NOA:CC - North American Construction - MacKellar Acquisition Makes This Too Cheap To Ignore

2024-01-17 15:38:34 ET

Summary

- North American Construction Group is a global provider of earthmoving services to the mining and oil and gas sectors.

- The recent acquisition of the MacKellar Group in Australia diversifies NOA's commodity exposure and is expected to boost earnings by ~50% in 2024.

- NOA's shares are trading at a low valuation of 6.7x Fwd P/E, making them a compelling buy with significant upside potential.

Boring is beautiful. While many investors love to chase the latest fad in artificial intelligence or cryptocurrency, I find companies generating strong returns on capital and trading at fair valuations to be one of the best ways to build long-term wealth. I believe North American Construction Group Ltd. ( NOA ) is an under-the-radar gem providing boring, but essential earthmoving services to the mining and oil and gas industry.

The company recently completed an acquisition of the MacKellar Group in Australia that should help diversify NOA's commodity exposure as well as boost adj. EPS by ~50% in 2024. Trading at just 6.7x Fwd P/E that is well-supported by contracted backlog, I believe NOA's shares are simply too cheap to ignore. I rate its shares a buy .

Company Overview

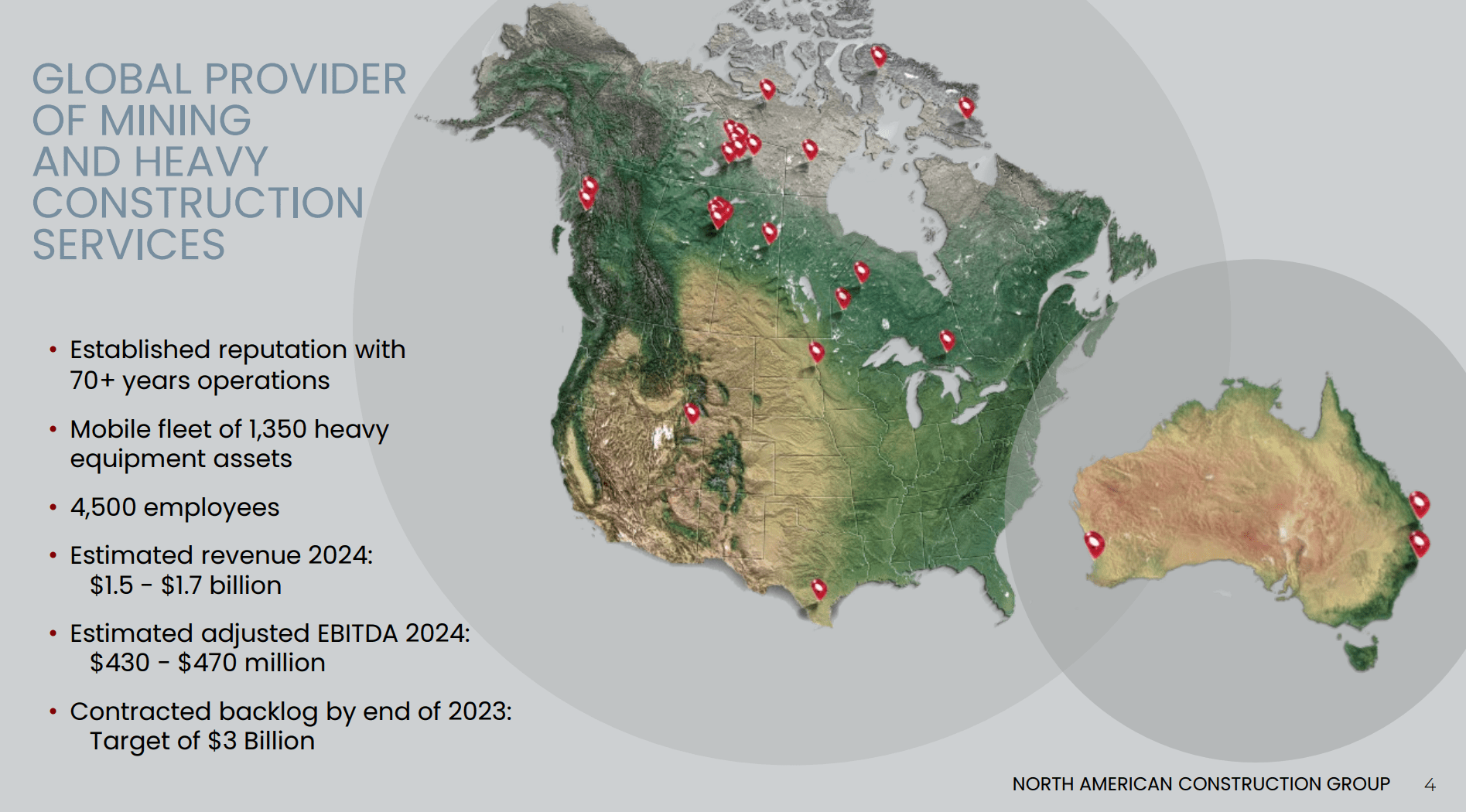

North American Construction Group Ltd. ((NOA)) is a global provider of mining and heavy construction services. The company is based in Canada, but has operations in Canada, the U.S., and Australia, with the recent acquisition of the MacKellar Group (Figure 1).

Figure 1 - NOA overview (NOA investor presentation)

