NAD - Nuveen Quality Muni Income Fund: The Pain May Be Over Soon

2023-06-02 18:54:43 ET

Summary

- Leveraged closed-end bond funds have faced challenges in the past year due to rising interest rates, with the Nuveen Quality Municipal Income Fund experiencing a total return of around -10%.

- The spread between bond yields and the cost of leverage is starting to widen again, which could lead to increased fund income and dividend increases for NAD.

- Nuveen's conservative management approach and the potential end of the interest rate hiking cycle could make NAD a good investment opportunity.

Tough Year For Leveraged Funds

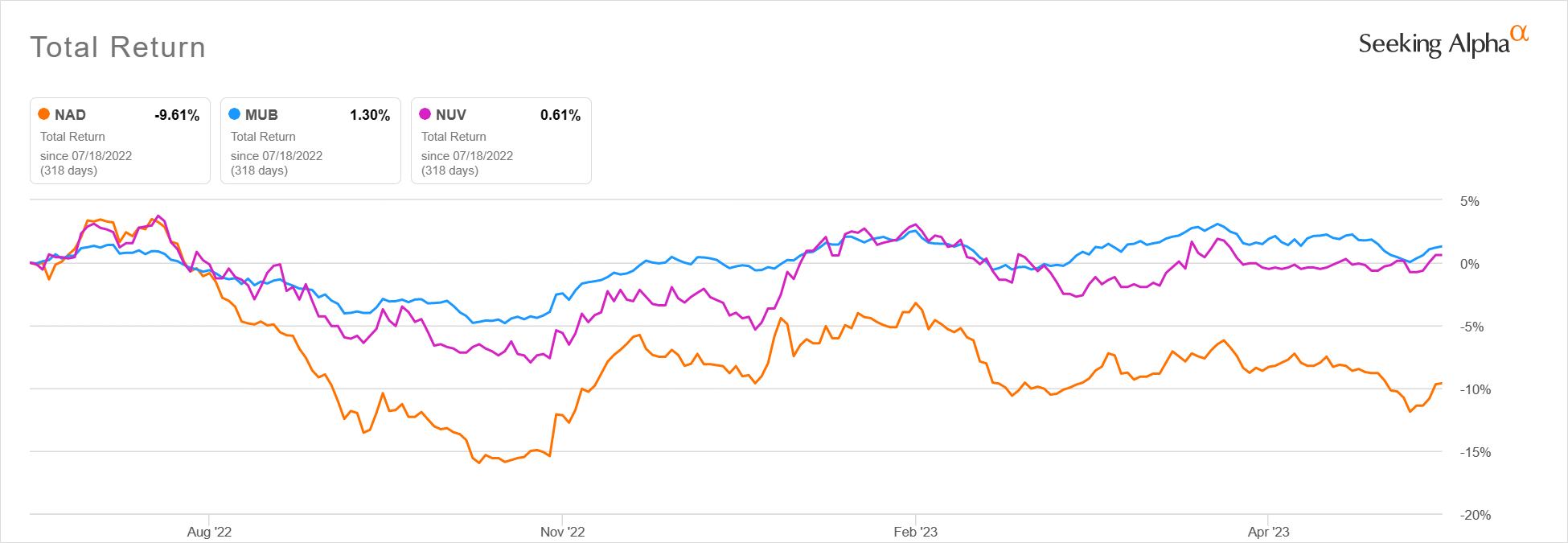

The rising interest rate environment has been a major headwind for leveraged closed end bond funds in the past year. The Nuveen Quality Municipal Income Fund ( NAD ), which I last covered in July 2022 , has been no exception. Total return since then has been in the neighborhood of -10%, compared to a slight positive for the low-leverage Nuveen Municipal Value Fund ( NUV ) or the unleveraged iShares National Muni Bond ETF ( MUB ).

{kind=link}

NAD is one of several closed-end muni bond funds operated by Nuveen. This fund consists of high credit quality municipal bonds, with 2/3 of the holdings rated A or better. The fund has a long average maturity of 18.15 years and a leverage adjusted duration of 13.74 years. You can see these and other characteristics of the fund on Nuveen's fund-specific website . The fund creates leverage by selling variable rate preferred shares and using the proceeds to finance some of its bond purchases.

