ORI - Old Republic International: No Flash Just Cash

2023-09-22 11:00:00 ET

Summary

- Old Republic International Corporation has a 42-year history of raising dividends and 82 years of consecutive payments.

- The company has returned $492 million to its shareholders in the 1H of '23 between dividends & buybacks.

- The insurance segment has outperformed the overall market in the last 1, 3, and 5-year periods.

- Old Republic International has experienced insider buying in recent months while peers have seen insider selling.

Introduction

During times of uncertainty and a looming recession expected in 2024, investors need stocks that will provide stable income in their portfolios. While bonds and T-bills may provide this currently, this will not last long as rates will decline eventually. When? That I don't know. Sometime in 2024 is my thought, but maybe in 2025. People talk about how rates were high in the '70s and '80s and how they climbed to nearly 20% in 1981. And while the FED did this to kill inflation, it sparked the recession of the early '80s. Maybe that will happen again, but all of this is speculation.

What we can do is navigate it as best as we can, by diversifying, and investing in solid stocks like Old Republic International Corporation ( ORI ). I've mentioned previously how I classify my dividend stocks. Stabilizers, growers, and showers. ORI is what I call a stabilizer. Modest growth. No huge earnings or revenue beats. Just stable income with low growth quarter after quarter, year after year. No flash, just cash!

I actually saw that line in the comments from a reader, and it instantly jumped out at me as it described ORI perfectly. So I decided to dedicate an article to the insurance oldie, but goodie. To some, these are too boring, but I enjoy boring, predictable stocks. I look at them as an employee. Would you want an employee who's on fire one day, then cold the next? Or that employee that shows up to work on time, does what's required of them, and repeats this on the daily? I know my answer and that's how I view ORI, dependable & reliable.

Who Is ORI?

Most of us are required to pay some type of insurance and will do so for the rest of our lives. But many are not familiar with this stock or have a complete grasp of how insurance companies operate. ORI engages in the insurance underwriting and related services business primarily in the U.S. & Canada. It's easy for insurance stocks to get lost in this market, although they're a very important part of our everyday life. It also happens to be one of the nation's largest insurance businesses and has been around for a century.

Some people call it old reliable and I couldn't agree more. Any company that's been around that long has to be reliable. It's not an easy task for any business no matter the sector to last that long. So they must be doing something right. They recently announced the formation of a new company , ORI Accident & Health, Inc. This is their sixth new company in the last 8 years. This is expected to expand their expertise and will focus on providing specialized coverages like employee stop loss.

No Flash

One thing I like about ORI is that it flies under the radar like many other insurance stocks. Many of them are not flashy like new A.I. or tech stocks. I remember telling a co-worker about Aflac Incorporated ( AFL ) and he replied, "They're still around?" Most of us remember the commercials as kids with the duck saying "Aflacccccc." The fact of the matter is they're still around and airing today. But a lot of people don't pay attention to them, or think about the business aspect of these companies and how integral they are to our everyday lives.

Insurance companies are some of the most boring, yet stable businesses. And a lot of them also pay dividends to their shareholders. These typically outperform the market over the long term. The industry as a whole outperforms the market over the 1- & 3-year periods and is in line over a 5-year period. Furthermore, ORI beats both the industry and overall market in the 1, 3, and 5-year periods. Not bad for a boring stock, right?

{kind=link}

Growing Dividend

This wouldn't be a Dividend Collectuh article without me mentioning the dividend, right? They recently raised the dividend earlier this year by 6.5% to $0.245 from the prior $0.2430. Again ORI is not going to knock your socks off with its dividend hikes. But one thing you can count on is a raise. And in this environment, I'll take it.

