NNGRY - NN Group: Unexpected Ruling Puts Provisions In The Spotlight

2023-11-14 13:06:29 ET

Summary

- NN Group has experienced growth and increased shareholder returns since its spin-off from ING Group.

- Ongoing litigation regarding unit-linked securities has significantly affected NN Group's share price.

- The company faces uncertainty and potential provisions for litigation, which will be clarified in the 2H23 results presentation in February 2024.

- Freezing the dividend and suspending share buybacks will allow management to continue rewarding shareholders while building a provision for a potential adverse outcome of the litigation.

- In February 2024, management will give an update, meaning uncertainty will linger thereby putting pressure on the stock.

Since NN Group ( NNGPF ) ( NNGRY ) was spun-off its former parent ING Group ( ING ) ( INGVF ) , the company has grown and increased shareholder returns. Nevertheless ongoing litigation concerning unit-linked securities has significantly affected the share price in recent weeks.

The reduction in share price has given the dividend yield a boost with the forward yield topping 9 percent. On the downside, estimates for the cost of litigation, in case of an adverse ruling for NN Group, vary from €390 million to €4.7Bn.

How management will perform the balancing act between shareholder returns and provisions for litigation will become clear on the 29 th of February 2024 when the 2H23 results are presented. Until then, the dividend seems appealing but the uncertainty brought by ongoing litigation will linger. Although the risk appears manageable, short term the stock will likely trade lower.

Company overview

During the Great Financial Crises the Dutch financial conglomerate ING Group received support from the Dutch government to shore up the balance sheet. One of the conditions for this support was the spin-off of insurance and investment banking activities by ING. This business segment was therefore made a separate entity and on the 2 nd of July NN Group became listed. Two years later ING had divested the entire shareholding in the group.

As such, the NN Group has a relative brief history on the stock market and many key positions are held by former ING staff. For example, until 2019, the company was run by CEO Lard Friese who held various position in the insurance sector before landing at ING. The current CEO, David Knibbe, took over the helm in 2019 and spent his entire career at ING until the NN Group spin-off.

Secondly, in spite of a presence in Europe and Japan, the company pre-dominantly operates in the Dutch market. Figure 1 shows a customer base spread over 11 countries, but this view requires nuance.

{kind=link}

Figure 1 - Company overview, annual report 2022 (nn-group.com)

If the Operating Capital Generation [OCG] is assessed, it follows about three quarter of capital is generated in the Netherlands. The other quarter is generated from the presence in 10 other countries. To pursue growth, investments will have to be done outside of the Netherlands as that market is rather saturated. In this respect it must be noted NN Group took over the business activities of MetLife ( MET ) in Poland and Greece.

Figure 2 - Operating Capital Generation per business segment based on 1H23 OCG, Company Profile August 2023 (nn-group.com)

