SBRA - Office Properties: Merger Update With Diversified Healthcare And Q2-2023 Results

2023-07-27 17:40:38 ET

Summary

- We last covered Diversified Healthcare Trust after it had a huge rally and investors were hoping for more.

- That potential merger has been heavily contested for a few reasons.

- We look at the Q2-2023 of OPI and highlight liquidity concerns on both sides of this merger.

- We end with our verdict on both securities.

When we last covered Office Properties Income Trust Inc. ( OPI ) and Diversified Healthcare Trust Inc. ( DHC ) we suggested that the $9.00 net asset value or NAV that Flat Footed LLC assigned to DHC was likely far from reality. Our best trade was to use the high price of DHC to head for the exits.

If we value the SHOP segment at 12X Q1-2023 NOI (annualized) of $70 million, we get that segment valued at $840 million. That is a cool $2.1 billion lower than what is shown. Then the net asset value drops from $2,189.5 shown to $89.5 million or less than 40 cents a share. Of course, we are not remotely claiming that our valuation is right, but using that expected $210 million 2024 EBITDA is a reach. We think the current rally in DHC should be sold.

Source: Is It Actually Worth Over $9.00?

Since then DHC has moved about 20% lower and OPI is pretty much unchanged.

We update our thesis with key developments from both sides.

OPI Q2-2023

The main press release numbers looked good at first sight.

{kind=link}

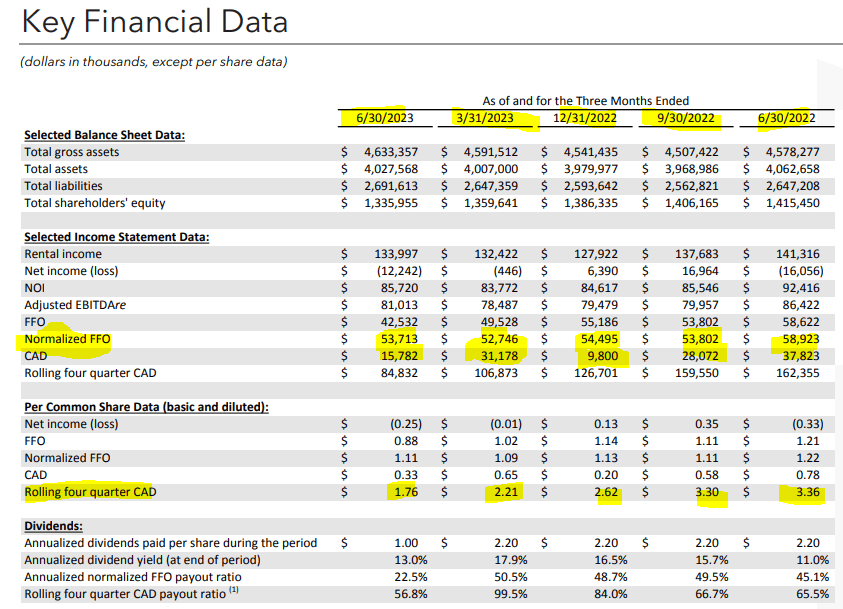

Normalized funds from operations or FFO came in at $1.11 for the quarter and one does not need a calculator to figure out that OPI is trading at less than 2X annualized FFO. The company also boosted its occupancy levels year over year and the presentation highlighted how things were going to exceed expectations.

OPI Q2-2023 Presentation

Upon closer look at the financials though, we can see several issues with OPI. The normalized FFO appears to have stabilized over the last four quarters but the cash available for distribution continues to be in a free fall. That number is almost 50% lower and has dropped from $3.36 to $1.76 on a rolling 4-quarter basis.

{kind=link}

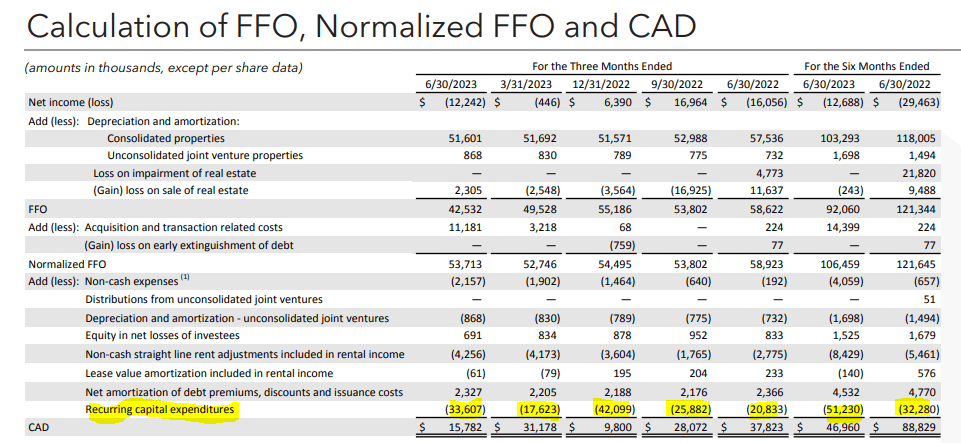

The differential here is what OPI classifies as recurring capital expenditures. That number has been quite firm though variable, and this quarter was almost two-thirds of the total normalized FFO.

