OPCH - Option Care Health: Market May Be Under-Reflecting Critical Factors Reiterate Buy

2023-10-18 11:00:00 ET

Summary

- Option Care Health has had a stellar run in '23, backed by robust fundamentals and growth rates.

- Recent pullback has opened the gates for additional allocations for long-term positioning.

- The market may be under-reflecting critical factors in OPCH's business returns at its current appraisal of the company.

Investment briefing

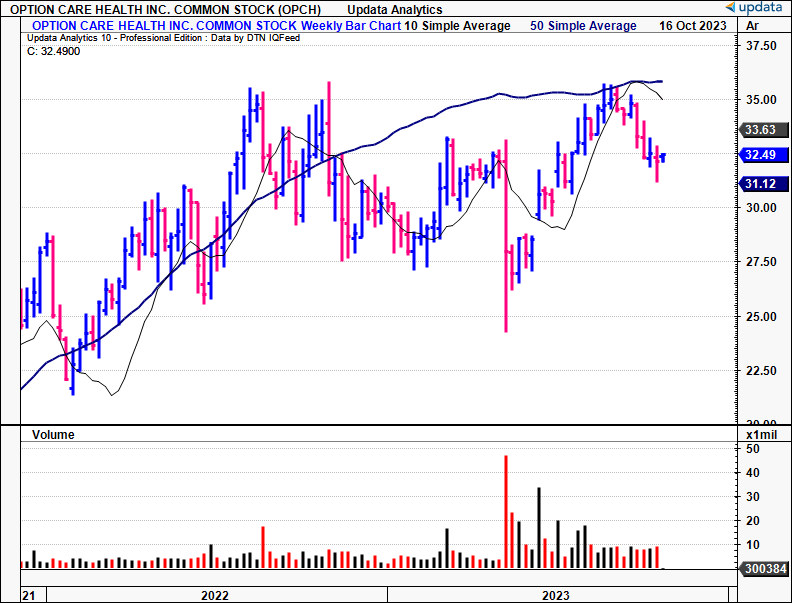

Option Care Health ( OPCH ) continues to offer prospects to unlock long-term risk capital based on the latest assessment of facts. Since my March publication , the company has caught a further bid, and withstood market pressures well. It nudged its 200DMA around 10 weeks ago before consolidating back to range, and my estimation is the next few weeks are critical to the company's prospects in FY'23 and beyond.

The last few publications on this channel have scrutinized OPCH's economics with great analytical rigour. What's critical now, is, at its current market value, what is required for this to make sense, and if there's any scope for these expectations to change.

This report will analyze the following investment facts:

(1). Price-implied expectations on growth, business returns, earnings reinvestment and intrinsic value,

(2). OPCH's business returns and projections,

(3). Comparison of required rates of return etc. to the business returns + forecasts,

(4). Technical considerations,

(5). Valuation(s).

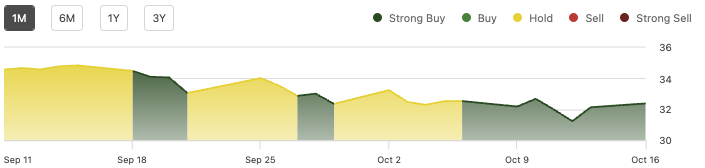

It's also worth noting the Quant system continues to rate OPCH a strong buy based on everything except valuation. It's worth understanding why this is so as well. Finally, Stan Druckenmiller's Family Office, Duquesne, added to its OPCH position, increasing its stake from 804,000 shares to ~4.4mm, as a vote of conviction for the company.

Net-net, I continue to rate OPCH stock a buy for the factors raised in this report.

Figure 1.

