TRMK - Northwest Bancshares: A Step Back Might Not Be So Bad (Rating Downgrade)

2024-01-17 06:28:33 ET

Summary

- Northwest Bancshares has seen strong growth in revenue and profits, with deposits and loans increasing.

- Net interest income and non-interest income have also improved, leading to higher net profits.

- NWBI stock is now closer to being fairly valued and may not have much additional upside potential.

In an ideal world, when we make an investment in a company, we would be able to hold that investment forever and attract strong returns the entire time. Unfortunately, in many cases, once shares of a business pop up, especially significantly so, they no longer make sense to hold on to. One such example that I could point to involves Northwest Bancshares ( NWBI ), a fairly small regional bank with a market capitalization of about $1.58 billion. Despite the troubles in the banking sector that emerged early last year, management has done well to grow revenue and profits for the institution. Deposits continue to expand and other measures of success for the institution are looking up as well.

Unfortunately, however, many investments hit the upper limit of what they are worth at some point or another. And Northwest Bancshares is no exception in my opinion. Back when I wrote favorably about the company on October 11th of 2023, I stated that the company deserved 'a bit of optimism'. The overall financial picture of the company looked attractive and shares were cheap enough at the time to warrant some appreciation. That led me to rate the enterprise a 'buy'. Since then, the market has had some stellar returns, with the S&P 500 appreciating by 9.6%. Over the same window of time, however, shares of Northwest Bancshares are up almost double that with a gain of 18.1%. That increase, to me, makes the company much closer to being fairly valued. So because of that, I have decided to downgrade it to a 'hold'.

