JPM - NPFD: Deep Discount Presents An Opportunity

2023-08-17 15:48:43 ET

Summary

- Nuveen Variable Rate Preferred & Income Fund provides exposure to preferred and income investments and is trading at an attractive discount.

- The fund's portfolio includes a mix of fixed-to-fixed and fixed-to-float securities, with a majority of the holdings being investment grade.

- NPFD has seen distribution cuts similar to peers as borrowing costs have increased quite materially.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Nuveen Variable Rate Preferred & Income Fund ( NPFD ) provides exposure to some floating-rate preferred investments and is currently trading at an attractive discount. The fund also focuses on holding a larger allocation to investments considered investment grade of BBB or above.

The fund launched near the end of 2021, and we generally see a discount widening happen shortly after a closed-end fund initially launches. In the case of NPFD, it was also met with an environment where CEFs overall started to go to wider discounts. Along with higher interest rates from the Fed that drove up yields through 2022, this fund was just as susceptible to everything else preferred funds went through earlier this year in the banking crisis.

An important consideration is that despite the "variable rate preferred" in its name, the majority of the portfolio actually isn't holding floating rate exposure, and they are quite flexible in what they can hold. That includes the now infamous contingent convertible securities (AKA CoCos, AKA AT1 Bonds).

Thus, this fund not only presents a decent opportunity with an attractive discount but investing in preferreds while they are beaten down can present another compelling argument to consider this fund.

The Basics

- 1-Year Z-score: -0.77

- Discount: -13.78%

- Distribution Yield: 6.51%

- Expense Ratio: 1.50%

- Leverage: 33.54%

- Managed Assets: $691.631 million

- Structure: Term (anticipated liquidation date of February 1st, 2034)

NPFD's investment objective is to "provide a high level of current income and total return." They attempt to accomplish this through "investing in primarily investment grade, variable rate preferred securities and other variable rate income-producing securities from high quality, highly regulated companies such as banks, utilities and insurance companies."

Interestingly, they go in more depth in their prospectus and mention that "under normal market conditions, the Fund will invest at least 80% of its assets in variable rate preferred securities and other variable rate income-producing securities." However, that isn't exactly how they are positioned at this time. The "under normal market conditions" seemingly leaves it a bit ambiguous and ultimately allows for management to invest how they see fit. Where it gets a bit more interesting is the "fixed-to-fixed preferreds," which they are likely counting as variable rates.

They also include that the fund may "invest up to 20% of managed assets in contingent capital securities or contingent convertible securities (CoCos) and up to 15% in companies located in emerging market countries but will invest in U.S. dollar-denominated securities."

They also mention that "more than 25% of managed assets will be invested in securities of companies in the financial services sector." This is generally the case with preferred funds anyway, since financial institutions are the largest issuers of preferreds that are non-cumulative perpetual to help with regulatory ratios.

The fund is leveraged, and the borrowing costs of the borrowings are quite elevated, as we've seen across all leveraged funds due to the Fed raising interest rates.

{kind=link}

When including the fund's expense ratio, the fund's total expenses come up to 3.85%. The fund didn't have any interest rate swaps in place as of their last semi-annual report but had some futures contracts where they were short U.S. Treasury 5-Year Notes. By being short, that works as a hedge against rising interest rates and yields.

Term Extensions And Perpetual Possibilities

As is the case with the overwhelming number of CEF issues launched after 2018, it's a term structured fund. This information can be found in the fund's prospectus .

In this case, the fund comes with a 12-year term, and it comes with the usual caveats of the Board being able to extend the term without shareholder approval. For NPFD, this is up for two one-year periods.

Additionally, the fund also can potentially present the opportunity to go perceptual through the utilization of a tender offer. This is also at the Board's discretion and not guaranteed to happen. The tender offer would be at 100% of NAV for 100% of shares. It would be done within 18 months preceding the anticipated liquidation date.

Most funds have provided a "termination threshold," which is the amount of net assets that would be left over if the shares that were tendered were purchased by the fund. The threshold is often $200 million, but some smaller sponsors have put it at $100 million. In the case of NPFD, they've also left this amount up to the Board at the time if they went through with a tender offer.