{kind=link}

Critical facts pattern underlining reiterated buy thesis

(1). Price implied expectations

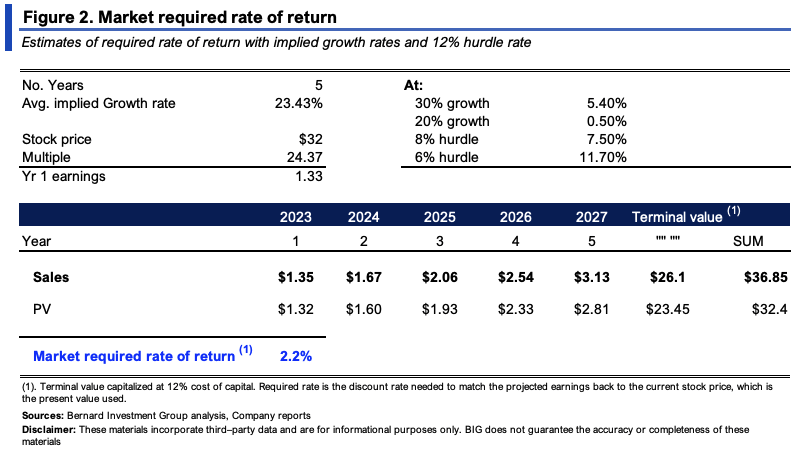

Being that we're in Q4 2023, markets are looking out to 2024 and discounting expectations from this point at the minimum. Consensus expects ~10% YoY decline in earnings next year for OPCH. But from FY'23—'25, it forecasts an average 23.4% bottom-line growth.

Further, with OPCH selling at ~$32–$33 at a 24.37x forward multiple , the market expects $1.33/share in earnings this year, whereas at 19.7x forward EBIT, it is looking at $329.40mm in pre-tax income, 37% YoY growth. This is what's already priced in.

A c.23% earnings growth rate is reasonable to project out to FY'28. After this, I've capitalized the continuing value at our 12% threshold margin (this reflects 1) internal requirements, and 2) long-term market averages). The market's required rate of return is the discount rate needed to discount these estimates to the current market value at the time of writing. You can see it is 2.2% under this convention, ranging from 0.5% to 11.7% under various scenarios.

This implies:

(i). Low level of expected risk priced into OPCH's current market values,

(ii). Low required return compensating for the risk + predictability of cash flows.

The stock trades at 2.5x EV invested capital at a trailing ROIC of 8.8% (discussed later). The expected ROIC is therefore 3.5% (1/(2.5x0.088) = 3.5%), and anticipated reinvestment from here (RI = g/ROIC) is just 10% or ~$33mm. The market therefore expects OPCH to compound its intrinsic value at 0.35% going forward. This is tight, and could explain the recent reversal in equity value.

{kind=link}

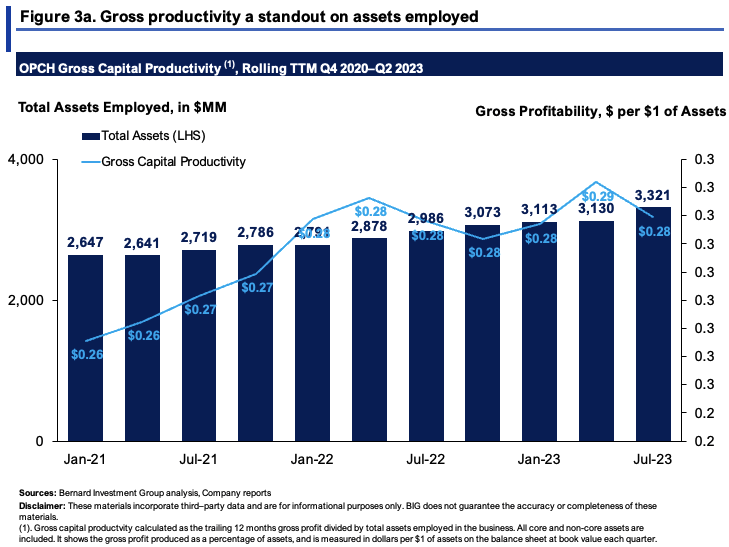

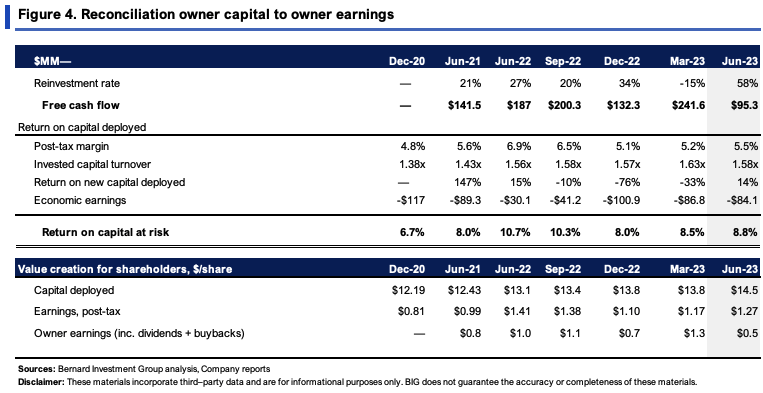

(2). Business returns + projections

The company has increased assets employed on the balance sheet to $3.2Bn as of Q2. On this, it rotated back $0.28 in gross per $1 in assets, up from $0.26 in 2020 (Figure 3a). Here, all core and non-core assets are included to gauge total asset efficiency.

