YARIY - NuStar Energy: Stability Improving Finances But No Distribution Increase?

2023-05-08 07:50:40 ET

Summary

- NuStar Energy reported very respectable results that generally show the company's financial stability.

- The company's cash flows did not grow as much as YOY net income performance implies.

- The company's ammonia pipelines are fairly unique in the sector and provide some growth potential due to the strong fundamentals for fertilizer.

- The company maintains a strong balance sheet with very acceptable leverage.

- The 10.54% yield is easily sustainable but it is curious that the company has not increased its payout.

On Thursday, May 4, 2023, crude oil-focused midstream partnership NuStar Energy L.P. ( NS ) announced its first-quarter 2023 earnings results. The market did not seem to be very impressed with these results, as the company's unit price fell a bit in the following trading session:

{kind=link}

However, we did see many of the characteristics that are normally associated with midstream firms reflected in these results. In particular, NuStar Energy showed remarkably stable revenue compared to the prior-year quarter. That was a nice change compared to companies like Energy Transfer ( ET ), whose revenue dropped significantly compared to the equivalent quarter of last year. NuStar Energy also posted year-over-year cash flow growth driven by success in the company's green energy initiatives. It is definitely nice to see these initiatives working out for the company, as NuStar Energy's traditional crude oil-focused operations are unlikely to experience much in the way of growth going forward. The company also offers an interesting way to play the agriculture industry through its ammonia operations which posted fairly strong financial performance during the quarter. Admittedly, as I have pointed out in previous articles, NuStar Energy does not appear to have the same growth prospects as some of its natural gas-focused midstream peers, but the company could still have investment potential due to these ancillary operations and its 10.54% current yield. In fact, that yield alone is enough for the company to be a reasonable investment as investors can generate an acceptable return even without growth.

Earnings Results Analysis

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from NuStar Energy's first-quarter 2023 earnings results:

- NuStar Energy reported total revenue of $393.867 million in the first quarter of 2023. This represents a 3.90% decline over the $409.863 million that the company reported in the prior-year quarter.

- The company reported an operating income of $159.985 million in the most recent quarter. This compares very favorably to the $58.426 million that the company reported in the year-ago quarter.

- NuStar Energy transported an average of 1.325282 million barrels of crude oil per day during the reporting period. This represents a 1.24% increase over the 1.309085 million barrels that the company transported on average during the equivalent quarter of last year.

- The company reported a distributable cash flow of $141.810 million in the current quarter. That represents a 55.74% increase over the $91.058 million that it reported at this time last year.

- NuStar Energy reported a net income of $105.936 million in the first quarter of 2023. This compares very favorably to the $12.312 million that the company reported in the first quarter of 2022.

It seems essentially certain that the first thing that anyone reviewing these highlights will notice is that essentially all measures of financial performance except revenue showed improvements compared to the prior-year quarter. This comes despite the fact that the company's crude oil transported volumes were only up 1.24% year-over-year. However, in the case of net income, this is rather misleading. This is because net income is affected by a variety of things that do not actually reflect the performance of the basic underlying business. For example, in the first quarter, NuStar Energy reported a $41 million gain due to a financing arrangement on its headquarters. This obviously has nothing to do with the company's basic business of moving hydrocarbons over long distances but had a significant impact on the company's net income. In the first quarter of last year, NuStar Energy recorded a charge against its income due to the disposal of a terminal facility in Canada. If we were to exclude these one-off events that are unrelated to basic operations, NuStar Energy would have posted a net income of $65 million in the first quarter of this year compared to $57 million in the first quarter of 2022. This is still a year-over-year improvement, but it is nowhere near as significant as what the company actually reported. This does overall showcase the strength and general stability of NuStar Energy's business model.

In fact, NuStar Energy's CEO Brad Barron reflected on the company's general stability in the earnings press release :

I am pleased to report another strong quarter of financial results where net income, earnings per unit, earnings before interest, taxes, depreciation, and amortization, and distributable cash flow were all up quarter-over-quarter and once again demonstrated the stability and strength of NuStar's assets.

