NOMD - Nomad Foods Stock: Solid Q2 Earnings Backed By Stabilizing Margins

2023-08-11 10:34:52 ET

Summary

- Nomad Foods is a European leader in frozen foods with a strong portfolio of leading brands.

- Second quarter earnings beat Revenue and EPS estimates.

- After two years of gross margin compression, They seem to have stabilized thanks to price increases.

- My Valuation suggests the company is trading below its intrinsic value.

Introduction

About a month ago, I initiated my coverage o f Nomad Foods ( NOMD ). The company reported second-quarter earnings on August 9th, 2023. In this analysis, I will explain my thesis in small detail and take a deep dive into the company's Q2 earnings.

Reaffirming The Investment Thesis

NOMD is a European market leader in Frozen foods (16% market share in countries of operation), underpinned by a strong portfolio of brands in staples like frozen fish and vegetables. I believe management is top-notch. Instead of expanding globally, they have focused their resources on acquiring top European brands to strengthen their presence and expand their reach in the continent.

The company also operates in a growing market. Historically, The European frozen food market has grown at 2%, and I expect it to keep growing because consumers love easy-to-cook meals in exchange for good value for money. I believe the company is still trading below its intrinsic value. Using the discounted cash flow analysis, I arrived at a fair value of $26.68, which equated to a 44% return from the current price.

Q2 Earnings & 23 Guidance

{kind=link}

Company's presentation

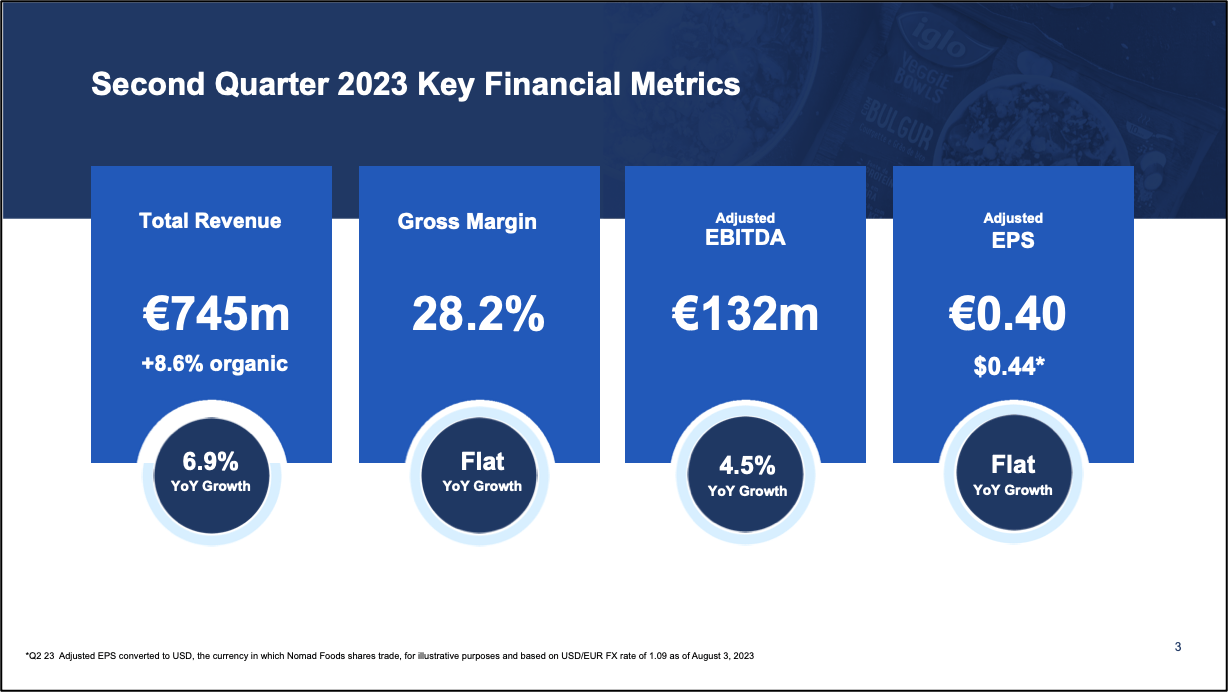

Nomad Foods reported good second-quarter earnings across the board, beating FactSet's revenue estimate by €4 million or $7.3 million and EPS by €0.03 or $0.04. Adjusted EBITDA of €132 million vs. FactSet's estimate of €127.9 million grew by 4.5% YoY, and EPS stayed flat. Gross margins stayed flat year over year due to the price increases that the firm had implemented.

90% of raw material costs are covered for 2023, and backed by solid cash flow generation, NOMD bought back €53 million worth of stock, reducing the share count by ~3.3 million in the quarter.