{kind=link}

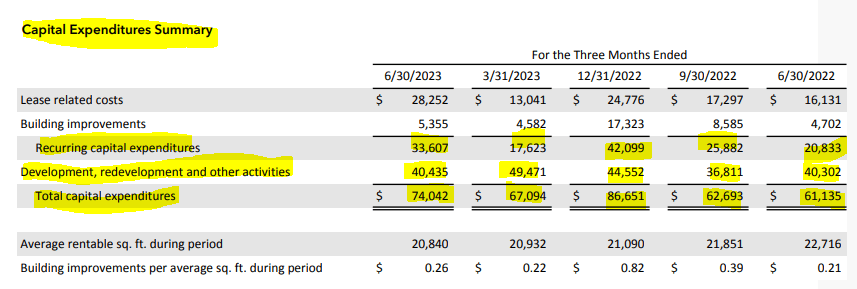

There are two dimensions to this. The first being that office properties is a tenant's market. They can and do demand rather big concessions to keep staying in the leased space. Recurring capex has crept up over time. The second aspect is of course inflation. As the landlord conducting these expenditures, OPI is fully exposed to the higher costs over time. But the high costs of recurring capital expenditures is not where OPI's troubles end. Total capital expenditures now dwarf FFO and by a pretty huge margin. Last quarter total capital expenditures were 138% of the normalized FFO.

{kind=link}

Still think it is cheap?

Refinancing A Big Issue

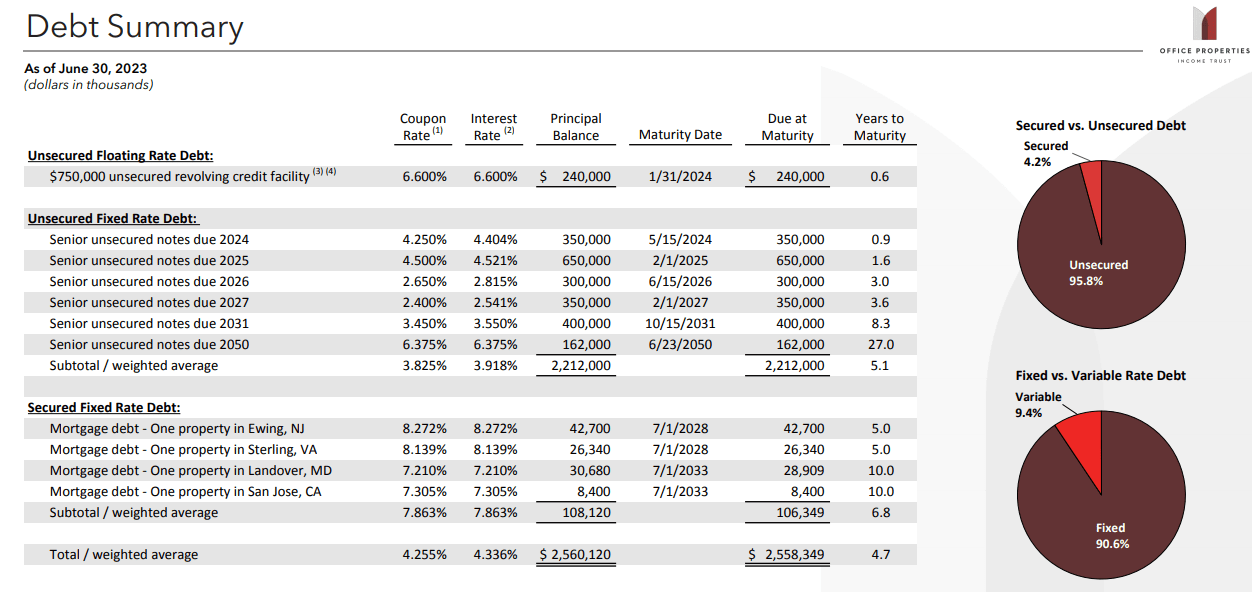

Keeping in mind that OPI produces no realistic free cash flow (as defined by FFO minus total capital expenditures) and is still paying a rather hefty dividend, let us look at the debt maturity schedule. The unsecured floating rate debt was just extended by six months as OPI exercised its option to do so. The rate on that will go up with the latest Fed hike.

{kind=link}

In the next 18 months, $1.25 billion comes due. Whatever you may believe or not believe about OPI's financial health, you have to know that the unsecured notes will not be reissued at anywhere close to those 4.4% yields. In fact, the 2025's are trading at over a 12.5% yield to maturity.

