BRW - OPP: Positioned For Near-Term Rate Cuts But Distribution Outlook Is Hazy

2023-12-03 05:33:18 ET

Summary

- The RiverNorth/DoubleLine Strategic Opportunity Fund offers a high level of current income with a 15.22% yield, but there are concerns it may have to reduce its distribution in the future.

- The fund's recent performance has been reasonable, but it has underperformed the S&P 500 Index.

- The fund's portfolio is managed by RiverNorth and DoubleLine, and it invests in a combination of traditional bonds and non-traditional assets like closed-end funds and business development companies.

- The fund could perform well if rates fall over the next year, as most of its assets are invested in traditional bonds. That is no guarantee, however.

- The fund appears to be unable to sustain its distribution and its valuation is more expensive than average.

The RiverNorth/DoubleLine Strategic Opportunity Fund ( OPP ) is a closed-end fund that specializes in providing a high level of current income for its shareholders. The fund’s current 15.22% yield certainly stands as a testament to its abilities in this area, as that yield far exceeds the yield of nearly every closed-end fund in the market. In fact, the fund’s yield is so high that there could be some reasons to suspect that it will have to reduce it in the near future. After all, even in the current high-yield environment, an asset with an outsized yield is typically a reflection by the market that the payout will need to be reduced in the near future. For what it is worth though, the fund has maintained its distribution year-to-date, although it did reduce it at the end of last year:

{kind=link}

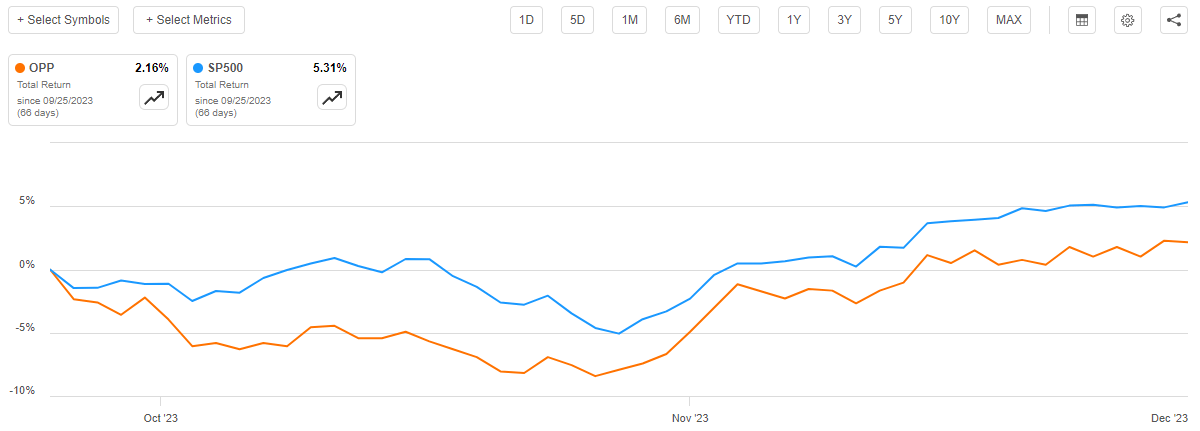

As regular readers will likely recall, we last discussed the RiverNorth/DoubleLine Strategic Opportunity Fund around the end of September. At that time, it did appear that there was some risk that the fund would have to reduce its distribution, as it is not funding its distribution out of its investment profits but rather by bringing in new money via the sale of shares to new investors.

The fund’s performance since the last time that we discussed it has been very reasonable. An investor who purchased the fund on the date that my prior article was published has earned a 2.16% total return including the distributions that the fund paid out over the past two months. This is worse than the 5.31% return of the S&P Index ( SP500 ) over the same period, however:

{kind=link}

However, the S&P 500 Index may not be the best index to compare this fund’s performance to since that index is not usually bought by those investors who are seeking to earn a high level of income from their portfolios. After all, the index only yields 1.55% right now and that is substantially lower than even a money market fund.

As a few months have passed since the last time that we discussed this fund, it could be a good idea to revisit it and see what changes have been made and whether or not this fund could still fit into a properly structured portfolio.