Eligible Tender Offer. The Declaration of Trust provides that an eligible tender offer (an “Eligible Tender Offer”) is a tender offer by the Fund to all holders of outstanding Common Shares as of a date within the 18 months preceding the Termination Date. If the tender offer is completed, Shareholders who properly tender Common Shares in the Eligible Tender Offer will receive a purchase price equal to the NAV per share on the expiration date of the Eligible Tender Offer. In an Eligible Tender Offer, the Fund will offer to purchase all outstanding Common Shares held by each Common Shareholder. At the time of the Eligible Tender Offer, the Board of Trustees will determine the Termination Threshold. The Termination Threshold will be based on prevailing market conditions at the time of the Eligible Tender Offer.

Performance - Attractive Discount

As mentioned, most new CEFs drop to a discount, but the environment for NPFD was particularly harsh. However, for investors buying now, it could still be a consideration.

Of course, this is assuming the Fed doesn't have to raise rates significantly from here, and yields don't start rising materially. Fitch downgrading the U.S. credit rating at this time is likely one more thing to consider as that has pushed up the 10-year Treasury Yield. The large discount and the beaten-down preferreds themselves in the underlying portfolio help provide some cushion here.

Since the fund's launch, the total NAV returns have performed about as well as we've seen in its peers. In fact, interestingly, it holds quite a tight correlation with the Flaherty & Crumrine Preferred and Income Securities Fund ( FFC ).

Ycharts

At first, one might believe that this is where the "variable" portion of its name and investment policy should kick in. In theory, that should have offered some downside protection relative to the peers that are "traditional" preferred funds. Well, this gives us a good idea that NPFD actually isn't too differently positioned from any of the other preferred CEFs.

Cohen & Steers Tax-Advantaged Preferred Securities and Income ( PTA ) has been able to perform somewhat better in this historical period. Of course, the fund has a narrower discount, and investing is about looking forward. What happened over the last year and a half since December 2021 is unlikely to be the environment that unfolds over the next year and a half. PTA had hedged against higher rates through interest rate swaps. NPFD realized some gains from their futures contracts, according to their last report, but PTA's strategy was seemingly more effective. F&C funds chose to go into the environment with no hedging at all, which didn't show any different result from NPFD's shorting futures contracts.

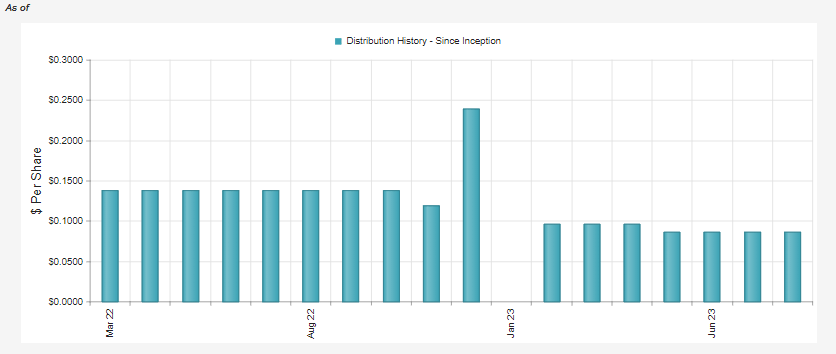

Distribution - Rising Borrowing Costs Bite

Similar to what we saw with most other preferred CEFs, leverage costs rising have negatively impacted the fund's distributions. The reason is that net investment income is declining due to rising borrowing costs through this period. That's resulted in three distribution cuts from NPFD since its launch, which is likely another driving factor in the fund's discount widening. We saw similar actions from the Flaherty & Crumrine funds, which also saw discounts widen out substantially after being some of the more richly valued in the space.