{kind=link}

If we plug in even 9% into the entire capital structure, the entire FFO goes negative. This negative FFO will be before dividends, and before any capital expenditure. So if you want to love the 2X FFO multiple, there is your reason not to. For this same reason we would be very cautious with Office Properties Income Trust 6.375% NT 50 ( OPINL ). The yield looks juicy, but it will likely go to way lower than the current price.

DHC

One new piece of information on DHC was their event of default under their credit agreement.

DHC today announced that a non-monetary event of default has occurred under its $450 million credit facility. The facility requires DHC to maintain collateral properties with an aggregate appraised value of at least $1.09 billion. The facility allows the facility's administrative agent to periodically reappraise the collateral properties and, on June 23, 2023, the administrative agent notified DHC that the reappraised value of the 61 medical office and life science properties securing the facility had declined from $1.34 billion to $1.05 billion, below the $1.09 billion threshold required under the facility. The appraised values of the collateral properties securing the facility declined 22% since they were last appraised in January 2021.

DHC is currently negotiating a limited waiver with the requisite lenders under the facility to waive the event of default through September 30, 2023, the outside closing date for DHC's pending merger with Office Properties Income Trust, at which time DHC's $450 million credit facility will be fully refinanced.

Because DHC is not currently in compliance, and it has not been in compliance for over two years, with its debt incurrence covenants, DHC cannot issue any new debt or refinance expiring debt.

Source: Seeking Alpha (emphasis ours)

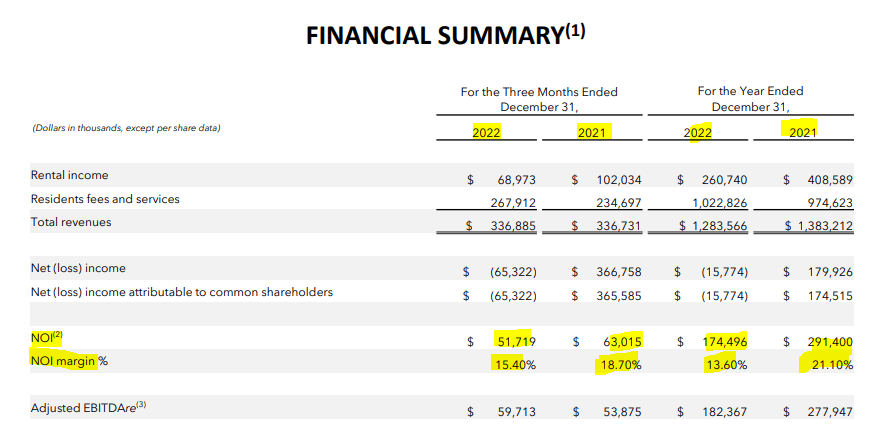

This default flies in the face of the $9.00 NAV as suggested by Flat Footed LLC. Some investors may reject this NAV drop, but this is about what we have seen for many REITs. For example according to S&P Global, Sabra Health Care REIT's ( SBRA ) analyst estimated NAV has dropped 20% over the last 18 months. While we cannot do a property by property assessment for DHC's collateral list, just have a look at the overall cash flow per share.

Some of this was obviously driven by interest expenses increasing. Yes, we agree. But just look at their net operating income or NOI and NOI margin, which are not impacted by interest expenses.

{kind=link}

That looks pretty straightforward here to us. The properties are likely worth a lot less today than what they were more than two years back.

How To Play

The current bull thesis on OPI is based on the low FFO multiple. As we showed above, that is misleading, and we think the company is ultimately going a lot lower as a stand-alone entity. On the merger front, there is significant opposition to The RMR Group Inc. ( RMR ) carrying this out. See the related SEC filing here . Clearly, some big shareholders don't think DHC merging with OPI is a good thing. We are agnostic on that front. Even if the merger with DHC succeeds, it will buy OPI just a little extra time. But we don't see DHC as so radically undervalued as to make a bull case for OPI.

On the DHC front, we had suggested investors hit the exits as there was no realistic scenario where DHC could justify that high a price. It was trading at a 100% plus premium to the OPI buyout price and also at a premium to consensus NAV. With the big drop since the last article, we are still at a premium to the OPI merger price, but less so. The price has now moved below consensus NAV. We still see big risks to the bull thesis here. Some less exuberant investors have gravitated towards Diversified Healthcare Trust 6.25% SR NT 46 ( DHCNL ). Those long-dated baby bonds look quite dangerous to us. We think the best play would be the medium-term notes if you are bullish.

{kind=link}

With a near 12% yield to maturity, you have a very good chance of at least breaking even if things go further south. Even in a default, your recovery odds with the underlying asset base should be quite high.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Office Properties: Merger Update With Diversified Healthcare And Q2-2023 Results