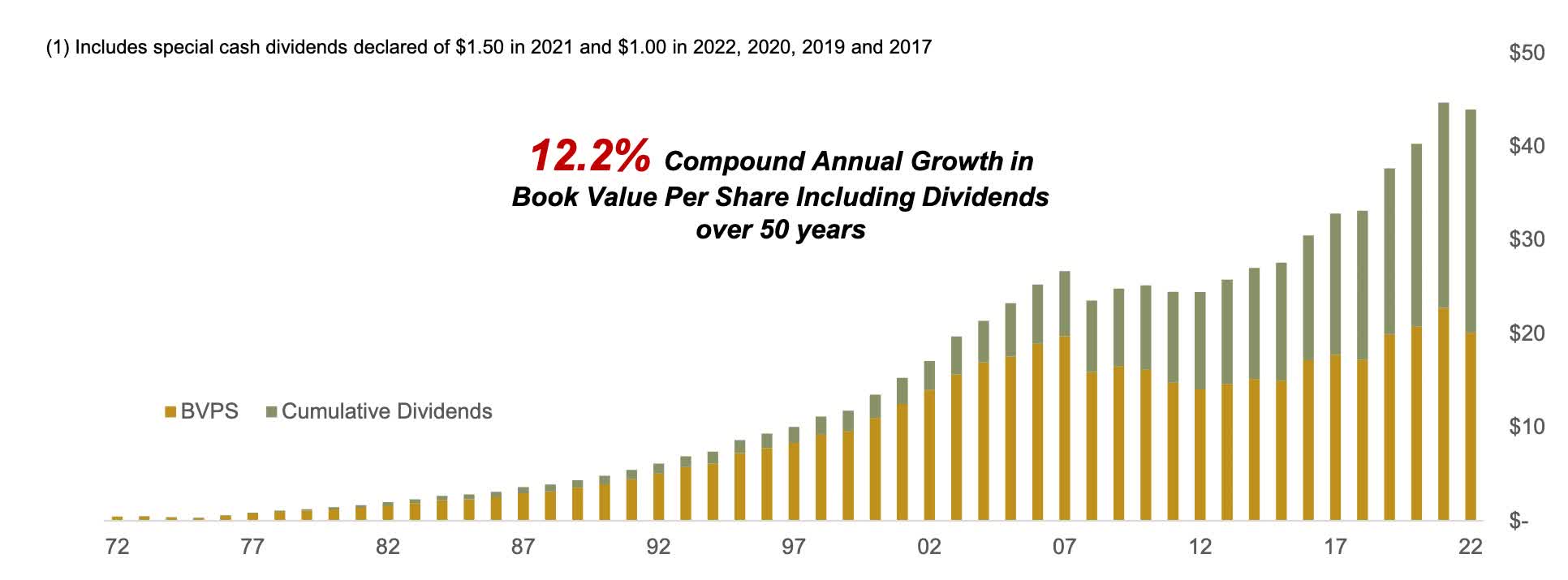

One thing the insurance company does from time to time is special dividends. They declared one every year the last few years with the exception of 2020. But I think we all know why. With the current macro environment, I'm not sure shareholders will get one, but again they did get a raise earlier this year. Additionally, ORI has a 12.2% CAGR in BV per share including dividends.

{kind=link}

Who knows, maybe they'll surprise shareholders with an end-of-year special this December. Another thing to like about ORI is their conservatism. They currently have a very low payout ratio of roughly 39%. They have increased the dividend every year for the last 42 years and paid a dividend consecutively for 82 years! The fact that they are very generous to shareholders is something else I really enjoy about ORI.

