ECCV - Our Picks In The Niche 7-10%-Yielding CLO Equity Senior Security Sector

2023-05-18 13:09:52 ET

Summary

- The CLO equity senior security sector is easy to overlook, but it has a number of attractive features such as high yields, strong asset coverage levels and mandatory maturities.

- We review the sector, the most common pitfalls, and discuss a couple of head-to-head comparisons.

- Finally, we provide a detailed risk/reward summary and highlight our picks.

This article was first released to Systematic Income subscribers and free trials on May 11.

In this article we update our view across the CLO Equity senior security space. Specifically, we look at baby bonds and preferreds of investment funds (both CEFs and BDCs) that allocate primarily to CLO Equity securities.

Although these securities don't have the double-digit yields of their common share counterparts, they do offer high single-digit yields as well as much lower volatility and stronger protections. This is why they continue to be part of our Income Portfolios.

First we highlight the attractive features of this part of the market. We then do a quick survey of the different ways investors can allocate their capital, run a couple of head-to-head comparisons and discuss the various common pitfalls. Finally, we round out the article by looking at the risk/reward on offer across the sector and highlight our picks.

Why CLO Equity Senior Securities Are Worth A Look

The CLO equity senior security sector is a niche area of the broader income sector. It includes preferreds and baby bonds issued by investment funds (both CEFs and BDCs) that primarily allocate to CLO Equity securities.

What makes the sector attractive is not just the risk/reward on offer but also a number of additional factors. Specifically, because CEF and BDC sectors are relatively bifurcated (few income investors are well-versed in both sectors), there are greater relative value opportunities than in other parts of the income market. And because the key risk metric investors use (i.e., asset coverage) is somewhat misleading, it's easy for investors to go astray. Both of these factors generate a significant amount of alpha for investors willing to put in the work.

The preferreds and baby bonds of the various CLO Equity funds tend to be overshadowed by their common shares which deliver incredible yields at an even more incredible volatility. However, for investors who want to acquire income securities with attractive absolute and risk-adjusted yields, senior securities may be more appealing.

This sub-sector has a number of unusual and attractive features. First, nearly all securities have mandatory maturities, even the preferreds. This lowers their duration and makes them less negatively convex from large changes in interest rates.

Secondly, a number of securities in the sector are monthly payers, which is both attractive for many investors and understates their yield relative to the usual quarterly-paying preferreds due to the additional compounding.

Thirdly, the sector features unusual mandatory redemption features which require the funds to redeem the securities if their asset coverage remains below a given level.

Fourthly, the sector has enjoyed repeated support from fund managers who tend to repurchase shares of their preferreds and baby bonds during drawdowns (otherwise they would not be allowed to pay distributions on common shares). This not only improved the asset coverage of the senior securities but also supported their prices in the market.

Investor Options in the CLO Space

Let's go through the different investment options in the sector:

- Investors can hold CLO Equity securities indirectly via private funds / managed accounts or public funds such as CEFs and BDCs. CLO Equity CEFs include popular vehicles such as OXLC, ECC, OCCI, EIC and tend to boast very high yields of around 10-20% or so.

- Preferreds are a lower-beta and lower-risk way to allocate to the CLO Equity space with high-single digit yields.

- Baby bonds are a further up-in-quality way to allocate to the CLO Equity space. The handful of baby bonds trade at yields around 8-9%. These include ECCV, OXLCL, OXSQL, among others.

CLO Debt vs. CLO Equity CEF Debt

In this section and next we discuss a couple of head-to-head comparisons of various CLO-related assets.

We were recently asked why we don't hold any CLO Equity CEF preferreds in the Portfolios (e.g., OXLCP, ECCC etc.) and the short answer is that the bonds (e.g., OXLCL etc.) offer much better risk/reward.

CLO Equity fund baby bonds and preferreds trade at very similar yields (even from the same fund) despite the fact that the bonds have strict priority in the capital structure.

CLO Equity CEF Preferreds vs. Bonds

Another good question was comparing CLO Equity CEF bonds vs BBB CLO Debt. Conceptually, CLO equity bonds should trade at yields well above BBB CLO Debt (e.g., JBBB) but this isn't actually the case.

The bonds (e.g., OXLCL, ECCW etc.) trade at yields of roughly 9% while BBB CLO Debt has yields of around 10%. On the face of it, this doesn't make sense since CLO Equity gets wiped out before BBB CLO Debt gets wiped out. CLO Equity generally takes first losses up to about 10% of the portfolio, then comes BB CLO Debt taking losses between 10-15% and BBB CLO Debt starts to take losses starting at around 15% of the CLO loan portfolio.

However, CLO Equity CEFs are not static securities. Unless losses happen extremely quickly, CLO Equity can actually benefit from loan weakness because it can reinvest repaid loans into other loans trading at depressed prices (when large losses happen or are feared to happen, loan prices will tend to drop sharply as well).

Every loan bought at 70% that repays its principal offsets the loan that defaults (with a 70% recovery). The second thing that helps CLO Equity CEFs (and by extension CLO Equity CEF debt) is that the fund will tend to deleverage (in order to keep leverage from blowing up) and this means selling assets and buying back debt. This obviously helps the debt by reducing exposure and increasing asset coverage.

Pitfall #1

In this section and next we take a look at a couple of pitfalls when analyzing CLO Equity senior securities.

Most investors who have a go at gauging the risk profile of various securities in the sector look to asset coverage - a measure of the amount of total assets relative to the principal/liquidation preference of a given security.