{kind=link}

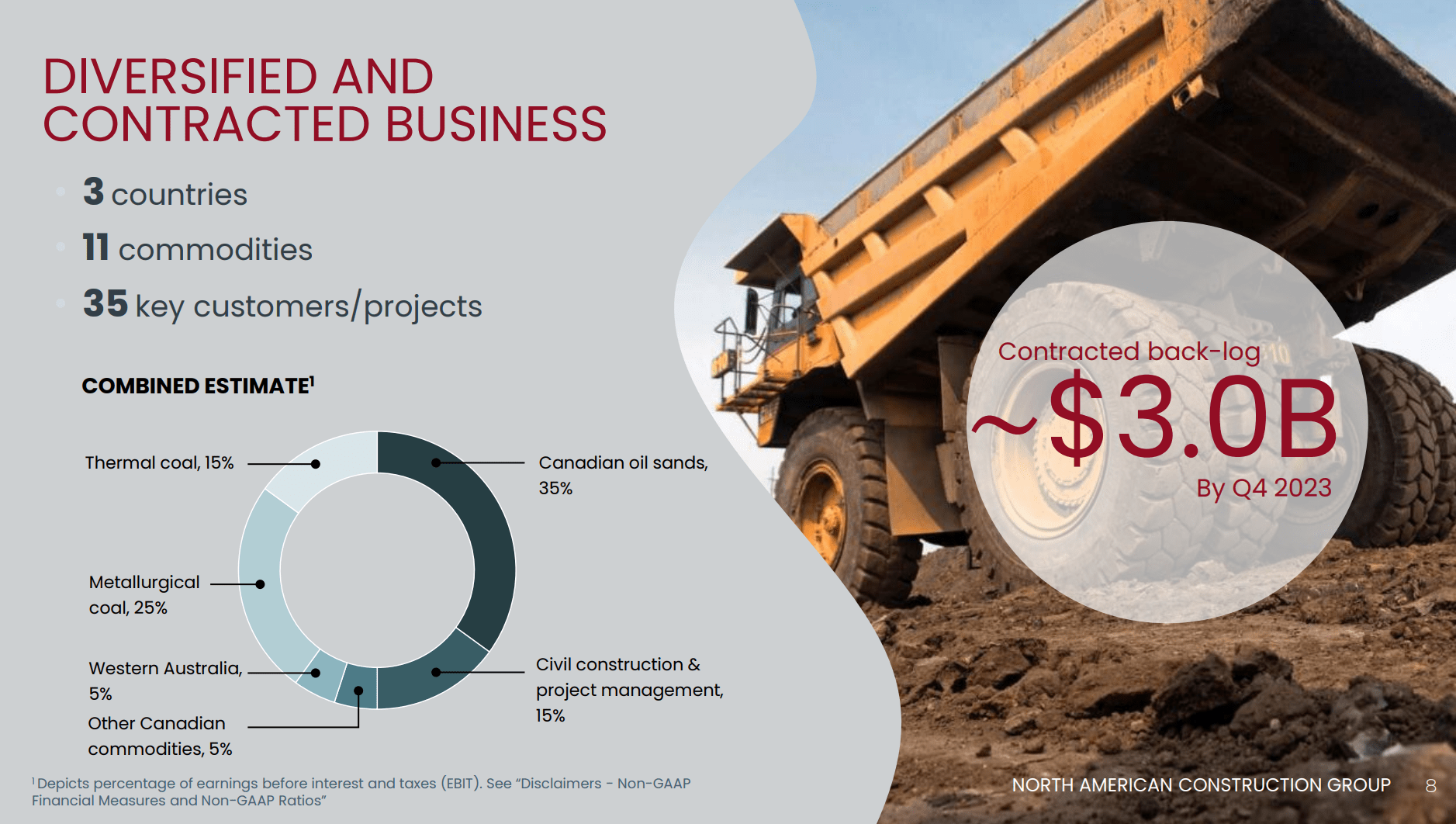

NOA has a mobile fleet of 1,350 heavy equipment assets and 4,500 employees providing heavy civil and bulk earthmoving services, as well as project and site management services. NOA is focused on providing earthmoving services to large mining projects such as coal and oil sands mines. Approximately 35% of the company's C$3.0 billion contracted backlog is involved in the Canadian oil sands, 25% is involved in met coal mines, and 15% is involved in thermal coal mines (Figure 2).

Figure 2 - NOA commodity exposures (NOA investor presentation)

{kind=link}

Oil Sands Is The Backbone of NOA

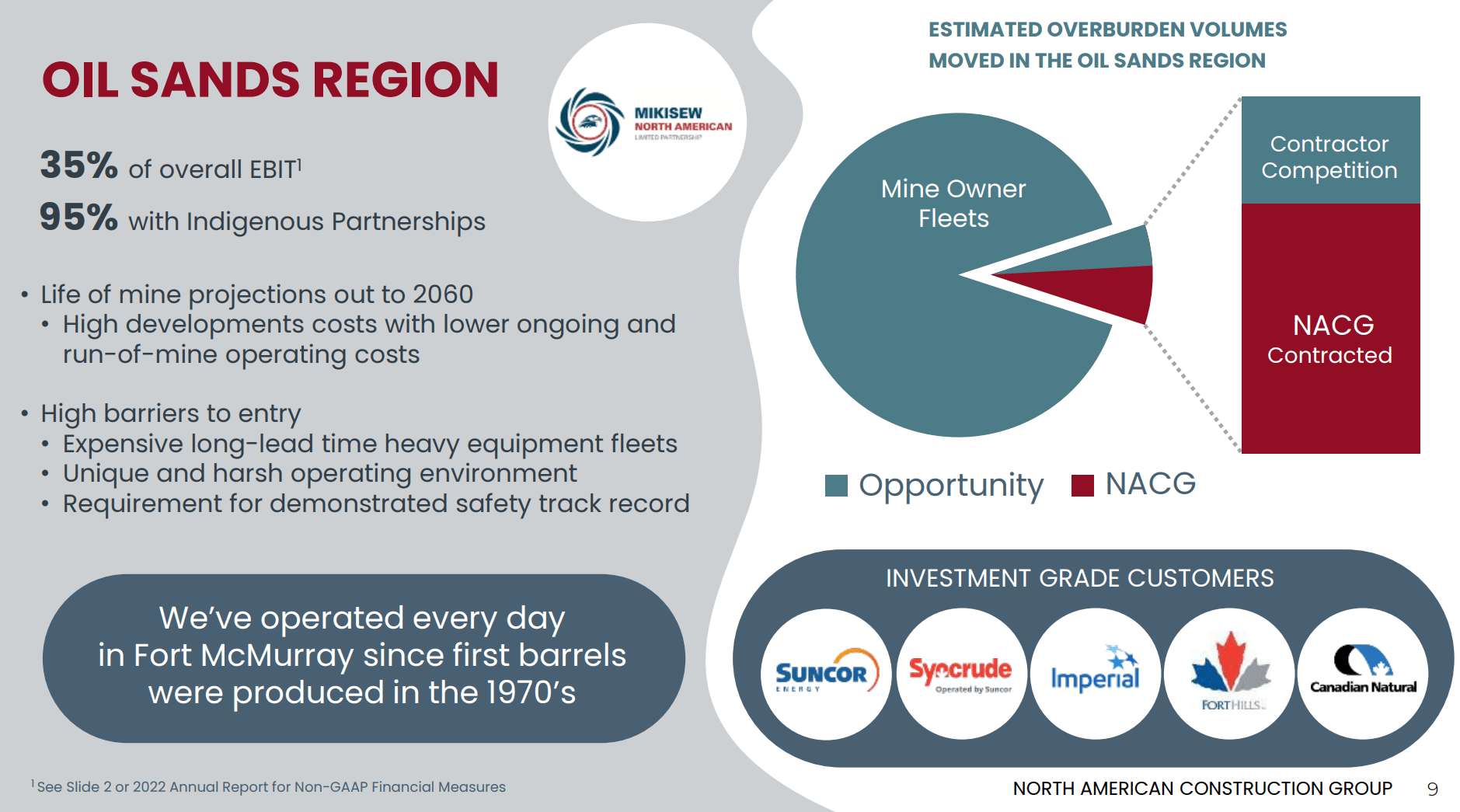

NOA grew out of providing earthmoving services to the Canadian oil sands, with NOA having been operating in Fort McMurray since the 1970s (Figure 3). There are high barriers to entry for providing earthmoving services, as the heavy equipment used is expensive, and the operating environment is harsh and unique. Oil sands provide 35% of NOA's overall pro forma EBIT.

Figure 3 - NOA oil sands overview (NOA investor presentation)

{kind=link}

The growth opportunity for NOA in the oil sands business is that as the mines mature, mine owners like Suncor and Imperial may look to outsource their earthmoving volumes and NOA can gain market share. Currently, NOA provides the majority of non-mine owner fleets in the oil sands region and the company should win its fair share of business if it ever comes up for bid.

