HTOOW - OPEC+ Might Have Killed Any Chance Of A Fed Pivot This Year

2023-04-05 07:41:05 ET

Summary

- The global economy has been on a sharp decelerating trend lately, yet the global commodities price index was still higher in Q4, 2022 than at any point in past decades.

- A slowing global economy, coupled with rising interest rates provided a respite from rising inflation, but we may be in for an oil price spike due to production cuts.

- Higher oil prices tend to push the price of everything up, which in this particular case comes at a time when inflation is already taking on a life of its own.

- Without aggressive monetary policies designed to moderate inflation, we could see it get out of control, which is why we are now very unlikely to see a monetary policy reversal, despite the potential implications to the health of the banking sector.

- Investment returns will be meager, or even mostly negative in real terms for the foreseeable future for most investors. The odds of investments at least beating inflation are increasingly low.

Investment thesis: The recent banking issues that have surfaced as a result of low-interest-yielding assets that are on the books as a result of the low-interest rate environment of the past decade, gave rise to growing speculation of an end to the Federal Reserve's fight against inflation. The fact that inflation rates slowed significantly from earlier highs provided added weight to the argument that interest rate increases should cease soon, and we should potentially even expect a move to reverse course. The recent OPEC+ decision to cut production by over 1 mb/d starting in May, makes it unlikely for the Federal Reserve as well as other major central banks to pursue a lower interest rate policy. Oil prices will probably move higher in the coming months, despite an increasingly weak global economic outlook, which will push inflation rates back higher. Central banks around the world will have no choice but to continue fighting inflation at the expense of growth, and with the risk of destabilizing the banking sector, because arguably losing control of inflation might become a bigger problem than the failure of banking institutions, or stagnated growth. Average investment returns will at best keep up with inflation going forward for the foreseeable future. The only chance of getting ahead of the average will be to pick stocks cautiously, and carefully, with a clear view of the big picture and what to do about it.

The global oil supply/demand balance outlook within the context of OPEC's recent move