The problem with asset coverage is that it is a poor proxy for relative risk of various securities. This is because it takes no account of differences in leverage, portfolio composition, and most importantly in the case of preferreds, the amount of debt in the capital structure.

In other words, asset coverage treats debt and preferreds the same and ignores the fact that debt has a more senior claim on the fund's assets than do the preferreds. So while asset coverage can be a sensible metric to use for debt (unless there is both unsecured and secured debt, which is rare for these funds), it can be highly misleading for preferreds.

It is obvious why a preferred with higher asset coverage but greater leverage in the portfolio and a higher allocation to CLO Equity may not actually be the "safer" option. However, the issue of the amount of debt in the capital structure is a bit more nuanced.

To illustrate how the preferred asset coverage metric can be misleading for a fund with debt in the capital structure, consider the following table.

Systematic Income

Source: Systematic Income

Here we have two funds: A and B, both of which hold $300m of assets and $100m of financing. Fund A financing is $50m each for debt and preferred while fund B financing of $100m is entirely in the preferred. The preferred asset coverage is 3x for both funds.

Now consider what happens in a stress test where the fund's assets suffer a 75% collapse, i.e., the asset recovery rate is 25%. In this case, both funds now have $75m of assets. However, fund A preferreds fair-value is 50% ($75m of total assets less $50m owed on the debt = $25 leftover for preferreds relative to the $50m liquidation preference).

On the other hand, fund B preferred fair-value is 75% because there is no debt to pay off ahead of the preferreds and the full $75m can go to service the $100m of the preferreds liquidation preference.

The key point here is that while the preferreds asset coverage is the same, the actual outcome for the preferreds can be very different. This issue is particularly relevant for this sub-sector because five of six CLO CEFs have sizable levels of debt in their capital structure and, hence, will give a misleading picture of asset coverage for the preferreds.

Pitfall #2

Something else to be aware of is that because all the securities in the sector except for two have mandatory maturities, the usual stripped yield (i.e., current yield) calculation is entirely useless. In other words, the yield equal to the coupon/price will give a very misleading picture of the actual yield particularly since most securities in the sector are trading well below "par".

The fact that the securities in the sector have both issuer redemptions and maturities requires investors to do some fiddly calculations to estimate the "real" yield of these securities i.e., their yield-to-maturity, yield-to-call and yield-to-worst.

Takeaways

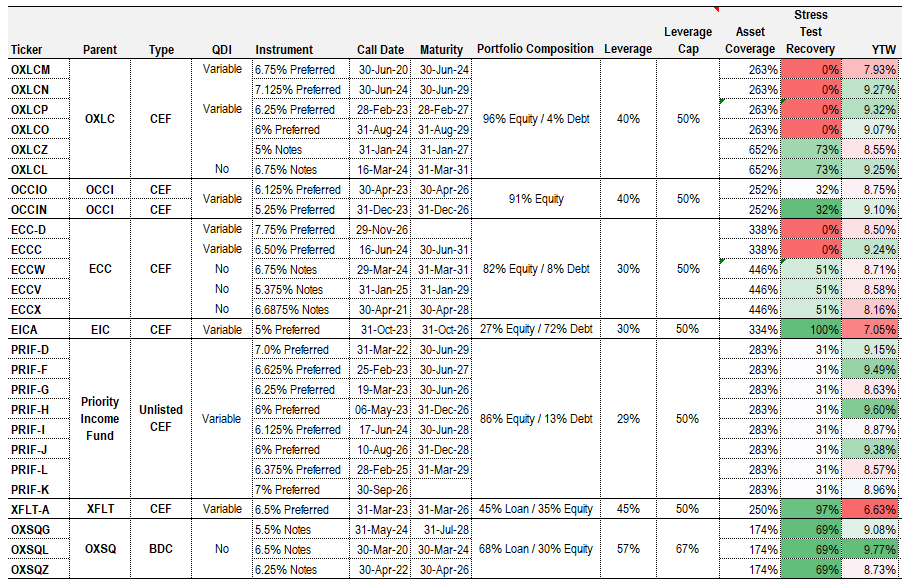

This is what the CLO Equity senior security space looks like at the moment.

The table below shows the various preferreds and baby bonds in the sector alongside the key data such as call date, maturity, and portfolio composition.

{kind=link}

Systematic Income

The key risk metrics are leverage, asset coverage, and Stress Test Recovery - our own calculation. Finally, there is the ever-important yield (i.e., yield-to-worst or YTW) figure.

The Stress Test Recovery is based on a very tough scenario where CLO Equity securities are valued at 10% and CLO Debt securities are valued at 40%. In our view, it provides a much better way to gauge risk than the more popular asset coverage metric.

If we combine this metric with yield we get the chart below. The highlighted quadrant is the "good quadrant" of high Stress Test Recovery and high yield.

Systematic Income

The chart shows that the sector does not differentiate a whole lot between securities with low and high Stress Test Recovery. This is a good thing as it allows investors to tilt to stronger securities without giving up much yield (except in the case of the strongest securities such as EICA and XFLT.PA).

The chart shows why we continue to favor two security suites in the sector: CEF OXLC baby bonds (e.g., OXLCL) and BDC OXSQ baby bonds (e.g., OXSQL), trading north of 9% yields. For more defensive portfolios we also like EICA and XFLT.PA.

For further details see:

Our Picks In The Niche 7-10%-Yielding CLO Equity Senior Security Sector