CHYHY - Novozymes: Close To Being A Buy Again

2023-10-10 21:54:11 ET

Summary

- Novozymes' stock is declining for almost two years and has lost almost 50% of its previous value.

- The company reported mediocre half-year results for fiscal 2023.

- But Novozymes has a wide economic moat around its business, making the company a good long-term investment.

- The stock is now trading close to its intrinsic value and could be a solid investment generating a 10% annual return.

In June 2023 I published an article covering the merger between Novozymes ( NVZMF ) and Chr. Hansen ( CHYHY ). In the article, I wrote:

In my opinion, the stock price in the last few years was just not reflecting the fundamental reality. And at least since 2021, an investment in Novozymes would not have been a good decision. It remains to be seen if Novozymes’ stock price will decline even lower and maybe become a good investment after all.

Since June 2023 the stock of Novozymes declined 17.5% and with the stock constantly declining, let’s take another look at the company and stock and try to answer the question if Novozymes is a good investment right now. The stock has lost already half of its value since the previous all-time high. In the following article, I will especially focus on Novozymes because it would be the stock I would buy right now when having to choose between the two Danish companies. Nevertheless, we will pay attention to both companies in the article.

Last Results

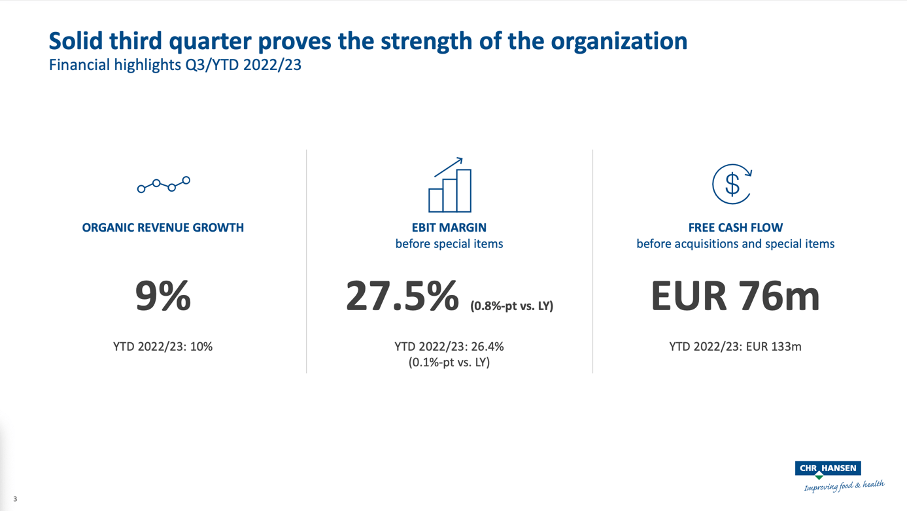

Let’s start by looking at the last reported results and between the two companies, Chr. Hansen seems to be reporting the better results right now. In the third quarter, Chr. Hansen could increase revenue from €318.3 million in the same quarter last year to €334.8 million this quarter – resulting in 5.2% year-over-year growth. However, organic growth was 9% and the negative currency effects had an impact on Chr. Hansen’s results in Euro.

Chr. Hansen Q3/22-23 Presentation

{kind=link}

EBIT before special items also increased from €84.8 million in the same quarter last year to €92.2 million this quarter resulting in 8.7% year-over-year growth. And free cash flow more than doubled from €30 million in the same quarter last year to €76.3 million this quarter, but in this case, the 2022 quarter was rather the outlier.

