HOCPY - Olympus: Experiencing Slower Growth Cost Overruns And FDA Scrutiny

2023-09-08 11:07:26 ET

Summary

- Olympus is experiencing slower growth and reputational risk, with the FDA investigating its endoscope manufacturing.

- We have concerns over the quality of management and lower growth prospects than consensus forecasts.

- Negative incidents have lowered earnings visibility and reputation, including lackluster China demand and quality control issues.

Investment thesis

Olympus ( OCPNF ) is experiencing slower-than-anticipated growth and is experiencing reputational risk with the FDA over the manufacturing of its core endoscope business. We have concerns over the quality of management and believe the upcoming growth trajectory is lower than current consensus forecasts. We rate the shares as a Sell.

Quick primer

Olympus is a Japanese medtech company with a 70% global share in gastrointestinal endoscopy (versus key peers FUJIFILM Holdings ( FUJIY ) and HOYA ( HOCPY ) and a 20% global share in laparoscopes (competing with Stryker ( SYK ) and Karl Storz (unlisted)).

With its origins coming from manufacturing microscopes and cameras, the business has divested all of its non-Medtech operations with the sales of the camera division in 2020, followed by the Scientific Solution Division spin-off in Q2 FY3/2023 to Bain Capital.

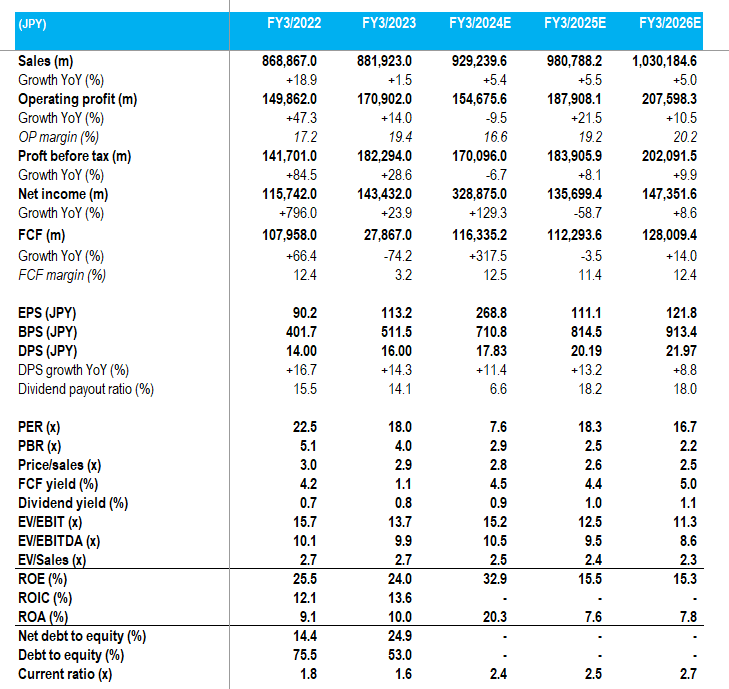

Key financials with consensus forecasts

{kind=link}

Key financials with consensus forecasts (Company, Refinitiv)

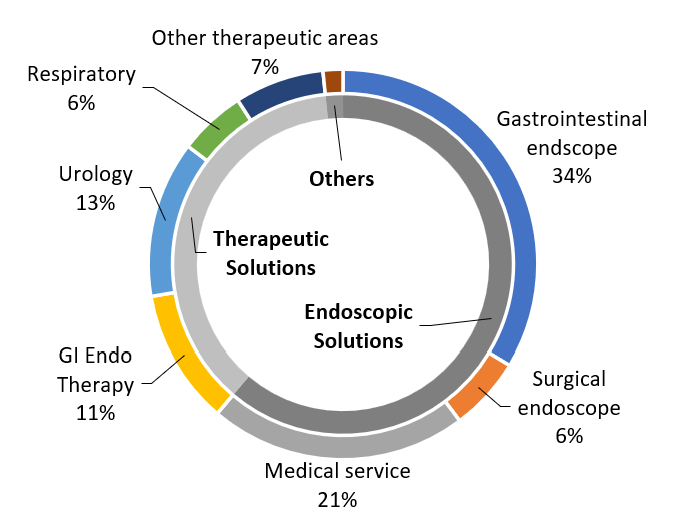

Sales split by business segment and key products - Q1 FY3/2024

{kind=link}

Sales split by business segment and key products - Q1 FY3/2024 (Company)

