XLRE - NRO: Looking Like A Value Now But A Couple Things To Consider

2023-06-04 01:13:09 ET

Summary

- Neuberger Berman Real Estate Securities Income Fund is currently trading at a substantial discount, making it more appealing for investors.

- The fund's distribution still seems unsustainable, suggesting further cuts could be in the cards, but any adjustment could see a muted reaction due to the discount.

- Caution should be exercised as the fund has filed an N-2, which could indicate a rights offering, potentially impacting the share price.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 19th, 2023.

It's been quite a while since I've covered Neuberger Berman Real Estate Securities Income Fund ( NRO ). In my last update going back to 2020, I had noted to stay vigilant with this name as the distribution seemed unsustainable and the valuation was a bit rich.

It turns out they cut shortly after that, and the fund was pressured, but it actually rebounded quite nicely. Throughout most of 2021, the fund enjoyed a relatively higher valuation based on its discount/premium. Even through 2022, the fund touched premium levels, but it has more recently sunk to a substantial discount.

That has made it much more appealing at this time. However, one thing that hasn't changed is the fund's distribution still seems unsustainable. So further cuts could be in the cards, but since it's at a substantial discount, any adjustment could see a muted reaction.

Further caution should be noted that a couple of months ago, the fund filed an N2 . That's the first step to a rights offering, but it is worth noting that it doesn't guarantee a rights offering. It could be simply filed for an at-the-market offering or dividend reinvestment plan.

When a rights offering is announced, funds often see a precipitous drop in their share price. Neuberger Berman High Yield Strategies ( NHS ) is going through this currently. Stanford Chemist recently provided an update about NHS and the rights offering more specifically. That said, shares of NRO are trading at a substantial discount, so a rights offering would be less than ideal right now. Unfortunately, that doesn't always stop fund managers from going ahead with them anyway.

Finally, the REITs and preferred that NRO invests in are currently under pressure. They've both been grappling with higher interest rates. Unlike some of the other more popular REIT/preferred splits, NRO actually invests a lot of their preferred into REIT preferred. For example, Cohen & Steers REIT and Preferred and Income Fund ( RNP ) carries around 50% of their portfolio in preferred securities. However, only about 3% of the preferred sleeve is allocated to real estate.

All this being said, historically speaking, the current valuation has often provided a time to consider investing in NRO.

The Basics

- 1-Year Z-score: -2.30

- Discount: -13.54%

- Distribution Yield: 13.32%

- Expense Ratio: 1.3%

- Leverage: 27.27%

- Managed Assets: $220.048 million

- Structure: Perpetual

NRO's investment objective is "high current income. Capital appreciation is a secondary investment objective." To achieve this, the fund will "develop a portfolio with a broad mix of real estate securities through superior stock selection and property sector allocation."

They continue that they can invest primarily in "securities issued by Real Estate Companies, including REITs." They don't exactly specify, but that does include both the common and preferred securities issued by REITs.

The fund is fairly small, and leverage helps boost its size. However, like most other funds that utilize leverage, that not only adds risks for greater volatility of the fund but higher leverage costs as interest rates increase. The total expense ratio for NRO came to 2.06% in 2022, up from 1.69% in the previous fiscal year. Interest expense went from 0.48% to 0.76% year-over-year.

While they aren't hedged with any derivatives, the borrowing costs here are somewhat sheltered. They had listed a total of $60 million in outstanding debt at the end of 2022. This included $30 million in a fixed rate 5-year term loan and another $30 million borrowed on their credit facility that charges a floating rate. So half of their borrowings aren't subject to the higher interest rates. In fact, they locked it in at a fairly low 2.96% rate. The fund saw some deleveraging in the last year, as they took borrowings down from the $70 million at the fiscal end of 2021.

Performance - Discount Makes This Fund Appealing

The fund's historical record isn't that strong. I don't consider this usually a name that is worth holding over the long term. Perhaps utilizing a dollar-cost average could be justified. However, they've severely lacked performance in most periods against their benchmark.

To be fair, they are only benchmarking against an equity REITs index, and around 33% of their portfolio is in preferred investments. The data below is from their annual report, which is for the period ending October 2022 . It still gives us some context of the fund's performance, which isn't too strong.

NRO Annualized Performance (Neuberger Berman)

More recent results for the fund, on a YTD basis, show that the total NAV return is hanging about flat. This was after the fund experienced a sizeable jump at the beginning of the year. Since then, while the broader indices seem to be doing great, it's mostly been the tech titans supporting all of the results. Companies in the REIT space and preferred have been significantly weaker.

YCharts

What makes NRO more interesting for me now is solely the fund's discount. That discount really opened up in the last month or two as the share price significantly underperformed the NAV. While the fund has touched wider discounts, historically, it appears now is a good time to consider the fund.

YCharts

At a discount is when the fund could outperform even if they suffer a shortfall in NAV returns. This is because the market price could rise closer to a premium, as we've seen in the last 5 or so years. Remember that if a rights offering is announced, it would likely pressure the fund further.

The other caveat is that this is a more recent trend for the fund in these last 5 or so years. Going back further, the fund traded at ~15% discounts for several years.

Distribution - Seemingly Unsustainable

At the current level, NRO's distribution seems unsustainable. The fund's current distribution rate works out to 13.32%, and on a NAV basis, it is 11.52%. Higher yields generally draw in more investors, but perhaps some investors saw the N-2 filing or know that a cut is likely. Whatever might be driving this discount to open up, it could suggest a distribution cut is already priced in. Therefore, a drop in the rate could be seen with a muted price action response. The last cut was announced to start in 2021 when the fund went from $0.04 per month to $0.0312.