Cash cow

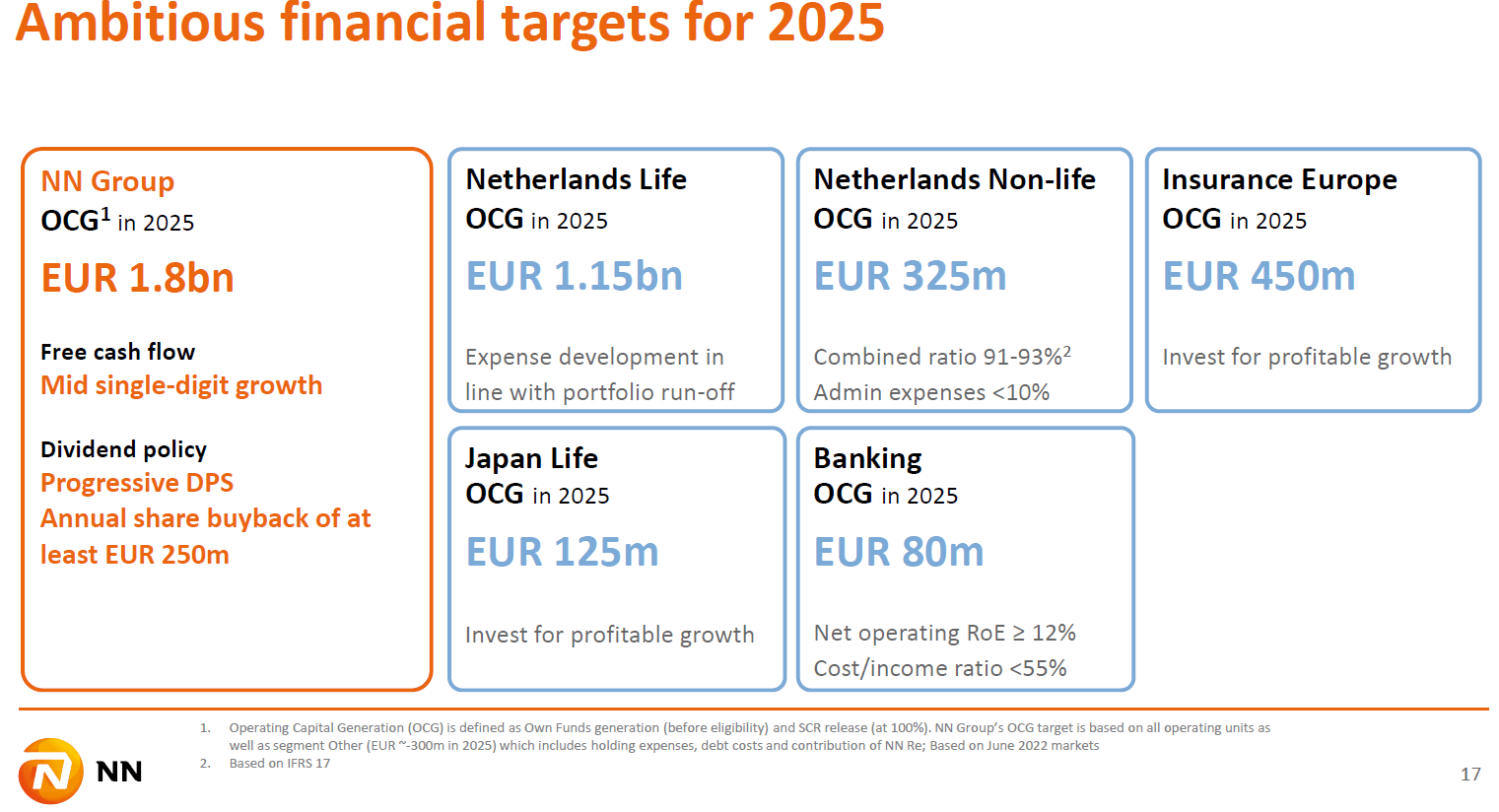

The notion growth must come from other geographies than the Netherlands is further substantiated by the targets, see figure 3. The aim is to drive strong cashflow in the Dutch home market and invest for profitable growth in Europe and Japan.

{kind=link}

Figure 3 - 2025 Financial targets, Company Profile August 2023 (nn-group.com)