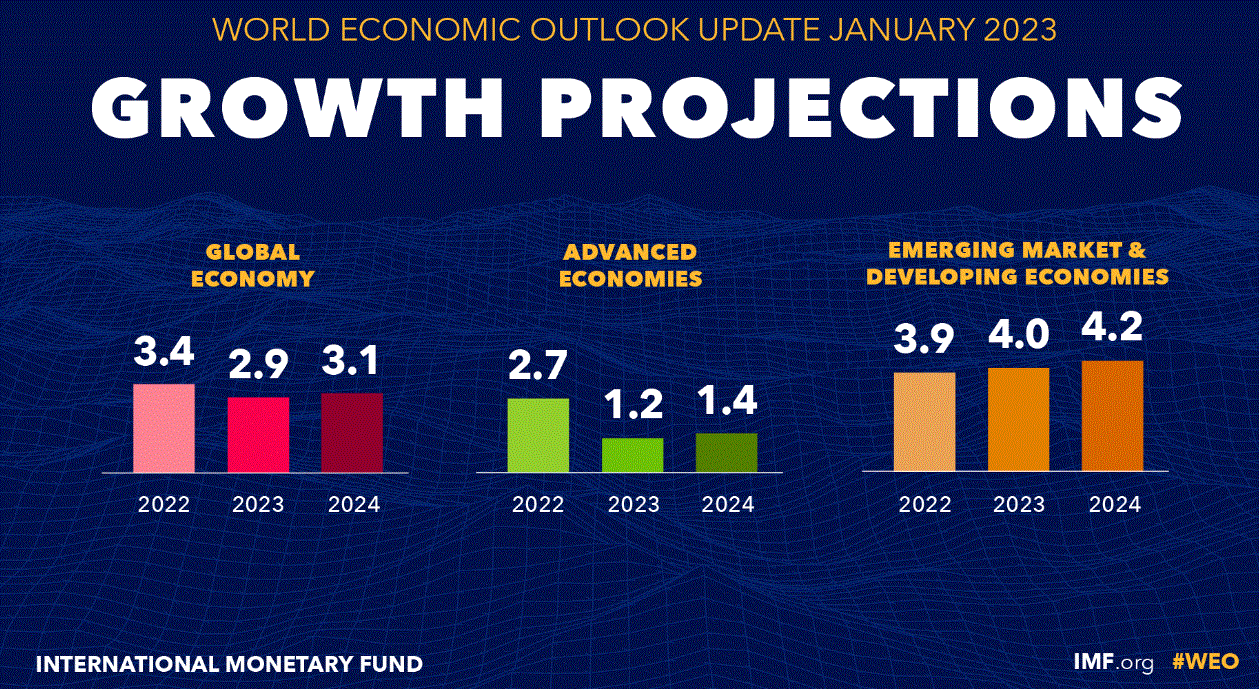

As of the latest IMF forecasts global economic growth is going to come in at a rate of 2.9% for 2023.

{kind=link}

Growth in the developed world is set to be particularly slow, growing about three times slower compared with the developing world this year and next.

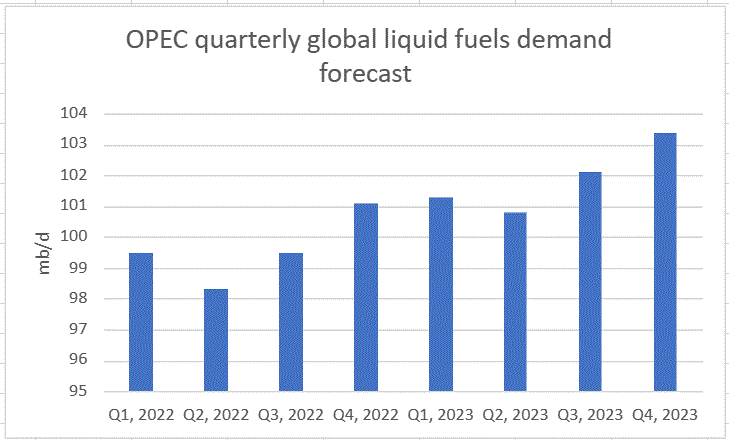

Based on these growth projections, OPEC has a quarterly global liquid fuels demand forecast, which shows a significant demand leap, set to happen in the third and fourth quarters.

{kind=link}

OPEC also has an estimate in terms of global liquid fuel supply, which tends to be the most up-to-date.

OPEC

As we can see, as of February of this year, the global liquids supply stood at 101.9 mb/d, which seems to be approximately adequate to cover demand all the way to the fourth quarter of this year, after which things were set to be less comfortable, in the absence of supply growth. The OPEC+ move to cut crude supply by about 1.15 mb/d, comes in addition to a .5 mb/d cut already announced and supposedly implemented by Russia last month. The total of almost 1.7 mb/d in supply cuts brings us into a situation of potential market imbalance, with supply shortfalls, as soon as the third quarter of this year, while making the fourth quarter of this year look outright disastrous, with a supply/demand gap of about 3 mb/d in the absence of supply growth elsewhere compared with February levels.

The gap is wide enough to necessitate demand destruction in order to bring the market back into balance and my guess is that central banks will prefer to see the demand destruction occur in a controlled manner, rather than have it crushed by market forces. In other words, we arguably do not want to see a massive oil price spike being the factor that will create conditions for demand destruction to occur, because it could push us into a stagflationary trap.

The reasons why demand destruction will mostly occur in the developed world

It is possible that some global liquid fuel supply growth will occur from levels seen in February, outside of the OPEC+ alliance, but at best it might only be enough to compensate for the roughly 1.7 mb/d in announced and implemented cuts. The February supply numbers that I am using as a reference probably came within the context of some liquids production around the world being curtailed, due to field maintenance which tends to sometimes happen in the winter months, when global demand is weaker. Production might improve in the coming months as some of those volumes that were lost due to seasonal maintenance production cuts come back online.

