ECCV - Oxford Lane Baby Bond: A Misunderstood 8.93% YTM Bargain

2023-11-03 12:00:00 ET

Summary

- Oxford Lane Corporation’s baby bond is misunderstood and offers great value.

- These bonds have an 8.93% yield to maturity and a relatively short maturity of 1/31/2027.

- Given the massive coverage (extremely low leverage) of OXLC’s bonds, the yield is extremely high relative to the bond’s safety.

- Although unrated, I consider OXLCZ to be investment grade quality making this bond extremely undervalued.

- Another very attractive baby bond in this space is from Eagle Point Credit with the ticker ECCV, but I believe the whole space is undervalued.

Oxford Lane Capital

Company Website

Oxford Lane ( OXLC ) is a closed end fund ((CEF)) that invests almost exclusively in the equity tranches of collateralized loan obligations (CLOs). These investments can be volatile and they do carry risk.

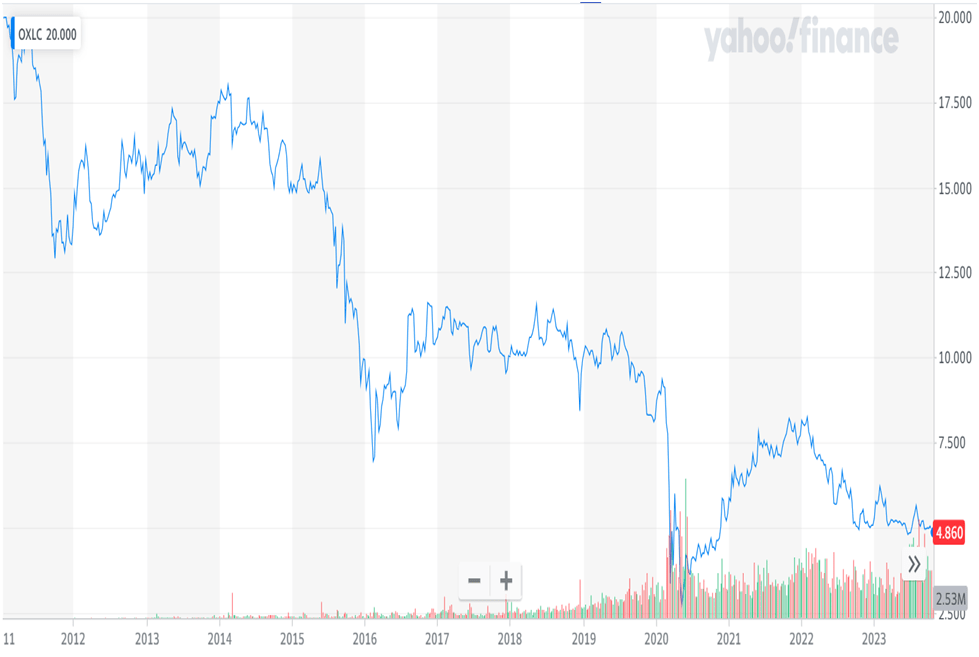

OXLC's track record for common stockholders has not been great. Here is the chart since inception.

{kind=link}

OXLC is a yield chaser's dream and a long term investor's nightmare. While OXLC's common stock generally offers very high yields, it has lost more than 75% of its value since inception which has led to a poor total return. I consider OXLC a trading stock at best, and people who have tried to pick the bottom just keep getting smacked in the head. The high fees extracted by their external manager is also a huge hurdle for producing a good total return for investors.

But their fixed-income securities, baby bonds and term preferred stocks, are excellent investments. They offer a high oversized yield with very little chance of default. Whereas with the common stock, principle has been decimated, that has never been a problem for their fixed-income securities and don't expect it will be a problem in the future. I will explain later why I consider their bonds, in particular, extremely safe.

OXLCZ Baby Bond

Current Price $22.43

Yield To Maturity 8.93%

Maturity Date 1/31/2027

Why I Consider OXLCZ Extremely Safe

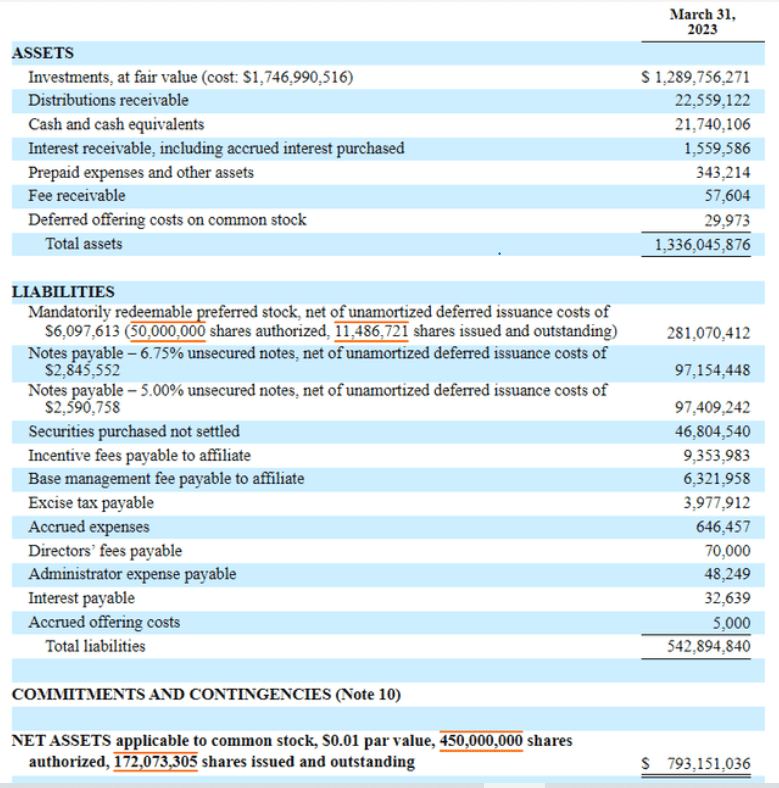

First , the leverage is incredibly low. Here is the balance sheet of OXLC from its most recent semi-annual filing.