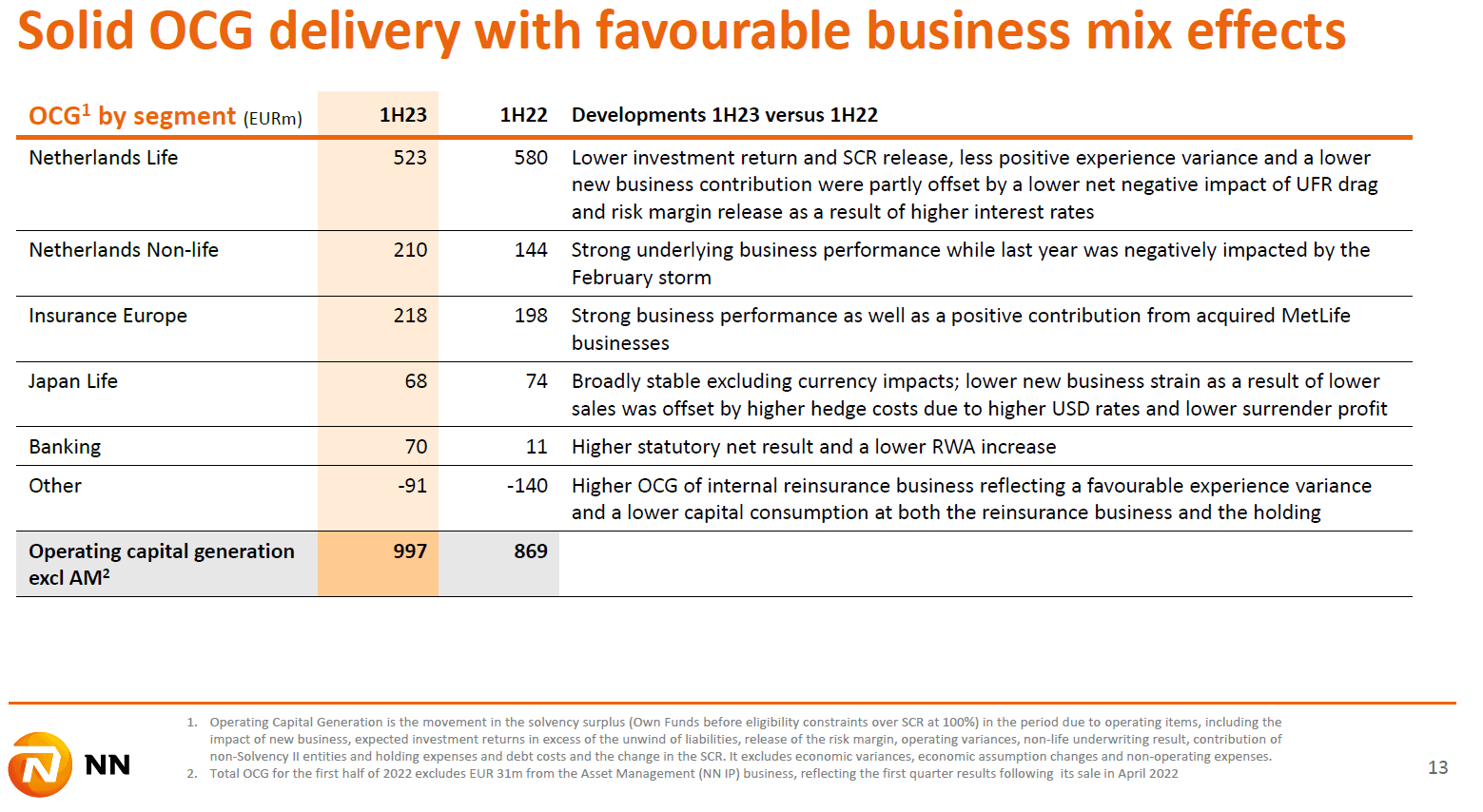

As it stands, the ambitious financial targets seem well within reach if the 1H23 performance is referenced, see figure 4. Total generation is about €1Bn for the first half of the year and the performance of each and every business segment aligns with the targets as well.

{kind=link}

Figure 4 - 1H23 Operating Capital Generation per business segment, 1H23 results presentation (nn-group.com)

Either 2023 is a year with massive tailwinds, or the company has been relatively modest settings its targets. If the comments accompanying the 1H23 performance in figure 4 are taken as reference, there are some positives but to speak of massive tailwinds would be an exaggeration. In this respect, the OCG goals set by management appear not so ambitious.