Insider Buying

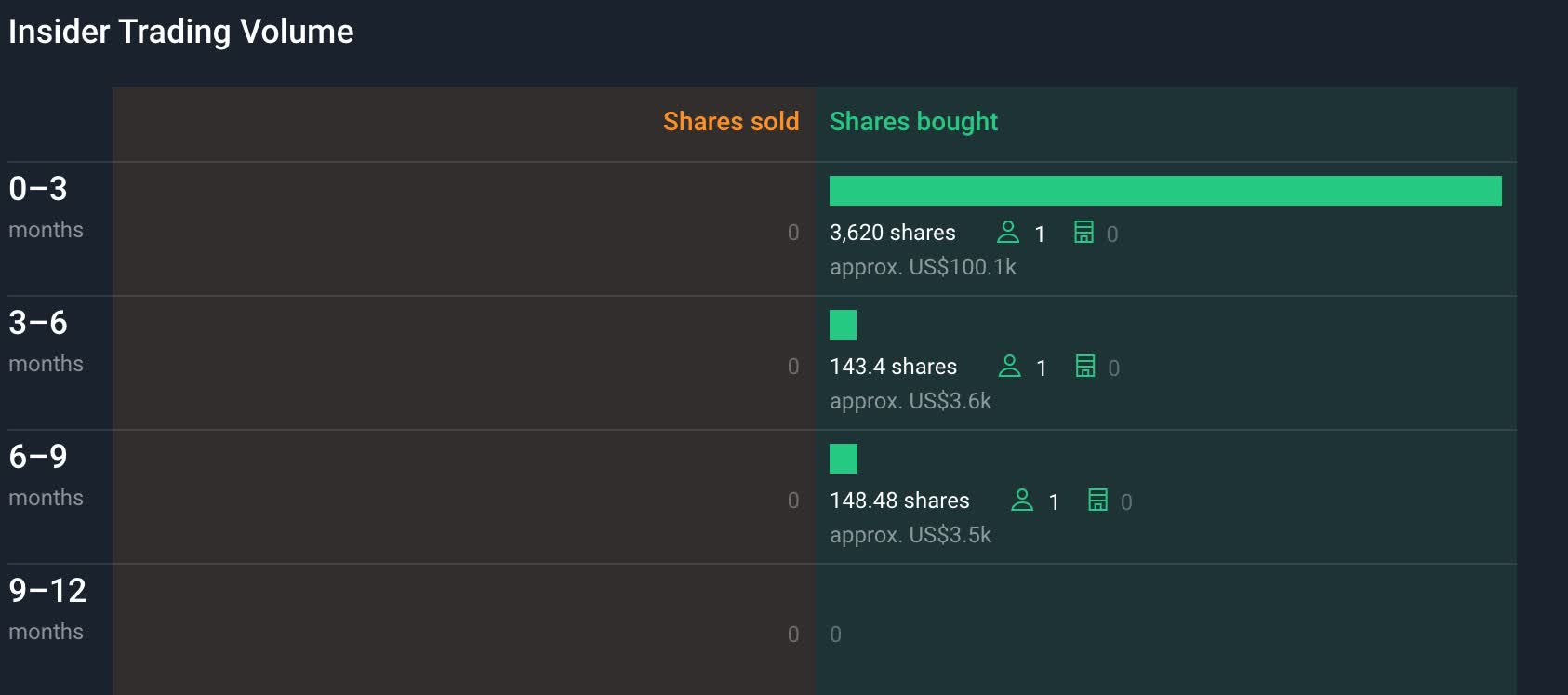

As you can see below, there have been no insiders selling shares in the last 12 months. One board member recently bought $100k worth of stock last month. And that's with the stock being up almost 25% in the last year. This tells me insiders expect the stock to continue growing, and with the new segment, I'm in agreement. To put this into context, popular insurance companies AFL and American Financial Group ( AFG ) have both experienced insider selling over the past 12 months. AFL's price has appreciated 27% in the last year while MetLife (MET) is down slightly over the same period.

