UTG - NXG: Attractive Distribution Doubled Deep Discount And An Interesting Portfolio

2023-09-01 12:52:33 ET

Summary

- Energy and renewables, as well as REITs and utilities, have been under pressure this year, affecting NXG NextGen Infrastructure Income Fund.

- The fund has announced a doubling of its distribution to try to narrow the discount and attract investors.

- The fund's portfolio is focused on a mix of energy and renewables, with a significant weighting towards energy and top holdings in sustainable infrastructure companies.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Energy and renewables have both been under pressure this year, in addition to real estate investment trusts ("REITs") and utilities also being under pressure due to rising rates and yields. This has put pressure on closed-end fund ("CEF") NXG NextGen Infrastructure Income Fund ( NXG ) since our last update, where some sizeable losses, even on a total return basis, have taken place.

NXG Performance Since Prior Update (Seeking Alpha)

The discount during this time has even narrowed a touch, which would have been a positive to contribute to limiting some losses. Still, as long as energy and power are needed in the world, the underlying portfolio can remain viable. The discount remains attractive, which also can make it a more compelling choice in the infrastructure space.

When I originally wrote this article, it was prior to the increased distribution, so I've updated it where appropriate.

To get this discount to narrow, the fund has doubled the distribution being paid out. Taking it from $0.27 per month to $0.54.

NXG Distribution Increase (NXG Investment Press Release)

This is something that had worked for its sister fund, NXG Cushing Midstream Energy Fund ( SRV ) previously.

The Basics

- 1-Year Z-score: 0.86

- Discount: -20.67%

- Distribution Yield: 18%

- Expense Ratio: 1.94%

- Leverage: 25.91%

- Managed Assets: $148 million

- Structure: Perpetual.

NXG will "seek high total return with an emphasis on current income." To achieve that objective, the fund will

"invest at least 80% of its net assets, plus any borrowings for investment purposes, in a portfolio of equity and debt securities of infrastructure companies, including: [i] energy infrastructure companies, [ii] industrial infrastructure companies, [iii] sustainable infrastructure companies, and [iv] technology and communication infrastructure companies. The Fund will invest no more than 25% of its Managed Assets in securities of energy master limited partnerships ("MLPs")."

The fund is fairly small, and the fund's expense ratio is high. These are certainly two negatives of the fund that should be considered before investing. The advisory fee is 1.25%, above the standard 1%. However, the Board has implemented an approval for a 0.25% waiver, so it brings it down to at least the industry standard.

The fund is leveraged, though they've decreased their outstanding total borrowings. That being said, the fund has had to deal with higher interest rates just as any other leveraged fund, causing borrowing costs to rise sharply. That is what pushes the fund's total expense ratio to 4%, as of their latest report.

Performance - Deep Discount

This is a very different fund from most infrastructure funds, especially the more popular ones, Reaves Utility Income Trust ( UTG ) and Cohen & Steers Infrastructure Fund ( UTF ). NXG is more heavily invested in a mixture of energy and renewables.

The fund was a more pure-play energy fund prior to 2020, which is one of the reasons why it did much more poorly through most of the period prior to that. That's one of the main reasons why the fund has produced negative total returns in the last decade.

Ycharts

However, if we look at the period since the Covid rebound to today, we see a very different picture. Energy had a stronger performance relative to what could be called these more traditional infrastructure plays.

Ycharts

It transitioned after the Covid collapse to be a more diverse infrastructure play that has incorporated a more renewable energy focus. With such ugly results during Covid, there is little to be enthusiastic about.

That being said, if there is a single victory that can be claimed there, it was that they had actually deleveraged down to nothing heading into Covid and then were able to add leverage to their portfolio while everything was beaten down. We highlighted the benefit of this relative to other energy funds in our prior update .

This could be something to continue watching going forward because they've been reducing their borrowings once again. At the end of fiscal 2021, they had $56.41 million, then took that down to $41.41 million by the end of fiscal 2022. Now, with the latest semi-annual report for the six months ended May 31st, 2023, leverage has been taken down to $33.91 million.