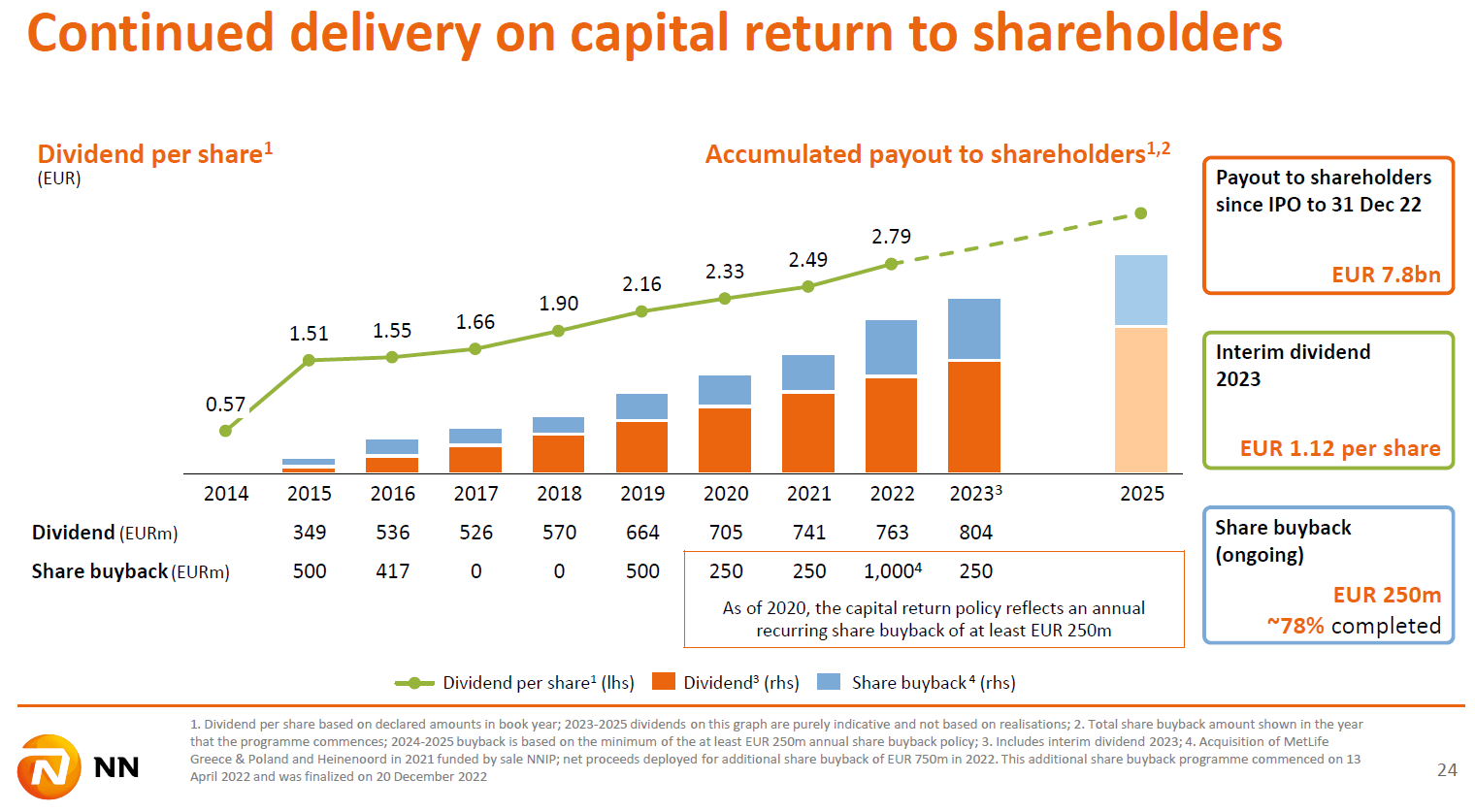

More ambition is displayed by the shareholder returns, see figure 5. The figure uses a favorable presentation as the cumulative returns are displayed. Nevertheless, the dividend growth is commendable at a compound annual growth rate of more than 9 percent if 2015 is taken as the starting year.

{kind=link}

Figure 5 - Historic shareholder returns, 1H23 results presentation (nn-group.com)

The generous dividend is further supported by annual share buybacks. On top of this, the company ‘intends to neutralise the dilutive effect of the stock dividend through repurchase of ordinary shares ’ according the dividend policy .