About The Fund

According to the fund’s website , the RiverNorth/DoubleLine Strategic Opportunity Fund has the primary objective of providing its investors with a very high level of current income and total return. This actually makes a lot of sense considering the fund managers involved. DoubleLine, for example, has earned something of a reputation for being an excellent credit fund manager, similar to PIMCO. RiverNorth, for its part, is a bit more unique as some of its other funds invest in closed-end funds, business development companies, and other things that are outside the traditional stock and bond universe. As I have pointed out in various previous articles, bonds are by their very nature an income vehicle since they have no net capital gains over their lifetimes. Closed-end funds and business development companies are entirely different animals, since they can benefit from share price appreciation and typically provide very high yields to their investors because they pay out the majority of their investment profits in the form of dividends and distributions. As this fund is managed by both companies, we can expect that it will be investing in a combination of traditional bonds and less traditional things such as closed-end funds and business development companies.

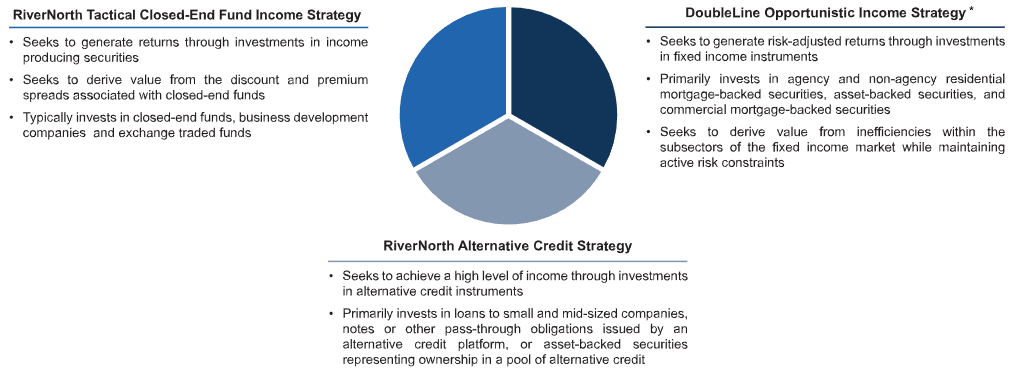

That is, in fact, what we find here. The fund’s website states that the RiverNorth/DoubleLine Strategic Opportunity Fund breaks up its portfolio into three segments. These are:

- Tactical Closed-End Fund Income Strategy

- Alternative Credit Strategy

- Opportunistic Income Strategy

Each of the two fund managers takes responsibility for one of these segments. As we can see here, DoubleLine takes responsibility for managing the opportunistic income strategy portion of the portfolio while RiverNorth is responsible for managing the other two segments:

{kind=link}

The basic objective here is to use the research and expertise of each of the two fund managers to try and maximize the overall return of the portfolio. This is similar to the strategy used by the Liberty All-Star Equity Fund ( USA ), except that the RiverNorth/DoubleLine Strategic Opportunity Fund only has two managers.

