NUMIF - Numinus Wellness: Cash Burn Concern (Rating Downgrade)

Summary

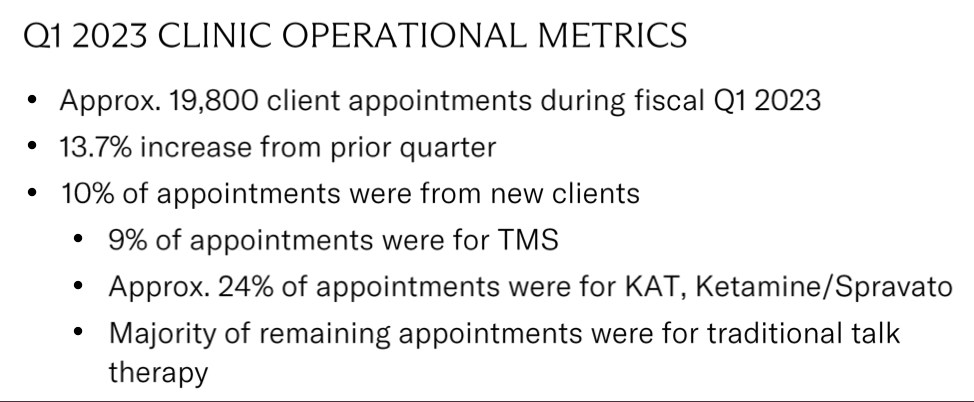

- Numinus reported solid improvements in operational metrics for its Wellness Clinic operations in 1Q23, including a 14% increase in client appointments relative to the prior quarter.

- Numinus is generating substantial revenue streams, but cash burn is a serious challenge for the company.

- Management believes that profitability can be achieved without further clinic site expansion, via practitioner recruitment and training.

- The case for regulatory approval of psychedelic-assisted therapy continues to strengthen, but there are many hurdles still to overcome, and the approval timeline remains unclear.

- Due to concerns regarding the potential for a large capital raise, I downgrade Numinus to SELL.

Introduction

Numinus Wellness ( NUMI:CA ) reported 1Q23 results on 16 January 2023. This note highlights items that caught my attention in NUMI’s 1Q23 materials and provides a refresher on significant sector news flow since my prior NUMI Seeking Alpha note published in October 2022 .

There is a lot going on in the psychedelics space and the sector is attracting ever more mainstream attention. The Economist even highlighted psychedelic-assisted therapy ‘PAT’ as one of five potentially transformational advances in 2023 – surely this is a positive sign that the remaining stigma hanging over the medical/wellness use of psychedelics is rapidly fading away.

As 2022 draws to a close, economic challenges, war and— in China—covid-19, seem all-consuming to many. But what else will the new year bring? With India set to overtake China as the world’s most populous country, America’s drug regulator considering approving a psychedelic to treat PTSD, and all eyes on the crown jewels at King Charles III’s coronation, The Economist reveals some of the less conspicuous stories to watch out for in 2023. Each has the potential to transform the world ahead.

Source: The Economist 2023: five stories to watch out for

Sector News

Currently, my main focus in the psychedelics space is on psychedelic-assisted therapy. I’m interested in groups that will be at the coal-face of delivering much-needed improvements to mental health and wellbeing to society. Other organizations that are solely or primarily working on drug development /discovery are better regarded as bio-tech stocks. From an investment perspective, bio-tech is something of a specialist field and an area that I plan to dive into over the coming months – although realistically, I’m not sure I’ll ever be able to move away from my current view that investing in bio-tech stocks requires a scatter-gun approach akin to that adopted by early-stage VC investors.

The volume and frequency of news flow in the psychedelics space can be somewhat overwhelming; listed companies, unlisted for-profit groups, not-for-profit entities and academia are all competing to stay relevant to investors and funders. It’s difficult to sort the wheat from the chaff in terms of significance/materiality, particularly at the drug discovery end of the psychedelics sector spectrum. I summarise important announcements/events over recent months relevant to PAT below.