{kind=link}

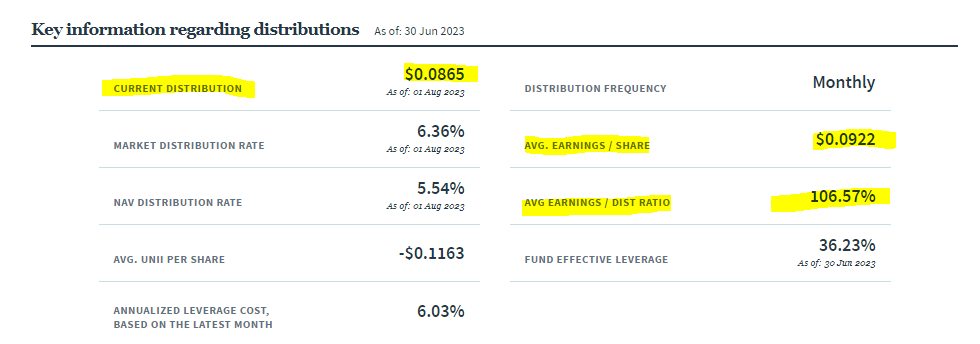

Based on the NII earnings in the last three months against the current distribution rate, we see that coverage is just over 106.5%.

NPFD Distribution Coverage (Nuveen (highlights from author))

{kind=link}

As the Fed put in another hike, the borrowings for this fund have also gone up again from this level which could mean further distribution cuts in the future if rates rise higher than anticipated. They pay at a rate of OBFR plus 0.85%, which means right after the Fed raised, we saw a pop in OBFR to 5.32% pushing NPFD's borrowing costs to 6.17%. Leverage in the fund, in this case, is less about generating additional yield at this point and more about expecting a future rebound in preferreds to provide an added boost to results.