{kind=link}

Company's presentation

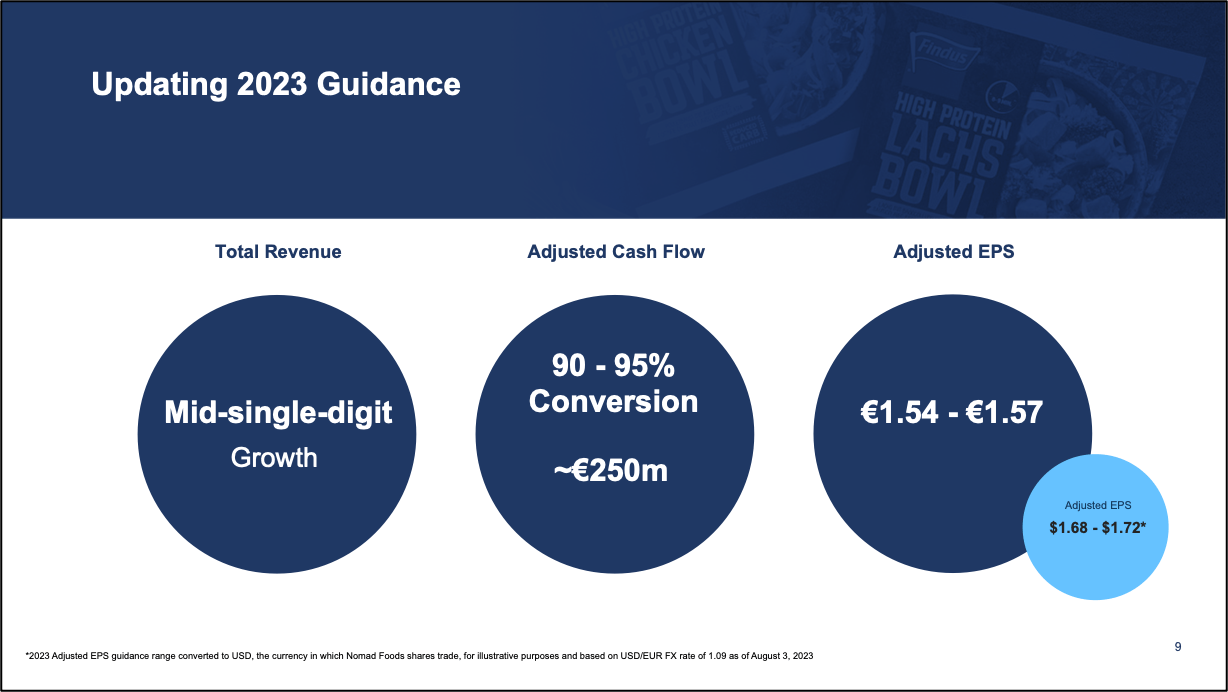

The company tweaked its guidance a little bit by revising its adjusted EPS target from €1.52-1.55 to €1.54-1.57, but it maintained mid-single-digit organic revenue growth and Adjusted Cash Flow conversion in the range of 90% to 95%.

NOMD highlighted in their presentation that Frozen Food is outperforming overall Food with double-digit sales growth year to date and more than half of its markets back in volume growth. As a result, the company expects market share and volume trends to improve sequentially in the second half. The firm believes that A&P investment will also help them gain market share in 2024 and beyond.

All in all, I believe the quarter was decent. The price increases that the firm implemented are starting to bear fruit. The company demonstrated strong organic growth, and 90% of the raw material costs for 2023 are covered. It is good to see gross margins stabilize, as they took a hit over the past two years due to price increases in raw materials. I believe the revision in EPS for 2023 indicates that either the company will buy more of its shares or profitability will increase. The CEO had this to say about buybacks in the earnings call :

We have been and will remain opportunistic on shares repurchased.

Valuation

In my last analysis of the company, Using a DCF, I arrived at a value of $26.20 per share. Post-earnings, My fair value is now $26.68 (+$0.48), which equates to a 44% return from the current price of $18.52. The bump in the price target is largely due to the company beating my estimate for Q2 in terms of revenue and profitability. I used a WACC of 8% and a terminal growth rate of 2%. I based my 2% growth rate assumption on the historic growth rate of the European savory frozen food market.

I model revenue to grow at an annual compounded growth rate of 2.82% from 2023 to 2027. For Q3-23, my revenue estimate is €779 million, EPS of €0.40 IFRS, and Gross margin of 28.20%. As for 2023, I expect the company to generate ~€3,068 million in revenue and an EPS of €1.27. NOMD had 174.4 million shares outstanding, cash of €389 million, debt of €2.2 billion, and a share price of $18.52.

Conclusion

The bottom line is that the strong momentum from Q1 earnings followed through to Q2. I believe the company is still trading below its intrinsic value, considering its long-term earning power, leading brands, market position, and great management team. The frozen food market seems to be outperforming its peers, which is understandable because consumers love easy-to-cook meals in exchange for good value for money. Long-term investments such as A&P will help NOMD further expand their footprint and reach new customers. In my opinion, the company seems to be in good shape going forward.

For further details see:

Nomad Foods Stock: Solid Q2 Earnings Backed By Stabilizing Margins