Alleged profiteering

While the company generates a lot of cash and lets investors share in this splendor, there is a catch. As stated in last years’ annual report:

"Since the end of 2006, unit-linked products (…) have received negative attention in the Dutch media, from the Dutch Parliament, the Netherlands Authority for the Financial Markets (…) and consumer protection organisations. Costs of unit-linked products sold in the past are perceived as too high and Dutch insurers are in general being accused of being less transparent in their offering of such unit-linked products."

What followed was lengthy litigation in which NN Group seemed to have the upper hand. However, on the 26 th of September 2023 the court in The Hague served a ruling in favor of the plaintiffs. Apart from the stock taking a beating the day after, several persons and institutions offered their view on the potential provisions NN Group would have to make.

Estimates for the actual provisions vary from €1k to €15k per insurance policy. The problem however is these estimates are subjective, the upperbound for example was a number floated by the spokesperson of the plaintiffs. This party obviously has merit by plugging a high number to benefit from what is called the anchoring effect in psychology.

On top of this there is no clarity whether the compensation is valid only for active insurance policies, or if inactive and closed policies are eligible as well. For reference, the amount estimated by Morningstar for the active policies and using the upperbound per-policy number, the total provision becomes €4.7Bn.

The lowerbound is given by analysts from ING, estimating the provision to be about €390 million. However, this estimate received criticism after which the analysts bumped the figure to €739 million.

On top of the compensation, under Dutch law creditors have the right to claim what is called ‘legal interest’. Basically, it is stated by law that payment arrears are subject to interest. While this interest rate is tied to the rate on capital markets, it stands at 6 percent at the time of writing. In other words, on top of the potential compensation, creditors have the right to claim interest over the amount that has been withheld by, in this case, NN Group. Given the compensation to be paid is not clear, it will be even harder to estimate the owed interest. Therefore the compensation estimates ex-interest will be used in this article. It must be noted however that an interest rate of 6 percent means the amount has doubled after 12 years. As just the litigation is ongoing for 10 years already, the knock-on effect of interest may be very substantial.

If anything, the estimates indicate there is a lot of uncertainty, but the potential effects of the upper and lowerbound estimates can be assessed on a per share basis. At the 31 st of October nearly 274 million shares were outstanding . Therefore, the lowerbound €390 million estimate equates to a risk of about €1.5 per share, whereas the upperbound accounts for more than half of the €8.5Bn market cap. With a EUR/USD exchange rate of 1.06, the provisions vary from US$1.60 to US$18 per share.

The lowerbound scenario

The lowerbound risk of about US$1.60 per share will change very little for shareholders. In all likelihood the company will maintain the dividend and continue the share buybacks. If the provision comes in this low, there likely will be a relief rally which will offset the per share costs of the litigation. Therefore, the lowerbound scenario is more a business-as-usual situation. The trailing twelve month dividend yield currently exceeds 9 percent according the dividend page here on Seeking Alpha, and this does not yet account for the upward potential of the stock price if litigation can be finalized.

The upperbound scenario

A dire picture emerges when the upperbound scenario is assessed. Based on the assumption total costs will become €4.7Bn, the finances of the company will look totally different. First off, translating this into the share price, the current value of more than US$33 could drop to about US$15 assuming the costs are fully translated into the market cap.

The price will potentially drop even further given a portion of investors merely hold this stock for the high dividend. As it stands, the company is able to return more than €1Bn per year to shareholders. However, in case a court orders NN Group to compensate the plaintiffs, they will become the beneficiaries rather than the shareholders. As such, one could argue shareholders will be deprived of more than four years of returns.

In case the company needs to shore up the cash to compensate customers, it remains speculation how this will be done. Available cash can be used, parts of the business can be divested, shareholder returns cancelled, new equity issued and so on. As the company is performing well and has options, the risk is not if the investment will dissolve through bankruptcy, but rather how long a shareholder needs to stay invested to recoup its loss.

The base case

While litigation is ongoing and there is little known about the height of a potential settlement, the assumption is made there may be a settlement in the order of €1 to €2Bn. This number takes the ING estimate into account, rounded up to €1Bn. Given the ease with which the analysts increased the estimate, and the potential risk of interest payments to be made, a safety factor of two is applied, to arrive at the value of €2Bn. On a per share bases this would amount to €7.30 or US$7.73.