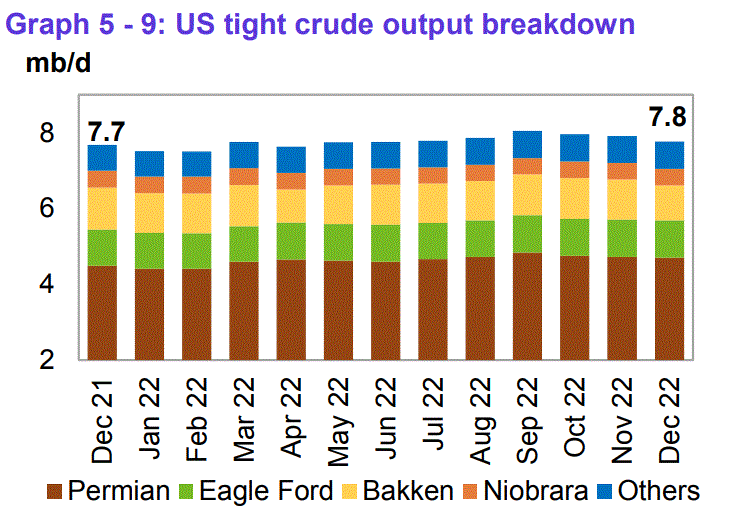

One source of production growth that we are unlikely to see pan out is US shale. Production has been stagnant in the past year or so, and all indications are that things are unlikely to change going forward.

{kind=link}

In a best-case scenario, US shale will add a few hundred thousand barrels per day of extra crude supply in the coming months. In a worst-case scenario, we could even lose some shale production, as companies continue to shy away from drilling second-tier acreage, while more and more drillers are running low on prime acreage inventories.

Given the wide gap between global supplies and forecast demand for the end of this year, it is reasonable to expect some demand destruction to occur, although there are clearly some supply/demand factors that make it impossible to accurately predict the magnitude of the demand destruction that will be needed. One factor going forward, which makes it far more likely that the North American & European economies will be the ones that will see most of the demand destruction occur is the fact that Asian oil importers are partly shielded from future potential price increases by the fact that they are buying significant volumes of Russian and Iranian crude at a discount. It would not surprise me if, for instance, Saudi Arabia will look to defend its Asian market share by offering a discount to Asian customers compared with the price it will charge Europeans. I doubt that Saudi Arabia will be satisfied with being stuck with the European market, while Russia & Iran capture a growing slice of the Asian market.

Taking a step back and contemplating the implications for central banks, China, India, and others in Asia that are able to access cheaper Russian or Iranian oil will not see as much resulting inflationary pressures from rising oil prices. Europeans on the other hand may have to start paying a rising premium just to attract shipments from elsewhere, after they stopped buying Russian oil and refined products.

The US oil market is likely to come under pressure as well, just as we saw with natural gas, due to the growing need to ship oil and refined products to Europe in order to shield it from the aftereffects of the economic divorce with Russia, which was the EU's biggest supplier of energy by far before 2022. We had a glimpse of what is to come in this regard with US natural gas prices, which soared to levels not seen in over a decade as EU demand for US LNG led to a tightening of the market.

US crude oil exports to the EU currently make it the top supplier, with 18% of all EU oil imports coming from the US currently, which is up from 13% at the start of 2022. It is very probable that the US will see a further increase in EU reliance on US energy exports going forward, making domestic energy inflation pressures more likely to occur.

The Federal Reserve might have considered pausing its rate hike policy at some point this year, perhaps soon before this happened, but evidently, this latest development is likely to change things. James Bullard , the President of the St. Louis Fed seems to have immediately taken note of the added difficulty that this will cause in balancing Fed policy going forward. While it may not be an easy decision, my opinion is that the Fed as well as other central banks around the world will favor fighting inflation, despite severe potential negative consequences that may come with the policy. The alternative will probably be deemed to be potentially worse.

Investment implications

In the absence of a reversal of current central bank policies to increase interest rates, very few investment opportunities are likely to perform well enough to beat inflation for the foreseeable future. Inflation is not likely to be brought under control and back to long-term stated central bank goals in most economies, given the price pressures that we are set to see from commodities, especially oil prices. This year and beyond, I foresee a struggle for investors to achieve returns that will at the very least keep up with inflation.