MacKellar Acquisition Diversifies NOA Into Australia

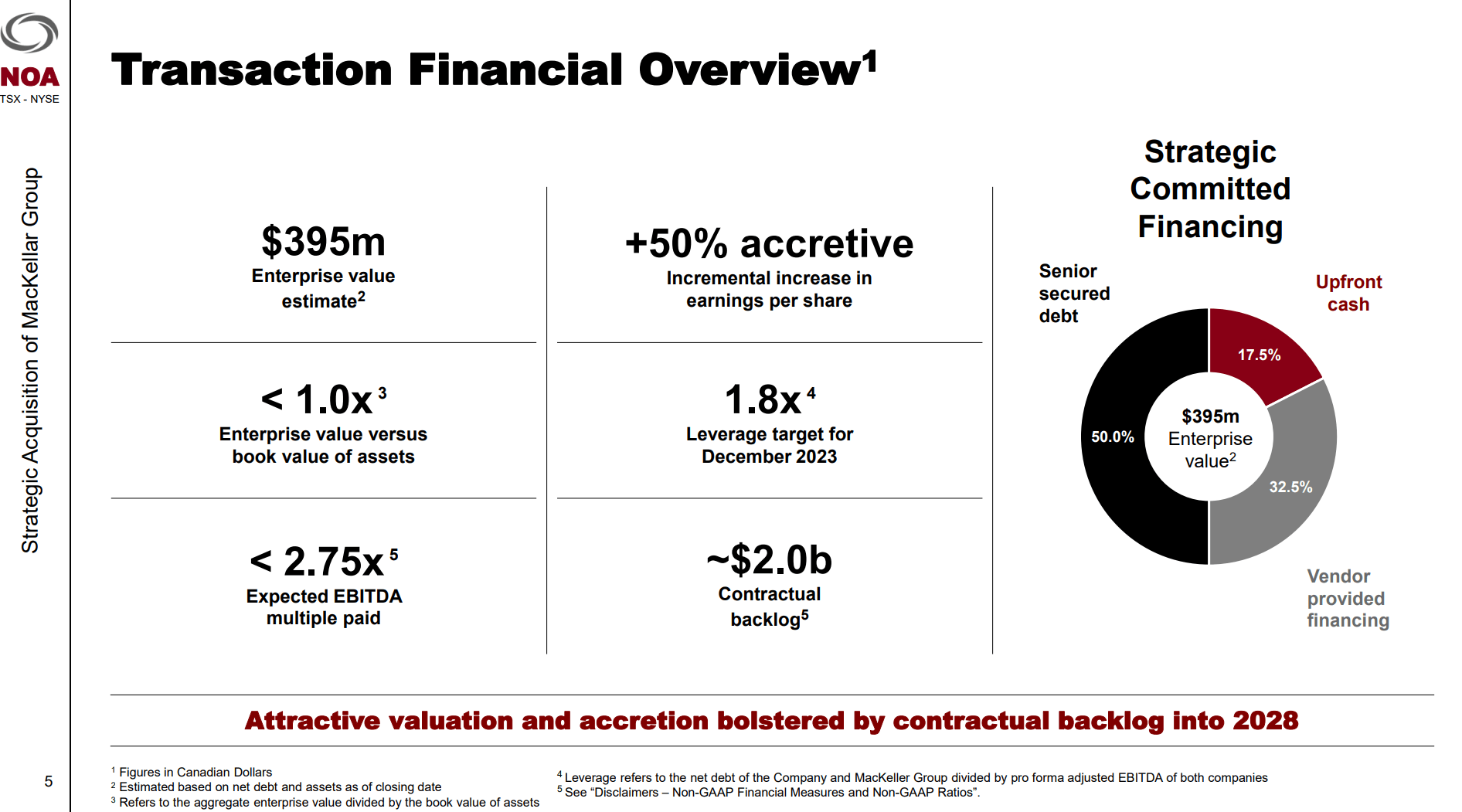

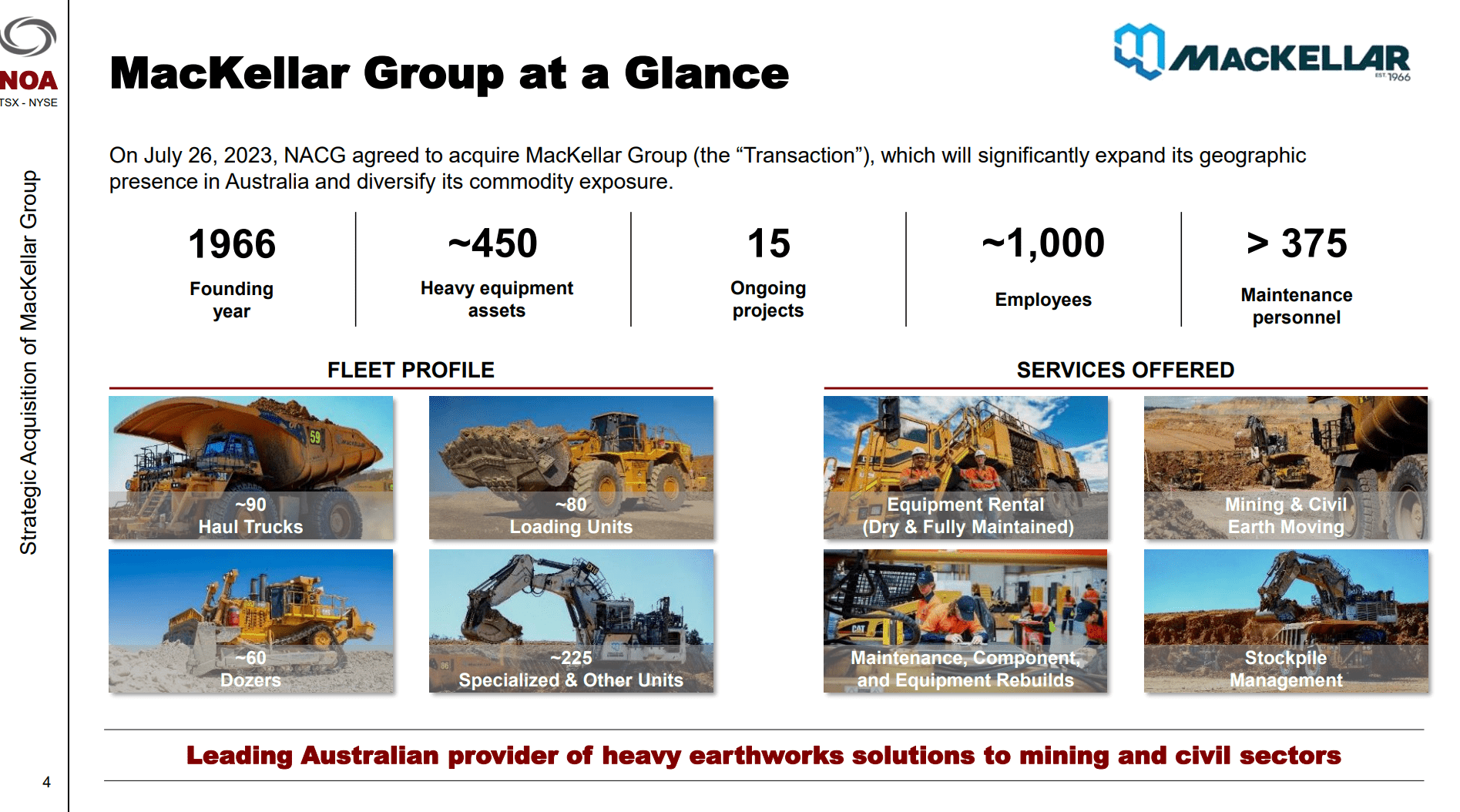

In July 2023 , NOA diversified into providing heavy equipment services to the Australian mining industry by acquiring the MacKellar Group in a ~C$400 million transaction (Figure 4).

Figure 4 - NOA acquired MacKellar Group in 2023 (NOA investor presentation)

{kind=link}

The MacKellar Group has a C$2 billion backlog providing similar heavy earthmoving services to 15 ongoing projects in Australia, ranging from coal to iron ore mines (Figure 5). This transaction not only diversifies NOA's geographical exposure, it also diversifies NOA's commodity exposure into iron ore and coal.

Figure 5 - MacKellar Group overview (NOA investor presentation)