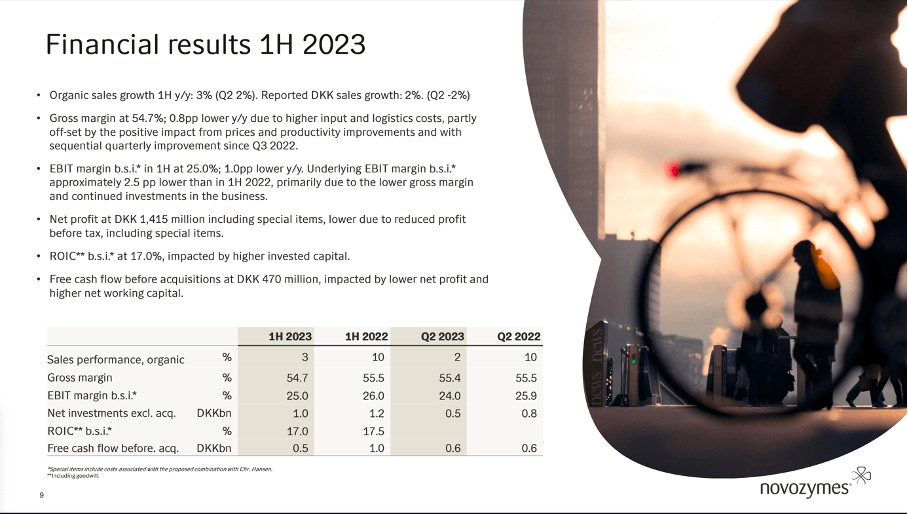

When looking at Novozymes’ results instead, we can also see the company growing its top line. Revenue increased 2.1% YoY from DKK 8,657 million in H1/22 to DKK 8,840 million in H1/23. But operating profit declined from DKK 2,252 million in H1/22 to DKK 1,999 million in H1/23 – resulting in an 11.2% YoY decline. And diluted earnings per share also declined 14.8% YoY from DKK 5.87 in the same timeframe last year to DKK 5.00 this year.

{kind=link}

And the mediocre results Novozymes is reporting are probably one of the reasons why Novozymes’ stock is constantly declining.

Intrinsic Value Calculation

In previous articles, the major reason for not investing in Novozymes was the price. Despite being a great business, I always considered the stock too expensive (and in June 2021 I even rated the stock as a “Sell” – something I do seldom for high-quality businesses with a wide economic moat).

However, when calculating an intrinsic value right now we can come to the conclusion that the stock might be fairly valued again. When calculating an intrinsic value, it makes sense to already look at the new company resulting from the merger between Novozymes and Chr. Hansen and I will actually make similar assumptions as in my previous article.

When looking at the guidance for Novozymes and Chr. Hansen, we can assume the new combined company to generate a free cash flow of around DKK 4.2 billion. Especially as Novozymes is rather generating a low amount of free cash flow (according to historic free cash flow conversion rates), we can be optimistic these assumptions are reasonable.

Let’s assume about 6% top line growth (although Chr. Hansen and Novozymes are a little more optimistic and assume between 6% and 8% till 2025). However, 6% growth is in line with Novozymes’ long-term organic growth rate. And similar to the past, Novozymes should also be able to improve its margins further. Let’s also be cautious and assume that margin improvements will add 1% growth to the bottom line. However, management is assuming operating margin to improve to about 29% in the next few years with Novozymes currently reporting “only” an adjusted EBITDA margin of 26%.

{kind=link}

In the past, Novozymes also used share buybacks. We can assume management will use share buybacks again and in most years during the past decade, Novozymes spent about DKK 2.0 billion on share repurchases. At a current market capitalization of DKK 65 billion, this is enough to buy back about 3% of outstanding shares. Let’s be more cautious and assume 2% additional bottom line growth due to share buybacks.

{kind=link}

Summing up, we can assume 9% growth for the next 10 years followed by 6% growth till perpetuity. As always, we are calculating with a 10% discount rate, and I will calculate once again with 434 million outstanding shares (the number calculated in my last article for the time following the merger). Calculating with these assumptions will lead to an intrinsic value of DKK 299 for the stock and Novozymes might be slightly undervalued already.

And while I would argue that 9% growth is a rather optimistic assumption, we must point out that Novozymes could grow earnings per share with a CAGR of 11.49% since 1999. From that point of view, 9% annual growth for the bottom line seems like a realistic assumption.

Strong Case for Novozymes

Usually, I would make the case for buying undervalued stocks – defined as stocks that are trading clearly below the calculated intrinsic value. But Novozymes might be one of the companies we can make an exception as the business is offering extremely high levels of stability and consistency and being fairly valued at this point is already implying a 10% annual return and an investment in Novozymes would already outperform the market. Let’s quickly recap why Novozymes is a great business.

Shareholder Structure

The first important aspect is the shareholder structure, which I already mentioned in previous articles. In the new company, Novozymes shareholders will hold 44%, and Chr. Hansen shareholders will hold 34% of the shares. The remaining 22% stake will be held by Novo Holdings, but it has already announced its intention to increase its stake to 25.5% in the foreseeable future. And as we can see in the chart below, Novo Holdings has voting power and is therefore able to control the business.

{kind=link}

And as I have explained in an article about “family-run businesses” it is often good when one major shareholder controls the business and is interested in the long-term performance of a company.