{kind=link}

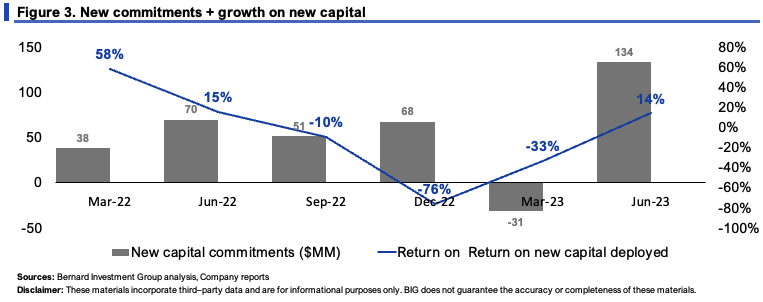

OPCH continues its reinvestment back into the business as well (Figure 3):

- Since Q1 '22, it has recycled net $329mm back into operations, vs. $196mm of maintenance CapEx, thus $133mm of growth investment.

- Last period it allocated $134mm vs. $29mmm of maintenance capital charge.

Returns have been cyclical on these investments, but returned 14% in profit last period, having grown post-tax earnings by that amount.

{kind=link}

It had $14.50/share of investment required to run the business in Q2 as well, which produced $1.27/share in NOPAT (TTM values), 8.8% return on investment.

This is below FY'22 highs, but well above 2020 range. Since 2020 in fact, it's invested ~$2.30/share to grow, expanding post-tax earnings by $0.41/share, or 20% incremental return on capital.

Critically, capital turnover drives the business returns for OPCH, at post-tax margins are single-digits, whereas capital turns is 1.6x–1.8x on average.

{kind=link}

(3). Comparison of business returns (inc. projections) to market-implied expectations

The comparisons are easily made between market expectations vs. OPCH's propensity to outpace these. To summarize:

- Market expectations:

- 37% growth in pre-tax income to $329mm,

- 3.5% ROIC and 10% reinvestment of pre-tax earnings,

- Required rate of return of 2.2% (ranging from 0.5%–11.9%),

- For OPCH to compound intrinsic value at just 0.35% by for FY'23 remainder.

- OPCH business returns:

- Cyclical return on incremental capital, at 14% last period,

- Heavy growth investment on a persistent basis, ranging from 20–60%,

- 8–9% return on existing capital deployed.

It also compounded sales at 3.1% per period the last 3 years, on stable average margins of 6.5%. Positively, the bulk of capital allocation is to NWC vs. fixed assets. Each new $1 in sales took $0.28 in NWC, whereas it reduced its fixed capital intensity by $0.03 on the dollar. ($0.10 was allocated to M&A as well).

These are reasonable estimates to carry forward. Management calls for 9% YoY growth in sales this year—another 3% if you factor in we are in Q4 already. I'd call for fixed asset intensity of 2% on each $1 in sales growth moving forward.

Under this convention:

(i). OPCH would need to invest $39—$44mm per quarter ($160–$176mm annualized), not far off the market's view of $33mm in Q4.

(ii). But pre-tax earnings could reach $275–$312mm, $228–$260mm post-tax, otherwise 8–9% return on existing capital.

(iii). The returns on incremental capital could push to 18% on average over the coming 12–24 months.

(iv). It could therefore compound its intrinsic value at an average 3% each period going forward out to FY'24/'25.

Note, this is above the market's required rate of return and expectations of intrinsic value growth. In my view, there is scope for further upside based on this dislocation to market implied expectations.