Today, the fund's discount remains deep and attractive for an investor willing to take a more speculative bet on this type of exposure. The fund's discount remains well below its longer-term average. Though at the time of writing on the news of a doubling of the distribution, we are expecting this discount to narrow materially after the close.

Ycharts

Then again, considering the fund's transition in 2020, it could be more appropriate to look at that period. When doing that, it would suggest a wider discount is going to be the norm.

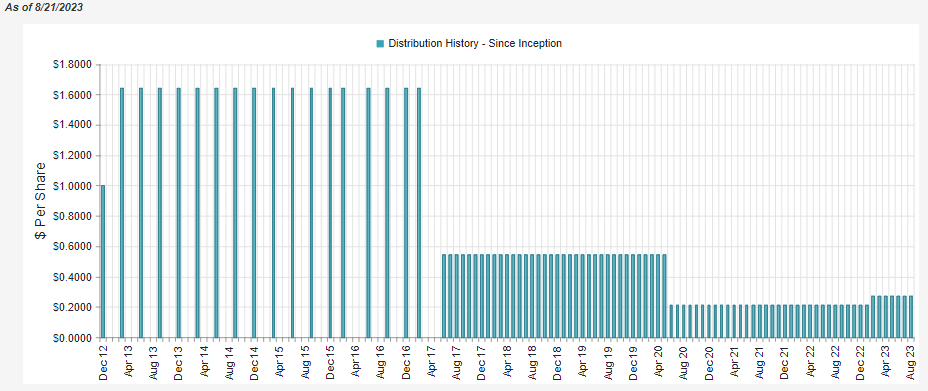

Distribution - Doubled Payout

Just like most energy funds in 2020, they slashed their payout. They have increased it modestly once since then but have otherwise kept it to a fairly modest level. However, they have now recently doubled it with their latest announcement, taking it to a distribution rate of 16.91%. On an NAV basis, it works out to 14.20%. The distribution hike is so hot off the presses that the chart below hasn't had time to update yet.

NXG Distribution History (CEFConnect)

{kind=link}

With energy funds, they will tend to carry significant master limited partnership ("MLP") exposure. In the case of NXG, they specify that it won't be over 25%. Well, this is actually for regulatory reasons because they want to qualify as a regulated investment company or RIC, which means they can't hold more than 25% in MLPs to qualify.

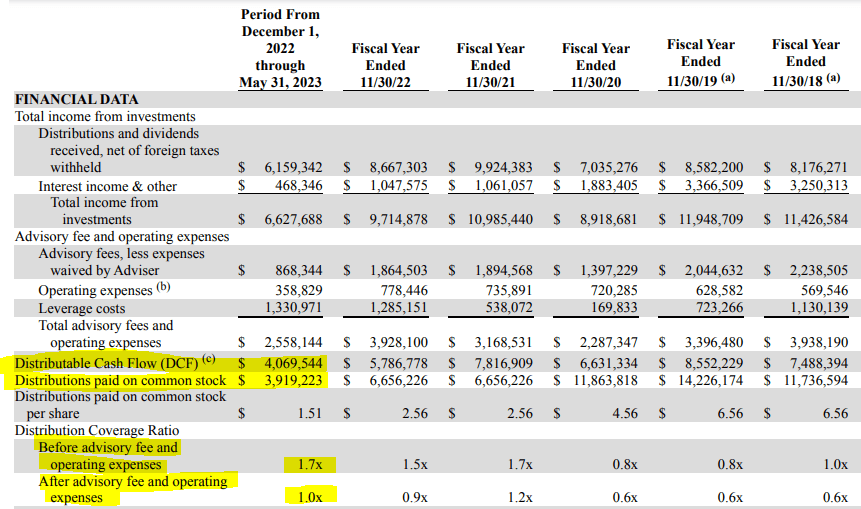

However, holding energy investments has an important distinction over other closed-end funds, where we typically look at net investment income or NII. This is because NII is reduced by return of capital distributions that are naturally generated from partnerships. Therefore, we look at distributable cash flow, a metric that investors in the MLP space are probably quite familiar with but could be new to some closed-end fund investors.

