OPCH - Option Care Health Is Delivering The Future Of Healthcare At Home

2023-12-27 14:51:15 ET

Summary

- Option Care Health gives investors exposure to two healthcare megatrends: (i) the shift to healthcare delivery in the home; and (ii) the development of specialty pharmaceuticals.

- I believe OPCH holds a competitive moat, not only as the largest infusion provider in the US, but also due to its business model (predictable revenue and sticky client/customer base).

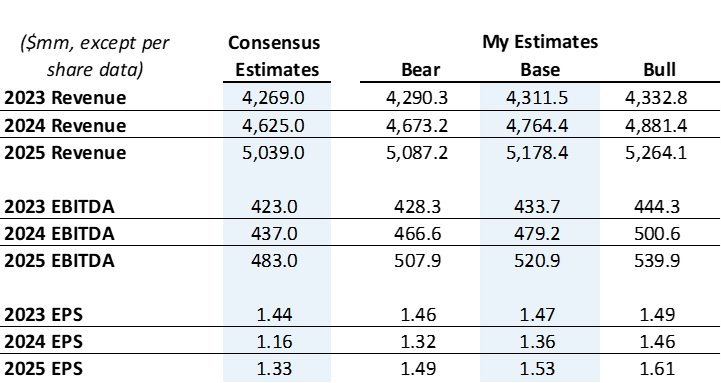

- I explain the street is highly conservative and project a ~150bps upside to FY24E EBITDA, and apply a ~15x multiple to that projection to arrive at my $38 2024 PT.

I’m drawn to Option Care Health ( OPCH ) in 2024, the leading home infusion provider in the US. There are two pivotal healthcare mega-trends that OPCH is capitalizing on: i. the cost-effective shift to home-based healthcare delivery and ii. the rapid rise of specialty medicines. With a strong operational footprint across the nation and a conservative market estimate of $15bn, I believe OPCH is in a perfect spot to further expand its market through consolidation of these trends and further boost shareholder value. My 2024 price target is set conservatively at $38, applying a 15.4x EBITDA multiple to my 2024 EBITDA estimate.

Option Care Health Explained

Option Care Health is an outpatient infusion provider, which means it offers medical treatments where patients receive medications through intravenous ("IV") or subcutaneous ("under the skin") injections, typically outside a hospital setting. This service was initiated from the acquisition of Walgreens’ infusion services in 2015. In 2019, Option Care merged with BioScrip Inc., expanding its reach in infusion and home care services. OPCH's treatment range is diverse, including nutrition support, bleeding disorders, pain management, chemotherapy, and heart failure management.

In simple words, OPCH sends medicines directly to people's homes. Imagine someone who needs medicine but can't go to the hospital all the time. OPCH steps in, sending nurses to give treatments at the patient's house. They buy these medicines in advance, store them, and then sell them to patients, usually getting paid by insurance companies. OPCH recognizes revenue when it administers the treatment to the patient. Since they deal with insurance companies, the actual cash receipt might happen later due to the nature of insurance reimbursements.

In terms of revenue, commercial payers are the backbone, contributing approximately 87%, followed by government payers at around 12%, and a small fraction (~1%) coming from self-pay patients. As of the second quarter of 2023, Option Care boasted a network of 170 locations, a notable increase from 157 in the same period of the previous year. This network includes 94 pharmacies and 76 ambulatory infusion sites, underscoring their expansive service reach.

A significant development in 2023 was OPCH's merger agreement with Amedisys, Inc., a provider of home health and hospice care, which was later terminated. The fallout of this merger led to Amedisys agreeing to pay Option Care $106mm, following Amedisys' decision to be acquired by UnitedHealth for $101/share, surpassing OPCH's offer of $97.38/share.

Further expanding its capabilities, Option Care acquired Revitalized, LLC, and Rochester Home Infusion, Inc. during the third quarter of this year. These acquisitions, specializing in specialty infusion services and in-home IV therapy, respectively, highlight OPCH's initiative to diversify and strengthen its service offerings.

