available for sale that are not maturing this year.

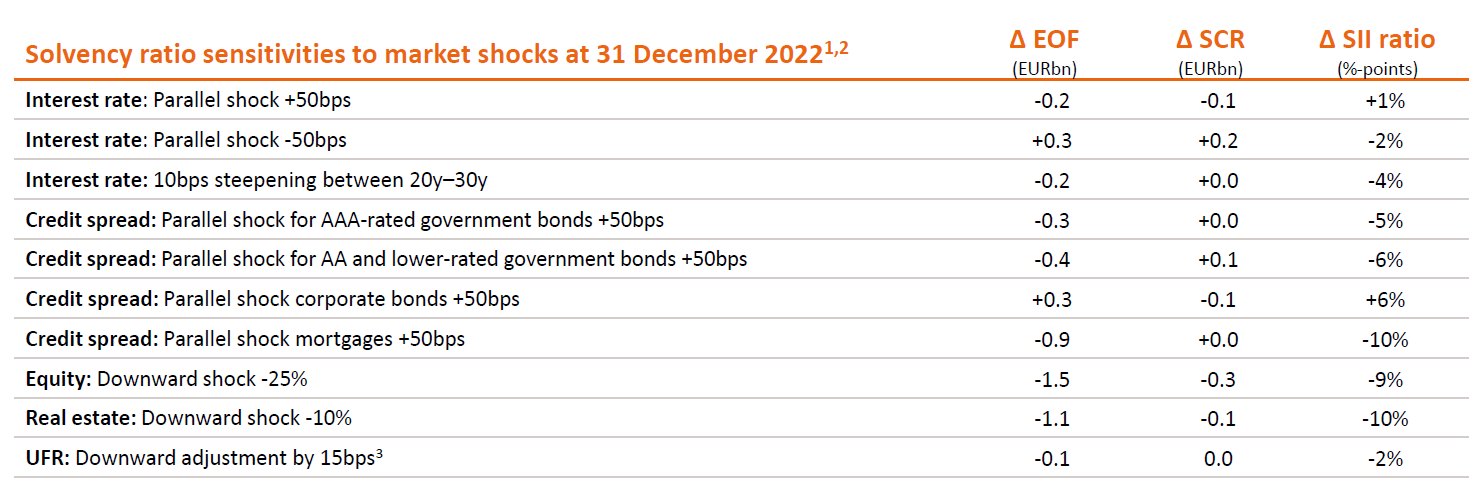

That could potentially be pretty dramatic, but NN Group also provided a sensitivity analysis showing the impact of interest rate shocks on the solvency rate (which was 197% as of the end of 2022, an increase from 196% a year earlier while the final dividend is already included in this calculation). As you can see below, a parallel shock of 50 basis points will actually increase the solvency ratio and the credit spread shocks will actually have a higher impact on the solvency ratio than purely an interest rate increase.

{kind=link}

All things considered, the impact of increasing spreads and interest rates on the solvency ratio is still pretty benign. That's mainly because the higher interest rates have no impact on the valuation of the liabilities as those were established using the interest rates at inception. And this puts NN Group in a special position. As the duration of its assets was matched with its anticipated liabilities at the date of inception, the books are balanced. But the main issue is the equity value on the balance sheet as increasing interest rates will further erode the book value of the company.

However, that does not necessarily have to happen. The recent shake-up in the financial sector has caused a 'flight to safety' and investors have been flocking back to government bonds. I am cautious but when I compare the interest rate of the countries NN Group has invested most of its debt in, I am actually cautiously optimistic on potentially a positive revaluation of the AFS portfolio in Q1.