The picture keeps improving fundamentally

{kind=link}

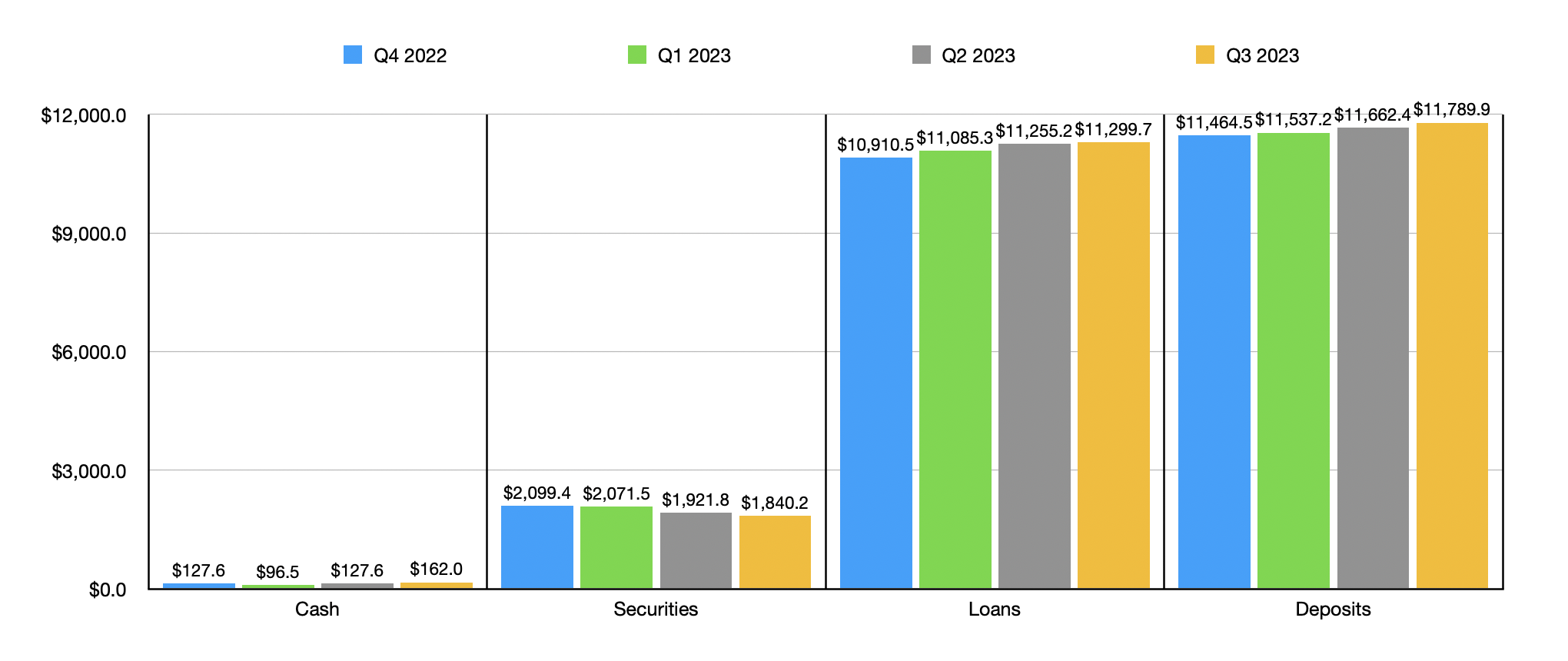

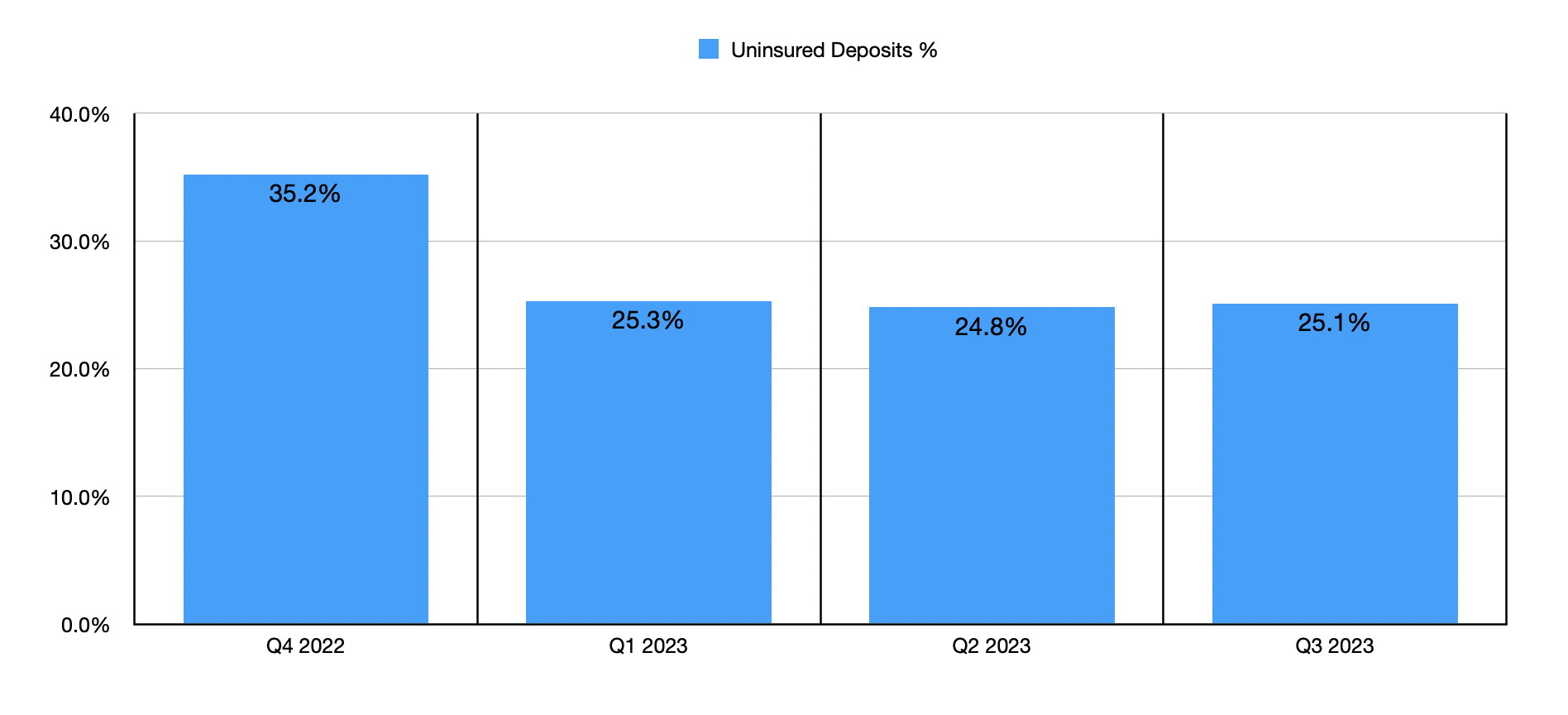

When I last wrote about Northwest Bancshares late last year, we had fundamental data covering the first two quarters of the 2023 fiscal year. Today, that data now extends through the third quarter . And by all accounts, things are going quite well. As an example, take the value of deposits on the institution's books. After hitting $11.66 billion in the second quarter, up from $11.46 billion at the end of 2022, deposits grew further to $11.79 billion. Uninsured deposit exposure did increase slightly from 24.8% of all deposits to 25.1%. But this is still comfortably below the 30% maximum that I tend to prefer and it is below the 35.2% the company reported for the end of 2022.