My 3Q 2023 Takeaways

Option Care’s performance in 3Q 2023 reported in October exceeded analyst expectations, showing attractive growth in both top-and-bottom-line. They reported a top-line of $1.093bn, surpassing consensus and marking a YoY increase of 7.1%. Similarly, the bottom line stood at $109.8mm, up by 28.2% YoY. Year-to-date, OPCH generated $298mm in FCF, up from $207mm last year.

Management attributes the strong top-line growth primarily driven by organic expansion. This growth was led by a moderate-single-digit % (MSD%) increase in acute treatments and a high-single-digit % (HSD%) growth in chronic therapy services within its portfolio. However, the growth was partially offset by the divestiture of its respiratory therapy assets, ALS (Amyotrophic Lateral Sclerosis) treatment therapies, and services focused on pre-term labor.

Cost of sales has been controlled well – revenue growth outpaced COGS thanks to strategic pricing, improved utilization of infusion suites, and efficient procurement strategies. This is reflected in the YTD GP margin of 23.1% vs. 21.8% last year. However, SG&A says a YoY rise of 10% - this increase is primarily due to the broader labor inflation trend in the healthcare sector.

I Believe Option Care Has A “Moat”

1.0 OPCH is the industry leader in independent providers of home and alternate site infusion services. This gives them a competitive moat in terms of scale and reach – their network consists of over 170 locations, including pharmacies and ambulatory infusion sites, allowing for widespread service availability, a key differentiator in the healthcare sector in my view. Additionally, OPCH’s history of strategic acquisitions not only enhances its service offering and geographic presence but also further consolidates its industry, giving it a competitive advantage. For example, their purchase of Revitalized and Rochester Home Infusion this year expanded their specialty infusion services and in-home IV therapy. Yes, expanded services but it also deepened its market penetration.

2.0 OPCH has a sticky customer/client base with predictable revenue , covering a wide range of treatments from nutrition support to complex chemotherapy and heart failure management. This not only broadens their client base but also reduces dependency on any single service line. Additionally, with ~87% of its revenue coming from commercial payers, OPCH has established strong relationships with insurance companies and healthcare providers – I think this not only ensures a steady revenue stream but also provides a competitive advantage in terms of network negotiations and client referrals.

3.0 OPCH, while it has fixed costs, it has demonstrated significant pricing stability – Cost of sales accounted for ~79% of sales in 2021 and 2022 and is expected to account for 76.5% of sales by year-end 2023, showing a 2.5% margin expansion in <2 years. Maybe pricing power is a bit of a stretch due to the nature of their industry and business model (having to work with insurance companies) but I think over time, as it continues to grow at ~9% CAGR YoY throughout the next 3-5 years, I expect the top-line growth to continue outpacing it’s cost of sales growth moderately.

Investment Thesis

In my view, Option Care Health is well-positioned for the shift towards home healthcare, and the explosive growth in specialty pharmaceuticals, through its leading market positioning alongside pivotal catalysts. I’m confident that OPCH’s top-line estimates are underestimated by the street and I see attractive upside potential to its margins/bottom-line that is not reflected in its recent earnings revisions or valuation. Overall, I believe OPCH has the potential to not only meet but significantly exceed consensus estimates for revenue, EBITDA, and EPS in the coming years. My projections and rationale are below:

{kind=link}

Author's Data

1.0 Top-Line Growth Is Underappreciated

1.1 Shift to Home Healthcare

With home infusion therapies offering substantial cost savings, I see a growing preference for them over traditional inpatient/outpatient settings. Given the projected savings of $1,928 to $2,974 per treatment course, I believe this could lead to increased adoption rates beyond what consensus estimates are accounting for. This is a revenue tailwind (even though it’s about cost savings) because the shift represents a broader market trend that can lead to an increase in service demand, directly impacting revenue as more patients and providers opt for home infusion services over traditional settings.

1.2 Underestimated Specialty Pharma Growth

The specialty pharmaceuticals market is expected to grow at a CAGR of 35.4% by 2027, a rate that I don’t believe is fully captured in the current high single-digit growth expectations for OPCH’s top-line. I believe there’s room for OPCH to exceed consensus revenue estimates by ~100-300bps annually through the next 4 years, driven by its strong/leading positioning in this fast-growing market.