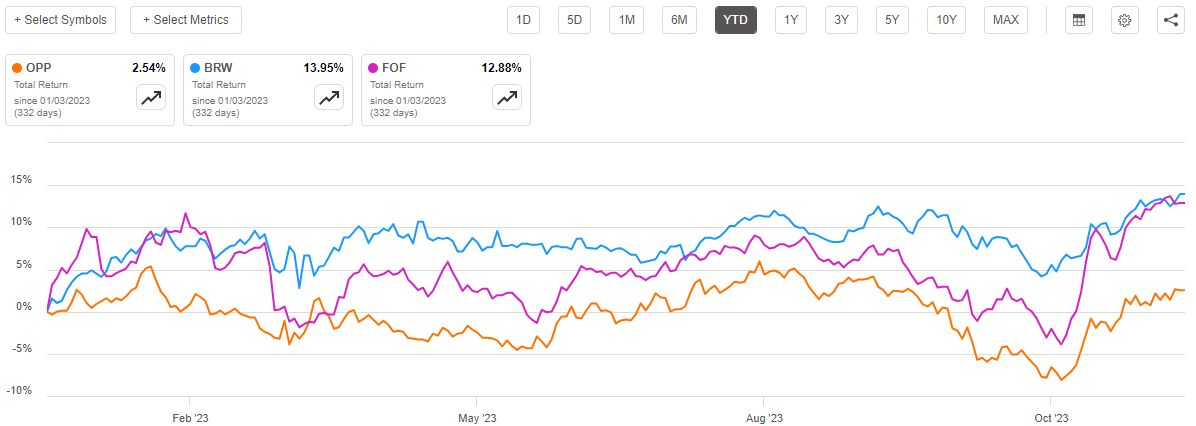

However, there are some questions about how successful it is. There are basically no other funds that use a strategy similar to this one. There are some other funds that invest in closed-end funds, however. For example, the Saba Capital Income & Opportunities Fund ( BRW ) and the Cohen & Steers Closed-End Opportunity Fund ( FOF ) both fall into this category. These two funds have both delivered a far better investment return year-to-date than the RiverNorth/DoubleLine Strategic Opportunity Fund:

{kind=link}

However, these two peer funds are certainly not perfect peers for the RiverNorth/DoubleLine Strategic Opportunity Fund. One reason for this is that the RiverNorth/DoubleLine fund’s portfolio is not perfectly balanced between the three strategy silos. In fact, right now the opportunistic income strategy segment accounts for 64% of the fund’s total assets:

{kind=link}

The opportunistic income strategy segment is basically a straightforward bond fund that primarily invests in mortgage-backed securities. As such, this fund currently looks like a bond fund with a twist. That explains why the fund’s own website benchmarks it against the Bloomberg US Aggregate Bond Index ( AGG ). If we do that, then the RiverNorth/DoubleLine Strategic Opportunity Fund has greatly outperformed its benchmark index on a total return basis:

{kind=link}

When distributions are included, the aggregate bond index ETF has delivered a 1.29% total return year-to-date, but the RiverNorth/DoubleLine Strategic Opportunity Fund has delivered a 2.54% total return year-to-date. This is a decent performance, but it still pales in comparison to some of the other things that are available in the market. For example, the Saba Capital Income & Opportunities Fund has proven to be a much better place to be in today’s volatile market environment.

With that said, we might be seeing better performance from the RiverNorth/DoubleLine Strategic Opportunity Fund in the near future. This comes from the fact that 64% of its assets are essentially invested in a straightforward bond fund. As everyone reading this is no doubt well aware, bond prices tend to go up when interest rates decline, and the market currently expects that the Federal Reserve will cut interest rates by 125 basis points next year. That is almost certainly the reason why this fund’s share price has been going up since the end of October. Investors are bidding up the price of long-term bonds in anticipation of these interest rate cuts and that process is forcing up the value of the bonds in the opportunistic income strategy silo. This naturally increases the fund’s net asset value, and the price of the fund’s shares usually correlates with the net asset value. If investors continue to be optimistic about interest rates and continue bidding up bond prices, then this is something that could continue for a while longer and cause this fund to deliver reasonably strong returns next year.

However, there is no guarantee that interest rates will be cut next year. The current members of the Federal Open Market Committee are only expecting a single 25-basis point cut next year, which is a far cry from the current market expectations. A quick search engine query reveals that most analysts are stating that it would take a severe recession for rates to be cut next year. While it is certainly possible that a recession will strike next year, that is by no means certain. Indeed, the Federal Government might try to do whatever it can to avoid having a recession in an election year and flooding the economy with borrowed money, and thus push interest rates up. In short, everything is up in the air right now. If rates are not cut to the degree that the market is currently pricing in, that would almost certainly negatively impact this fund as the price of the bonds in its opportunistic income strategy segment decline and push its net asset value back down. Of course, the fund’s alternative credit strategy segment invests in floating-rate loans and similar assets that will actually benefit from such an event, so if the fund were to change allocations, then it might be able to avoid such a decline.

