NHYKF - Norsk Hydro: Future Looks Bright But I Am Not Buying At This Price

2023-03-21 11:29:20 ET

Summary

- I have a long-term bullish thesis for Aluminum and expect demand to increase over time due to electrification and transition to green energy.

- Norsk Hydro is a very well-positioned player within the space, and it's one that I understand deeply due to my direct involvement with the company during my PE career.

- I discuss the way forward and why I'm not buying at this level.

Dear reader/followers,

Today I want to present my analysis of Norsk Hydro (NHYDY) which is the fourth largest producer of aluminum outside of China (and the seventh largest worldwide). The company is headquartered in Norway and has been on my radar since the very start of my Private Equity career because one of the very first deals I was asked to analyzed was an investment into an aluminum producing facility in Central Europe where Hydro was a 50% JV partner. I've followed the company closely since and today I want to share some of my insights with you to hopefully help you decide whether to invest or not.

Note: As with all European stocks I cover, the article is based on the native share, ticker NHY which can be bought on the Oslo Stock Exchange. For anyone not interested in the native share, there is also an ADR available under the ticker NHYDY.

Aluminum production

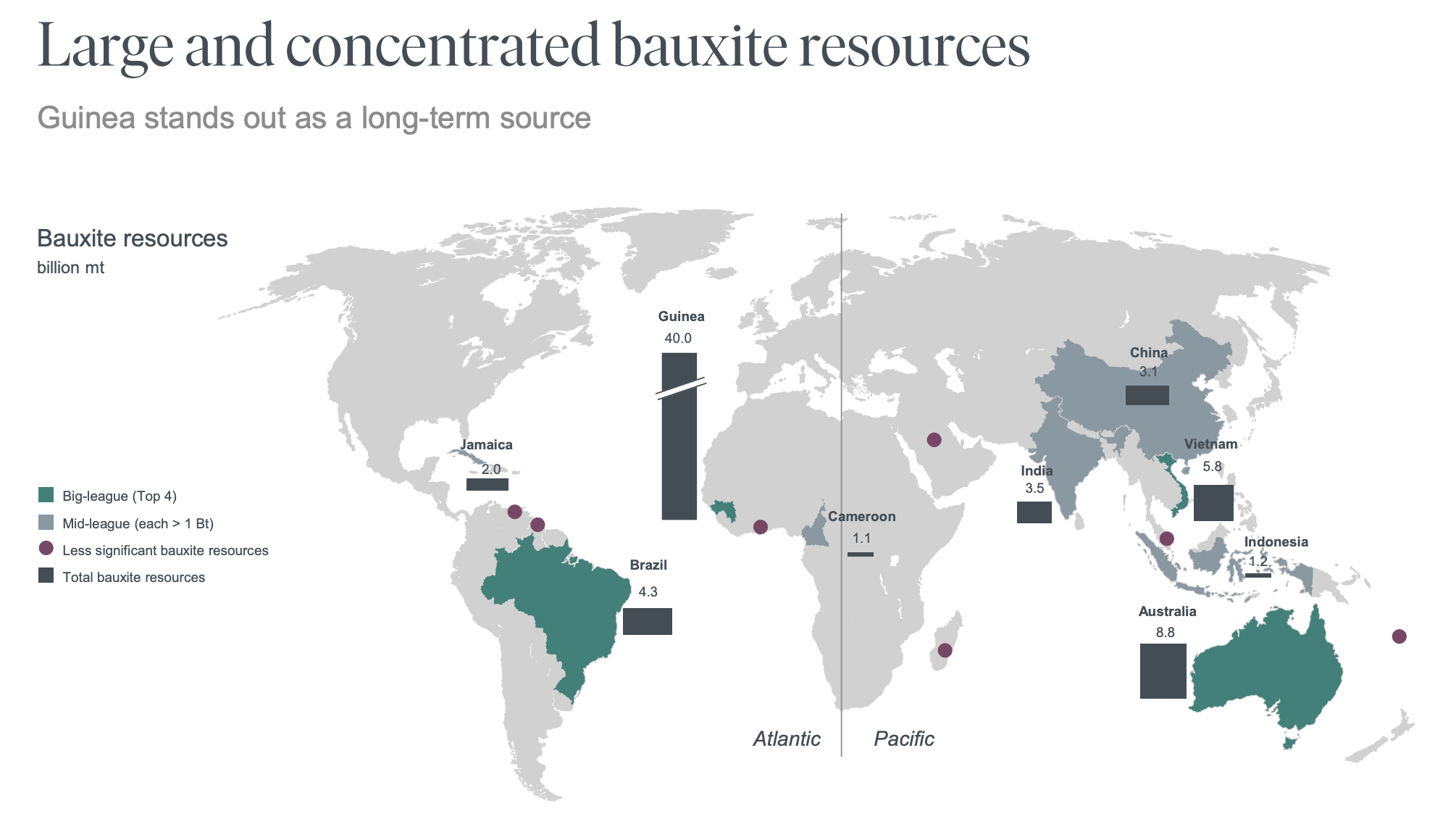

To understand the company, you first have to understand the process of aluminum production, so let's cover the basics. Unfortunately aluminum cannot be mined directly, because it only exists in nature as part of the bauxite ore. The majority of bauxite supply is concentrated in just a few places around the world, particularly in Guinea, Australia, Vietnam, Brazil, China and India. Transportation of bauxite would be costly, because it is essentially a rock that only has a fraction of aluminum in it so the first step of aluminum production always happens in close vicinity to the mine. This involves crushing the bauxite into powder and mixing it with water and chemicals to create alumina. This is done through what's called the Bayer process in case you want to research it further, but for our understanding of the business we just need to know that this always happens near the mine and it is very polluting process with a ton of very toxic waste.