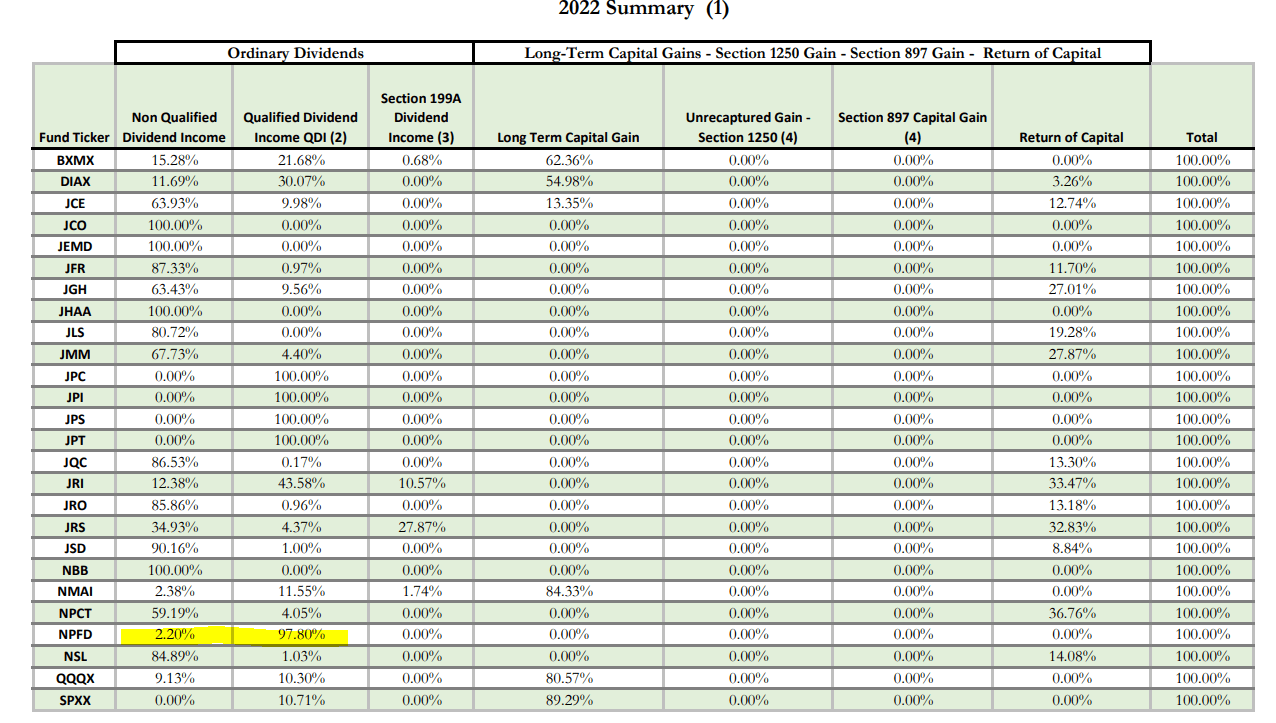

In terms of taxes, the majority of the fund's distribution in the prior year was classified as qualified dividend income. This is also another benefit of preferred investments that most of their dividends are qualified, and that should make them tax-friendlier relative to ordinary income rates.

Nuveen CEF Tax Classifications (Nuveen (highlight from author))

{kind=link}

NPFD's Portfolio

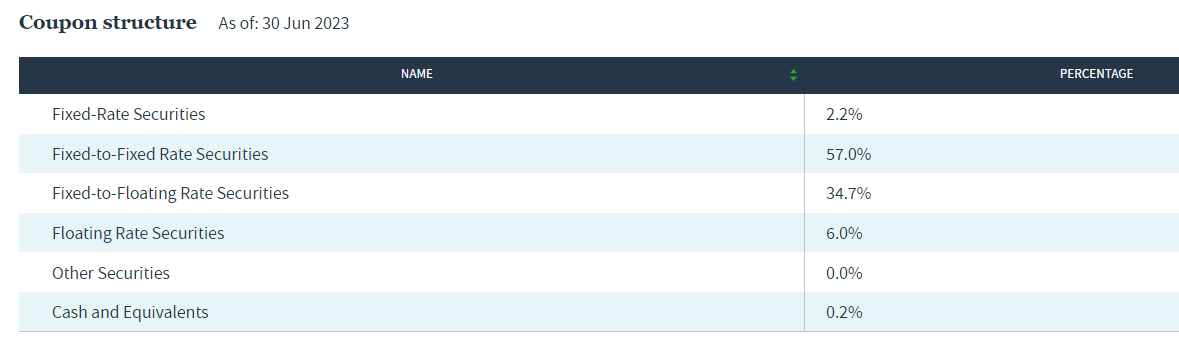

To give us a better understanding of how the fund is positioned, we can take a look at the coupon structure breakdown that they provide. That's where we see the majority of the fund is dedicated to fixed-to-fixed rate securities.

{kind=link}

This is where I assume they are counting these as "variables" since they are reset based on a schedule. Between those and the fixed-to-float securities, which are also being pooled at a variable rate for the purposes of their investment policy, then we are over the 80% hurdle they outlined.

One of the problems with fixed-to-fixed is that the schedule can be years. If it is about to reset to a much higher rate, the company could simply redeem them instead. This is a similar problem with fixed-to-floating, the floating rate could kick in also in years down the road, and when they do, it can be redeemed.

So a number of these don't generally end up floating at all. Instead, the main benefit here would be seemingly the upside of realizing gains when they are called if they are currently trading at a discount.