{kind=link}

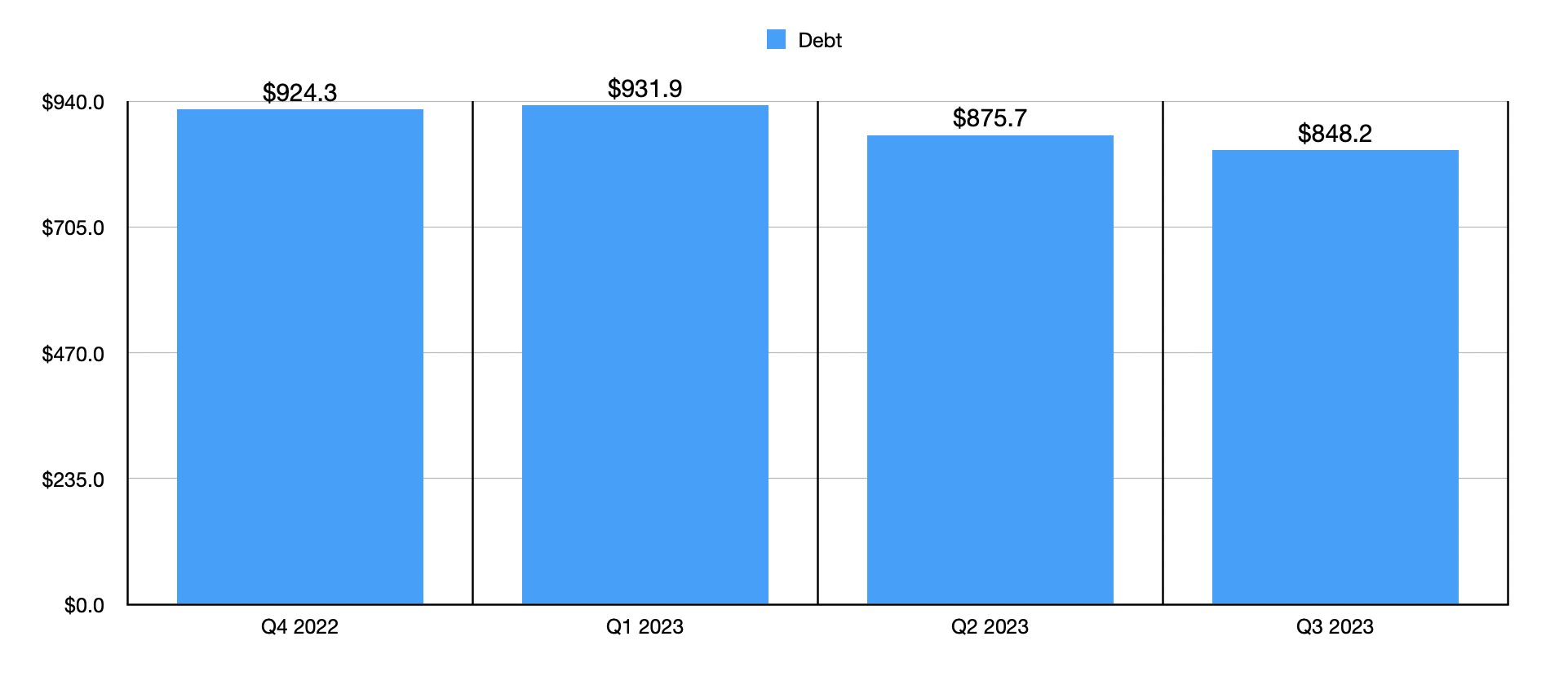

This wasn't the only area in which the company demonstrated growth. The value of loans at the end of the second quarter came in at $11.26 billion. As of the end of the most recent quarter, loans had grown to just under $11.30 billion. We have seen a drop in the value of securities from $1.92 billion to $1.84 billion but this corresponded with a rise in the value of cash from $127.6 million to only $162 million. Debt has also dropped, falling from $924.3 million to $848.2 million. What this all shows is that, even though the value of securities declined, the company got healthier in almost every other respect possible.