The point is that nothing is certain at the moment. The fund’s current positioning should work reasonably well for a falling interest rate environment if indeed that is what we experience in 2024.

The RiverNorth/DoubleLine Strategic Opportunity Fund does have the ability to alter the size of each of the silos as a percentage of the fund’s total assets. From the fact sheet (emphasis mine):

RiverNorth allocates the fund’s assets among three principal strategies: Tactical Closed-End Fund Income Strategy, Alternative Credit Strategy, and Opportunistic Income Strategy. RiverNorth manages the Tactical CEF Income Strategy and the Alternative Credit Strategy, DoubleLine manages the Opportunistic Income Strategy. RiverNorth determines which portion of the Fund’s assets is allocated to each strategy based on market conditions.

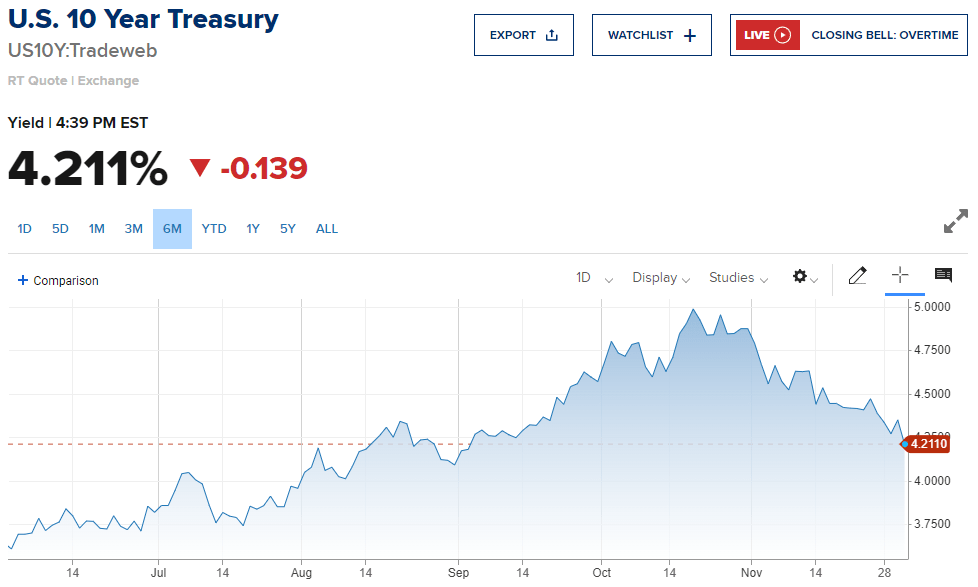

Please note the bolded sentence. This particular statement means that the fund may increase its allocation to the Alternative Credit Strategy silo if it appears that interest rates are unlikely to decline in the near future. However, it does not appear that the fund is taking advantage of that ability. As I noted back in September, the Opportunistic Income Strategy silo had 64% of the fund’s assets on August 31, 2023. That is the same as what that silo had at the end of October. In August and September, long-term interest rates were increasing throughout the economy. After all, the ten-year U.S. Treasury was at 4.0910% on August 31, 2023, but ended up peaking at 4.9880% on October 19:

{kind=link}

In such an environment, it would have made sense to pull some of the money away from the Opportunistic Income Strategy and put it into the Alternative Credit Strategy, as floating-rate loans outperformed traditional bonds and mortgage-backed securities during that period. However, the fund does not appear to have done that. As such, the fund might not be the best holding if the market proves to be wrong about the interest rate trajectory over the course of 2024.

Leverage

As is the case with most closed-end funds, the RiverNorth/DoubleLine Strategic Opportunity Fund employs leverage as a method of boosting the effective yield of its portfolio. I explained how this works in my previous article on this fund:

Basically, the fund is borrowing money and using that borrowed money to purchase fixed-income assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As the fund is capable of borrowing at institutional rates, which are significantly lower than retail rates, this will usually be the case.