1.3 US Home Infusion Market Growth Prospects

The US home infusion market is expected to expand from $18.82bn in 2023 to $33.2bn by 2030 (8.4% CAGR). OPCH, as the largest player in this market, is well-positioned to capture a larger share of this growing pie, which I believe adds an attractive upside to consensus’ expected 8.4% and 8.9% top-line growth in 2024 and 2025, respectively.

1.4 Fragmentation and Consolidation

Given the fragmented nature of the market, OPCH’s strategy to consolidate and leverage scale could lead to an accelerated revenue story. Combining my expectations for market expansion with OPCH’s roadmap for value creation (accelerating organic growth, leveraging infrastructure, new therapies/services, and M&A), I see an opportunity for OPCH to surpass street top-line estimates by at least 2-3%, translating to potential additional revenues of $85mm to $255mm annually through 2027, based on the 2023 projected sales of $4.27bn.

2.0 Margin Expansion Projections are Conservative

2.1 Gross Margin Improvements

The cost savings from home infusion services are a critical factor in gross margin improvement. For OPCH, gross profit has increased from 22.2% in 2019 to 23.2% in 2023. I anticipate gross margin to potentially surpass the street’s estimate by 1-2 percentage points (22.6% and 22.5% GP margin estimated for 2024 and 2025), primarily due to operational efficiencies of scale. This would lead to an incremental $42.7mm to $85.4mm in gross profit based on 2023 revenue estimates. Thus, enhancing EBITDA and EPS for shareholders.

2.2 EBITDA Growth from Procurement Efficiencies

OPCH’s focused procurement strategies have already shown benefits with a $12mm to $14mm added to the gross profit line in 3Q23. If such efficiencies continue, even at a reduced rate post-2023, I believe there could be an additional 50-150bps impact on the 2024/2025 EBITDA margin (~9.5% expected by consensus in 2024/2025 vs. 9.9% in the LTM!). I believe this is conservative and that we will see an additional increase in EBITDA of $31.2mm to $63.8mm annually, which is not reflected in the $423mm EBITDA projection for 2024.

2.3 Operating Leverage from Fixed Costs

With ~80% Cost of Sales margin, any increase in revenue can significantly impact profitability due to operating leverage. I believe that as volumes grow, OPCH can continue to leverage its market position to see an improved EBITDA-Capex margin, easily pushing it beyond the $401mm expected in 2024. If this margin were to increase by just 1% more than street estimates, it would mean an additional ~$50mm to EBITDA-Capex for 2024 (which is expected to be 8.7% of sales in 2024 vs. 9.1% in the LTM ).

3.0 Market Share and Strategic Positioning

3.1 Increased Market Share through Licensing and Operations

OPCH’s licensing across all 50 states and operations in 45 states give it a broad reach that I don’t see fully appreciated in the stock price or street estimates. With the expected increase in the home infusion market size, OPCH’s expansive footprint should continue to capture additional market share, which I believe should add ~150bps to its 2024 top-line, or ~$60mm in additional revenue.

3.2 Focused M&A Strategy

Post the Amedisys acquisition attempt, a pivot to smaller, more strategic acquisitions could lead to better-than-expected synergies and integration efficiencies. These acquisitions, as mentioned earlier, consolidate the industry to bolster market share and pricing power. I have no rational estimate for these potential synergies, but due to the smaller scale of the acquisitions, it could range from 0-100bps to the bottom-line margin.

3.3 Underestimation of Strategic Positioning

I don’t believe Mr. Market is valuing OPCH’s strategic initiatives and how they contribute to market share gains. I expect that OPCH’s targeted approach in deleveraging, adding new therapies, integrating its recent acquisitions, capitalizing on its unique platform, and expanding its infusion suite footprint should continue to lead to upward EPS revisions and beating EPS estimates by at least $0.1 on an annual basis, as it has done since 2019.