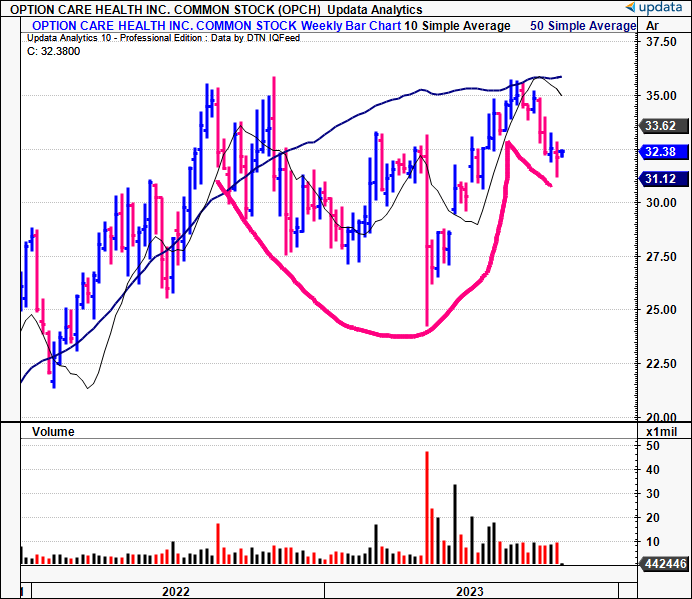

(4). Technicals are mixed

Leading into earnings season market technicals become increasingly important to gauge sentiment and investor positioning. Directional moves can be captured early in this fashion.

Several points are worth noting here:

- The pattern from 2022–'23 has formed a wide cup with handle after the latest pullback.

- What's needed is a break from here to see prices reach the pivot point and trade to new highs, at which point this could be a bullish factor.

Figure 5. Wide cup with handle, yet to create pivot point to new highs

{kind=link}

Money flows have also been positive into OPCH for the bolus of FY'23. This is important as it shows investors remain net long the stock, providing demand needed to see it trade higher with the right catalysts.

Figure 6. Money flows into/out of OPCH equity across '22/'23

Data: Updata

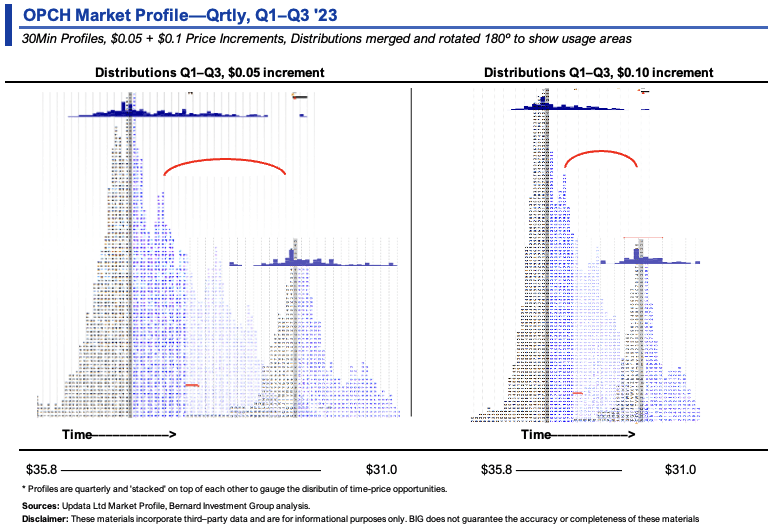

This is critical information when examining the market profile for OPCH across Q1–Q3, as seen in Figure 7. Markets tend to move from areas of high usage to low usage. You can see the high usage in the figure below, around the $34–$35 region. There is risk, therefore, we could see a vacuum to fill the distribution in the low usage areas shown. With the recent pullback over the last 10 weeks, this does make some sense.

Figure 7.

Data: Updata

This is shown in an alternative view by rotating the profile on its axis to present the distributions in a more comprehensive view (Figure 8). This is a positively skewed market trading OPCH and there is scope to see investors complete the distribution seen across '23 into a more normal fit. This implies:

- Potential for incremental, small losses until the distribution is filled,

- With a few larger gains once this is completed.

In my opinion this supports a long-term view to remain bullish.

Figure 8.

{kind=link}

The point and figure studies are also looking to the $33 region. These are based on objective formulae provided by the studies. Again this corroborates a potential filling of the distribution between $31–$35, meaning OPCH could continue trading sideways around an area of value for the time being.

Figure 9.