Unfortunately, the use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. As such, we want to ensure that a fund is not employing too much leverage because that would expose us to too much risk. I do not usually like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

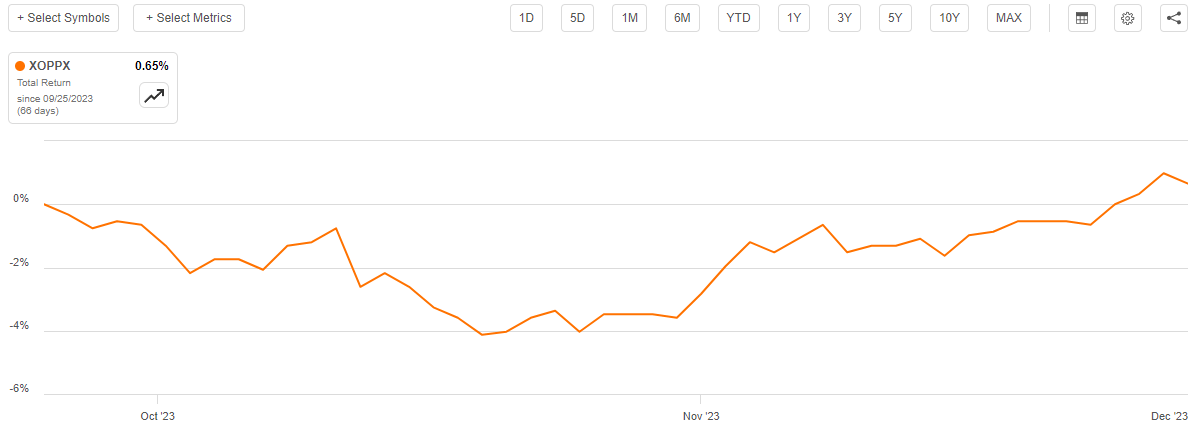

As of the time of writing, the RiverNorth/DoubleLine Strategic Opportunity Fund has leveraged assets comprising 36.09% of its portfolio. This is relatively in-line with the 36.17% leverage ratio that the fund had the last time that we discussed it. This makes a certain amount of sense as the fund’s net asset value is up 0.65% since the last time that we discussed it:

{kind=link}

As such, if the fund’s leverage remained static then its leverage ratio would naturally come down a bit just due to the increase in assets. That appears to be what happened here.

As was the case the last time that we discussed this fund, the current leverage ratio is probably okay despite being a bit higher than the one-third level that we would really like to see. After all, this fund is primarily investing in bonds and other securities that are not especially volatile. As such, it should be able to sustain a higher level of leverage than an ordinary equity fund could.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the RiverNorth/DoubleLine Strategic Opportunity Fund is to provide its investors with a high level of current income and total return. In order to achieve this goal, it primarily invests in a portfolio consisting of both traditional and floating-rate debt securities. These securities provide the majority of their total returns in the form of direct payments to the investors, and when we consider that the leverage allows it to control more securities than it otherwise could, we can quickly see how this would result in this fund having a fairly high effective yield from this portion of the portfolio. This fund also purchases shares of closed-end funds and business development companies that tend to have very high yields. The money that the fund receives from all of these various sources gets pooled together, and the fund adds any capital gains that it manages to realize to this pool of money. The fund then pays all of this money out to its shareholders, net of its own expenses. We can probably expect that this will allow the fund’s own shares to boast a very high yield.