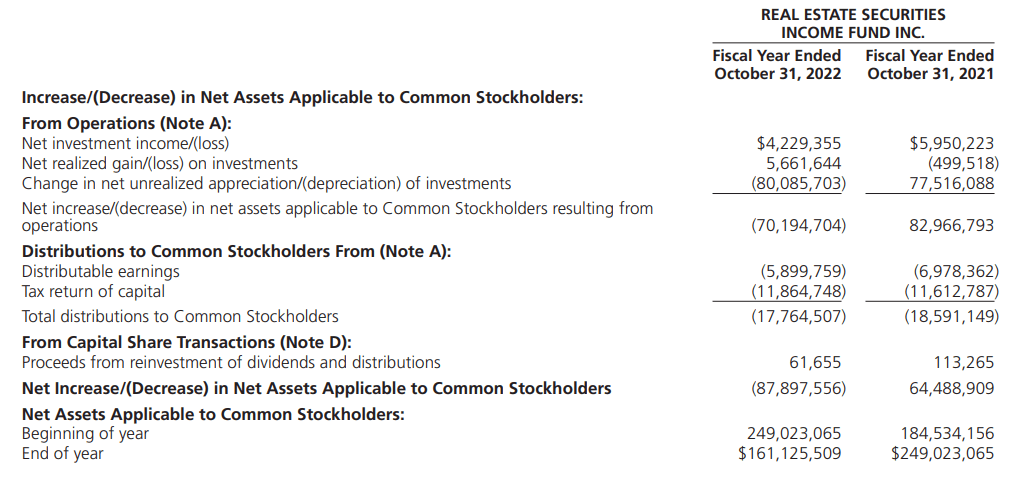

The fund saw its net investment income decline over the last fiscal year. This would have been driven by the fund's deleveraging and rising leverage costs. However, the fund will primarily rely on capital gains to fund its payout anyway.

{kind=link}

NII coverage was 23.8%, leaving the remainder needing to be funded by capital gains. Given the tough year for this fund and all REITs, that certainly wasn't considered covered in the prior year. That's why we are at the elevated distribution NAV rate in the first place, as the fund's assets slid lower.

Lower rates don't seem to be in the cards for anytime soon as the Fed is looking to pause. Lower rates would be one way to provide NRO with a boost. It would see its leverage costs recede and likely cause some of the pressure to come off of its underlying holdings. There have even been new discussions starting about another 25 basis point hike in June. Therefore, things could be pressured for a while here for this fund that's already paying an elevated rate.

Return of capital distributions has been the source of the majority of the tax classification in each of the last two years.

{kind=link}

This was even the case when it technically wasn't destructive in 2021, as the fund did experience a tremendous amount of unrealized gains. That said, 2022 would have definitely been considered destructive.

NRO's Portfolio

The fund is split between preferred and common equity positions. The preferred is the smaller sleeve of the fund. This was the breakdown from their Q1 2023 update.

NRO Asset Breakdown (Neuberger Berman)

What makes NRO a bit more unique in terms of what we see from other REIT funds is that REIT issuers dominate this preferred. As mentioned above, RNP's preferred portfolio comprises almost entirely financial or insurance names.

Over time, RNP has proven to be a significantly better-performing fund.

YCharts

On a YTD basis, I would have thought that NRO should be outperforming on a total NAV return basis. This would be due to not having that preferred financial exposure. However, the performance between NRO and RNP is nearly identical.

YCharts

Besides preferred positioning, NRO also focuses more on what could be considered value-oriented sectors compared to its benchmark Nareit.

NRO REIT Sector Exposure (Neuberger Berman)

They carry significant overweight positions in diversified and lodging breakdowns. They also have heavier exposure to shopping centers and single-family homes. Lodging and shopping centers are going to be areas of the market that are generally more sensitive to overall economic conditions.

They also have a slight overweight to office exposure. The office exposure has been a big detractor in performance, and they hold both equity and preferred positions. As of their last annual report, they had listed 3.2% of equity office REIT exposure Alexandria Real Estate Equities ( ARE ), Boston Properties ( BXP ) and Vornado Realty Trust ( VNO ).

As of the end of January 31st, 2023, they showed that these three were still positions, but the weighting dropped to 2.9%, not through any reduction in shares held but simply due to underperformance. The big news from VNO is that they recently suspended their dividend for the entire year. That would mean less income for NRO once again if they are still holding the position today.

ARE has been holding up quite well, relatively speaking. However, these three positions significantly underperformed the Real Estate Select Sector SPDR ( XLRE ).

YCharts

VNO also makes up four of the six total office preferred holdings. The others are preferreds from Highwoods Properties ( HIW ) and SL Green Realty Corp ( SLG ).

{kind=link}

HIW Series A is a non-publicly traded preferred, while the others are publicly traded. Given their fixed rates and the overall uncertainty, these preferreds have been hammered almost as badly as the equities have.

{kind=link}

Growth primarily has been coming from data centers and infrastructure REITs, each area where NRO carries underweight positions relative to its index.

Their strategy overall just hasn't seemed to work. However, for means of diversification, there could maybe be an argument made there.

Conclusion

While I don't necessarily see NRO as a long-term hold type of position, an argument could be made as it could be seen as a diversifier. Most of my REIT exposure is tied up to C&S, and they could start underperforming, as history is no guarantee of future success. All that being said, I believe that NRO is attractive due to the current discount on the fund. At this level, historically, the fund has tended to bounce. If you are a long-term holder, taking advantage of dollar-cost averaging down could be worth considering too.

For further details see:

NRO: Looking Like A Value Now, But A Couple Things To Consider