{kind=link}

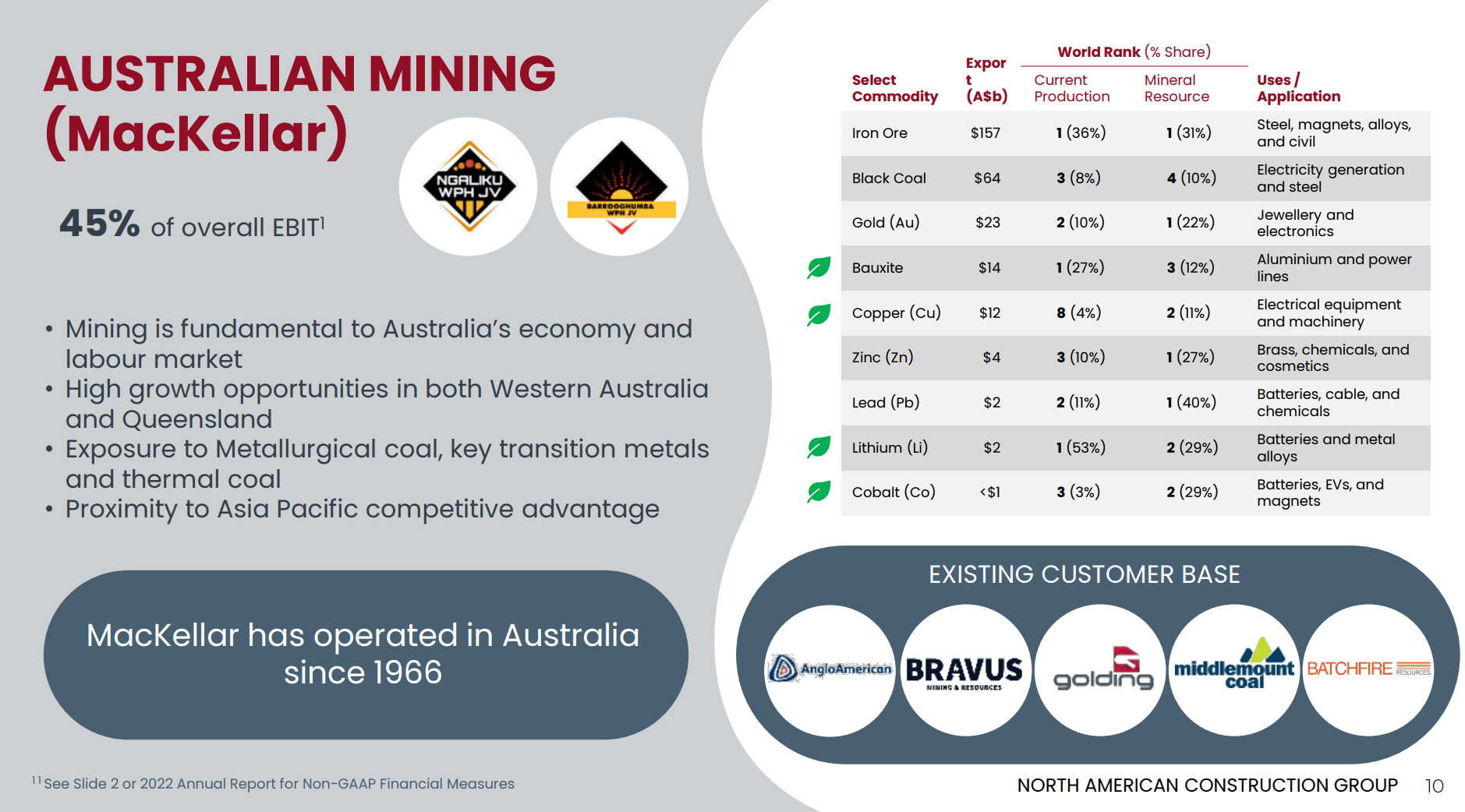

Based upon the company's estimates, the MacKellar Group will contribute 45% to the company's pro-forma EBIT with exposure to high growth opportunities in Western Australia and Queensland (Figure 6).

Figure 6 - MacKellar Group is expected to contribute 45% to pro-forma EBIT (NOA investor presentation)

{kind=link}

Financial Performance Has Been Stellar

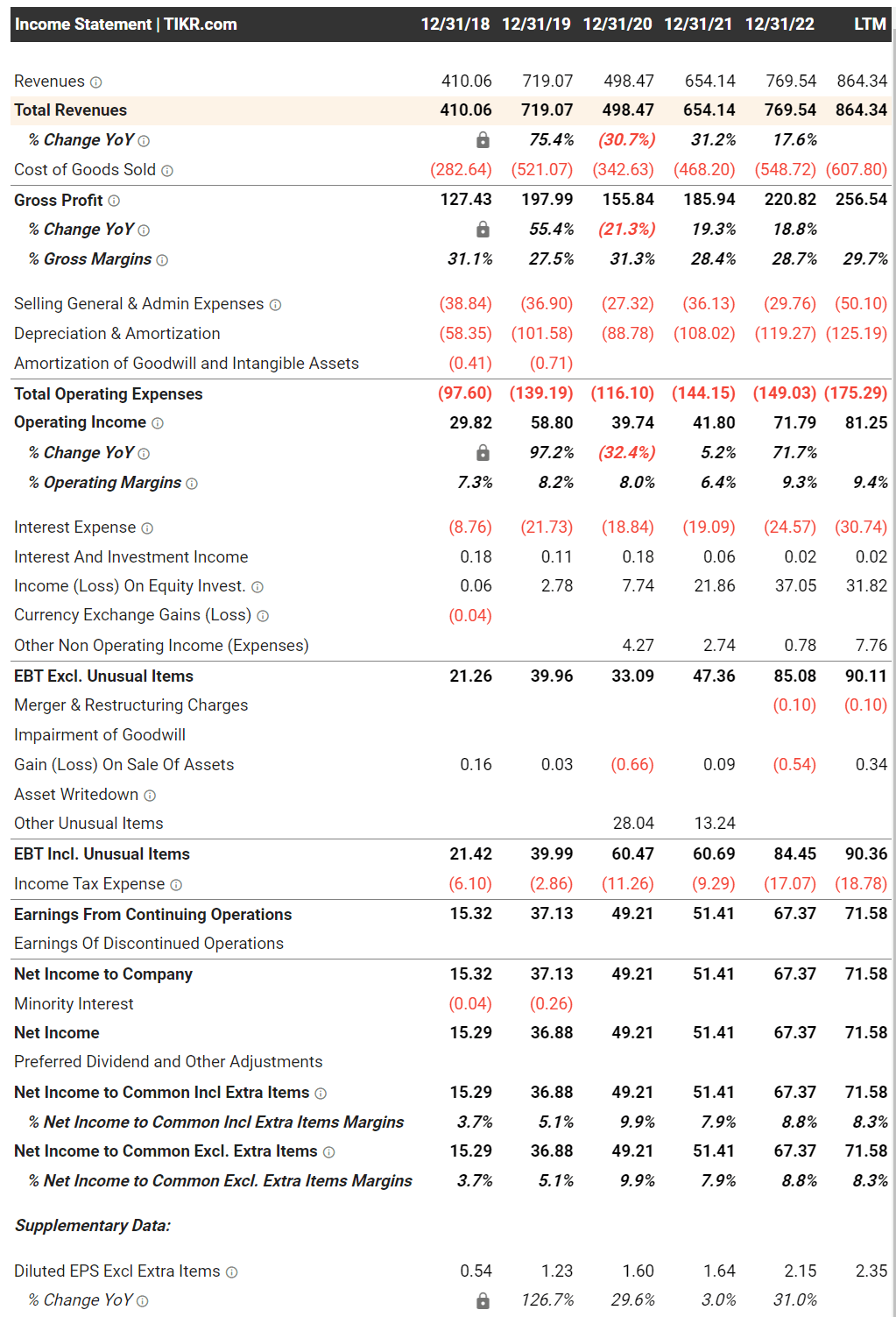

Financially, NOA's performance has been stellar, with the company delivering revenues of $864 million in the trailing 12 months (including 2 months of contribution from MacKellar), and operating income of $81 million (Figure 7).

Figure 7 - NOA financial summary (tikr.com)

{kind=link}

Impressively, NOA has been consistently profitable, even during the COVID pandemic in 2020, when the company saw a 31% decline in revenues and a 32% decline in operating income, but operating margins stayed healthy at 8.0%. Net income in the COVID years (2020 and 2021) was boosted by government wage subsidies, helping NOA report strong net income growth despite the drop in headline revenues.