{kind=link}

Buybacks & Cash

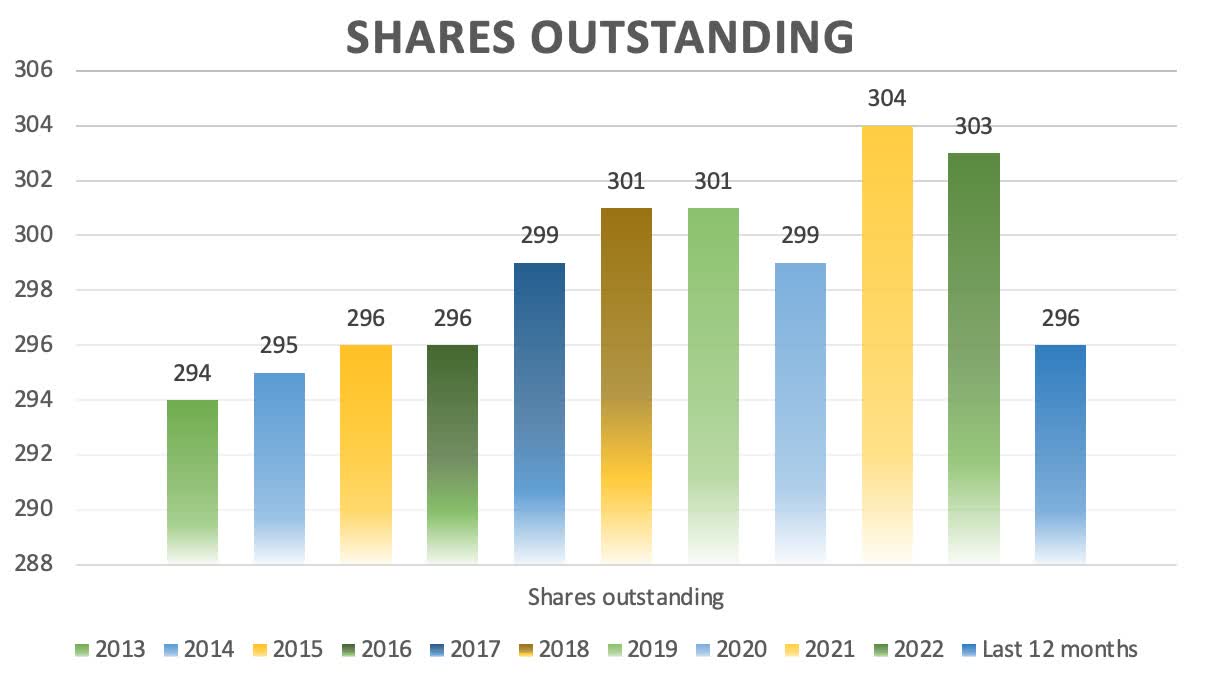

One reason for their modest dividend raises is their share buybacks. Many investors actually prefer buybacks over companies paying dividends or huge raises. ORI does both. Another thing I like is the declaration of specials where they see fit. Instead of doing large raises, something investors can be spoiled with as they will continually expect them. The company often declares specials, which I think is good because management can properly assess the macro environment. Buybacks are great and they are another way companies return cash to their shareholders. Depending on the sector, stocks can issue shares to raise capital. But when a company repurchases its own shares, your percentage in the business increases because there are less shares on the market, and this increases earnings over time.

In Q2, ORI repurchased $220 million worth of shares for a total of $290 million returned to shareholders. They also repurchased an additional $83 million worth at the end of the quarter, leaving them with a remaining $180 million balance in the program. As you can see, shares have gradually increased over the last decade but are now decreasing due to the $450 million buyback announced back in May of this year. Between buybacks and dividends, ORI has returned a total of $492 million to shareholders in the 1H of '23.

{kind=link}

Strong Balance Sheet

In a high interest rate environment, strong balance sheets are a must to ensure our dividend safety. Companies with weaker balance sheets could be headed for disaster, especially if rates continue to climb. What if rates get as high as they were in the '80s? Early '90s? A company that's been around since 1923 has seen and been through it all. They also managed to decrease their debt since the end of 2022 and currently have $1.5 billion, which is manageable. They also boast an investment grade rating of BBB+ and have almost $1 billion in cash & short-term investments.

