NOMD - Nomad Foods: A Stable Performer

2023-12-12 00:06:40 ET

Summary

- Nomad Foods manufactures and distributes frozen foods in Europe.

- The company has achieved growth through acquisitions and a very modest organic growth.

- Despite high debt, Nomad Foods seems stable as the company's operating earnings have proven good stability.

- The stock price seems to have some upside left with a forward P/E of 9.1 and with my DCF indicating upside.

Nomad Foods ( NOMD ) manufactures and distributes frozen foods in Europe with a focus on countries such as the United Kingdom, Italy, and Germany. The company sells through brands such as Findus, Birds Eye, Iglo, Frikom, and Ledo. Around 40% of the company’s revenues come from fish products, 20% from vegetables, 10% from ready meals, and the rest from other products including frozen poultry and pizza.

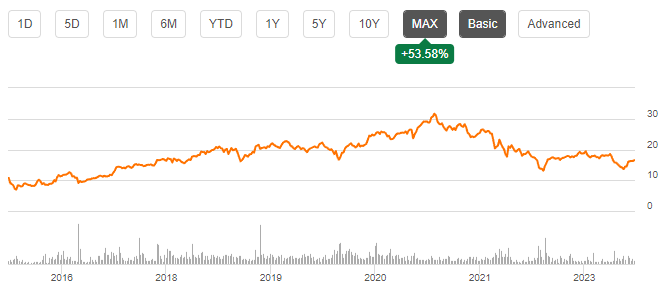

After the stock began trading in early 2016 after the anchor acquisition of Iglo Group, the stock price appreciated in a very stable manner until 2021, as rising interest rates started to affect both Nomad Foods’ EPS and required return:

{kind=link}

A Modest History of Growth

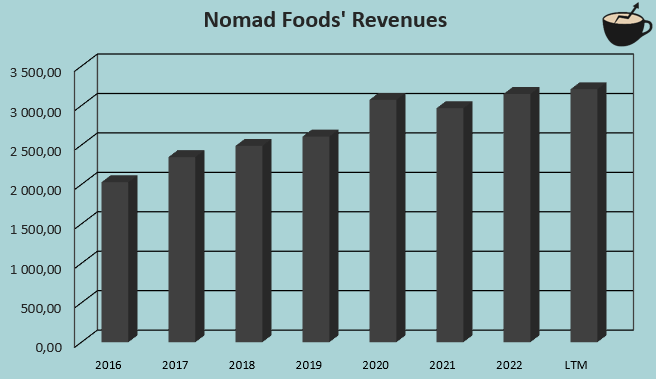

Nomad Foods has been able to grow revenues through acquisitions and some organic growth. From 2016 to trailing figures as of Q3/2023, the company has achieved a CAGR of 7.0% :

Nomad Foods' Revenues () (Author's Calculation Using Seeking Alpha Data)

{kind=link}

The growth shouldn’t be extrapolated into the future, though; Nomad Foods has had significant acquisitions to boost the growth. Most notably, the company acquired Fortenova’s frozen food business in Q3 of 2021 for around 615 million euros, adding 279 million euros to the company’s revenues. In the prior year, Nomad Foods also acquired the Findus brand for around 110 million euros. Compared to the current market capitalization of 2.6 billion euros, the total contribution of past acquisitions is quite significant.

Great Stability Despite High Debt

Despite some challenges with inflation, Nomad Foods’ operational earnings have stayed very stable in recent quarters. In the Q3 results reported on the 9 th of November, Nomad Foods reported an organic revenue growth of 1.6%; revenues seem to reflect a stable position in the market. The company did have a good amount of cost inflation that Nomad Foods wasn’t able to completely translate into higher customer pricing – Nomad’s gross margin fell by 0.7 percentage points year-over-year along with SG&A inflation, leading to a lower EBIT margin of 14.6% compared to previous year’s Q3 EBIT margin of 16.8%. In total, the margin change was still quite minimal in significance in my opinion.

The cost inflation does seem to be somewhat of an issue – in addition to a margin hit for Nomad Foods, the company seems to have had lower volumes in Q3. In Nomad Foods’ Q3 earnings call , CEO Stefan Descheemaeker told that the company has lost volumes due to lost business with a few retail partners – the achieved low growth is due to higher pricing in the highly inflationary economy instead of volume increases. Nomad Foods is planning to increase its marketing spend significantly, and has already seen good progress in volumes for Q4, expecting the positive trend to continue into 2024.

On a long-term basis, the company has very good margin stability. From 2016 to current trailing figures, the company currently has its lowest trailing EBIT margin at 13.5%, with a high of 15.1% in 2021; the EBIT margin fluctuates within a tight range despite challenges concerning inflation and the Covid pandemic in previous years – the operations are very stable in nature, as demand for frozen foods stays very constant.