A key announcement for the future of PAT was recently released by MAPS (Multidisciplinary Association for Psychedelic Studies) on 05 January 2023 . Whilst some commentators might argue that MDMA is not a classic psychedelic, confirmation from MAPS that their second Phase 3 trial of MDMA-assisted therapy for treatment of PTSD was successful is a clear positive for the broader psychedelics sector. MAPS aim to publish full data from the trial in a peer-reviewed journal later this year, to be followed by lodgement of a new drug application with the US Food and Drug Administration ‘FDA’. There are still many hoops for MAPS to jump through, but there appears to be genuine potential for MAPS to receive FDA approval for an MDMA-assisted therapy protocol for treatment of PTSD in late 2024.

Compass Pathways ( CMPS ) is rarely out of the news for long, and has published several noteworthy updates over recent months. The company announced the launch of Phase 3 trials applying their COMP360 psilocybin therapy to treatment-resistant depression ‘TRD’ in October 2022; this was followed by the November 2022 release regarding publication of the CMPS Phase 2b trial of COMP360 psilocybin therapy for TRD in the New England Journal of Medicine. The CMPS Phase 2b trial is the largest published psilocybin trial to date, with 233 participants receiving treatment combining psilocybin and therapy (which CMPS prefers to call ‘psychological support’ for reasons that are not yet fully clear). I think it is fair to say that the trial results were met with a lukewarm response from sector commentators and experts; it is difficult to assess whether or not the trial outcome points to a material advance in terms of the treatment of TRD versus existing treatment options.

CMPS put out an interesting announcement in December 2022 . The headline of the release referred to the use of COMP360 psilocybin therapy for the treatment of bipolar disorder, but the more intriguing comments are to be found in second half of the announcement. CMPS refers to new data from the Phase 2b trial of COMP360 psilocybin therapy for TRD regarding the mechanisms by which the therapy works. The wording paints a general picture that the therapy part of PAT may not be the primary driver of beneficial patient outcomes.

I have previously written that CMPS has a foot in both the therapy camp and also the drug development/discovery camp in regard to psychedelics. This latest announcement suggests to me that CMPS is deliberately placing more weight on the drug development/discovery aspect by emphasizing the pharmacological action of COMP360 psilocybin – which is a sensible commercial step for CMPS (a drug ought to be easier to patent than a relatively undifferentiated therapeutic method) - but the position being promoted by CMPS runs counter to views held by many others regarding the importance of therapy in PAT treatment protocols. CMPS says that it will investigate the matter further in its Phase 3 Comp360 trials, so we can expect to eventually hear more from the company on this rather controversial topic.

With two of the sector’s big names, MAPS and CMPS, making significant positive announcements in recent months, it is easy to feel optimistic about the future prospects for the psychedelics sector. The sector’s hype machine is still running pretty hard, and negative news flow often fails to get much attention, but Nasdaq-listed Atai Life Sciences ( ATAI ) put out an announcement in early January 2023 that serves as a reminder regarding the risks inherent in investing in the psychedelics space. ATAI is a clinical-stage biopharmaceutical company focused on mental health which makes investments in businesses active in drug development and associated enabling technologies, with a heavy skew towards psychedelics. ATAI’s 06 January 2023 announcement reported that its majority-owned unit Perception Neuroscience's therapy PCN-101 (R-ketamine) had flopped in a Phase 2a trial for treatment of TRD. ATAI has a number of bets on the table, but this was clearly a big one based on the market’s unhappy reaction to the news.

Numinus 1Q23 Result

The vast majority of NUMI’s revenue is generated by the Wellness Clinic operations. NUMI reported a solid increase in client appointments of almost 14% in 1Q23 relative to 4Q22, and the Wellness Clinic operations generated 88% of total group revenue for the quarter.

{kind=link}

Source: NUMI 1Q23 Presentation, slide 12.