The next step in the production involves dissolving alumina in cryolite and subjecting it to electrolysis (using electricity to split water into hydrogen and oxygen). This process transforms alumina into aluminum. Again the details are not important here, but what is that the process requires an immense amount of energy. That's why aluminum production facilities tend to be located in place that have abundant and cheap energy which usually comes from hydro power plants. Norway is a great example of such country and so is China. Once aluminum is made, the last step is to form it into beams through a process called extrusion, these beams are than sold on the market.

{kind=link}

So now that we understand the process it should be clear why to be a truly great aluminum producer, the company has to be global. It needs to mine bauxite and produce alumina in one part of the world, then finish the production process in another part of the world with cheap energy. Norsk Hydro is a global player and is involved in all part of the production process from mining bauxite in Brazil to producing aluminum and finally extruding it into beams. In addition to this the company also produced 9.4 TWh of hydropower in the Nordics which gives it access to cheap electricity and a unique advantage.

The company is also positioning itself to benefit from the green energy trend by strengthening their position in recycled and low-carbon aluminum production and diversifying into renewable energy. In terms of production costs Hydro is amongst the best in the world. Its cost for bauxite & alumina are in the 30th percentile while in the smelter business they are in the 17th percentile.

Aluminum demand

Aluminum is a great product. It is lightweight, corrosion resistant and conducts electricity well. Its properties make is essential for products that we use in our everyday lives. Moreover it will likely benefit from electrification of transportation (since batteries need a lot of aluminum) and the transition towards renewable energy which should increase demand from green transition by a factor of 2.5x over the next 7 years. Total global aluminum consumption is expected to grow by a CAGR of around 3% for the rest of the decade. I also want to point out that the future growth will be increasingly met from aluminum recycling which is expected to grow by over 5% annually.