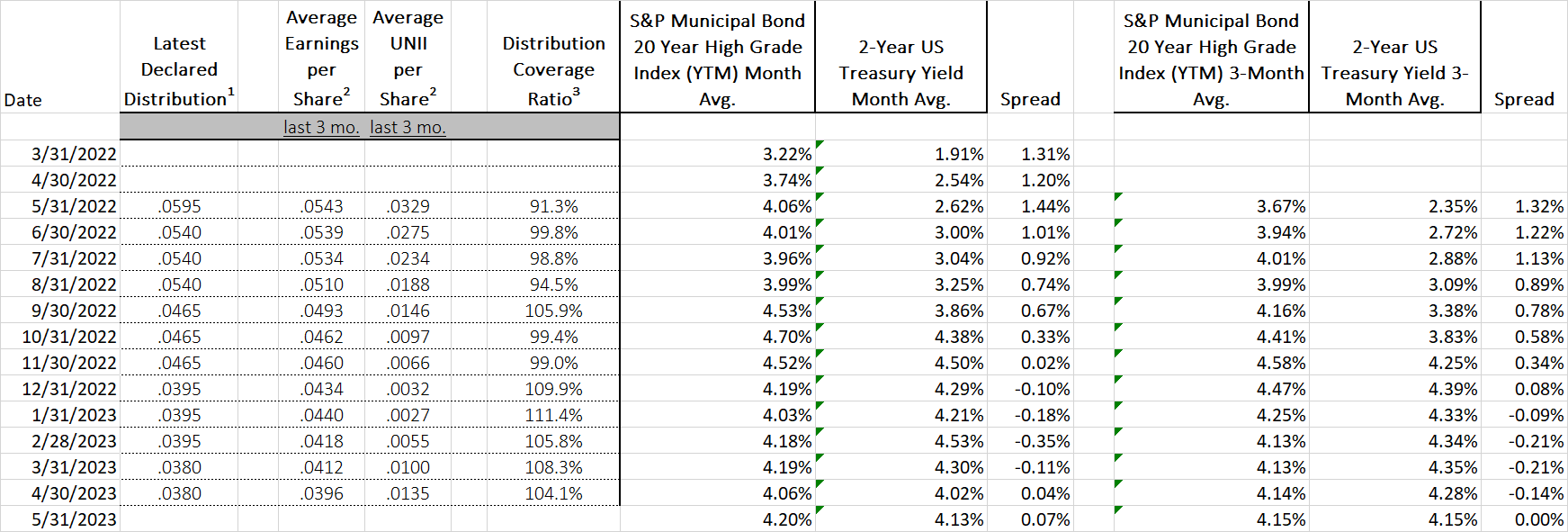

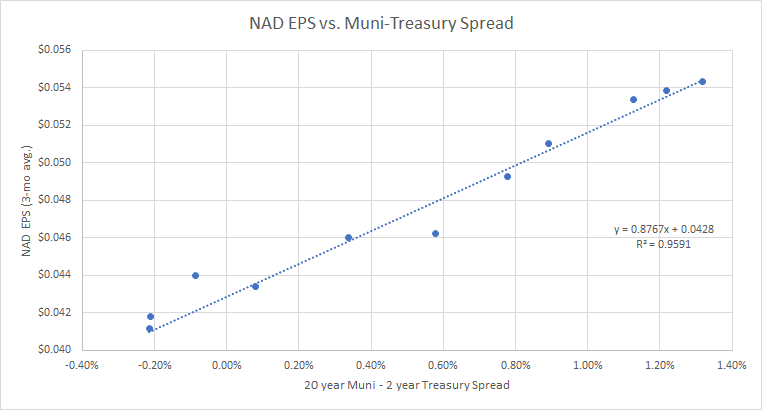

The higher interest rate environment, as well as the narrowing spread between the fund's holdings and the preferred shares, have resulted in declining monthly income over the past year. Nuveen has a conservative distribution policy and tries to avoid overpaying the monthly dividend. This has resulted in a dividend cut each quarter of the past year. The fund's income correlates well with the spread between two readily available indices. The S&P Municipal Bond 20-Year High Grade Index is a good proxy for the fund's holdings, while the 2-year US Treasury note yield is a close match to the fund's cost of leverage.

Author Spreadsheet (Data sources: Nuveen, S&P, and US Treasury)

{kind=link}

{kind=link}

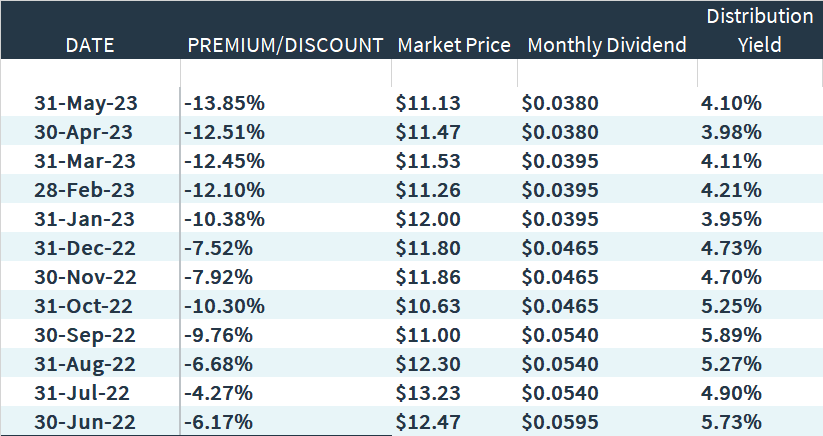

In addition to the declining income, NAD's market price has been subjected to a widening discount to net asset value over the past year. The discount is now barely off its worst levels of the year, -14.76% on 5/24/2023.