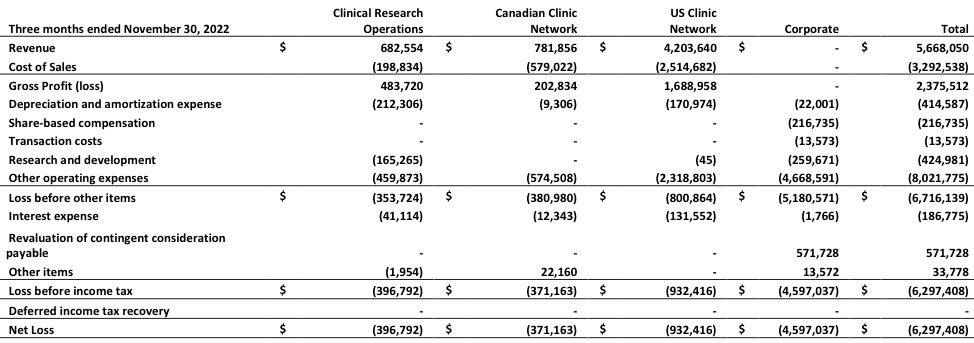

NUMI currently operates 12 Wellness Clinics, 5 of which are in Canada and 7 of which are in the USA. Revenue per clinic is significantly higher for the USA clinics (3.84x Canada average for 1Q23); the USA clinics generated 84% of Wellness Clinic total revenue in 1Q23. Looking at NUMI’s 1Q23 statutory accounts, a quick calculation reveals that the USA clinics are generating a much higher gross profit margin (~40%) than the Canada clinics (~26%). It is unclear if a significant proportion of the difference between the Canada and USA margins is due to business mix, but I am inclined to assume that scale is a factor. The USA clinics also perform better (or less bad!) after other operating expenses are allowed for, with a ‘loss before other items margin’ of around -19% relative to the Canada loss rate of around -49% (author’s calculations).

{kind=link}

Source: NUMI 1Q23 Financial Statements, Note 13.

NUMI’s view is that practitioner recruitment and training is the key to achieving profitability, rather than further clinic footprint expansion. There is insufficient data available to form an opinion as to how realistic management’s view is. Statistics regarding available appointment slots, practitioner availability and utilization will be needed if the market is going to buy in to management’s story.

We firmly believe that recruiting and training practitioners is one of the most important factors in achieving our growth. As having a full roster of practitioners is directly linked to the number of appointments we can offer even more so than the number of clinics we operate. In fact, we're confident that we can reach profitability through our existing network of clinics once we're able to operate these locations at full capacity with full scheduled practitioners to reach clients.

Source: NUMI 1Q23 Transcript, Seeking Alpha , page 4.

An obvious point to highlight on the financials is that the company is making heavy losses. Looking beyond the P&L accounting, the operating cashflow outcome is even worse – NUMI chewed through ~CA$7.1m of cash in 1Q23. Recruiting and training practitioners is a key focus for NUMI, and this is likely to increase cash burn given that such a strategy involves up-front costs and deferred revenue benefits. I comment further on NUMI’s cash flow position below.

In regard to the Clinical Research Operations segment, CEO Payton Nyquvest points to this being NUMI’s highest margin activity.

In total, the CCR team managed clinical trial sites for 14 clinical trials during the first quarter, with a total of 191 clinical trial participants. These services generated $680,000 of revenue during the quarter and an impressive 70.9% gross margin, firmly establishing CCR's clinical trial management as our highest margin activity.

Source: NUMI 1Q23 Transcript, Seeking Alpha, page 4.

Investors and analysts would be well-advised to take the above statement with a healthy pinch of salt. After allowing for expenses that fall outside ‘cost of sales’, Clinical Research Operations was actually the least profitable business segment in terms of margin outcomes in 1Q23.

Patient Finance Offer – Opportunity or Risk?

Over the years, I have seen way too many examples of mis-selling of financial products to consumers. Distribution of financial products via third parties, with the selling group/agent heavily motivated by generous sales commissions, is particularly worrisome in regard to mis-selling risk. I was therefore rather concerned to read that NUMI has effectively become an agent for iFinance .

- On September 13, 2022, Numinus launched a new financing option for clinic patients in Canada. This new payment option will increase the accessibility of its traditional therapy and Ketamine-assisted therapy to a wider client population. Offered through iFinance, a third-party financing partner, Numinus' new financing option will allow Canadian clients to apply for financing with interest rates based on the applicant's credit history. Once approved, Numinus will provide the requested therapy services and collect full payment from iFinance following the completion of the treatment plan.