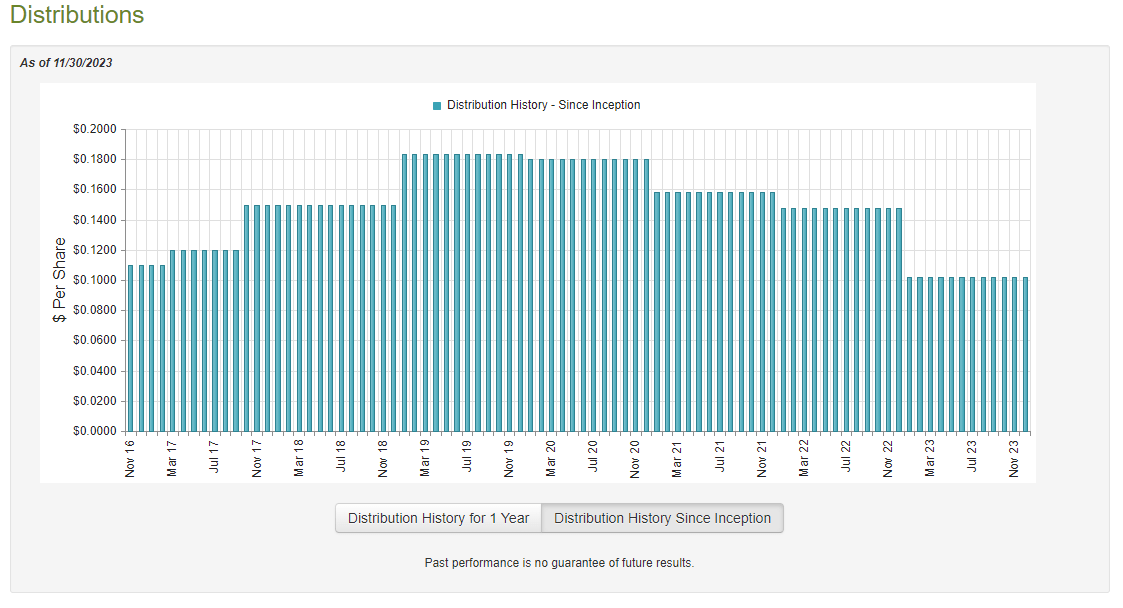

This is indeed the case, as the RiverNorth/DoubleLine Strategic Opportunity Fund pays a monthly distribution of $0.1021 per share ($1.2252 per share annually), which gives it a whopping 15.22% yield at the current price. That is a much higher yield than what we find with just about any other closed-end fund, which could be a sign that the market believes that the current distribution is unsustainable. The fund’s history does not exactly impart much confidence in its ability to sustain it, as the fund has been consistently cutting its payout since 2019:

{kind=link}

This will almost certainly reduce the fund’s appeal in the eyes of those investors who are seeking to receive a safe and secure income from the assets in its portfolio. This is a category that will likely include most retirees and others who are dependent on their assets to cover their bills or finance their lifestyles. The fact that the fund has been cutting its distribution over the past few years is also a sharply negative thing in today’s current inflationary climate, as inflation is constantly reducing the number of goods and services that we can pay with the distribution that the company pays out. In such an environment, we need our incomes to be rising if we are to maintain our current lifestyles, not falling.

However, the fund’s past is not necessarily the most important thing for anyone who is purchasing the fund’s shares today. After all, anyone who buys the fund’s shares today will receive the current distribution at the current yield and will be completely unaffected by the actions that the fund has taken in the past. As such, the most important thing for us right now is to determine how well the fund can sustain its current distribution.

Fortunately, we do have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on June 30, 2023. This is a nice period for the report to cover because it should give us a good idea of how well the fund managed to perform in two very different market environments. During the second half of 2022, the market was in a powerful bear period, as the impact of the Federal Reserve’s rate-hiking cycle was pulling down bond prices and the share prices of funds that invest heavily in bonds, such as this one. This all changed during the first half of 2023, as investors suddenly became euphoric and began buying up bonds and stocks, pushing prices up. That could have given this fund the opportunity to realize some investment gains.

During the full-year period, the RiverNorth/DoubleLine Strategic Opportunity Fund received $22,307,745 in interest and $4,109,979 in dividends from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund had a total investment income of $26,482,261 during the period. It paid its expenses out of this amount, which left it with $21,517,833 available for the shareholders. That was, unfortunately, nowhere near enough to cover the distributions that the fund actually paid out during the full-year period. The fund’s distributions totaled $32,884,481 during the period, which was $11,366,648 more than the fund’s net investment income. This is disappointing, because we usually like a fixed-income fund to be able to fully cover its distributions out of net investment income. While this fund is not exclusively a fixed-income fund, we still want it to get closer to covering its distributions out of investment income than we see here.

