CRTSF - Novozymes: Becoming A Global Leader In Bio-Solutions With Chr. Hansen Merger

2023-12-21 10:27:09 ET

Summary

- Novozymes and Chr. Hansen are close to completing their merger, creating a global bio-solutions leader with strong competitive moats.

- The combined company is expected to deliver higher revenue growth and increased profitability through cost and revenue synergies.

- However, the current valuation of the company is too high, leading to a 'Hold' rating and the need for a lower share price for investment.

Novozymes ( NVZMF )( NVZMY ) is one of our favorite European companies, as it has excellent profit margins, decent growth, and a very strong competitive moat. To increase the size of this moat, Novozymes re-invests ~11% of its sales into R&D projects for product innovation and productivity improvement. The company has usually traded at an expensive valuation, which is why we rated the company as a 'Hold' the last time we covered them. It has been almost a year, and shares are only slightly higher, significantly underperforming the STOXX Europe 600 Index ( STOXX ), the Euro STOXX 50 ( FEZ ), and the S&P 500 ( SPY ).

Still, the company is close to completing its merger with Chr. Hansen ( CHYHY ), which will transform the company into a global bio-solutions leader. Novozymes already dominates in enzymes, and Chr. Hansen adds significant microbial capabilities. Chr. Hansen produces microbial solutions for the food, beverage, and pharmaceutical markets. The company also has a strong competitive moat thanks to the strength of its intellectual property, high customer switching costs, and scale.

As a microbial and fermentation technology leader, Chr. Hansen has one of the world's largest commercial bacteria collections of ~40,000 strains, and re-invests ~8% of revenue into R&D. Its portfolio of intellectual property includes 3,400 patents and 3,100 trademarks. This gives the company an edge over competitors, and significant pricing power, which are part of the reasons the company is now guiding for full-year organic revenue growth of between 9% and 11%.

The expectation is that their merger will be completed very soon, most likely in the first few months of 2024. In this article, we'll take a look at how the combined company will probably look, and whether this helps make shares more attractive. At the time of the merger announcement, Novozymes shares reacted negatively, as investors probably thought the premium paid for Chr. Hansen was too high. Novozymes offered public shareholders of Chr. Hansen, a 49% premium, which represents 1.5326 Novozymes shares per Chr. Hansen share. To its credit, Novo Holdings, which is a significant shareholder in both companies, accepted a much lower ratio of 1.0227. This reduced the blended premium paid for the company to 38%.

Company Overview

Novozymes is a world leader in enzymes, which are used in applications like detergents, bio-energy, and food and health applications. For its part, Chr. Hansen is focused in microbial applications such as fermentation, and its applications are mostly in food, health, and nutrition applications.

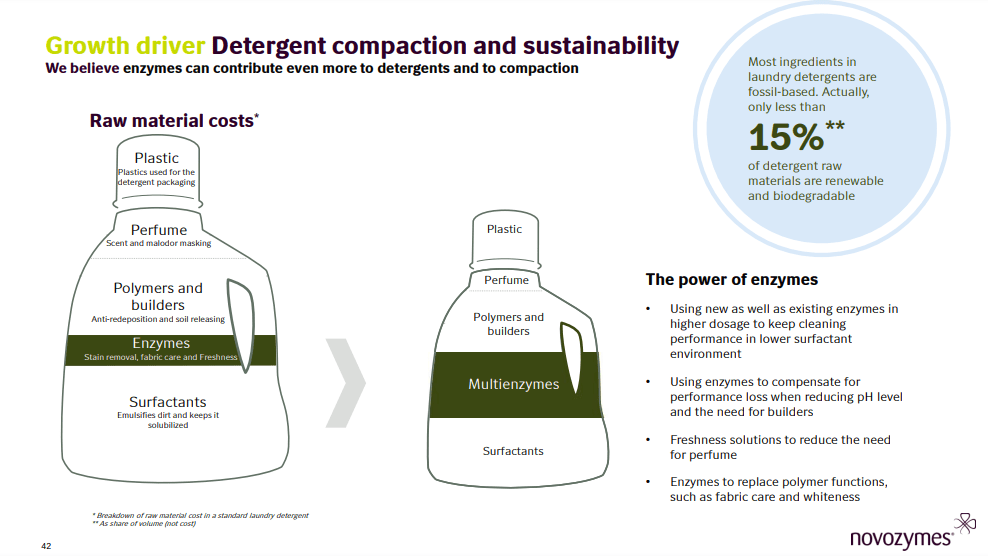

Novozymes' largest segment is household care, and it continues to generate new innovations like multi-enzymes to further reduce fossil-fuel and perfume ingredients.