Source: NUMI 1Q23 MDA, page 4.

When it comes to health matters, it is clearly not desirable for financial constraints to block access to important treatments. An argument can therefore be made that provision of financing plans can improve patient access to medical services. The upsides for the medical provider (NUMI in this case) from offering/promoting patient finance are clear:

- it increases the potential pool of patients,

- financing may allow patients to purchase additional/more expensive services than they otherwise would have been able to afford,

- commission payments (in some form) will be received.

In the area of mental health services, it doesn’t take much imagination to come up with a scenario in which a vulnerable patient finds themselves in financial difficulty after taking out a loan sold to them at precisely the time when their ability to properly asses the risks and benefits of that financial product are likely to be highly compromised. I hope that NUMI have implemented sound governance and risk monitoring procedures to ensure that mis-selling does not occur. The emergence of cases of mis-selling of financing plans could cause quite catastrophic damage to the reputation of NUMI’s wellness clinics.

Of course, we should be mindful that access to financing plans could be vitally important for some patients. In the extreme case of a person suffering from suicidal ideation, accessing finance to fund ketamine-assisted therapy could be the difference between life and death.

Cash Burn

In my view, the key investment issue for NUMI and other listed psychedelics stocks is whether or not the company can stay afloat long enough for PAT to receive regulatory approval, whilst also avoiding massive shareholder dilution from multiple discounted capital raisings. It is therefore vital to pay attention to the company’s balance sheet position and rate of cash burn.

As outlined in my previous NUMI research, I concluded that the company’s view (as per the 3Q22 results management speech) that the group had sufficient cash for “approximately two years” (implying through to ~31 May 2024) was optimistic. Based on the 3Q22 cash and equivalents of almost CA$41.8m, and assuming a quarterly operating cash flow of -$6.1m, back in October 2022, I concluded that NUMI would need to raise fresh capital in early 2023 if the company wanted to maintain a strong financial position (which I aligned with a minimum cash balance of CA$25m).

In the 1Q23 Q&A session, CEO Payton Nyquvest gave the following response to a question regarding cash burn.

Yes, we definitely anticipate that number to continue to trend down. This quarter, in particular, was really about learning -- doing more learning and growing the revenue and profitability side and margin side of the business. But with that, we definitely have identified places where we can continue to reduce the burn rate and while also being able to grow the business at the same time.

Source: NUMI 1Q23 Transcript, Seeking Alpha, page 11.

As at 1Q23 (30 November 2022), NUMI’s cash balance of CA$26.4m was only slightly above my minimum benchmark of CA$25m. The period end cash balance would have been ~CA$0.9m lower at 1Q23 without the exercise of warrants and options. With the share price now trading below CA$0.30, future balance sheet support from the exercising of warrants and options is unlikely to be material. Note 11 of the 1Q23 accounts shows that there were 38.7m warrants on issue as at 30 November 2022, with exercise prices ranging from CA$0.595 to CA$1.785 (weighted average exercise price CA$1.16); of this total of 38.7m, ~11.3m warrants have already expired unexercised. In regard to options, there were 11.4m options on issue as at 30 November 2022, with exercise prices ranging from CA$0.25 to CA$1.25 (weighted average exercise price CA$0.79); of this total of 11.4m, ~2m options have already expired unexercised.

Given the high rate of cash burn observed in 1Q23 (~CA$7.1m at the operating activities level), the CEO’s reference to an anticipated downward trend in cash burn doesn’t provide me with much confidence that the cash burn rate is going to shrink substantially in the near-term. Add in the expectation that warrants and options are unlikely to provide much balance sheet support, and I conclude that NUMI shareholders should be braced for an imminent capital raise.

Conclusion

The improvement in operational metrics for NUMI’s Wellness Clinic operations is positive, but the company has a very long way to go before reaching profitability. There is insufficient data available to confidently estimate the bottom-line benefit of management’s strategy to increase practitioner recruitment and training.

NUMI’s cash burn rate remains high. The balance sheet cash position is rapidly approaching a point at which I think a large capital raise is likely. I therefore downgrade NUMI to SELL.

For further details see:

Numinus Wellness: Cash Burn Concern (Rating Downgrade)