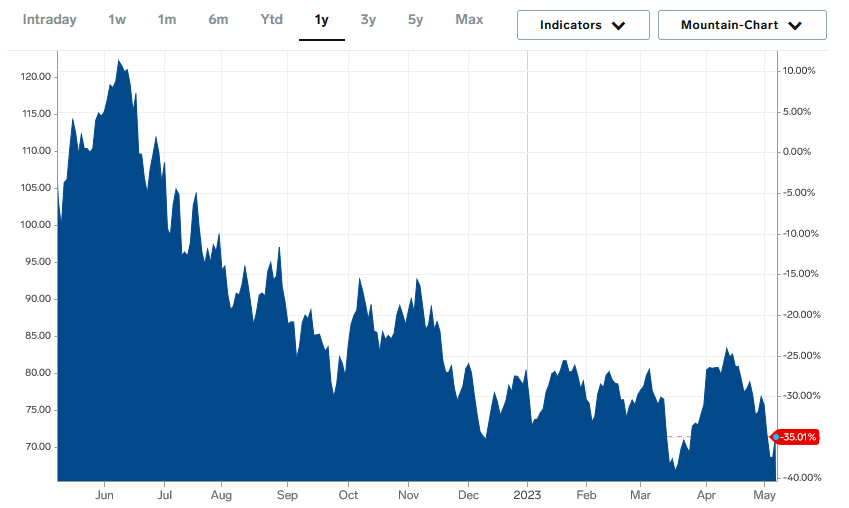

The overall stability is clearly shown in the highlights as revenue and adjusted net income did not vary by very much. Certainly, we do not see as much revenue fluctuation as we saw in peer company Energy Transfer's first quarter results, which were announced last week. This stability comes from NuStar Energy's basic business model. In short, NuStar Energy enters into long-term contracts with its customers under which NuStar Energy transports the customer's hydrocarbon resources through its pipelines from one point to another. In exchange, the customer compensates NuStar Energy based on the total volume of resources that are transported, not on their value. This protects NuStar Energy from fluctuations in energy prices, which is important today as crude oil prices are significantly lower than they were at this time last year:

{kind=link}

As NuStar Energy is compensated based on the volume of resources that are transported, not on their value, the company was not really affected by this. In fact, as we can see above in the highlights, NuStar Energy actually saw its volumes increase compared to the previous year, albeit not by very much.

NuStar Energy did not state precisely why its crude oil volumes were up year-over-year, although the company did state that the Permian Basin and Corpus Christi systems in Texas were responsible for most of the increased volume. According to the Energy Information Administration, the Permian Basin is currently producing significantly more crude oil than it did at this time last year:

U.S. Energy Information Administration

Thus, we can assume that the higher volumes were driven primarily by producers in the region increasing their production. The big question at the moment though is whether or not this will last. As I discussed in a recent article , the national demand for crude oil has begun to decline despite the fact that we are entering the summer months. This is why the price jump that was expected following the substantial production cuts by the Organization of Petroleum Exporting Countries has yet to materialize. The reason for this fall in demand is probably that consumers are cutting back on travel as inflation remains high and the economy is showing signs that it will soon enter a recession.

This reduction in demand puts some pressure on NuStar Energy as it can logically be expected to eventually result in a reduction of transported volumes. This is exactly what happened in the latter half of 2020 as upstream producers cut back on their crude oil production in response to the pandemic-driven lockdowns and an increasing number of people forgoing travel and opting to remain at home. Fortunately, NuStar Energy has a way to protect itself against this. In short, the contracts that the company has with its customers contain minimum volume commitment clauses. These clauses specify a certain minimum volume of resources that the customer must send through NuStar Energy's pipelines or pay for anyway. This provides the partnership with a significant amount of protection against a fall in cash flow that might otherwise accompany a drop in crude oil production. We can see this insulation simply by looking at the company's trailing EBITDA figures:

| FY 2022 |

| FY 2021 |

| FY 2020 |

| EBITDA |

| $722,585 |

| $693,063 |

| 719,082 |

(all figures in millions of U.S. dollars)