{kind=link}

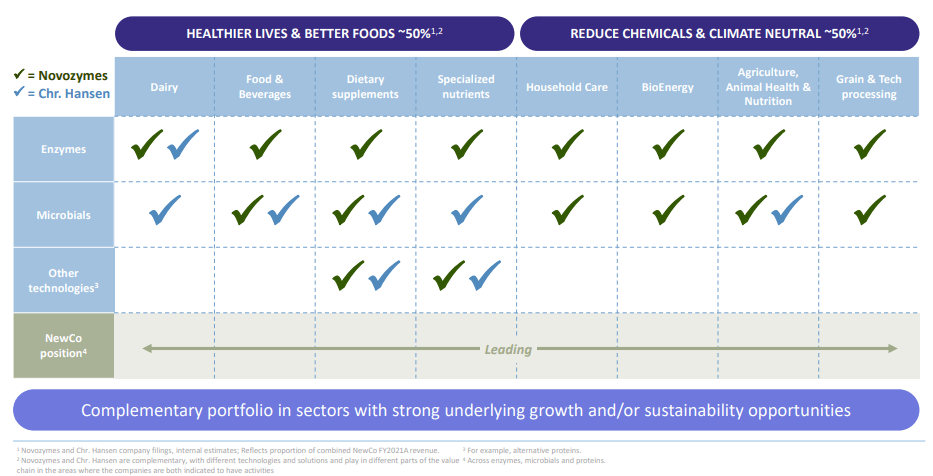

As can be seen below, the combined company offers solutions for many applications, from simple ones like dairy, to bio-energy and specialized nutrients. Together they will be a bio-solutions innovation powerhouse. One particular example of an innovation Novozymes is developing that we found very promising is a product that would help replace a fraction of the more than one hundred billion dollars of nitrogen fertilizer with a biological solution that is non-polluting to water quality and marine life. Novozymes' solution targets a solution fixating 25-30% of the required nitrogen, allowing replacement of 50-60lbs of fertilizer per corn-acre per year.

{kind=link}

Company Control

One important aspect to mention is that the company is effectively controlled by Novo Holdings A/S, which has around a quarter of the shares but close to three quarters of the voting power. Novo Holdings A/S is wholly owned by the Novo Nordisk Foundation, which has the objectives of providing a stable basis for the commercial and research activities of the companies in the Novo Group, and to support scientific, humanitarian and social causes.

Novozymes

Growth

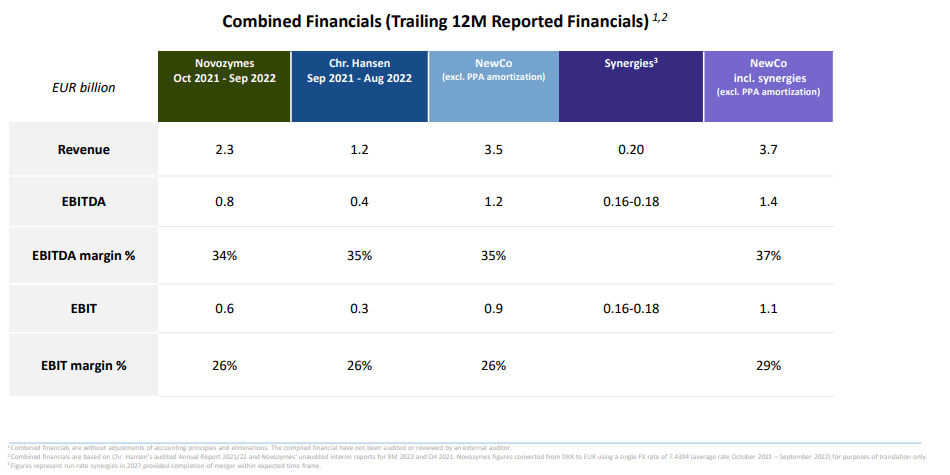

We believe one of the motivations behind the Chr. Hansen's acquisition, besides the cost and revenue synergies, was the higher revenue growth the company has been delivering. Management has guided for the combined company to deliver organic revenue growth between 6% and 8% until 2025, including synergies. For 2023 Chr. Hansen 2023 guided for revenue to grow between 10% and 12%. This is higher than Novozymes organic sales growth of 4% to 6%. As can be seen in the graph below, Chr. Hansen has been averaging a higher revenue growth rate, even if it has been more volatile.