Improving margins, high RoIC

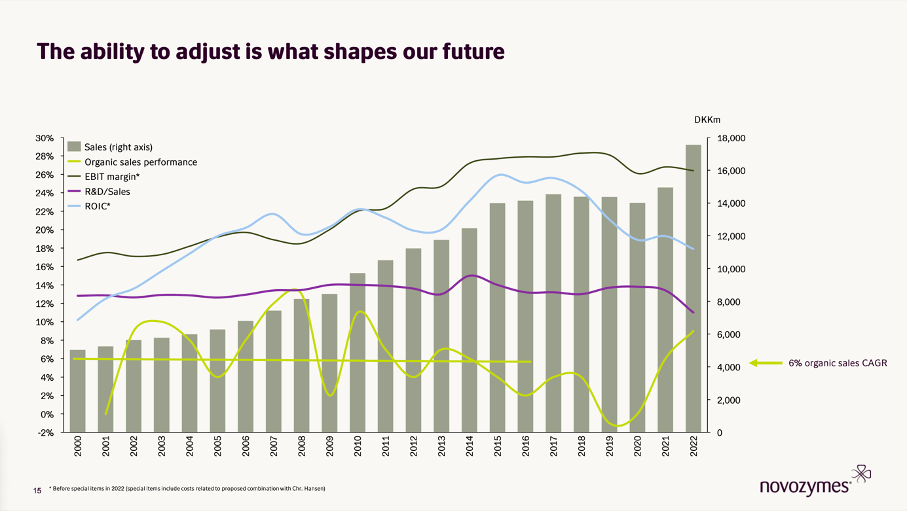

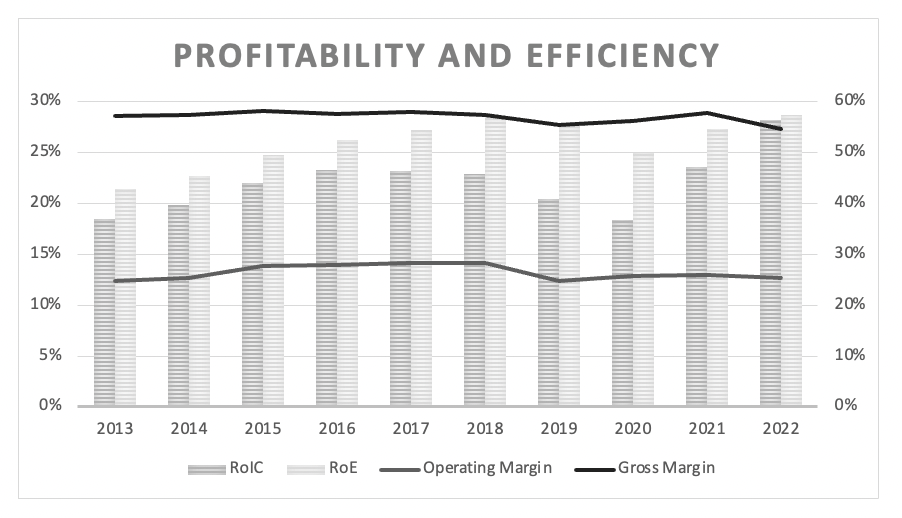

When looking at Novozymes, we see not only extremely stable gross and operating margins over the last ten years, but we also see a return on invested capital that was above 15% in every single year and in most years even above 20%. And the average RoIC was 22.01% in the last five years.

Novozymes - Margins and Return on invested capital (Author's work)

{kind=link}

We can also look at the metrics for Chr. Hansen – especially for return on invested capital as I consider this metric to be one of the most important. In the last ten years, Chr. Hansen could report an average RoIC of 15.98%.

Chr. Hansen - Margins and return on invested capital (Author's work)

{kind=link}

Growth: Stability and Consistency

Another important aspect is the high stability and consistency we are seeing when looking at revenue and earnings per share growth. Since 1999 Novozymes could not grow every single year, but we see a picture with little fluctuations – a strong hint that we are dealing with a high-quality business.

{kind=link}

Recession-resilient business

Novozymes is not only growing with a rather stable pace and high levels of consistency. When looking at the last few recessions, we also see a rather recession-resilient business. During the 2020 recession, Novozymes had to report revenue declining 2.5% year-over-year. And while a decline is not great, we are talking about a low-single digit decline. And the picture during the last two recessions (Great Financial Crisis and the recession following the Dotcom Bubble) is similar. The worst annual decline during the Great Financial Crisis was 3.7% in 2009 and in the years between 1999 and 2003, revenue increased every single year.