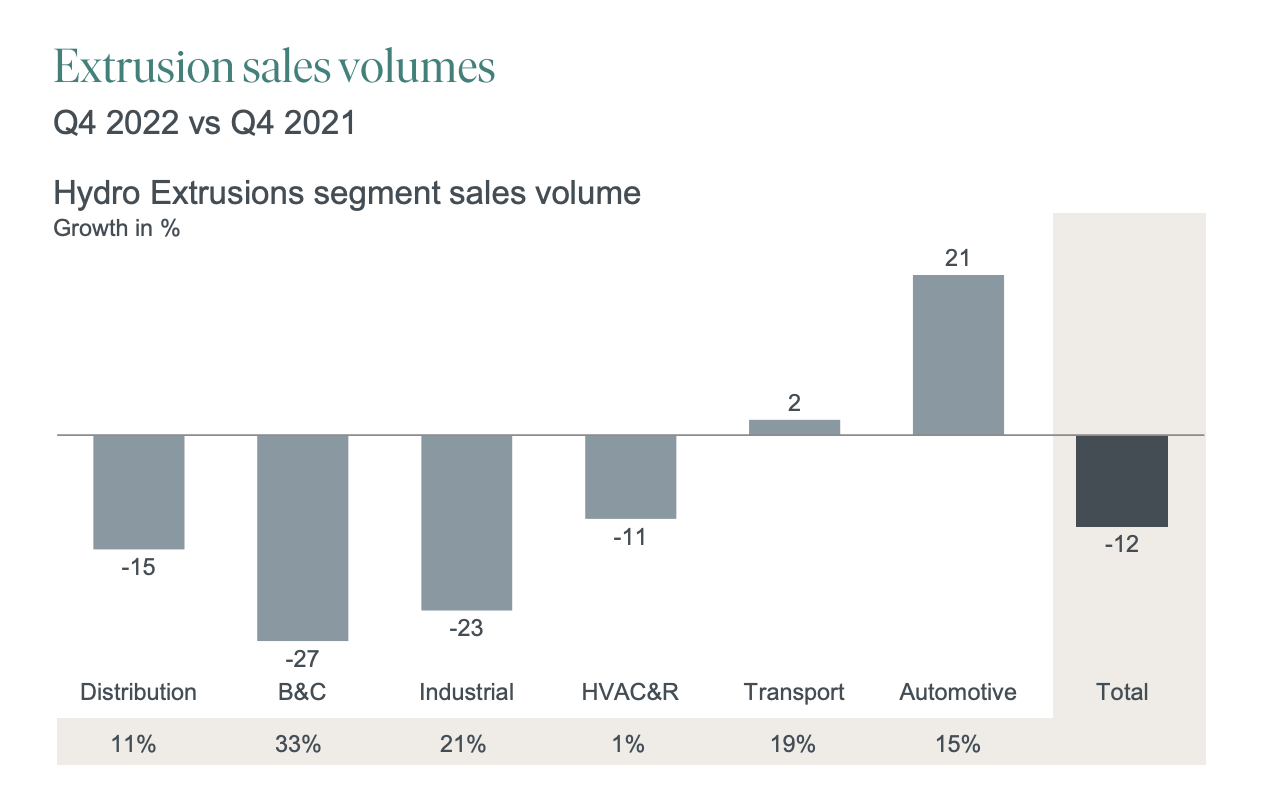

So over the medium to long-term I am not too worried, but meanwhile in the short term, it feels as though demand has peaked already. Aluminum prices peaked in May 2022 and have come down quite significantly since and extrusion sales volumes have declined across almost all categories in 2022 with the exception of automotive. This short-term weakness could very well materialize into a price decline, given the cyclicality of the business so it is something to pay attention to.

{kind=link}

Company financials

2022 results have been great as adjusted EBITDA increased by 36% YoY to almost NOK 40 Billion ($3.7 Billion). Adjusted EPS increased by over 50% to NOK 10.70 per share. The increase was primarily driven by a sharp increase in their biggest division - Aluminum Metal which increased by 70% YoY primarily due to higher commodity prices. The only division that saw a YoY decline was Bauxite & Alumina which declined due to lower Alumina prices and higher energy costs. What's important is that on a quarterly basis, all divisions except for Energy have seen a steady decline from the peak in Q2 2022 as a consequence of the drop in aluminum prices and a slight decline in extrusion volumes.