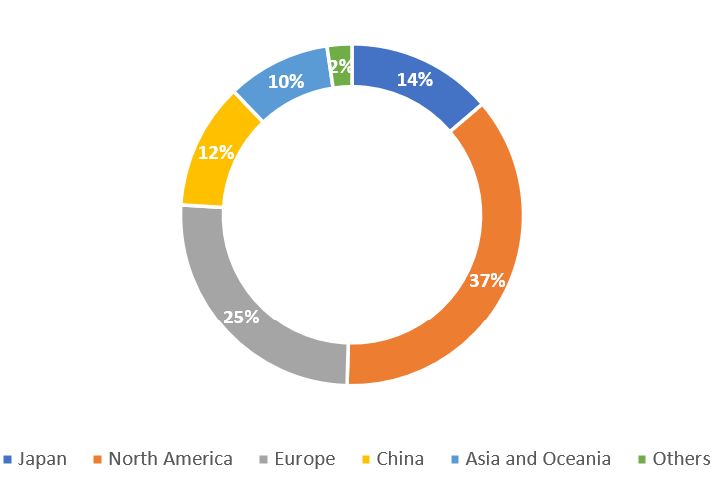

Sales split by geographic market - Q1 FY3/2024

{kind=link}

Sales split by geographic market - Q1 FY3/2024 (Company)

Updating our view in light of negative developments

We updated our view from June 2021 where we rated the shares as a buy, based on the company's predictable earnings growth from the following structural drivers - aging global demographics, improvements in healthcare services, growing demand from emerging markets, and shifts towards personalized care models.

Whilst these trends remain broadly intact, Olympus has experienced two negative incidents that have lowered earnings visibility as well as its reputation. The first is lackluster China demand ( page 1 ), with a slower-than-anticipated recovery post-lockdowns due to ongoing inventory adjustments. The second is related to warning letters from the FDA (3 of them!) regarding quality control over endoscope manufacturing, which is the mainstay of their business; this has resulted in JPY22 billion of costs related to QARA (quality assurance and regulatory affairs) initiatives in FY3/2024, resulting in an expected decline in operating profit YoY. We want to assess whether these issues can be addressed, putting the company back on a growth trajectory.

Q1 FY3/2024 results were a negative surprise, with operating profit declining 50% YoY despite sales volume growth of 8% YoY and an FX tailwind. The company experienced cost overruns, as well as slower-than-expected demand in the US and China.

Chinese demand is set to recover more slowly

Although China sales grew by 148% YoY in Q1 FY3/2024 ( page 20 ), very low hurdles make this performance look positive. However, management was expecting greater activity as surgical procedures were recovering. Customer demand was softer than anticipated due to high customer inventories, which leads us to believe that similar to Stryker, there are negative implications from China's volume-based procurement policies that result in low pricing. When inventory channels are cleared, the company expects firmer demand to return, but there was no timing given for this.

The key driver of demand is procedure volume growth, and we see no reason why China will trend differently from the rest of the world post-lockdown - a backlog will need to be cleared. There will be more pricing pressure ahead in our view, but overall we expect to see the China market be a growth market for Olympus. However, with the state opting for greater product localization, and some constraints expected over healthcare funding in the current economic climate, the growth trajectory could slow quite dramatically into FY3/2025 in our view.

FDA warning letters, a red flag

A warning letter from the FDA is designed to be an advisory comment from the regulator. However, getting three letters in the space of as many months concerning the same subject is a red flag - Olympus is being viewed as violating federal requirements regarding manufacturing practices for its endoscopes. Remedial measures are expensive which indicates the seriousness of this issue, forecast to be JPY22 billion/USD151 million in FY3/2024. This is an indication of ineffective management in our view.

Although Olympus is the runaway market leader in endoscopes with approximately 70% market share, this looks optically negative and gives its competitors some leeway to win share. The FDA has highlighted weaknesses in Olympus's reusable endoscopes, which can be problematic given its requirements for cleaning and disinfection.

The company has already experienced cost overruns due to QARA-related complaint handling cases in Q1 FY3/2024. Although the company states that these costs are on track (page 2), we believe that there is a risk of overruns due to 1) potentially more activity from the FDA, and 2) management's reactions to the warning letters have been slow, meaning that remedial measures may take more time to establish, with plans running over and potentially extending into FY3/2025.

Valuation

On consensus forecasts, the shares are trading on P/E FY3/2025 18.3x, and a free cash flow yield of 4.4%; however, we believe stable 5% sales growth will be difficult to achieve given the economic backdrop. The P/E multiple is at a material discount to other MedTech peers, such as (on a GAAP basis) Stryker on 35x and Medtronic ( MDT ) on 24x. However, the company has a track record of regulatory risk, which may explain some negative market sentiment being reflected on its valuations.

Risks

The company's slow start to Q1 FY3/2024 was partly due to supply chain issues. If these are to clear up, business activity will step up a gear, which would raise earnings visibility. Rigorous measures to meet FDA's concerns will put the endoscope business back on track, especially with the planned introduction of next-generation surgical endoscopy systems.

There is continued regulatory risk with the FDA regarding endoscope manufacturing, and if left unresolved could develop into a more serious matter, particularly with new product releases planned. In a recessionary environment, elective surgery volumes tend to decline, cutting demand generally for medical instruments.

Conclusion

Olympus remains a market leader in its specialist field of endoscopes, but we have concerns over management quality. The economic environment is likely to act as a headwind for the business, and the growth trajectory in China may be lower than current expectations. Although the shares have corrected, we do not see this as a buying opportunity and have downgraded our rating to a sell.

For further details see:

Olympus: Experiencing Slower Growth, Cost Overruns And FDA Scrutiny