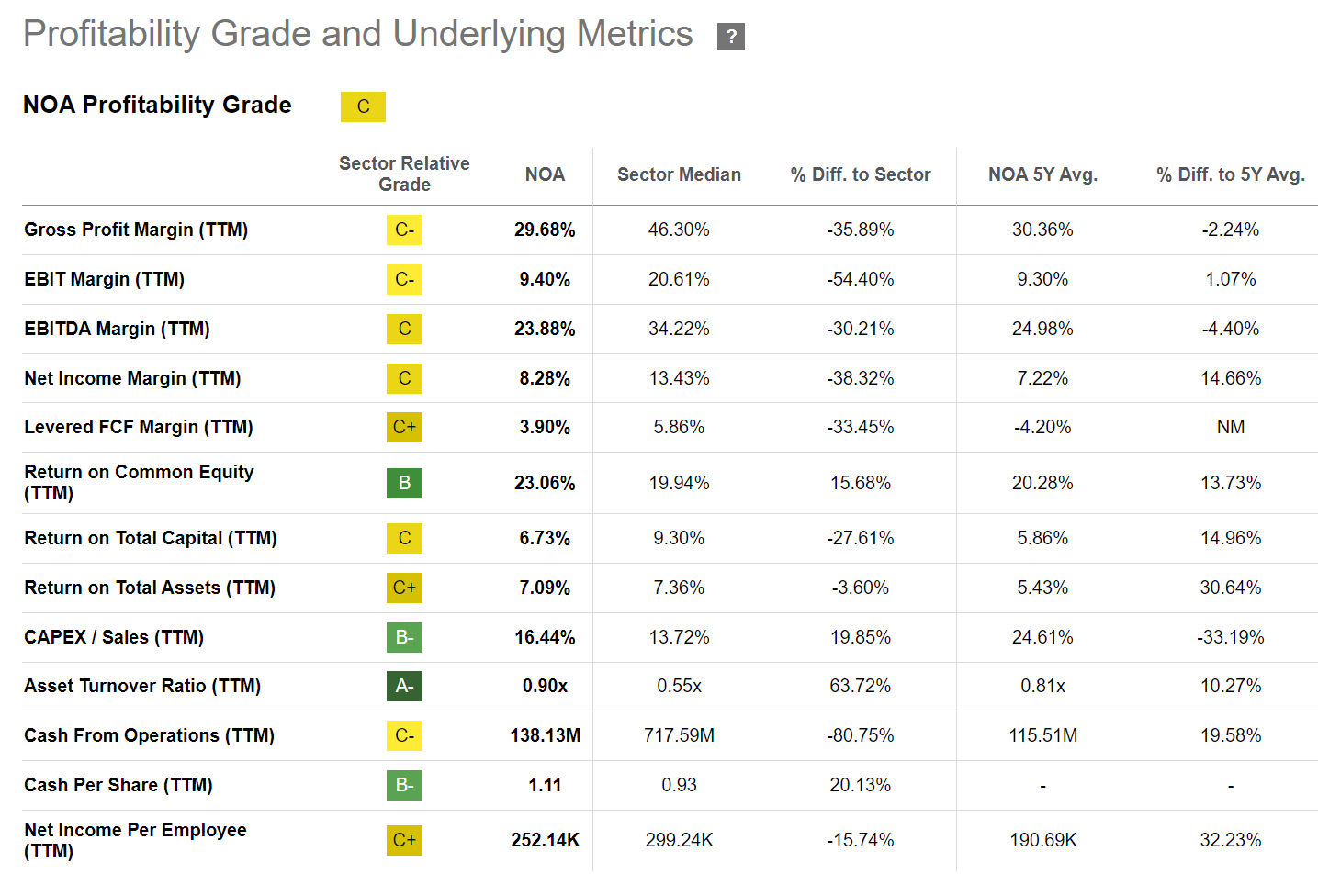

Looking at NOA's returns on capital and equity, although profit margins in NOA's businesses are slim (net margins ~6-8%), NOA is able to leverage that into an impressive ~20% return on equity (Figure 8).

Figure 8 - NOA profitability and returns on capital (Seeking Alpha)

{kind=link}

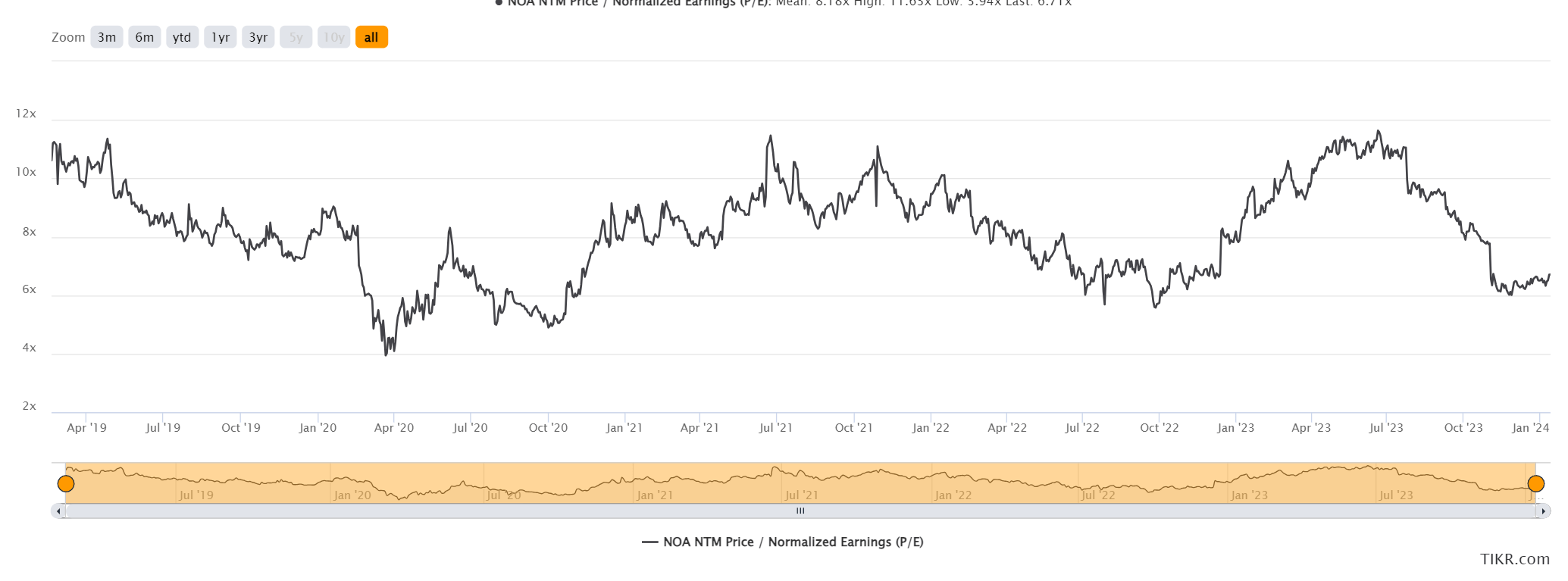

Valuation Depressed Due To Oil Sands Concentration

However, when it comes to the stock, NOA's historical valuation has been depressed, consistently trading at sub-10x Fwd P/E. I believe this discounted valuation was due to fears surrounding the company's concentrated exposure to the Canadian oil sands (Figure 9).

Figure 9 - NOA has consistently traded sub-10x Fwd P/E (tikr.com)

{kind=link}

While NOA has visibility into contracted revenues, future contracts are tied to sentiment surrounding the oil sands. Historically, when oil prices were depressed, development work on the oil sands slowed and NOA's revenues were negatively impacted. Also, as the world moves towards low-carbon resources, there is a fear that oil sands will become a stranded asset and NOA's heavy earthmoving equipment will likewise be stranded.