| Adj. EBITDA (mNOK) |

| 2021 |

| 2022 |

| delta |

| Bauxite & Alumina |

| 5 336 |

| 3 122 |

| -41% |

| Aluminum Metal |

| 13 500 |

| 22 963 |

| 70% |

| Metal Markets |

| 867 |

| 1 673 |

| 93% |

| Extrusions |

| 5 695 |

| 7 020 |

| 23% |

| Energy |

| 3 790 |

| 4 926 |

| 30% |

| 29 188 |

| 39 704 |

| 36% |

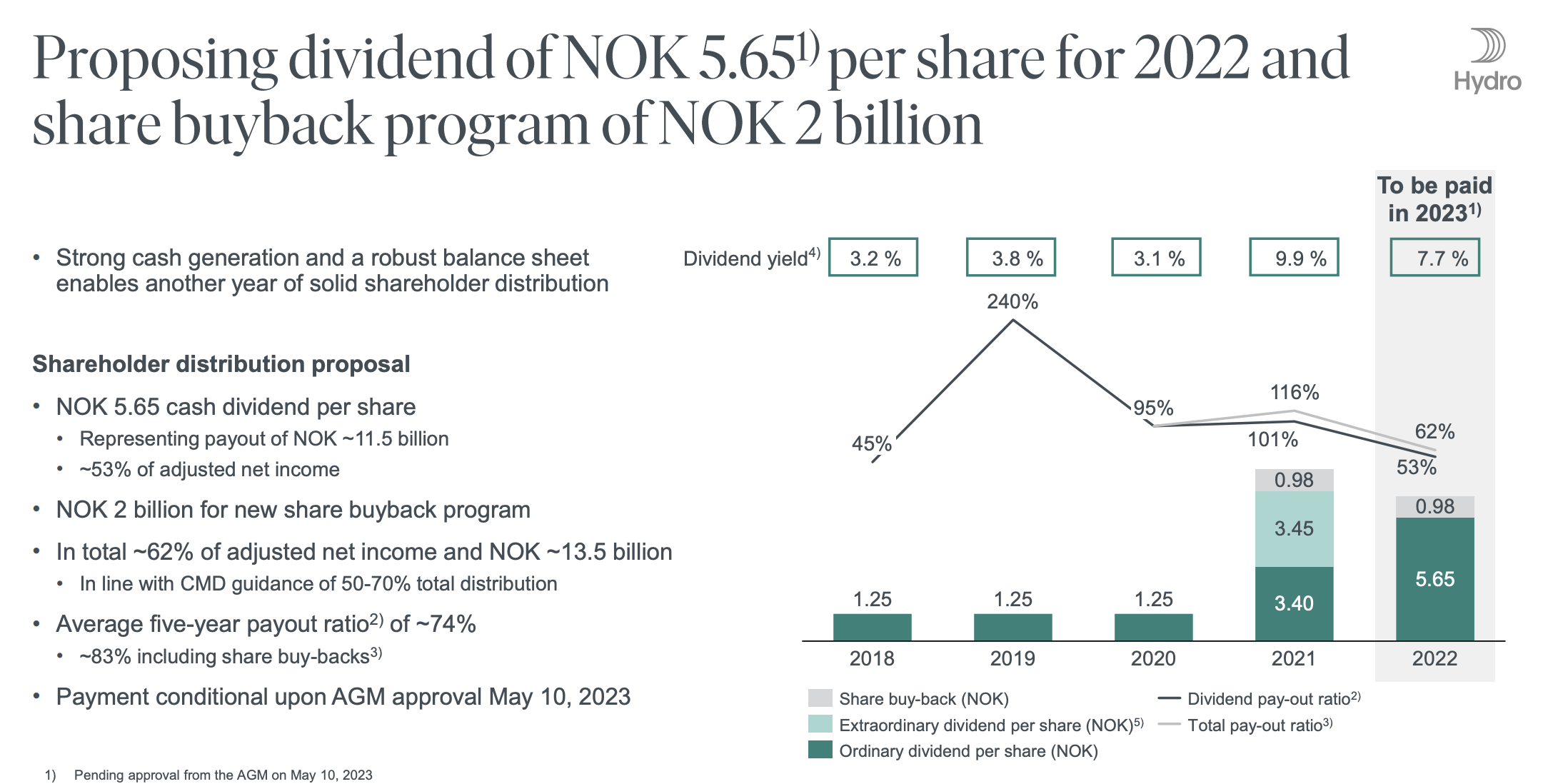

These good results have translated into a second consecutive year of extraordinary shareholder distributions while maintaining a record low payout ratio (just 53% of adjusted net income vs 5-year average of 74%). The dividend for 2022 has been proposed at NOK 5.65 per share which corresponds to a yield of 7.9% at today's prices. Beyond 2023 it's anyone's guess if the dividend will stay at this elevated level or not. With demand for extrusions already slowing in 2022 and aluminum prices significantly down from their peak in mid-2022, I don't think this level of dividend will be sustainable over the long-term. I could be wrong here, but I wouldn't rely on this dividend to cover my living needs as it could easily get cut in half at some point over the next few years if demand slows and commodity prices drop.

{kind=link}

The company does have hedges for over 75% of their near term (Q1 2023) production and about 30% of their 2023-2024 production which does provide some (though limited) visibility into future earnings. I am personally quite bullish on aluminum over the medium to long-term, mainly because it's heavily needed for electric vehicles and renewable energy projects. With high inflation, the commodity business should do fairly well so the stock can act as a nice hedge against inflation, if it persists. With that said, no company is a buy without consideration of price so let's have a look at valuation.

Valuation

Given the exposure to commodity prices, the business is inherently cyclical. This is also evident from their earnings which have been pretty volatile over time. The business is relatively simple, but it's not easy to forecast a profitability that is entirely dependent on commodity prices. Hydro does a good job of hedging but they will still likely be affected by a short-term slowdown in demand which we're starting to see in their 2022 numbers. Because of this and because the stock has rallied by 50% from the October low, I remain quite cautious to buy at these levels.