{kind=link}

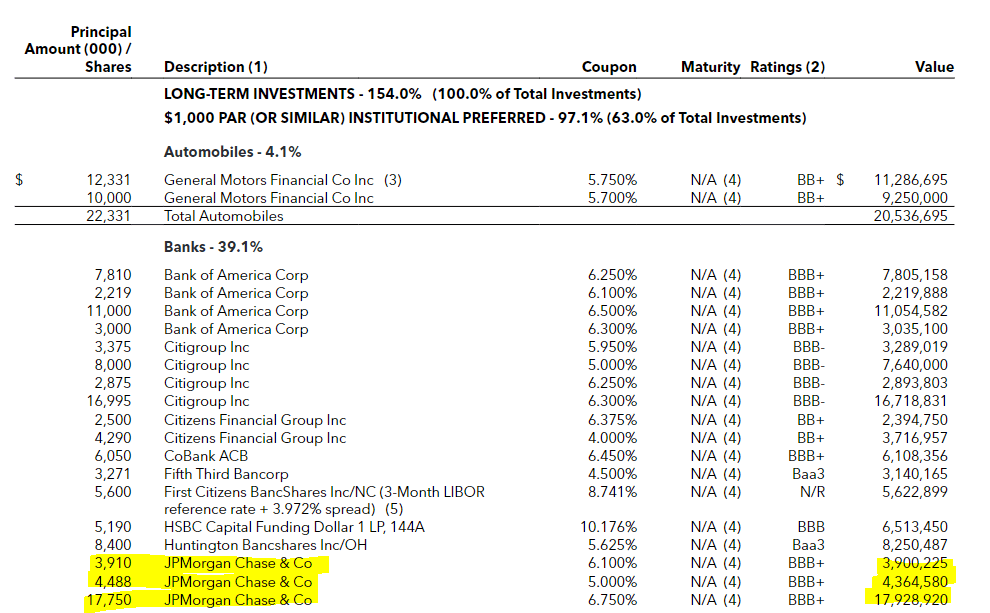

An example of this could include the JPMorgan ( JPM ) preferred they are carrying here.

{kind=link}

The first one listed here is the JPM 6.1% Fixed-to-Floating Rate Non-Cumulative Preferred Series X. The floating rate period for this position would kick in on October 1st, 2024. It would be based on three-month LIBOR plus 3.33%. LIBOR is discontinued now, and things are transferring over to SOFR or OBFR, but these are older preferred issuances we are looking at. Overall, it's a decent rate that they are currently paying, but assuming rates were flat from here, they would see a significant increase in the dividend yield they'd have to pay on this Series X issue.

That is what could compel them to simply redeem this preferred instead of letting it hit the floating period. Of course, assuming that it makes financial sense for them to do so. Near the end of 2022, JPM redeemed their Series I preferred that were also fixed-to-float. Series I was allowed to float for a period of time with an initial redemption date of April 30th, 2018; however, the fixed rate was 7.9% after being issued in 2008. The floating rate was three-month LIBOR plus 3.47%. It just so happened to be that in September 2022, LIBOR started to push through 3% and nearer to 4% by the end of the month , therefore, driving up the costs on the Series I to start getting near the original fixed rate.

JPM is a solid company, and this was issued with a fairly strong yield for an investment-grade business, so the principal amount relative to the value isn't indicated tremendous upside. Still, there would be some upside when it was redeemed in terms of capital appreciation.

However, then another example of a position that would actually see some downside from current levels would be the JPM 6.75% Fixed-to-Floating Rate Non-Cumulative Preferred Series S. It isn't provided what the cost basis is for NPFD, but from this last report, we see that principal amount was at $17.75 million while the carrying value came in at $17.929 million.

The floating rate for this issue is a bit sooner , on February 1st, 2024. Similar to the fixed rate, the floating rate is also higher at three-month LIBOR plus 3.78%. For the reasons of the floating rate coming sooner and the higher overall rate that's what can make the Series S run at a higher value relative to the Series X of the same issuer.

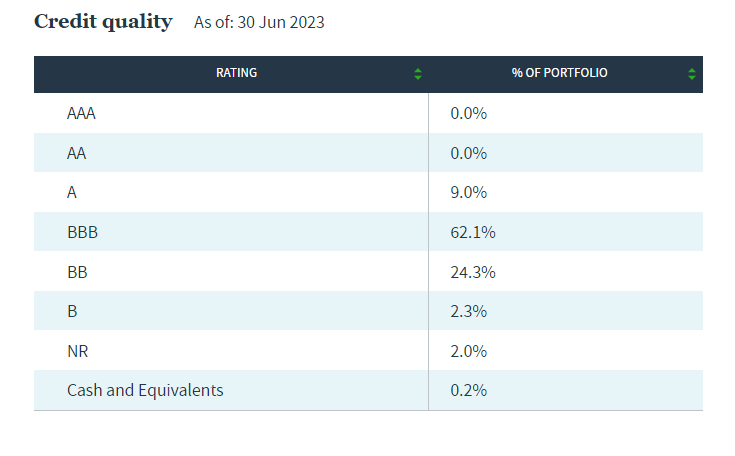

Overall, the fund has stuck with mostly an investment grade portfolio, a common characteristic of most preferred CEF peers. Though note that the portfolio isn't entirely investment-grade, and they do carry a material allocation to BB as well.