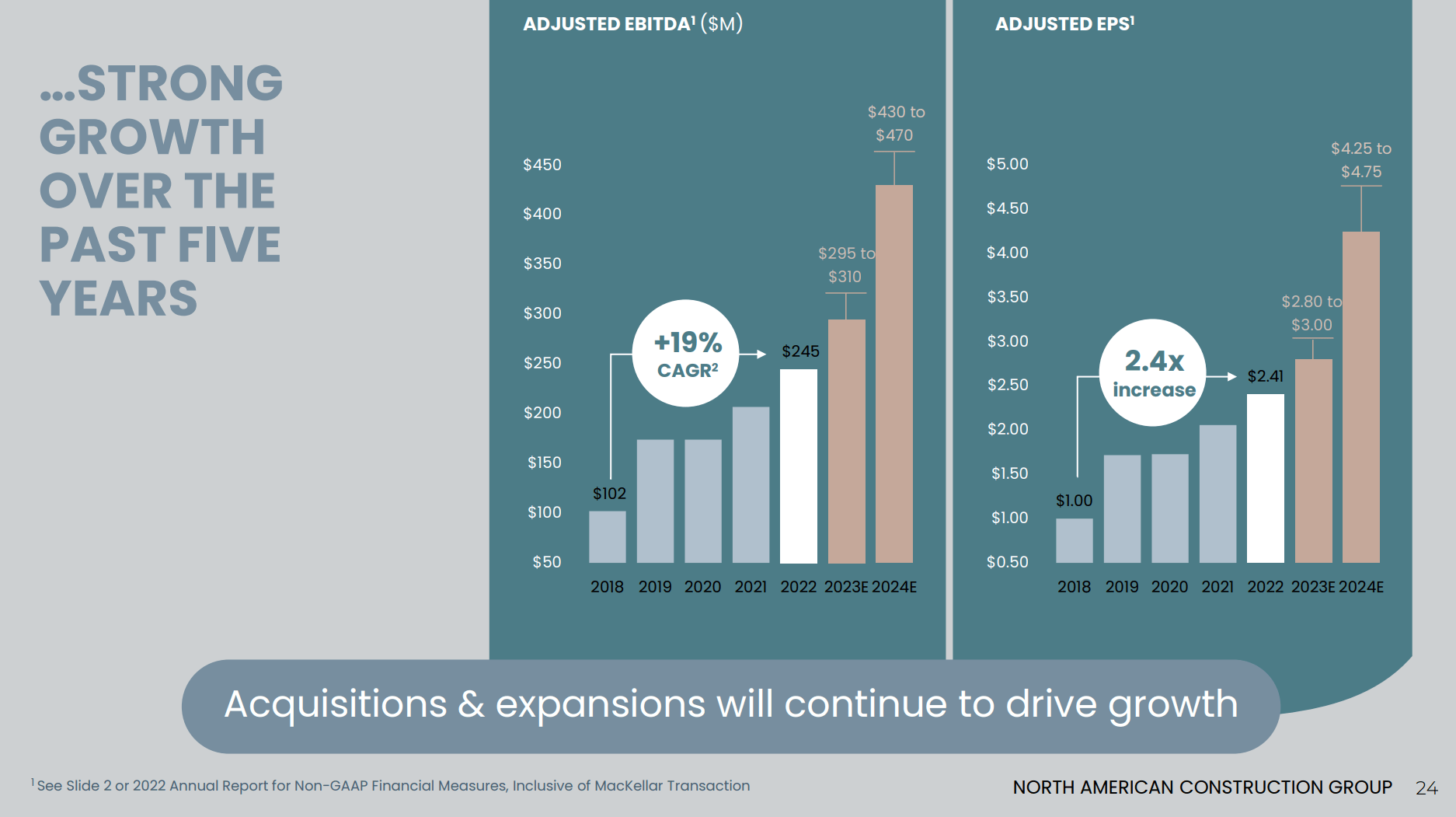

However, I believe the recent acquisition of the MacKellar Group provides an important catalyst for NOA. First, it reduces NOA's oil sands concentration to just 35% of pro forma EBIT and backlog. More importantly, adding MacKellar's contracted backlog to NOA provides visibility to C$4.25 - C$4.75 in adjusted EPS for 2024, according to the company's guidance (Figure 10).

Figure 10 - Contracted backlog backstops ~50% growth in EPS (NOA investor presentation)

{kind=link}

Management's guidance for 2024 EPS looks like a good estimate as these figures are based on contractual revenues that are expected to be received from the company's backlog that extends into 2028. Furthermore, NOA was able to acquire MacKellar at very cheap valuations at sub-3x EV/EBITDA. That is why the earnings accretion looks so large between 2023 and 2024.

Once analysts rolled their estimates forward to 2024 in the last few months, NOA's valuation discount widened even further to just 6.5x Fwd P/E currently.

I believe NOA's forward valuation should expand to 10x Fwd P/E and beyond, as the company has addressed its over-concentration in the Canadian oil sands by adding revenue streams tied to other mining projects. Furthermore, by diversifying into other commodities like coal and iron ore, NOA is no longer purely reliant on sentiment toward the price of a single commodity.

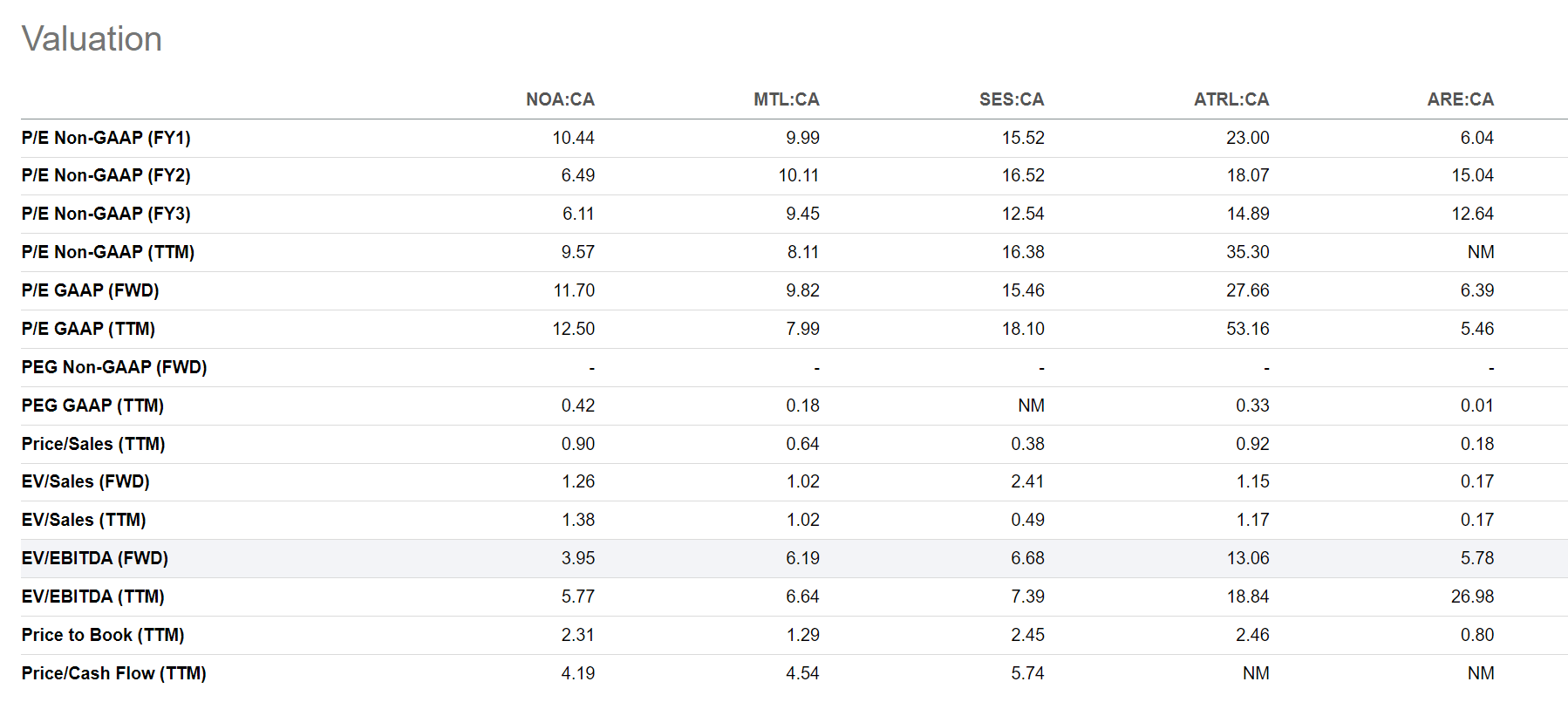

Furthermore, if we look at peer comparables, Canadian energy service peers that provide ancillary services (i.e., not drilling or pressure pumping) like Mullen Group Ltd. ( MTL:CA ) and Secure Energy Services Inc. ( SES:CA ) trade at 10.1x and 16.5x 2024 P/E respectively compared to 6.5x for NOA. Once investors see the earnings accretion from the MacKellar transaction, I believe this valuation gap should close over the coming year (Figure 11).