An additional reason why the potential compensation must be capped is the consolidation that has taken place in the Dutch market. Figure 4 shows NN Group and ASR, another defendant in the unit-linked policies case, combined control 42% of the Dutch Non-life markets. Mind this does not yet account for Life division meaning the presence of NN Group in the Netherlands is even larger. Therefore the judges delivering a ruling in this case have to weigh the fact that these players have a societal function by guaranteeing insurance for many Dutch citizens. In case it comes to a ruling against NN Group, the compensation has to hurt, but can’t be outsized.

Figure 6 - Effect of consolidation in Dutch insurance market, 1H23 presentation (nn-group.com)

As litigation is still ongoing and time will be needed to work out all details in case a final adverse verdict is delivered, the company has time to make provisions.

Given the latest ruling is the first set back over the course of many years of litigation, management will have to start making provisions. Therefore I assume the dividend will be frozen and buybacks cancelled. This course of action will allow management to continue high pay-outs to shareholders at 9% dividend yield while simultaneously allocating funds for a possible adverse outcome of the court case. Given the potential €2Bn hit, an annual provision seems minor, but even if NN Group would lose in court, it is estimated several years will be needed before actual pay-out will be done.

As the company only reports results every 6 months, the next investor update will be a the 29 th of February meaning patience is required to learn which course of action will exactly be taken.

In the meantime, adding to the uncertainty is the fact further downside may emerge if, based on a potential favorable outcome for the plaintiffs, other parties will start litigation, from the 2022 annual report:

"The book of policies of NN Group’s Dutch insurance subsidiaries dates back many years, and in some cases several decades. Over time, the regulatory requirements and expectations of various stakeholders (…) have developed and changed, increasing customer protection. As a result, policyholders and consumer protection organisations have initiated and may in the future initiate proceedings against NN Group’s Dutch insurance subsidiaries alleging that products sold in the past fail to meet current requirements and expectations. In any such proceedings, it cannot be excluded that the relevant court, regulator, governmental authority or other decision-making body will apply current norms, requirements, expectations, standards and market practices on laws and regulations to products sold, issued or advised on by NN Group’s Dutch insurance subsidiaries."

Buybacks accelerated

After the ruling on the 26 th of October, NN Group bumped its share buybacks. During the nine trading days following the ruling, 5.4 million shares were bought and the company finalized its buyback program as shown by the transaction history for the March 2023 to February 2024 program . Moreover, the amount of buybacks done account for approximately half of average daily volume on the Amsterdam stock exchange. Inevitably this has supported the price.

While the company supported the stock through buybacks, the current stock price is back at 2017 levels if the covid effect is neglected. Also, in January 2022 the stock price almost reached a price level of US$60, after which the stock started its descent. With the company having finalized the buyback program, the post-ruling support disappears and uncertainty is left especially as the next official investor update is months away.

Conclusion

Since NN Group was spun-off its former parent ING Group, the company has grown and increased shareholder returns. Nevertheless the stock price nearly halved since it reached a high in January 2022. To a large extent this drop was caused by a ruling against NN Group concerning the litigation on unit-linked securities.

Although lower and upperbound estimates vary a lot, potentially affecting the company by an amount of US$18 per share, my base case is a provision of €2Bn needs to be made. This value equates to a potential provision of US$7.73 on a per share basis.

As management has to take action after the latest ruling, it is expected the dividend will be frozen and buybacks cancelled. This course of action will allow management to continue high pay-outs to shareholders at a 9% forward dividend yield while simultaneously allocating funds for a possible adverse outcome of the court case.

Which course of action management will take becomes clear at the update in February which is still several months away. Although the dividend is appealing, the uncertainty brought by ongoing litigation will linger. Short term the stock will likely trade lower making this a Hold.

For further details see:

NN Group: Unexpected Ruling Puts Provisions In The Spotlight