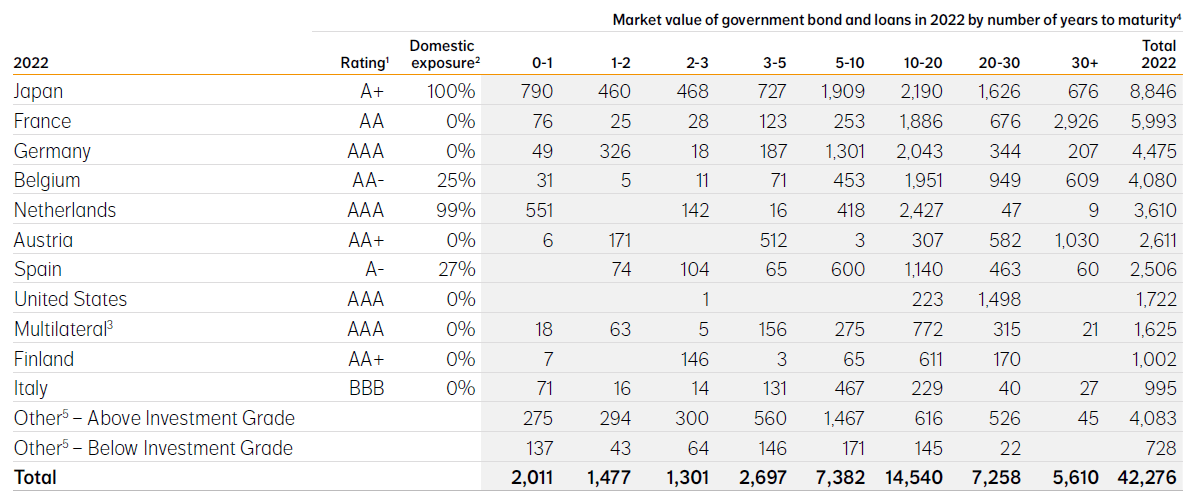

About 42B EUR of the securities AFS portfolio consists of government bonds, and as you can see below, the five largest countries are Japan, France, Germany, Belgium and the Netherlands which represent about 27B EUR or 64% of the government bonds in the portfolio, and in excess of 30% of the entire AFS portfolio.

{kind=link}

The image below shows the 5 year government bond rate as of the end of 2022 and the current rate for the 3, 5 and 10 year government bonds (not a perfect comparison but a close enough mix between short term and longer term bonds).

Author's table

As you can see above, the government bond yields in NN's most important markets have gone down since the end of last year. 'The best cure for low oil prices is low oil prices'. Well, the opposite is true in the government bond market: thanks to the panic on the markets and the rapid flight to safety, there could very well be a theoretical GAIN on at least this portion of the AFS portfolio in the current quarter.

That's the theory. We simply don't know what NN group did in the past 10 days. If they sold a chunk of securities during the panic selling then it won't see a sudden increase in its securities portfolio. Additionally, the portfolio also contains corporate bonds and credit spreads may be different there. But based on the evolution of the interest rates on the government bonds in the AFS portfolio, NN Group likely is not headed towards a disastrous first quarter.

Investment thesis

Right now, the biggest uncertainty in Europe is the potential fallout from the Credit Suisse ( CS ) problems. Although NN Group likely doesn't have any direct exposure, a collapse of Credit Suisse would send the same ripple effect through the European markets as SVB Financial ( SIVB ) had.

NN Group hasn't provided a lot of details on its exposure to increasing interest rates and how that impacts the book value. We know the impact on the solvency ratio is rather low but I am unsure about how the equity value on the balance sheet will hold up. I'd rather want NN Group to be safe rather than sorry so I hope the insurance company decides to make the stock dividend as attractive as possible while suspending its share buyback program until this has all been sorted out. It was encouraging to see Moody's ( MCO ) came out with a rating upgrade for NN Group from Baa1 to A3 .

That being said, I speculatively added to my position in NN Group (knowing very well it for sure is not a 'safe bet') and I wrote a few out of the money put options as well. The management has proven in the past it knows what it's doing and I like the relatively low impact of the interest rate increases on the solvency ratio of the business. I hope NN Group will provide an interim update before it reports on its Q1 results to reassure the rattled market and I would rather want to wait for that before substantially increasing my position.

For further details see:

NN Group: The Drop In Sovereign Bond Yields Is Good News