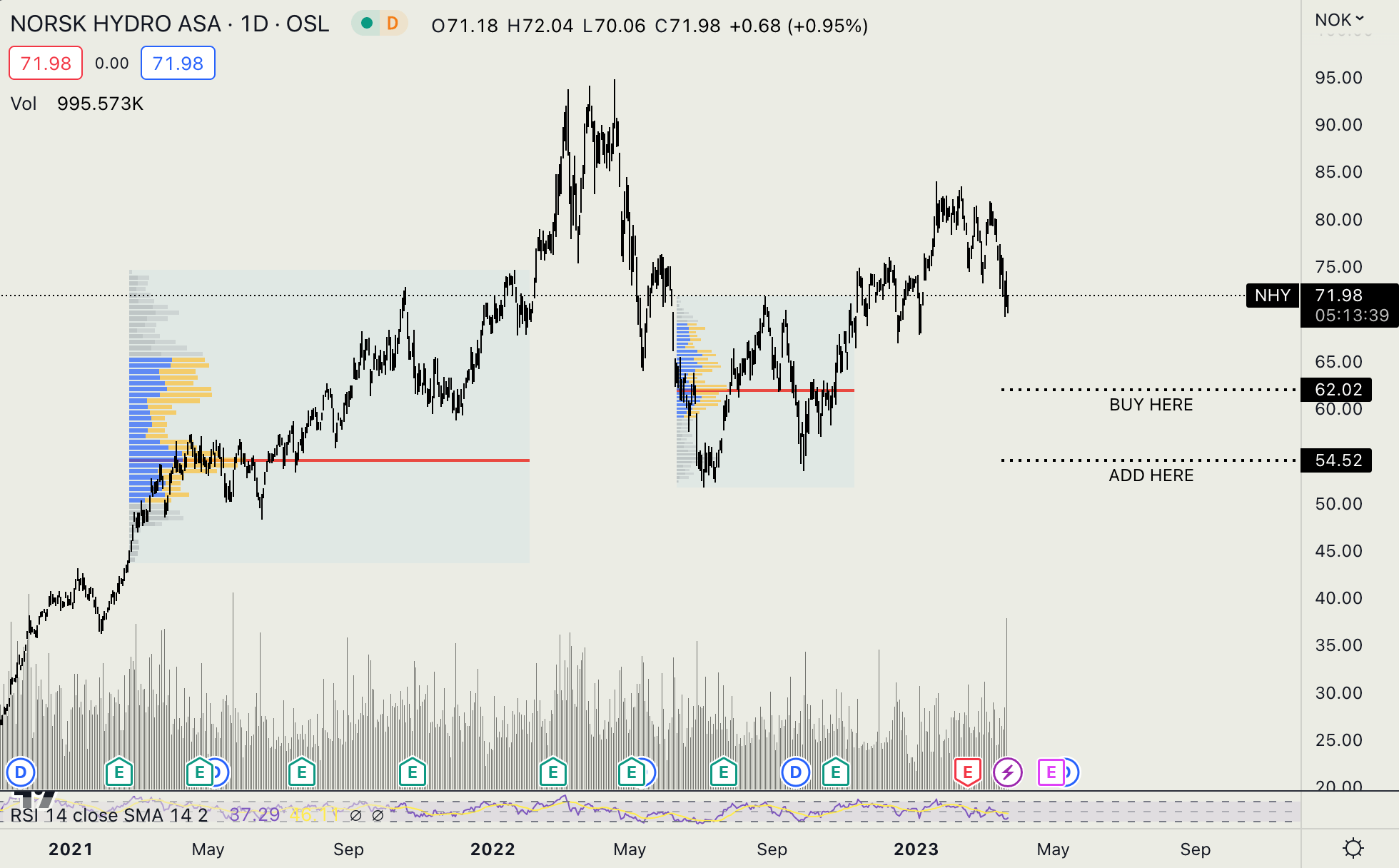

The 8% dividend yield is intriguing, but with a potential recession and given the cyclicality of the business, I expect the stock to come back and therefore rate Norsk Hydro as a " HOLD " here at NOK 71 per share. This outlook is confirmed by technical analysis which suggests a pullback to at least NOK 62 per share. Nonetheless I think the future for Aluminum is bright and Norsk Hydro is a quality business and if the price drops to NOK55-62 per share I will flip to a BUY rating. I think the probability of the price getting there at some point in 2023 is quite high, given the cyclicality of the business.

Author's analysis on Fast graphs

{kind=link}

For further details see:

Norsk Hydro: Future Looks Bright But I Am Not Buying At This Price