{kind=link}

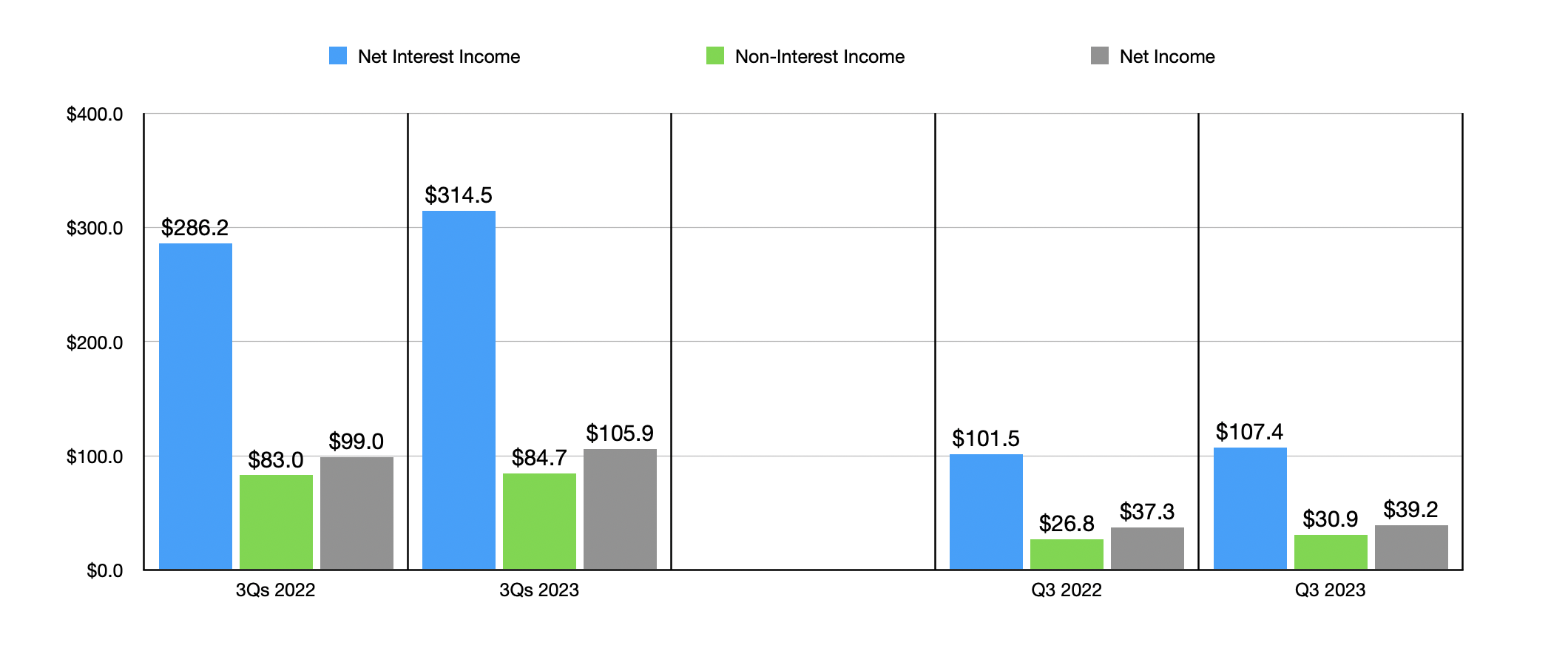

There have also been improvements elsewhere. As an example, we need only to look at the firm's income statement. In the third quarter of 2023, Northwest Bancshares reported net interest income of $107.4 million. That's up from the $101.5 million reported for the third quarter of the 2022 fiscal year. The aforementioned balance sheet improvements more than accounted for this increase. However, it was offset to some extent by a slight contraction in the company's net interest margin from 3.42% to 3.23%. This decline was driven in large part by higher interest expense. For instance, the $129.5 million worth of junior subordinated debentures that the firm has on its books reported an increase in interest rate from 4% last year to 7.42% this year. Time deposits jumped from 0.54% to 3.32%, while borrowed funds, excluding junior subordinated debentures and subordinated debentures, reported an increase from 0.75% to 4.89%.

{kind=link}

At the same time, the net interest income increased, and so did non-interest income, rising from $26.8 million to $30.9 million. These two improvements, combined, helped to push net profits for the company up from $37.3 million last year to $39.2 million this year. As you can see in the chart above, the third quarter on its own was not a one-time thing. The institution was strong for all of the first nine months of last year relative to the year prior. Unfortunately, this strength did not stop the company's book value per share from declining slightly, going from $11.89 in the second quarter to $11.79 in the third. A similar decline can be seen when looking at tangible book value per share.

{kind=link}

{kind=link}

If we use analysts' estimates for the firm's upcoming fourth-quarter earnings release, we should anticipate net profits for 2023 of about $136.4 million. That would be up from the $133.7 million reported for 2022. This should translate to a price-to-earnings multiple of approximately 11.6. Meanwhile, the price-to-book multiple is about 1.05, while the price-to-tangible book multiple is 1.42. In the chart above, you can see how shares of the company are priced on both a price-to-book basis and a price-to-tangible book basis relative to five similar enterprises in the space. And in the chart below, you can see the same thing but for the price-to-earnings approach. In all three valuation cases, only two of the five companies ended up being cheaper than our prospect. That means it is very close to being fairly valued or perhaps only marginally undervalued.