Lucky us, NXG provides the figure for us (though it is a rather easy calculation to come up with if we had to on our own as it's simply NII plus the ROC distributions added back in.) NXG provides a breakdown of discounted cash flow, or DCF, coverage on two different metrics, without and with the expenses of the fund. As we can see, DCF, with the expenses factored in, provides coverage at 1x. Given that the fund is an equity fund, seeing DCF coverage at 1x or greater is really all we are looking for. This coverage has also increased since the last fiscal year-end.

NXG DCF From Semi-Annual Report (NXG Investment (highlights from author))

{kind=link}

This is because we could expect that the fund could see some appreciation in its portfolio over the long term, which would provide capital gains to the fund, which could also be utilized in the payout for shareholders. The fund also utilizes options that can contribute to realized gains for the fund as well. In the last report, they realized gains of ~$473k in the last six months.

Given these coverage metrics of the old distribution, it would show us that the fund will be coming in short of coverage by about half due to the payout being doubled. At least, DCF will be at about half. The remainder could be made up with capital gains, but that isn't guaranteed to happen. That being said, that also isn't that uncommon for equity-focused funds that regularly rely on capital gains in order to have their distribution covered. This just happens now to carry a 14.2% NAV rate which seems to be a high hurdle to achieve. At the same time, we should see the discount narrow materially if history is any guide.

For 2022, the entire distribution was classified as return of capital. This can be for multiple reasons beyond just the fact that the fund receives tons of ROC distributions from its underlying holdings. The fund had sizeable carry forward capital losses from prior years and still has some left as of its last annual report .

NXG's Portfolio

The managers in this fund are incredibly busy, with the latest turnover at 94.82%, which is stated as being NOT annualized. At this pace, we would see higher turnover than in 2022, when it was at 124.56% and in 2021, when turnover came to 125.8%. Those were much higher than the 71.35% it reported in 2020, the year it made the transition to become a more broadly diversified infrastructure fund and shifted its focus.

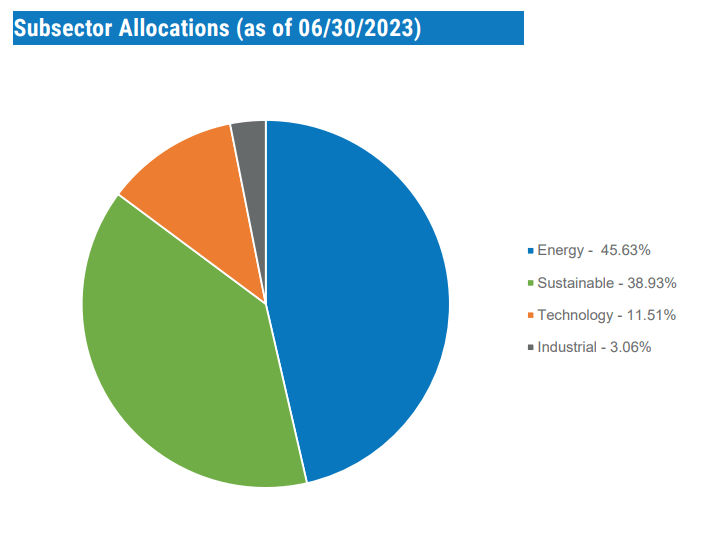

One area that has remained a material focus on the fund is the energy exposure though. This remains the case today with a nearly 46% weighting to energy.