Financials

Thanks to cost and revenue synergies, management is guiding for the EBIT margin to increase by roughly 2-3%, and is expected to reach 29% by 2025 when excluding integration costs and PPA amortization. In any case, it is clear both companies enjoy above average profitability, which is the result of their strong competitive moats.

Balance Sheet

As Chr. Hansen's shareholders are being paid with new Novozymes shares, no additional debt is expected to be issued as a result of the merger. Leverage is expected to remain quite low, with a target of net interest bearing debt to EBITDA of roughly 1.3x to 1.7x, and the company plans to keep it within that range going forward.

Novozymes also took the opportunity to share its dividend policy, with the company planning on maintaining a ~50% payout ratio, while retaining the remaining earnings to finance growth opportunities.

Valuation

The combined enterprise value of both companies is around $26 billion. The value should actually be a bit lower because of Novo Holdings accepting a lower exchange rate, but let's simplify it by assuming this as the EV of the new company.

When they shared the plans to merge, they guided for a potential EBIT of €1.1 billion, or about $1.2 billion. That puts the post-synergies EV/EBIT multiple at ~22x, which will likely result in a price/earnings ratio, once taxes and interest are considered, above 30x. In other words, shares are not cheap, even if the company delivers on its synergy promises.

{kind=link}

Similar companies in the specialty ingredients industry trade at very high multiples. For example, Givaudan ( GVDNY ) has an EV/EBITDA of close to 28x, while Symrise ( SYIEY ) is trading with a ~22x multiple. International Flavors & Fragrances ( IFF ) looks cheaper, but has been dealing with negative revenue growth.

We've come to the conclusion that much of the synergies benefit will simply compensate for the premium paid for Chr. Hansen. Perhaps it does come with some diversification benefits, and might provide some financial benefits in the longer term if their innovation teams work well together to come up with innovations that would otherwise not happen. Based on our calculated net present value for our estimated future earnings, we believe shares are currently overvalued. To get a ~10% return, we believe an investor would have to purchase the shares at close to $40, and they are currently trading slightly above $50. We have to discount earnings at a ~7% rate to get to the current price.

| EPS |

| Discounted @ 10% |

| FY 24E |

| 1.82 |

| 1.65 |

| FY 25E |

| 1.98 |

| 1.64 |

| FY 26E |

| 2.16 |

| 1.62 |

| FY 27E |

| 2.36 |

| 1.61 |

| FY 28E |

| 2.57 |

| 1.60 |

| FY 29E |

| 2.80 |

| 1.58 |

| FY 30E |

| 3.05 |

| 1.57 |

| FY 31E |

| 3.33 |

| 1.55 |

| FY 32E |

| 3.63 |

| 1.54 |

| FY 33E |

| 3.95 |

| 1.52 |

| FY 34E |

| 4.31 |

| 1.51 |

| Terminal Value @ 4% terminal growth |

| 65.88 |

| 20.99 |

| NPV |

| $38.39 |

We therefore agree with Seeking Alpha's 'D-' grade for Novozymes' valuation, and will maintain a 'Hold' rating. Still, we believe this is a company worth following, and we might invest if shares were to trade at a slightly lower valuation.

Seeking Alpha

Risks

We believe the company has very good geographical and customer diversification, and strong competitive advantages. The main risk we see for investors is the high valuation multiple at which the shares trade. If revenue growth disappoints, or if there are integrations issues during the merger, this could result in a significant price decline.

Conclusion

With the Novozymes and Chr. Hansen's merger expected to complete very soon, we wanted to take a new look at the investment opportunity they present. The combined company will have impressive capabilities, and it is clear it will be a biological solutions power house. Unfortunately, the valuation remains too high in our opinion, and we are therefore keeping a 'Hold' rating.

For further details see:

Novozymes: Becoming A Global Leader In Bio-Solutions With Chr. Hansen Merger