History & Future Growth

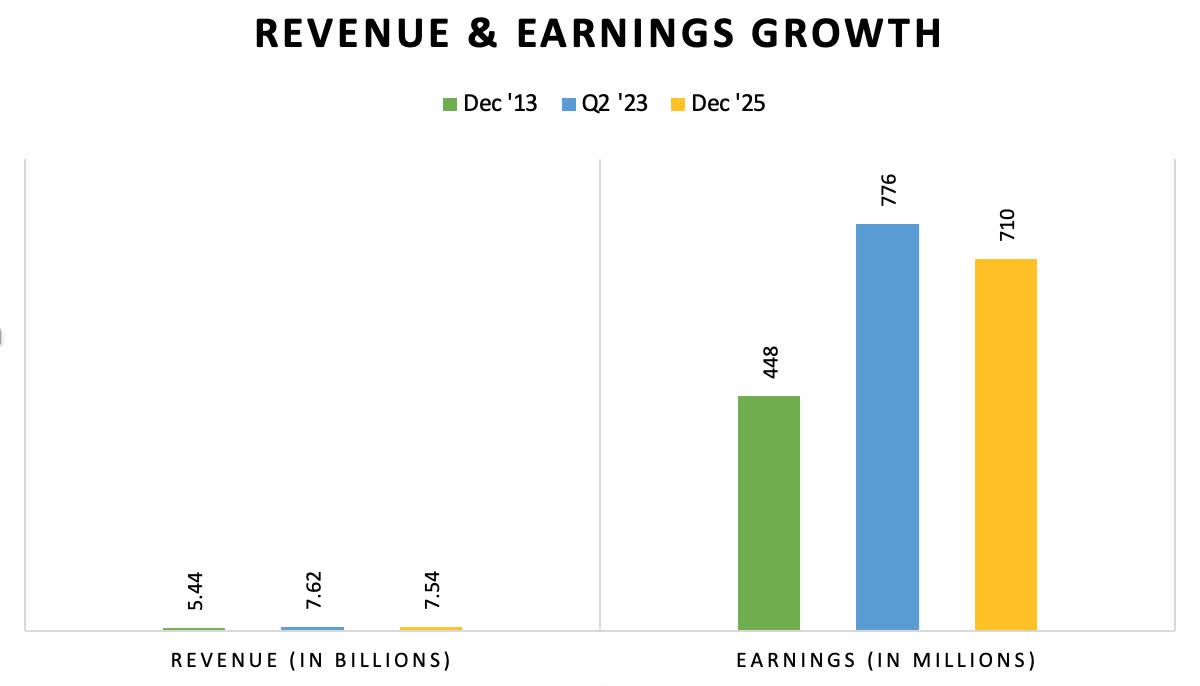

Like I previously mentioned this stock is a stabilizer. One of your holdings you don't have to worry about as much as others. It's just going to continue trotting along. It's a SWAN stock in my eyes. No flash, just cash. Below is ORI's earnings growth over the last decade and expected growth over the next two years. Over the past decade, revenue has grown by 40% while earnings have grown 73%. Again nothing that jumps out at you, but growth is still growth. And although earnings and revenue are expected to decline over the next two years, the decline is minimal.

ORI's revenue & earnings have been slightly volatile over the last decade, but for a company that's been around for a century, they're bound to face tough times. And it certainly won't be the last time either. But as you can see their financials have been on an upward trajectory, which is all you can ask for from your holdings.

{kind=link}

Valuation

Analysts currently have a price target of $30 offering investors some upside from its current price. Using the Dividend Discount Model ((DDM)) and expecting a penny increase to next year's dividend due to the economic uncertainty, and an expected 10% ROR, I have a buy price of slightly above $20. Can I see the price going this low? Most likely not. In the last 6 months, the share price has appreciated in the double digits causing the P/E ratio to trade above its 5-year average. The last time the share price was around $20 was in September of '22.

If we do go into a recession, the stock could fall to that price level again. And if so, I will be buying all the way down. Most quality stocks trade at a premium so getting them below their book value is always a steal.

Risks

It's clear the current high interest rate environment has affected and will continue to have an effect on the business in the near term. Net operating profit & net income were both down quarter-over-quarter. Commercial premiums were also down 37% due to market conditions. But management plans to take advantage of opportunities presented with tools and resources available as stated in the earnings call.

On a positive note, general insurance net written premiums were up 8% and the company expects solid growth in profitability in the segment going forward. But if we do enter into a recession, economic headwinds will continue to affect the volume of transactions in the business, which will most likely lead to lower earnings & revenue.

Investor Takeaway

ORI is a stable, century-old company that's been through several economic downturns and ultimately came out with minor scratches. The company has rewarded its shareholders with increased dividends for 42 years and paid for 82 years consecutively. And I expect them to continue marching towards dividend king status.

Furthermore, the insurance segment has outperformed the overall market while ORI has outperformed both handily. The insurance company has seen some nice price appreciation over the last 6 months, some of this I suspect is due to investors looking for safe-haven stocks during current economic uncertainty.

I believe Old Republic International Corporation stock is fairly valued right now and investors should look to add on any signs of share price weakness. I personally like them under $25, but investors with a long-term outlook on the stock shouldn't have a problem nibbling here and dollar cost averaging in on dips.

For further details see:

Old Republic International: No Flash Just Cash