{kind=link}

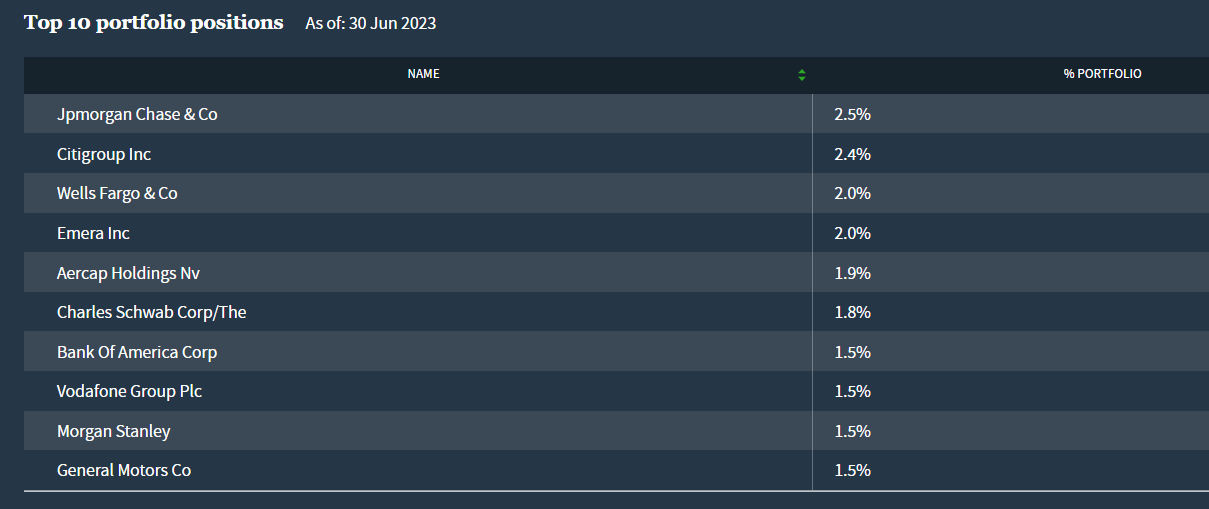

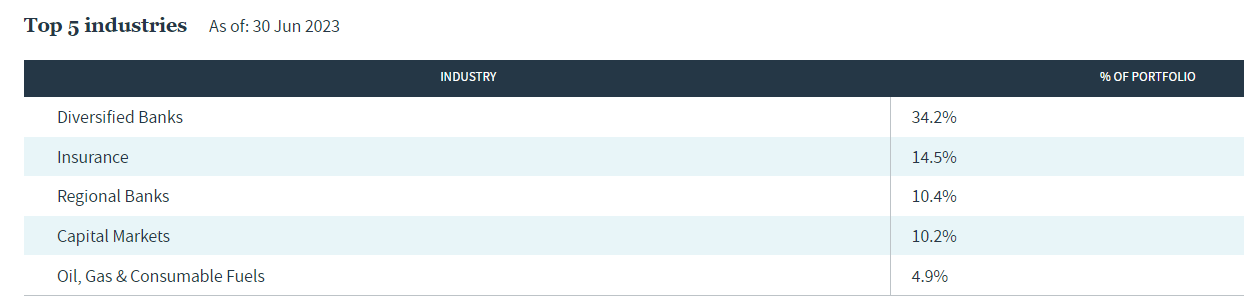

Between diversified banks, insurance, regional banks and capital markets, those industry allocations make up nearly 70% of the fund's invested asset. These are all various institutions related to the finance sector.

{kind=link}

Conclusion

NPFD is a newer offering in the preferred and income closed-end fund space. However, it's mostly similar to its older peers in the space. That's where exploiting the fund's discount/premium can come into play against peers. If you are going to own a fund that performs nearly identically to its peers, then buying those at the deepest discount can make sense.

For further details see:

NPFD: Deep Discount Presents An Opportunity