The company had an EBITDA of $228.103 million in the first quarter of 2023, which works out to $912.412 million annualized. However, its guidance is for $700 million to $760 million for the full-year 2023 period, which is roughly in line with the company's prior-year numbers while still showing a small amount of growth. Thus, the cash flow stability that we typically appreciate with midstream companies is fully visible here. This is nice because overall stable cash flows provide a great deal of support to the distribution. After all, it is much easier for the company to pay out a significant percentage of its cash flow to the unitholders if it can be relatively confident that its cash flow will be similar during the next period.

Ammonia Business

In the introduction to this article, I stated that NuStar Energy has some opportunities available to it in the agricultural space. This comes from the company's ammonia pipeline system, which is a rather unique business that sets it apart from any other major midstream company. NuStar Energy owns 2,000 miles of ammonia pipelines stretching across much of the Mississippi River Basin:

NuStar Energy

As everyone reading this is likely aware, this is a region that includes much of the American agricultural heartland of the Great Plains. As such, we can quickly see that this network covers many farms and their supporting businesses. This is important because approximately 90% of the world's ammonia production is used in agriculture. In particular, it is a key ingredient in fertilizer and approximately half of the world's food production is dependent on ammonia.

This, therefore, creates an impressive growth opportunity for NuStar Energy. As I have pointed out in various previous articles on farmland investment company Gladstone Land ( LAND ) and fertilizer producer Yara International ( OTCPK:YARIY ), farmers desperately need to increase their yields because the global population is increasing, and the supply of arable farmland is going down. This points to the certainty that fertilizer production will need to increase over the coming years. That will require a growing demand for ammonia, which NuStar Energy is poised to supply. Although the company does not produce ammonia itself, the company's network is the largest ammonia pipeline system in the United States so it seems likely that the partnership will capture some of this business.

NuStar Energy is already moving to exploit this opportunity. From the earnings press release:

Barron closed by highlighting an agreement that was jointly announced by NuStar and OCI Global yesterday that will involve NuStar transporting ammonia on a new segment of its existing 2,000-mile anhydrous ammonia pipeline to OCI's state-of-the-art ammonia products facility in Iowa.

This project is likely to increase the volume of ammonia moving through the company's system overall as an additional supply will be needed to supply this ammonia products facility. NuStar Energy's ammonia business operates under the same basic contractual volume-based business model as the rest of the company's operations, so an increase in volumes should result in an increase in cash flow. Hopefully, this will not be the last of the company's deals for the use of this ammonia transportation infrastructure, particularly considering that the demand for ammonia is almost certain to grow over the coming years.

Financial Considerations

It is always important that we examine the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a business than equity because debt must be repaid at maturity. This is typically accomplished by issuing new debt and using the proceeds to repay the existing debt. That can, naturally, cause a company's interest expenses to increase following the rollover under certain market conditions. As interest rates are currently at the highest level that we have seen since 2007, this is a very real risk today. In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company's cash flows to decline could push it into financial distress. Although midstream companies such as NuStar Energy usually have remarkably stable cash flows, this is still a risk that we should not ignore.

The usual way that we judge a midstream company's debt load is by looking at its leverage ratio. The leverage ratio is also known as the debt-to-EBITDA ratio, which basically tells us how long it would take the company to completely repay its debt if it were to devote all of its pre-tax cash flow to that task. As of March 31, 2023, NuStar Energy had a leverage ratio of 3.46x based on its consolidated debt and trailing twelve-month EBITDA as of that date. This is a very respectable ratio that is a substantial improvement over the 3.98x ratio that it had at the end of the fourth quarter of 2022.