High barriers to entry

Novozymes also has high barriers to entry. Companies that are trying to enter the sector are faced with high upfront costs and the fact that Novozymes is spending between 10% and 15% of sales on research and development (see chart above). This is making it very difficult for companies (especially small businesses) to keep up with Novozymes and match the spending on R&D as well as innovation. This is creating high barriers to entry for every new competitor.

Growth Potential

Novozymes is addressing a huge market. And although Novozymes is clearly among the market leaders (even more so after the merger with Chr. Hansen), the company generated about DKK 18 billion in revenue while the overall addressable market of enzymes, microbes, and alternative proteins is expected to be around DKK 100 billion right now.

{kind=link}

And not only could Novozymes grow by gaining additional market shares in the years to come, but the underlying market is also growing at a healthy pace and different studies are expecting sales growth in the mid-single digits in the years to come. One study is expecting a CAGR of 6.7% until 2030 and another study is seeing the market growing with a CAGR of 6.9%.

{kind=link}

Overall, Novozymes is a world leader in a growing market. And as already mentioned above, Novozymes is not only spending huge amounts on research and development, but it also has a best-in-class production and a highly diversified base of 2,000 customers across 30 industries and 140 countries. We are therefore dealing with a wide moat company, that has also a dominant position in the industry and is operating in a growing market.

Technical Picture

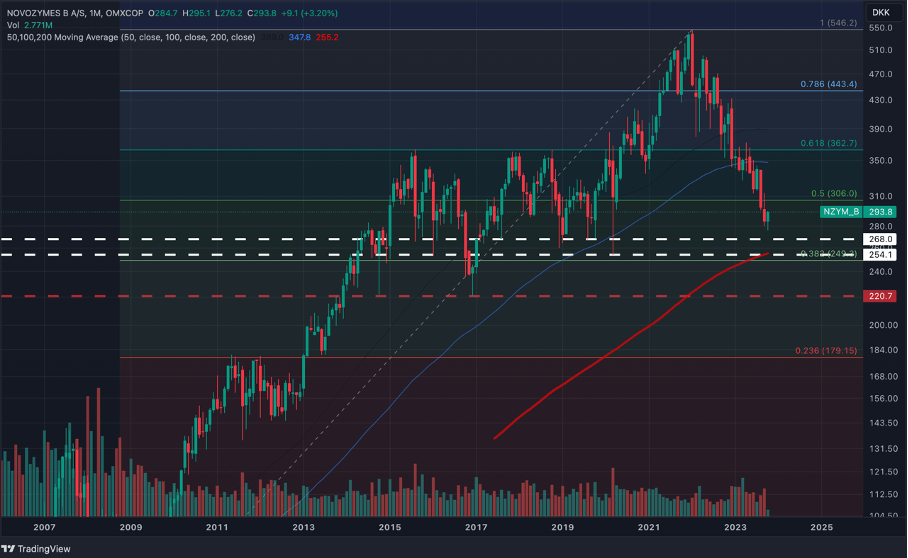

A final aspect we should pay attention to is the chart of Novozymes. Since the beginning of 2022, Novozymes’ stock is declining – and it is in good company as many other stocks also peak at the end of 2021 or the beginning of 2022. But after almost two years of constant decline, Novozymes is slowly getting towards levels where the stock could bottom and where we find strong support levels in the chart.

Monthly chart Novozymes (TradingView)

{kind=link}

When looking at the chart, I would argue to be a little more patient at this point as it seems likely for Novozymes to drop a little lower. Around DKK 250 we find a strong support level for Novozymes. Here we can not only find the 38% Fibonacci retracement of the bullish wave that took Novozymes from the Great Financial Crisis lows to the previous all-time high. We also find a strong support level from previous lows marked in the years 2018 to 2020. And finally, the 200-month simple moving average is also in this range.

If this support level does not hold, we find two additional support levels around DKK 220 (previous lows from 2014 and 2016) and around DKK 180 (23% Fibonacci retracement and 2011 highs that led to a correction for the stock). And while I don’t want to rule out that Novozymes might decline further, I don’t know if the stock will decline to DKK 180.

Conclusion

Novozymes is constantly moving closer to a price range where I could consider buying the stock. But maybe we should wait a little longer as we find a strong support level for the stock around DKK 250 and if the stock reaches that price level, we can also argue for Novozymes being undervalued. But Novozymes is already the cheapest it has been in the last three years since I started covering the company in 2020.

For further details see:

Novozymes: Close To Being A Buy Again