{kind=link}

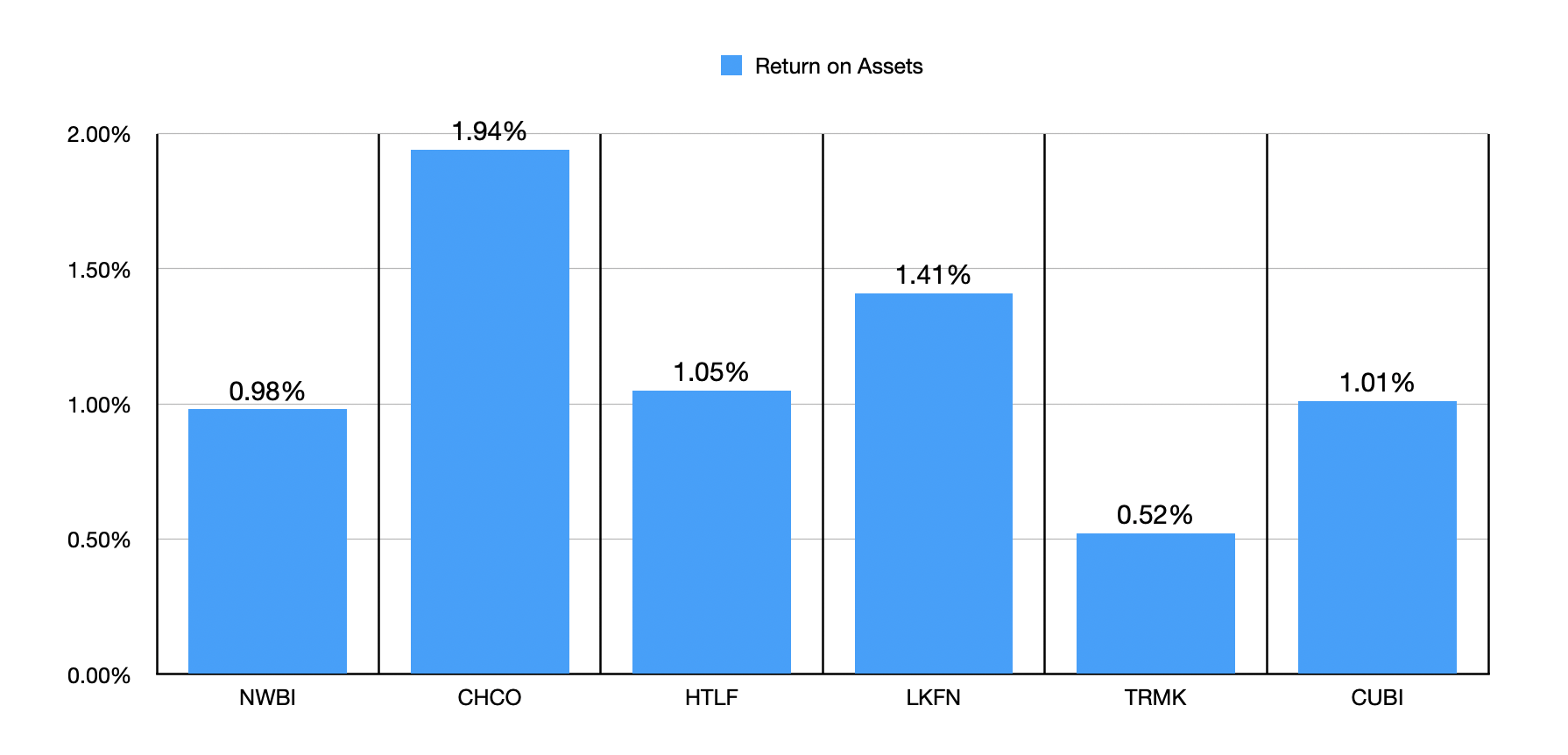

Now, a case could be made that Northwest Bancshares deserves to trade at a meaningful premium to similar firms, which in theory would make the stock still attractively undervalued. However, I don't think this is the case. If anything, the stock probably deserves to trade at a modest discount to similar regional banks. In the first chart below, for instance, you can see the return on assets of our candidate stacked up against five other regional banks of a similar size. Only one of the five enterprises shown has a return on assets that is lower than what Northwest Bancshares has. And keep in mind that 2023 was not a year in which very many institutions reported year-over-year profit improvements. So if anything, this return on asset picture exists even as some other players in the market certainly reported weakening compared to the year prior. In the subsequent chart below, you can see the same type of analysis, except using return on equity. Once again, only one of the five companies was lower than Northwest Bancshares.

{kind=link}

{kind=link}

Takeaway

We have had a pretty nice run over the past few months. Shares of Northwest Bancshares have outperformed the market on a scale of almost two to one. But all good things come to an end and I believe that additional upside for this particular prospect is limited. As a value investor, I do have a history of selling shares of businesses too soon. It is possible that my assessment might leave some money on the table, but when compared to other opportunities that exist out there, I think that this is a small risk that investors are taking. At the end of the day, I feel that a downgrade to a 'hold' rating is most appropriate.

For further details see:

Northwest Bancshares: A Step Back Might Not Be So Bad (Rating Downgrade)