OPCH - Option Care Health: Profitability Returns On Capital Attract Buy Rating

Summary

- Double-digit growth in core business segments, coupled with strong FCF conversion.

- Profitability remains strong, a good springboard for its growth initiatives for FY23'.

- Multiples are justified, I price OPCH at 21x forward EBITDA.

- Net-net, reiterate buy.

Investment Summary

Looking to the latest numbers from Option Care Health, Inc. (OPCH) for its Q4 and FY22' period , it was pleasing to observe double-digit growth vertically down the P&L and strong free cash conversion below the bottom-line. In the previous publication on OPCH I reiterated the stock as a buy given the growth trajectory it was on in its divisional performance and the return it is seeing on its invested capital. To use CFO Mike Shapiro's language on the call , OPCH is "in investment mode" and is constructive on the potential of its infusion suite strategy as a mid-term growth lever into FY23' and beyond. The global infusion therapy market is poised for substantial growth over the coming decade, with market research forecasting a CAGR 11% to $81.5Bn into FY32', driven by outsized growth in the APAC region and substantial upside in the specialty pharmaceuticals segment of the market. This is key given the company's recent acquisitions made last year, plus its efforts in expanding its footprint of infusion centres. Further, the company is looking to another double-digit period of growth this year at the upper end of guidance and given the factors discussed in this report, I'm reiterating OPCH as a buy at a $42-$45 price range.

OPCH weekly price evolution, FY21-date

{kind=link}

Before continuing, you might want to check out my last two publications on OPCH:

Closer look at OPCH fundamentals

As mentioned it was a noteworthy growth route OPCH embarked on in both Q4 and across the entirety of FY22'. Q4 revenue came in-line at $1.02Bn with upsides versus consensus at the bottom-line with EPS of $0.26. Looking at its full-year numbers, the company clipped $3.94Bn in top-line sales, growing turnover by 14.7% for the period on adj. EBITDA of ~$343mm, up 18% YoY. Moving down the P&L, it saw a gross margin of 22.5%, recognizing YoY gross profit expansion of 11.2% to $867mm, and operating income of $240mm or 6.1% of turnover. The company wasn't immune to cost-inflation over the last quarter, absorbing a c.$15mm headwind to operating margin from the increase in expenditures. It pulled this down to earnings of $150mm for the year, clipping $0.83 in GAAP EPS for the period.

On face value the company's thin margins could be a potential cause for concern. However, two points I'd raise to push back on this:

- Despite an increasing cost of revenues, the company has continued to realize an uptick in core EBITDA and FCF margin over the last 2-years to date. Here I took rolling TTM periods to illustrate the same [Figure 1] and noted that income is still feeding down the P&L, with substantial TTM earnings growth from negative $86mm in FY20' to $150.6mm in the last 12 months.

- Cash flows haven't been impacted as a result of this, with CFFO driving sequentially higher on a rolling TTM basis over the last 2-years to date as well - in Q2 FY20', TTM CFFO clipped $70.5mm, in FY22', it clipped $267.5mm, a 279% overall increase.

Fig. (1)

Note: Rolling TTM periods are used. (Data: Author, data from OPCH SEC Filings FY20-22')

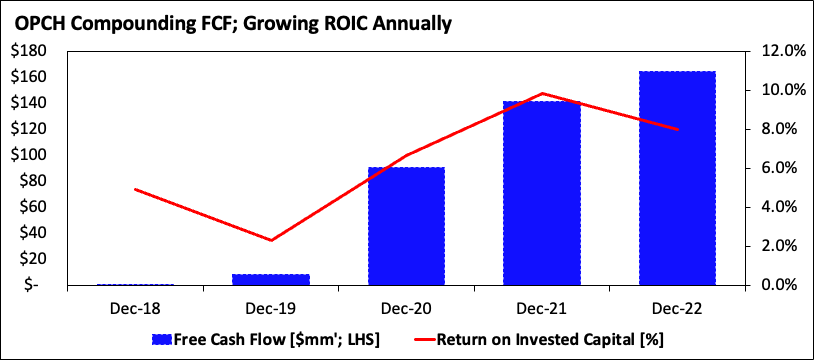

Extending from the above points, I'd also touch on the CFO's language from earlier, in that the company is in 'investment mode'. This is an important factor for consideration, because it finished the year with $164mm in FCF and has been compounding this figure for the last 5-years [Figure 2]. At the same time, it has maintained a strong ROIC profile by growing the return on its capital investments to 8% in FY22. Understandably, this performance becomes relevant as a measure of the company's ability to generate incremental return on its investments for future growth. Notably, the company completed the acquisition of Specialty Pharmacy Network last April, and has been investing diligently in growing its infusion centre network. To illustrate, it opened another 22 ambulatory infusion centres over the year, now boasting ~150 sites. From this, it added another 63 infusion chairs, bringing the total on its books to >575. The net effect of this is that it brings more visits and therefore more revenues in for the company. Very importantly, the incremental ROIC OPCH has generated since FY18 lands at 10.65% - ahead of the annual returns on capital over this time, as seen below - thereby illustrating its new centre openings and acquisitions have generated additional profitability and top-line growth, rather than act as a drag on the same. It plans on adding another 20 sites this year, hence, if it can at least hold an 8% return on these investments there's a good case to be made for its ability to drive earnings to the bottom-line in years to come.

Fig. (2)

{kind=link}

FY23 guidance looks to another reasonable growth period

Management are constructive on the outlook for FY23', calling for 11% YoY growth at the upper end of guidance with a $4.375Bn revenue projection. Notably, it expects a sizeable pullback in its ALS and high-risk pregnancy exposure, baking in a 200bps headwind as a result of this. On this forecast, it looks to $370-$390mm in adj. EBITDA, calling for 14% YoY upside at the upper bound, and also recognizes a potential 510bps headwind from inflationary impacts to its operating costs. In my estimation, the key performance indicator will in terms of profitability , and we'd need to see the company maintain its reasonably high ROIC and a c.11.5% ROE in order to maintain a buy case. The key point is that it has been generating growth in FCF, and compounding the incremental ROIC over time, a trend that I'd be benchmarking OPCH against this year. As mentioned above, it looks to add another 20 sites to its portfolio this year, so the return on this investment will be critical in order to continue driving value for shareholders into the coming 12-24 months by estimation.

Valuation and conclusion

Because of the profitability factors outlined above I continue to see OPCH generating value in the coming periods. Still, the stock is trading at a premium to peers at 21x trailing CFFO, and 37x trailing P/E. Coupled with growth in the underlying infusion care market, and given the company's standing within said market, I do opine that it should trade at a premium to the industry. Looking at its 21x EBITDA multiple and assigning this to management's EBITDA range of guidance derives a price target of $42-$45, around another 40-50% upside potential on today's market value. These are attractive numbers in my estimation and call for a buy rating.

Net-net, the combination of momentum OPCH has exhibited to date, coupled with its forward-looking growth numbers, are supportive of a buy rating in the best estimation. Profitability is a key standout for the company, especially with its increasing FCFs that can be put to effective use in its strategic growth initiatives. I see the stock trading with further valuation upside to a 21x forward EBITDA multiple, otherwise $42-$45 apiece. Reiterate buy.

For further details see:

Option Care Health: Profitability, Returns On Capital, Attract Buy Rating