{kind=link}

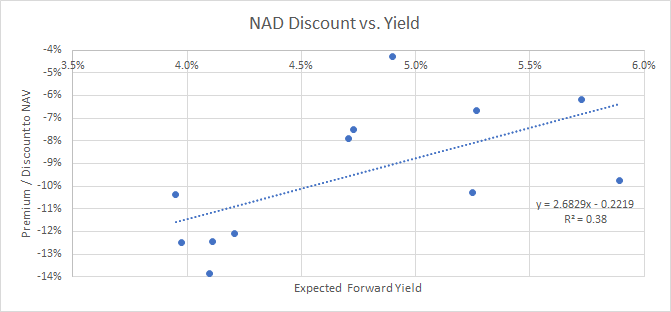

I showed in my last article that the discount to NAV relates closely to the dividend yield of the fund. For similar funds, lower yields translate to wider discount. Looking at a single fund over time, this relationship holds but is not as tight of a correlation, indicating other factors are in play as well.

{kind=link}

Looking only through the rearview mirror, NAD and other closed end funds look like a bad bet, with declining payouts and negative market sentiment hitting the share price even as NAV is stabilizing. The data suggest we may be hitting a bottom, however.

Why A Turnaround Is In Order

The spread between bond yields and cost of leverage is starting to widen again

If we look at the first table above, we see that this spread actually turned negative between January and April, bottoming in February and March (on a trailing 3-month average basis). With the spread around zero, leverage is ineffective at boosting the fund's income. In fact, we see that NAD has decreased effective leverage from 42.56% on 10/31/2022 to 39.87% on 4/30/2023. As of May, the spread is back to zero. While we have yet not seen the fund's income results for May, I would expect them to tick back up above the $0.04 level.

Looking forward, Fed Funds rate increases appear to be nearing an end. The CME FedWatch tool predicts only a 1/3 chance of a 0.25% rate increase at the June meeting, despite strong employment numbers and inflation still running warm. The FedWatch tool does currently predict the most likely rate outcome of the July and September meetings in the 5.25%-5.50% range, followed by nearly one 0.25% rate cut per meeting through the end of 2024. The 2-year Treasury yield matches well with the expected average Fed Funds rate over that period, so I expect the cost of leverage to follow it lower.

As for the yields of the fund's holdings, the average coupon is now 4.08%, about in line with the S&P 20-year muni bond index yield. Bonds that are maturing can therefore be replaced with new bonds at a similar yield. The long average maturity of the fund should keep this stable, with only 13% of the fund's holdings maturing in the next 9 years.

Nuveen's preference to keep UNII low should result in a dividend increase when income allows it

Unlike some fund operators, Nuveen does not focus on a stable dividend but is willing to change it quarterly to match fund income. Over the last year, this has resulted in cuts, but in the past, the fund has also increased payouts frequently when it has the income. For example, the fund ramped up dividends following the 2008 financial crisis and 2020 Covid crash.

{kind=link}

If we do see an increase in fund income for May, I would expect the dividend to increase as soon as the August 1 pay date.

If I'm wrong, and the spread between bond yields and cost of leverage stays around zero, the fund has the option to continue reducing leverage

The fund is financed by several types of preferred shares (sold by private placement and not publicly traded) which are described in Note 5 of the Annual Report . These shares are redeemable at the option of the fund, although some types require payment of a premium if redeemed. When the spread is near zero, Nuveen can redeem preferred shares with proceeds of maturing bonds at little overall impact to the net income of the fund. While the fund's long average maturity limits the pace of deleveraging, this option is at least a mitigating factor if leverage costs stay high. The fund can also issue common shares for cash to delever, but this would be unattractive with the fund trading at a steep discount.

Conclusion

NAD has suffered dividend cuts and widening discounts over the past year thanks to the increasing interest rate environment and narrowing spread between bond yields and cost of leverage. With this spread possibly bottoming, fund net income should increase, followed shortly by dividend increases. Nuveen's conservative management that causes them to cut dividends regularly as income drops should operate in reverse when it increases. This usually also leads to an improvement in the discount to NAV. NAD is a way to play the end of the interest rate hiking cycle, partially mitigated by the ability to deleverage if it does not happen as expected.

For further details see:

Nuveen Quality Muni Income Fund: The Pain May Be Over Soon