Taking from shareholders’ stability, though, is Nomad Foods’ leveraged balance sheet . The company holds over $2.2 billion in long-term debt, almost the size of Nomad Foods’ market capitalization at the time of writing. With trailing figures, interest expenses account for around 23% of Nomad Foods’ EBIT; because of the stable operations, I don’t believe that the high amount of debt makes Nomad Foods a particularly risky stock, as even with rising interest expenses the company’s bottom line for shareholders is mostly stable.

Some Upside Left in Valuation

Nomad Foods’ current forward P/E multiple is quite low at 9.1. The multiple is well below the stock’s average of 12.8:

{kind=link}

With Nomad Foods’ stable operations, the low P/E seems irrational. A discounted cash flow model further estimates that the stock price has upside left with a continued stable level in operations.

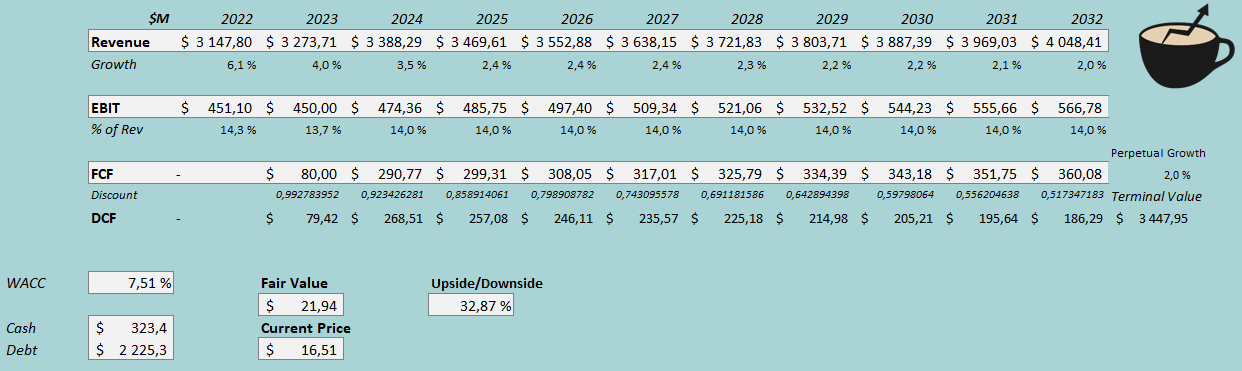

In my DCF model, I estimate a revenue growth of 4% for 2023, which slows down into a perpetual growth rate of 2% in steps. The revenue estimates represent Nomad Foods’ increased marketing spend, contributing to the growth estimate of 3.5% in 2024. The model doesn’t account for further acquisitions, constituting very modest estimates.

For Nomad Foods’ margins, I estimate a stable performance with a 14.0% EBIT margin in 2024 and forward. The estimate is slightly up from a 13.7% EBIT margin estimate for 2023 as a result of a more stable inflation rate, which I estimate to contribute slightly positively to Nomad Foods’ margins. The company’s cash flow conversion is modestly good, although quite constant restructuring changes seem to worsen the conversion from EBIT. With the mentioned estimates along with a cost of capital of 7.51%, the DCF model estimates Nomad Foods’ fair value at $21.94, around 33% above the stock price at the time of writing – the stock seems to have upside left.

DCF Model (Author's Calculation)

{kind=link}

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q3, Nomad Foods had $26.4 million in interest expenses. With the company’s current amount of interest-bearing debt, Nomad Foods’s annualized interest rate comes up to 4.75%. Nomad Foods utilizes a great amount of debt in its financing, as the company’s operations are very stable – for a long-term debt-to-equity ratio, I estimate 50%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.25% . Nomad Foods’ operations are in Europe, and the fair equity risk premium should be taken from the company’s operative footprint; to get a rough estimate, I use the average of the United Kingdom’s, France’s, Germany’s, and Croatia’s equity risk premium, as the countries represent some of Nomad Foods’ major markets. With Professor Aswath Damodaran’s latest estimates , the average of the countries’ equity risk premiums is 6.14%. Yahoo Finance estimates Nomad Foods’ beta at a figure of 0.82 . Finally, I add a small liquidity premium of 0.2%, crafting a cost of equity of 9.48% and a WACC of 7.51%.

Takeaway

At the current price, Nomad Foods seems to be a stable pick. The company’s forward P/E of 9.1 seems low considering the company’s stable operations, which makes the stock likely to provide investors with stable returns. The company’s investors do have a meaningful risk concerning interest rates, though – the company’s high amount of debt, as well as lower-than-average WACC, make the DCF model’s fair value highly sensitive to interest rates. I still see the stock’s risk-to-reward favorable at the moment, and have a buy rating for the time being.

For further details see:

Nomad Foods: A Stable Performer