Data: Updata

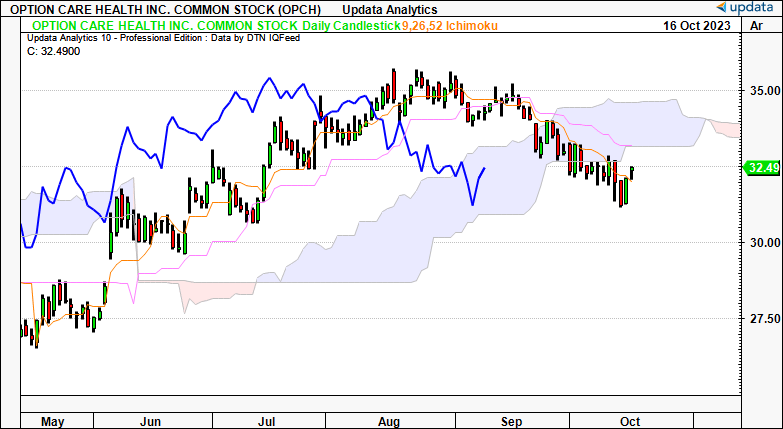

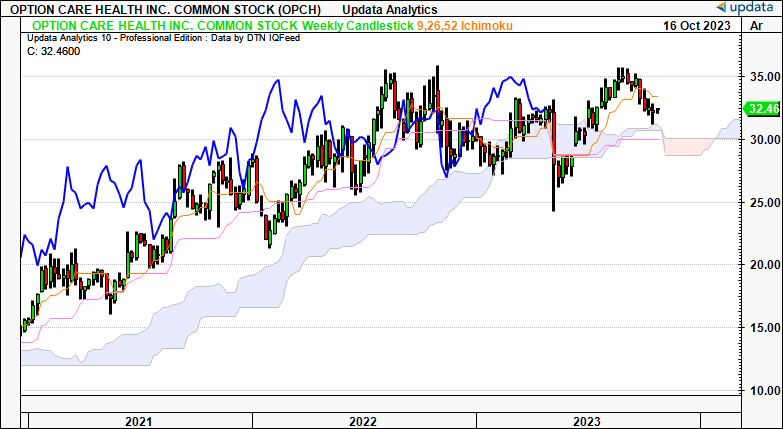

As to the trend action, daily studies are unsupportive over the coming weeks of trade. This is something to consider heading into OPCH's Q3 earnings. Both price and lagging lines are beneath and into the cloud, respectively. A break to $34.00 is needed to reverse this picture.

Figure 10.

{kind=link}

Weekly frames, looking to the coming months, are more constructive. Here, we remain within the long-term uptrend, and a consolidation to $30–$31 could be accepted before turning more neutral over the coming months based on this.

Figure 11.

{kind=link}

(5). Valuation

The stock sells at 23.7x forward earnings and ~20x forward EBIT as mentioned. The former is ~2 points ahead of my last publication. It also trades at 25x NOPAT at the time of writing with a $5.78Bn market value (5,780/229 = 25x). It also compounded post-tax earnings at 14% from its incremental investment last period, calling for $261mm in NOPAT moving forward. This aligns with the market's $329mm in projected EBIT adjusted for a 20% tax rate—more than reasonable. Assuming the same 25x multiple, the company warrants a $6.53Bn market value (261x25= $6,526), or 13% value gap.

Note this is (i) higher than the market's required rate of return, and (ii) than its estimates on OPCH's capacity to compound intrinsic value. These factors are further support of a buy rating in my opinion. As mentioned earlier, the quant system has full support of this buy rating with the latest pullback in market pricing, as seen below.

Figure 12.

{kind=link}

Discussion summary

There appears to be a dislocation in the market's expectations priced into OPCH's equity value and the propensity of the company to outpace these. In my opinion, OPCH can continue to catch a bid based on its reinvestment activity, and the incremental rates of return it is producing on these investments. Market technicals are mixed, and a short-term consolidation is not out of the question either. Long-term however, OPCH remains on track to continue its ascent with a set of attractive economics and the potential to surprise against market-implied expectations. Net-net, reiterate buy.

Key risks to consider:

- Broad macro risks cannot be ignored, including the rates/inflation axis. Rates in particular are driving capital flows at the present.

- Geopolitical risks could have either upside or downside risks on global markets.

- OPCH's upcoming earnings may also disappoint, leading to a revision to some of the numbers presented in this thesis.

Investors must realize these risks in full before proceeding further.

BIG Insights

For further details see:

Option Care Health: Market May Be Under-Reflecting Critical Factors, Reiterate Buy