{kind=link}

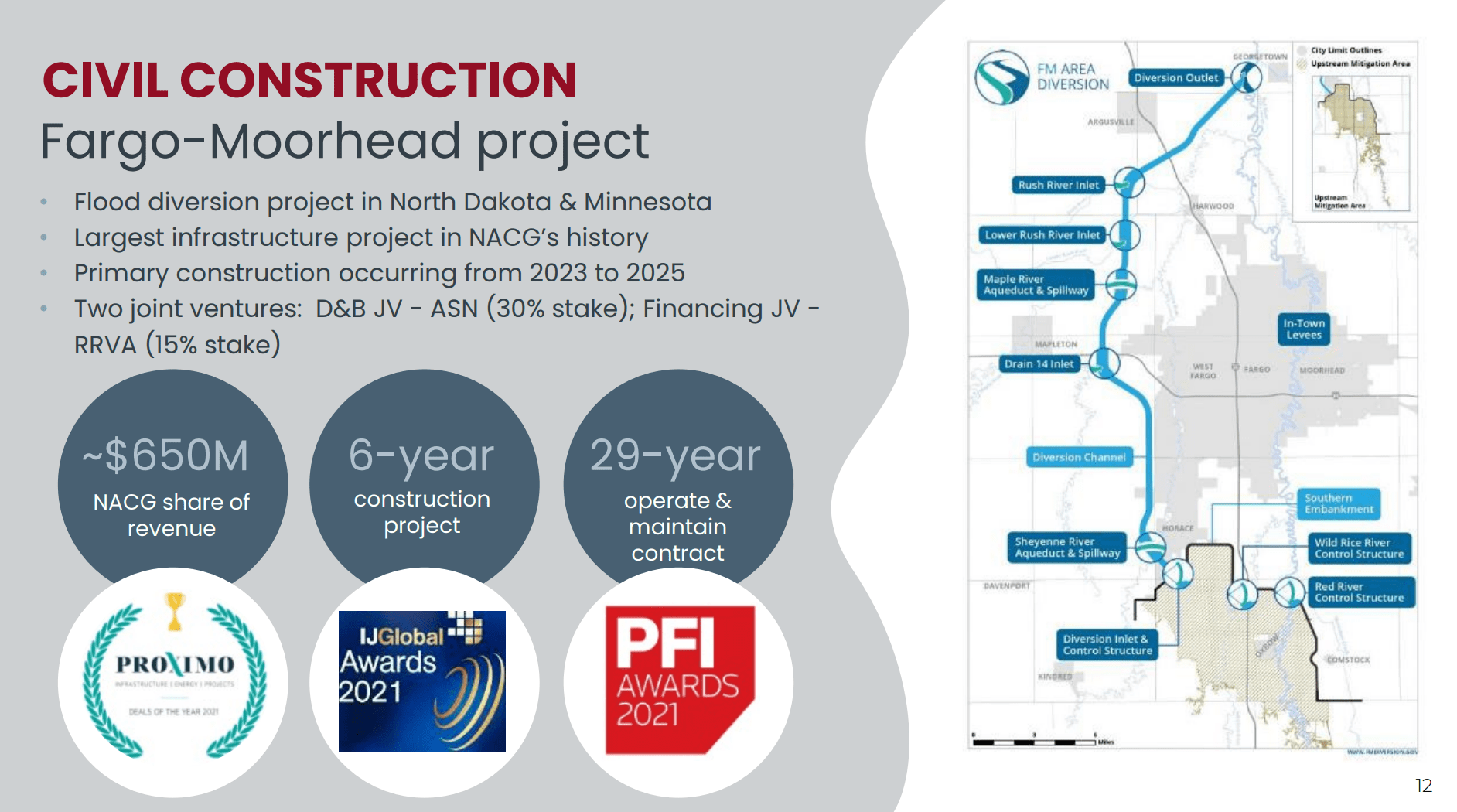

In fact, over the long-term, I believe there is an upside to NOA's valuation, away from energy services multiples to construction and engineering services multiples, since those are essentially the services provided by NOA. NOA's C$3 billion backlog currently has 15% exposure to large-scale civil and engineering projects like the $650 million contract for the Fargo-Moorhead flood diversion project in North Dakota & Minnesota (Figure 12).

Figure 12 - NOA has exposure to large-scale civil engineering projects (NOA investor presentation)

{kind=link}

SNC-Lavalin Group Inc. ( ATRL:CA ) and Aecon Group Inc. ( ARE:CA ), two Canadian construction and engineering services companies, trade at 18.1x and 15.0x 2024 P/E respectively.

if NOA simply trades up to 10x 2024 P/E, the low end of its peer group, I expect its shares to be worth C$45 or ~US$34 / share, approximately 50% upside to current valuations.

Risks To NOA

However, NOA is not without risks as the MacKellar Group is heavily exposed to coal mining, a 'dirty' hydrocarbon that may eventually be phased out like the oil sands.

But before investors throw out the baby with the bathwater, they need to keep in mind that these large-scale mines routinely last decades. Even if no new oil sands or coal mines are developed, existing mines will still need to be serviced for years to come.

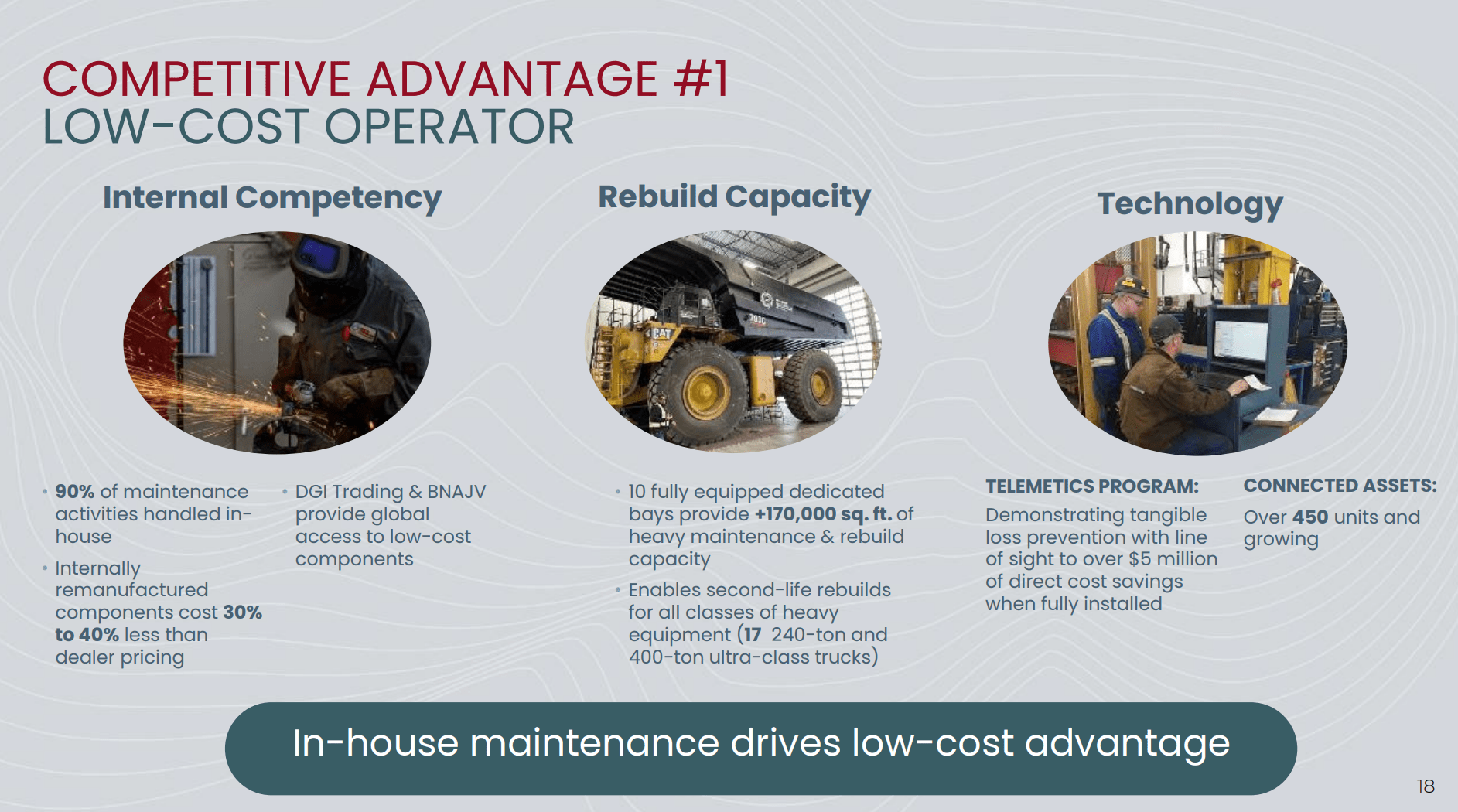

Furthermore, NOA is a low-cost provider of earthmoving services, with the company performing its own maintenance and rebuilds (Figure 13). As growth in oil sands and coal mining slows and reverses, operators may look to recycle capital away to higher growth areas like copper mining. This leaves NOA as one of the preferred bidders for maintenance contracts that could last decades.