Valuation

Using the same projections I used above, I apply a 15.4x (reflective of its current valuation) EV/EBITDA multiple to my 2024 EBITDA estimate to arrive at an implied share price of 37.5, or an ~11% upside to today’s prices, which I find conservative due to the high-growth trajectory the company is in. See below for those calculations:

Author's Data

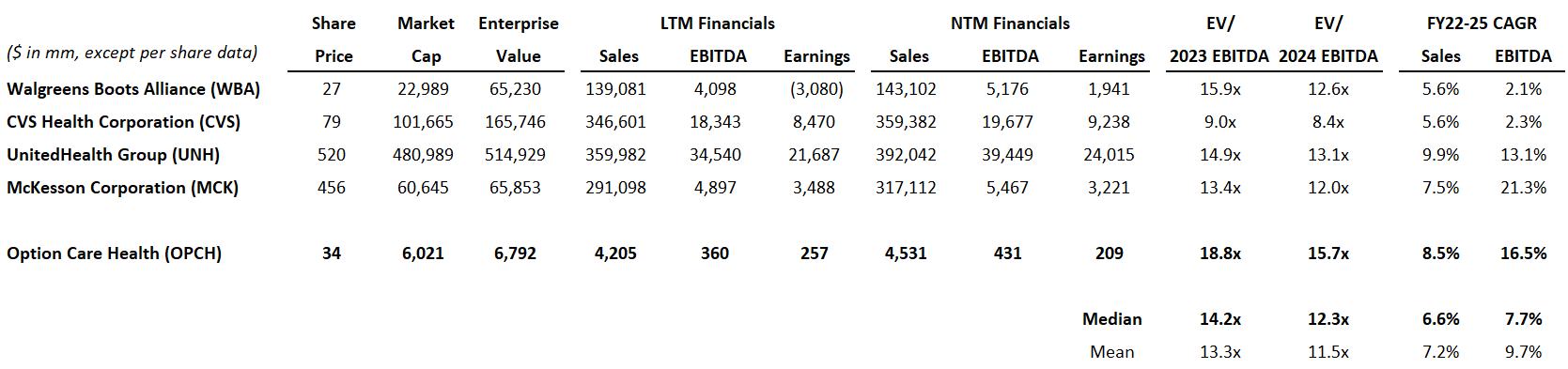

Comparable Companies Analysis

For the comps below, the main thing I wanted to highlight is the projected Sales and EBITDA growth for the competitors vs. OPCH. Option Care Health has the highest projected EBITDA growth by the street (which I have reason to believe is conservative), and thus justifies its higher valuation vs. competitors.

{kind=link}

The other thing I wanted to highlight is its competition. None of those companies specialize in home infusion services, they just have similar end-markets as Option Care. This further shows how OPCH is truly differentiated, and the industry leader. Now, this is not to say that they are in the best position possible - these companies could probably compete with OPCH if they wanted to, but it's not core to their business models (which explains why Walgreens spun off Option Care back in 2015). Finally, since CVS, UNH, MCK, and WBA are so different from OPCH, it's also not a very useful comparable analysis (since they have different business models and strategies and hardly compete with each other). Precedent transactions are also hard to find with similar business models to OPCH. However, there are precedent transactions with similar end markets - according to Capital IQ, the aggregate is ~25x TEV/ LTM EBITDA, with premiums at ~35%, which makes OPCH seem undervalued.

Risks to Rating and Price Target

- OPCH’s reliance on large insurance customers like UnitedHealth and Aetna ( CVS ), which have their own home infusion divisions, is a big risk. Changes in their network strategies would lead to market share losses.

- The multi-year, in-network agreements with these insurers are crucial. There’s a risk if these are not renewed on favorable terms, impacting OPCH’s market position.

- There is limited visibility into OPCH’s drug spread and rebate contributions. Any changes by drug manufacturers or wholesalers would impact profitability.

Bottom Line

OPCH’s commanding presence in the home infusion market, combined with its strategic alignment with healthcare mega-trends, underscores my confidence in the company for 2024 and beyond. Considering the conservative market size estimates and OPCH’s potential for growth through industry consolidation, I initiate a buy rating with a $38 price tag on OPCH for 2024

For further details see:

Option Care Health Is Delivering The Future Of Healthcare At Home