NXG Sector Allocation (NXG Investment)

{kind=link}

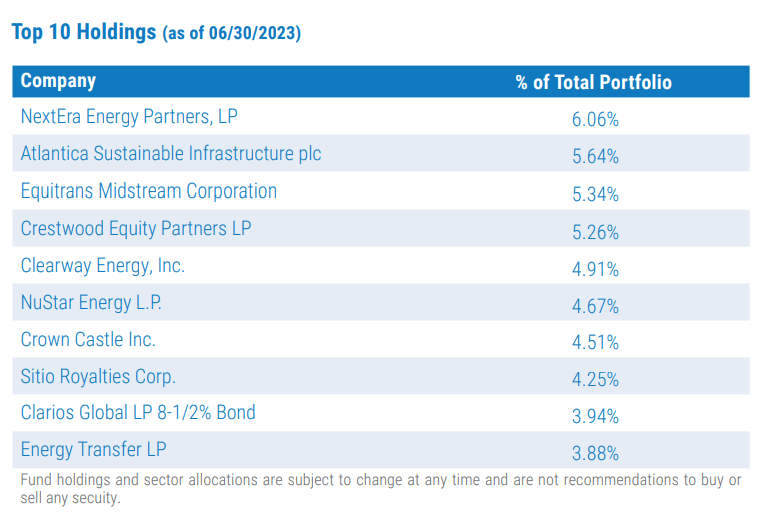

This is fairly represented in the fund's top ten holdings. However, the "sustainable" category is also substantial. Some of these sustainable names are actually the fund's largest holdings, with an allocation to NextEra Energy Partners ( NEP ) as its top position and Atlantica Sustainable Infrastructure plc ( AY ). It also has Clearway Energy ( CWEN ) in a top spot as well.

NXG Top Ten Holdings (NXG Investment)

{kind=link}

Equitrans Midstream Corp ( ETRN ) is a more traditional pipeline infrastructure play, as is Crestwood Equity Partners ( CEQP ). CEQP is currently the target of being acquired by Energy Transfer ( ET ) in an all-stock deal , which could see NXG's ET position grow.

Crown Castle ( CCI ) also makes an appearance in NXG's top ten positions, which highlights they are willing to incorporate REITs into their portfolio as well. This is actually fairly common in other infrastructure funds as well.

In the last year, energy hasn't been too strong of a performer, but renewables have been much worse. In fact, NEP is down nearly 50% in the last year. This is one that I've personally invested in, added lower and even sold puts at a much higher strike price. So I've certainly been acutely aware of the deteriorating unit price. It isn't alone, though, as AY and CWEN aren't showing trajectories that are too dissimilar.

Ycharts

However, I believe that NEP is incredibly undervalued - even if it could be a more speculative position. Higher interest rates, low unit prices that limit the capital raised through new issuances, and even some investors' thoughts that subsidies for renewables could come under pressure are things to consider. At this point, subsidies have been trending higher , but if the political environment changes and subsidies slow down, that could impact the growth that renewables have been benefiting from.

With all that being said, I believe that not only do we see NXG trade at a deep discount, but then several of its largest holdings are also trading at attractive valuations.

Conclusion

NXG NextGen Infrastructure Income Fund is trading at a deep discount, and it remains an interesting investment choice for a portfolio that is split between traditional and renewable energy. This is a fund that can very much take advantage of the energy transition but also take advantage of investing in the old trusty fossil fuel plays as well. The fund has had a rough history, and most of that is due to its energy exposure. However, NXG seems to continue to present a long-term opportunity for those willing to take a risk. As long as power is needed for society to function, then most of NXG's underlying portfolio should remain viable and critical long-term infrastructure to accomplish that.

Thanks to the large discount on the fund's shares and now a doubling of the distribution, that should really pique investors' interest to realize some of this discount. With the last report, the fund's DCF also showed a fully covered distribution, but that should be roughly cut in half now in terms of DCF. The rest would have to be made up from capital gains in the underlying portfolio.

Is the new payout sustainable? I'd say it's very unlikely, given the high NAV rate hurdle. That being said, it could still be viewed as the right thing to do for investors to realize this massive and lingering discount.

For further details see:

NXG: Attractive Distribution Doubled, Deep Discount And An Interesting Portfolio