Figure 13 - NOA is a low-cost provider of earthmoving services (NOA investor presentation)

{kind=link}

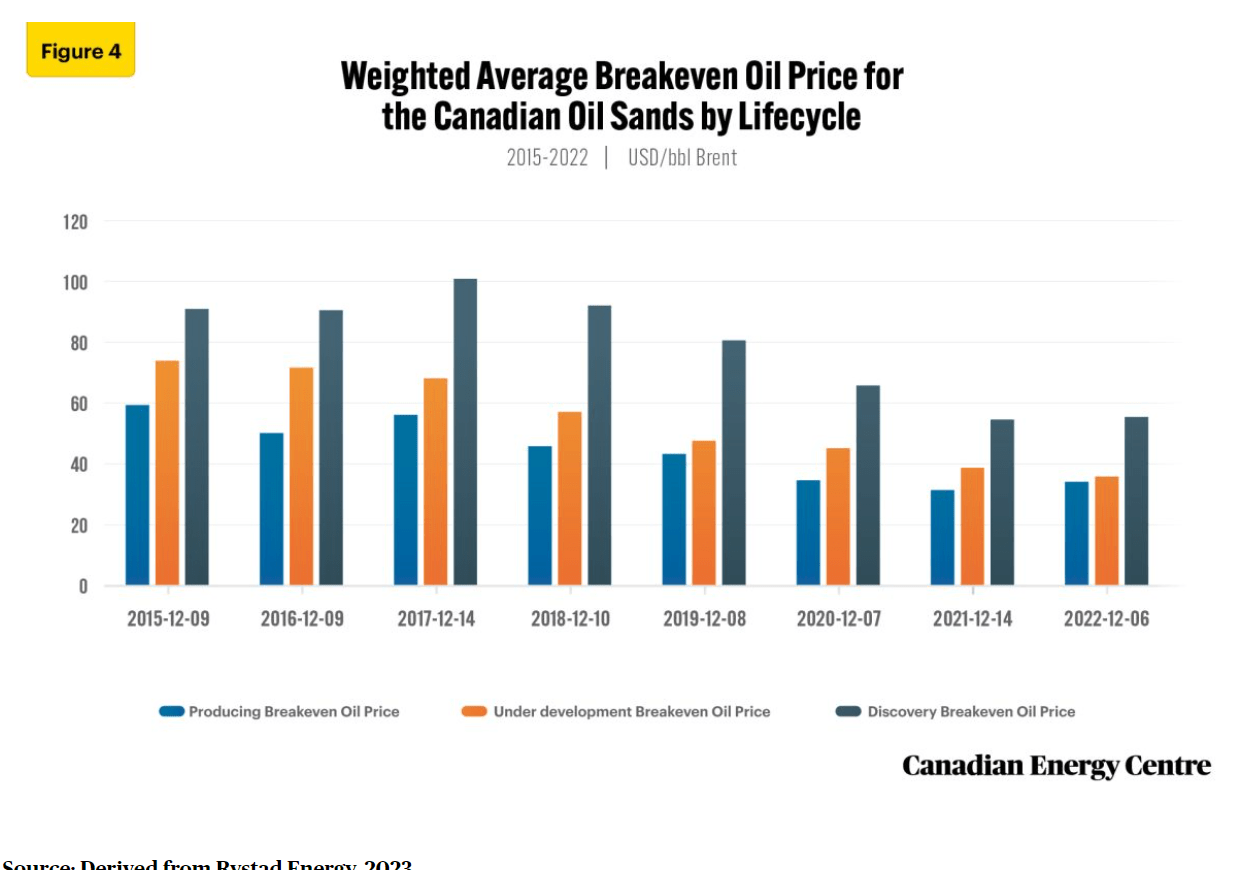

Other risks with NOA mainly revolve around commodity prices. For example, if the price of oil stays depressed for an extended period, that may negatively impact the development plans of the Canadian oil sands and/or lead to the shutdown of these relatively high cost barrels altogether (Figure 14).

Figure 13 - Breakeven cost of Canadian oil sands (canadianenergycentre.ca)

{kind=link}

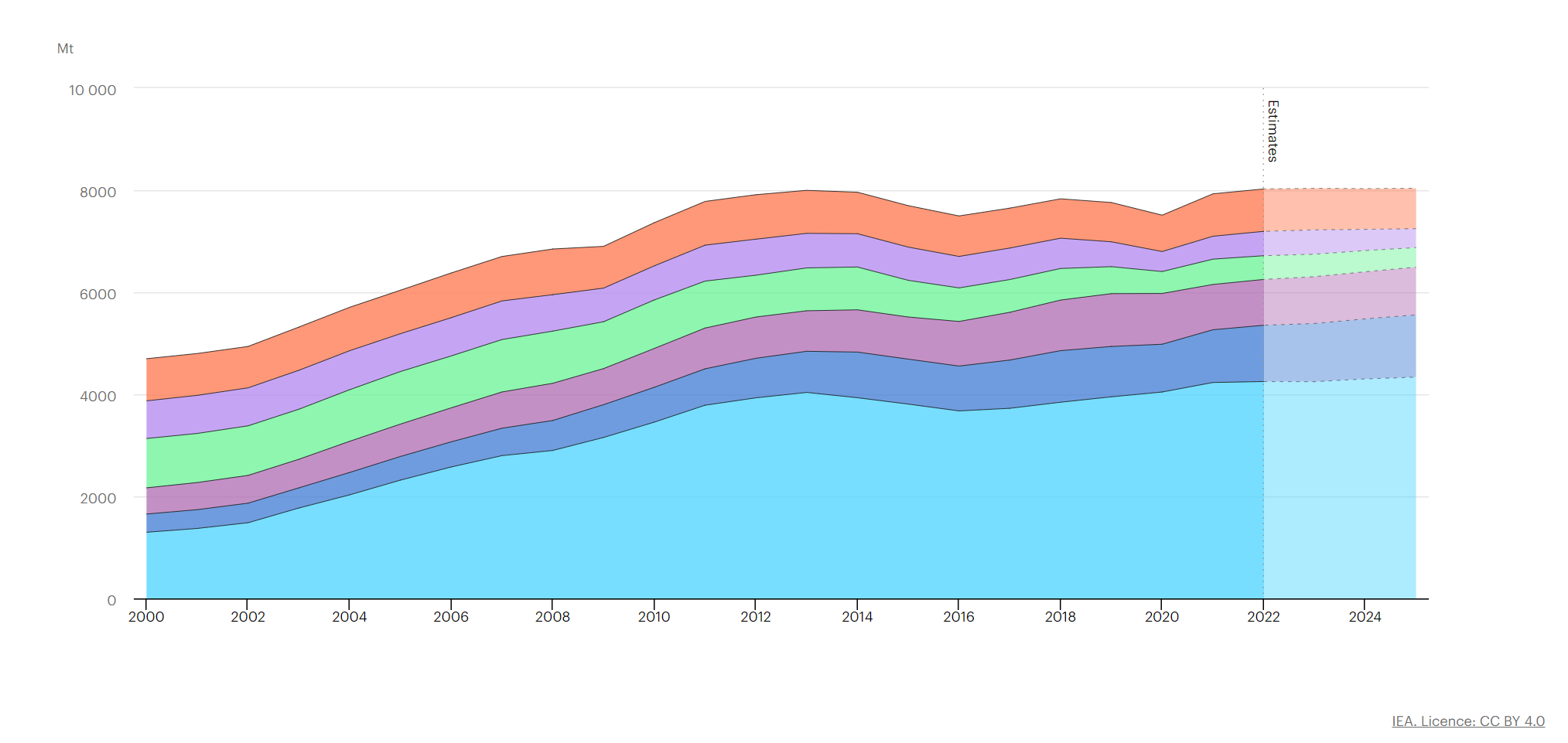

Similarly, if governments phase out the use of coal as an energy source, then the Western Australian coal mines serviced by NOA may become stranded assets. I personally do not believe the phasing out of these energy sources is likely, at least in the near term. Estimates from the IEA suggest flat coal consumption out to 2025, with growth in China and India offsetting declines in the rest of the world (Figure 14).

Figure 14 - Coal consumption is expected to remain steady (IEA)

{kind=link}

As a reminder, coal, especially from Australia, is also used in steelmaking and China is the number 1 importer of Australian met coal . Unless scientists perfect processes to make steel without coal ( possible , but still nascent), Australian met-coal will still be mined for years to come and shipped to China.

Investors should monitor developments in the oil sands and coal mining sectors to assess how much operational runway NOA has.

Conclusion

North American Construction Group is a global provider of earthmoving services to the mining and oil and gas sectors. Concentration in oil sands has depressed the company's valuation, however, a recent deal to acquire a complementary business in Australia could help diversify the company's commodity exposure as well as boost earnings in the coming years.

Trading at just 6.7x Fwd P/E, I believe NOA's shares are simply too cheap to ignore. I rate NOA a buy .

For further details see:

North American Construction - MacKellar Acquisition Makes This Too Cheap To Ignore