Oil stocks seem like a good bet within the current environment. About a fifth of my current stock portfolio is related to oil & gas, with Suncor ( SU ), and Canadian Natural Resources ( CNQ ) being my main choices. I like Canadian oil sand producers because they have a proven track record of profitability within the context of average oil prices we saw in the past decade, while they tend to sit on reserve life ratios that are higher than the average of the overall global industry. The fact that Canada has arguably lower than the average geopolitical risk associated with investment risk profiles, is also attractive within the current global geopolitical context.

While I do find the oil sector to be one of the more attractive long-term investment options, we should be mindful of the fact that the odds of a massive oil price spike that would provide spectacular potential investment returns are not particularly high as long as major central banks continue to pursue an inflation-fighting policy. In fact, there is always a risk that the resulting demand destruction will at some point drive oil demand far below current supply prospects. In the short term fundamentals matter less, and momentum driven by the news matters more, therefore I expect that oil producers will see a boost to their stock price in the next few weeks and even months.

Precious metals should do well within the context of a stagflationary environment, with high-interest rates, despite the general perception that high-interest rates tend to dampen market enthusiasm for gold & silver. Interest rates may be higher, but adjusted for inflation they are actually lower than they were most of last decade. For instance, the US 10-year treasury bond currently yields 3.5%, while inflation is running at 6%, meaning that government bonds do not offer full wealth preservation, only slowing down the loss in real buying power, relative to cash. Gold on the other hand has a long-term historical track record of outpacing inflation, even if some years it does not feel like it does, depending on one's investment timing.

In addition to physical gold & silver which I constantly held for the past decade and a half, I have a small position in the SPDR Gold Shares ETF ( GLD ), and I own stocks in Barrick Gold ( GOLD ), Wheaton ( WPM ), and Silvercorp ( SVM ). These positions make up about 15% of my investment portfolio currently.

With rising Asian economic giants like China & India benefiting from cheaper energy imports, it might make some sense to invest in ETFs that offer exposure to those countries, since lower energy prices, and potentially a more accommodating monetary policy can be good for domestic stocks in those countries. I have a small position in the iShares MSCI China A ETF ( CNYA ), which offers broad exposure to Chinese stocks, but other than that, I have been keeping my distance, mostly because fundamentals may end up being overshadowed by geopolitics. There is an endless list of potential outcomes that could see investors, particularly, non-domestic ones get hurt as tensions continue to rise.

My stock holdings of all other assets, ranging from AMD ( AMD ), and Ford ( F ), to European startup green hydrogen producer Fusion Fuel ( HTOO ) make up about a third of my portfolio, and I regard this segment to be most at risk in the event that the economic picture worsens, as it gets squeezed by higher interest rates as well as potentially higher energy and other commodities prices. In the event that I am wrong, I want to continue holding on to these positions, about 15 stocks in all. In the event I am right, I am currently sitting on about 30% cash, which will allow me to add to some of these positions, as well as seek out new ones. Cash may not seem like a good bet with inflation running high, but I believe it may pay in the long run to have some for the short term available in case good entry points appear.

My current overall portfolio is one that I am satisfied with, given ongoing events and trends. I expected this decade to be a tough one for investors. Already, in the spring of last year, I warned that we are likely on the cusp of a long era of commodities scarcity, where the Fed will become more of a reactionary institution rather than the one that will shape events.

The recent OPEC+ move to cut production runs counter to our economic interests of bringing down inflation. The hope was that with the help of what was until recently thought of as an environment of commodities price deflation from all-time highs, in the face of decelerating global economic growth, we could see a return to a low-interest rate environment. OPEC+ essentially opted to put its interests ahead of ours, which is a sign of growing confidence in the balance of power shifting in the favor of net commodities exporters. It is a new era we are entering and as investors, we have to recognize that it will be tough, and we need to make the best of it, by trying our best to understand it and what to do about it.

For further details see:

OPEC+ Might Have Killed Any Chance Of A Fed Pivot This Year