With that said, there are some other methods through which the fund can obtain the money that it needs to cover its distributions. For example, it might be able to take advantage of changes in bond prices to pocket some capital gains. Unfortunately, the fund failed miserably at this task during the period. The fund reported net realized losses of $6,667,210 and had another $9,087,794 net unrealized losses during the period. This was clearly nowhere near enough to make up the difference needed to cover the fund’s distributions.

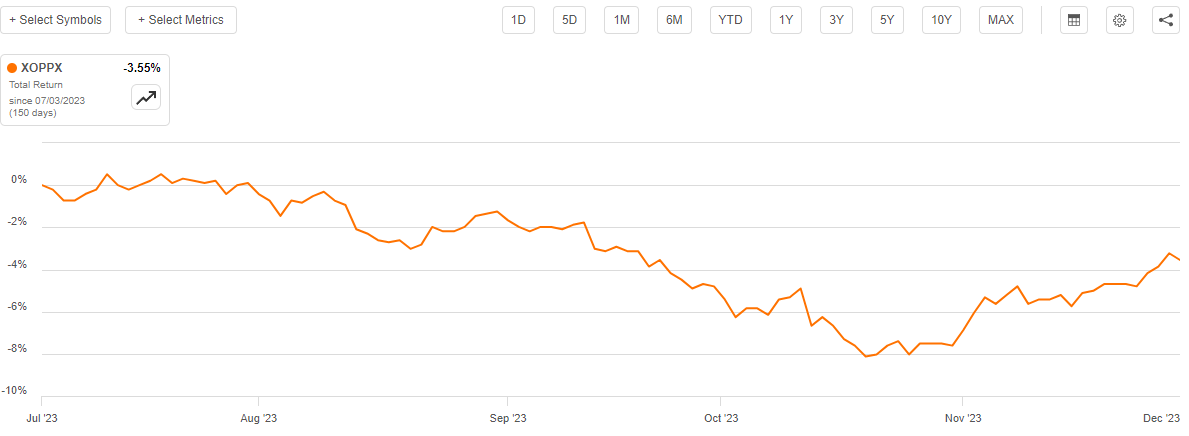

The fund seemingly covered its distributions using $33,999,204 that it brought in by selling shares to new investors. That amount was completely enough to cover the distributions and left the fund with some money left over. Its net assets went up by $1,535,659 over the period after accounting for all inflows and outflows. It is questionable though how well it can sustain its distribution if it is relying on new money coming into the fund to maintain it. This certainly explains why the fund saw fit to cut the payout at the end of last year. It is uncertain how sustainable the fund’s distribution will be at the new level, but right now it is not looking good. As we can see here, the fund’s net asset value is down 3.55% since July 1, 2023:

{kind=link}

This strongly suggests that the fund is not earning enough investment profits to maintain its distribution at the current level. If this continues, there might be another cut. That certainly explains why the market is currently assigning this fund such a high yield right now.

Valuation

As of November 30, 2023 (the most recent date for which data is currently available), the RiverNorth/DoubleLine Strategic Opportunity Fund has a net asset value of $9.25 per share but only trades for $8.17 per share. This gives the fund an 11.68% discount on net asset value at the current price. That is much more expensive than the 15.91% discount that the fund’s shares have traded at on average over the past month. As such, it might be a good idea to wait and see if it is possible to get a better price, especially since the fund does not appear to be fully covering its distribution.

Conclusion

In conclusion, the RiverNorth/DoubleLine Strategic Opportunity Fund is an interesting closed-end fund that currently sports a whopping distribution yield. The fund’s incredibly high yield unfortunately suggests that the market believes that it will not be able to maintain it, and the fund’s finances and recent net asset value performance suggest the same thing. The fund’s portfolio is reasonably well-positioned for falling interest rates next year, though, so anyone buying today might be able to make some gains if that scenario does indeed play out. That is unfortunately quite uncertain right now and it is unknown whether or not the fund will manage to avoid a distribution cut. As such, it might be a good idea to wait for a larger discount before buying in, although the current price is not awful.

For further details see:

OPP: Positioned For Near-Term Rate Cuts, But Distribution Outlook Is Hazy