However, as already shown, the company's EBITDA was unusually strong during this quarter and even NuStar's own guidance states that it will probably not be able to reproduce such levels of performance over the rest of this year. Thus, we can expect this ratio to get a bit worse going forward. The company did state that it expects to have less than a 4.0x ratio at the end of 2023 though, and I agree that this is likely to be the case given the company's current budget and cash flows. Wall Street analysts usually consider anything below 5.0x to be acceptable for a midstream company. However, I am more conservative and would like to see this ratio under 4.0x in order to add a margin of safety to our position in the company. As we can see, NuStar Energy appears to be fulfilling this requirement, and as such the company appears to be well-financed. We should not have to worry too much about its debt level.

Distribution Analysis

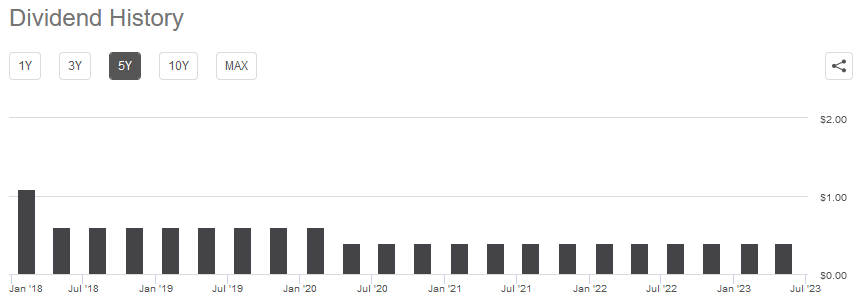

One of the biggest reasons why we invest in midstream companies like NuStar Energy is the high yields that they typically possess. NuStar Energy yields 10.54% at the current price, so it is hardly an exception to this rule. Unfortunately, the company's distribution history leaves a lot to be desired as it has cut its payout twice over the past five years:

{kind=link}

The fact that the company cut its distribution twice in five years is likely to be a turn-off for many income-focused investors. However, many midstream companies reduced their distributions in 2020 in response to the pandemic-driven collapse in oil prices that drove many investors from the market. The market is still not particularly friendly to many of these companies, as I discussed in a recent blog post . Thus, it is important for these companies to internally fund their operations and growth so that they do not have to care how friendly the market is to their capital needs. The fact that NuStar Energy has not made any attempt to raise its distribution like Energy Transfer or Targa Resources ( TRGP ) now that conditions have improved from a few years ago is disappointing, however.

With that said, anyone buying today will receive the current distribution at the current yield and so does not really have to care about the company's past performance. The important thing for anyone buying today is how well the company can maintain the current payout. After all, we do not want to find ourselves the victims of yet another distribution cut as that would reduce our incomes and almost certainly cause the stock price to decline.

The usual method that we use to analyze a midstream company's ability to afford its distribution is looking at its distributable cash flow. Distributable cash flow is a non-GAAP metric that theoretically tells us the amount of cash that was generated by a company's business operations and is available to be distributed to limited partners. In the first quarter of 2023, NuStar Energy reported a distributable cash flow of $141.810 million. That was sufficient to cover its distribution 3.19 times over. This is easily one of the highest coverage ratios in the midstream sector and it is well above the 1.20x ratio that Wall Street analysts usually consider to be sustainable. The fact that NuStar Energy has not increased its distribution is confusing and disappointing in this light, as it can clearly afford to. At least it appears that we do not have to worry about another distribution cut.

Conclusion

In conclusion, NuStar Energy posted respectable results during the first quarter of 2023 that show the company's general stability. The company unfortunately does not have the growth potential of some of its peers, but its yield more than makes up for that. In fact, the combination of high cash flow and a strong balance sheet makes it rather confusing that the company has not hiked its distribution recently as some of its peers have begun to. The company is still worth buying though as the current yield appears sustainable and is sufficient to provide an acceptable return even without growth. Its unique ammonia business offers some diversity to an energy-income portfolio as well.

For further details see:

NuStar Energy: Stability, Improving Finances, But No Distribution Increase?