{kind=link}

As you can see under liabilities, there are 2 notes payable, OXLCZ and OXLCL, each $97 million in size at par. So there is a total debt of $194.5 million at par and actually less than that at the current prices of these 2 baby bonds. But we will use the higher $194.5 million. This $194.5 million is covered by $1336 million in assets for a coverage ratio of almost 7 times. In theory $793 million of common equity would have to be wiped out and then the $281 million of preferred stock would have to be wiped out before the bonds would have any impairment at all.

Maybe a better way to look at this is looking at leverage. The 2 OXLC bonds have a current market value of $175 million and OXLC has assets of $1336 million. Thus leverage is only 13.1%. That is an extraordinarily low leverage. And don't forget that OXLC's 2 baby bonds are at the top of their capital stack. OXLC has no secured debt nor any borrowings on a line of credit. That adds to their safety.

Second , because OXLC is a CEF it has leverage limits by law. OXLC cannot issue debt and preferred stock greater than 50% of their assets. So how does one go bankrupt when their assets are always at least twice their debt? They don't. A CEF has never gone bankrupt because of these strict leverage limits. These leverage limits are even stricter than BDC leverage limits and part of the reason why you see many preferred stocks from CEFs given an "A" credit rating. And to make the situation even better for OXLCZ, bond leverage cannot exceed 33.34% of assets so the leverage limits on the bonds are even stricter than their overall leverage limits.

Third , if a CEF breaches the 50% leverage limit (or the 33.34% leverage limit on their bonds) they must issue more stock to raise cash to bring the leverage limit back down. OXLC is expert in selling common stock on the open market. OXLC common stock seems to always trade at a premium to NAV and thus OXLC gets very good prices when they issue stock.

Seeing the common stock chart might look worrisome as the company has lost 75% of its value, but the company is actually much bigger now than it was when it was trading at $20.00 at its inception. So the coverage of their preferred stock and bonds has not diminished at all despite the huge drop in the common stock price.

It is interesting to note that when OXLC issued its first annual report in 2011 it had only 1.9 million shares outstanding. It its most recent report shows them 172 million shares. So there is 90 times more shares and thus, despite the huge drop in stock price, the market value of OXLC is 22 times greater now than it was. This is great for their fixed-income investors and for the external managers of OXLC.

Fourth , OXLC likes to keep their leverage safely below the 50% legal limit so whenever their assets drop some in value, they simply issue more stock to bring it leverage comfortably below 50%. As you can see from the above balance sheet, overall leverage is around 40% which is where they tend to keep it.

Relative Valuation

First off, I want to say that I consider all fixed-income securities from CLO CEFs to be considerably undervalued. I believe that many people see the letters "CLO" and turn away from these securities just assuming they are risky. And this lack of understanding of all the protections that CEFs have is not understood. In my opinion the fact that these CEFs invest in CLOs almost doesn't matter for buyers of their fixed-income securities. So for me, it is not a matter of whether or not to buy these securities but it just a matter of which one is the most undervalued and best to invest in.

Personally, I consider OXLC's baby bonds investment grade for the reasons stated above about why these bonds are so safe. They are not rated but you shouldn't make the mistake of assuming unrated securities are more risky. In my experience, unrated securities provide the best values in the market. They are automatically dismissed by many investors and institutions but if you do your own homework, here is where the bargains are.

I also think the letters "CLO" scare people who don't understand the structure and leverage limits and thus their bonds tend to be very undervalued. Personally, the largest allocation in my portfolio are in the term preferred stocks and baby bonds from CLO CEFs like OXLCZ.

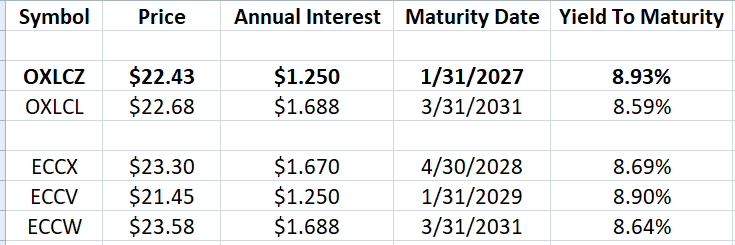

OXLCZ Versus Other CLO CEF Baby Bonds

{kind=link}

As I wrote earlier, I believe all CLO CEF baby bonds are undervalued, but which one to buy. There are 5 baby bonds issued by CLO CEFs. Two from OXLC and 3 from Eagle Point Credit ( ECC ). As you can see, despite OXLCZ having the shortest maturity and thus the least near term price risk, it is offering the best yield to maturity (YTM) of the 5. And compared to OXLCL, which has a maturity of 4 years longer and from the same company, it again looks undervalued with its higher yield. To me, this is a mispricing and thus I have a strong preference for OXLCZ. Mispricings often occur when the current yield is lower than the others and bond buyers mistakenly look at current yield rather than total return. Buying the higher current yield simply means paying more current taxes each year.

Baby bond ECC V also looks undervalued. It offers a higher YTM than ECCX , which has a shorter maturity and also a higher yield than ECCW which has a longer maturity. That makes little sense. Again it appears that investors are focusing on current yield rather than total return or YTM.

OXLCZ Versus BBB- Rated Bonds

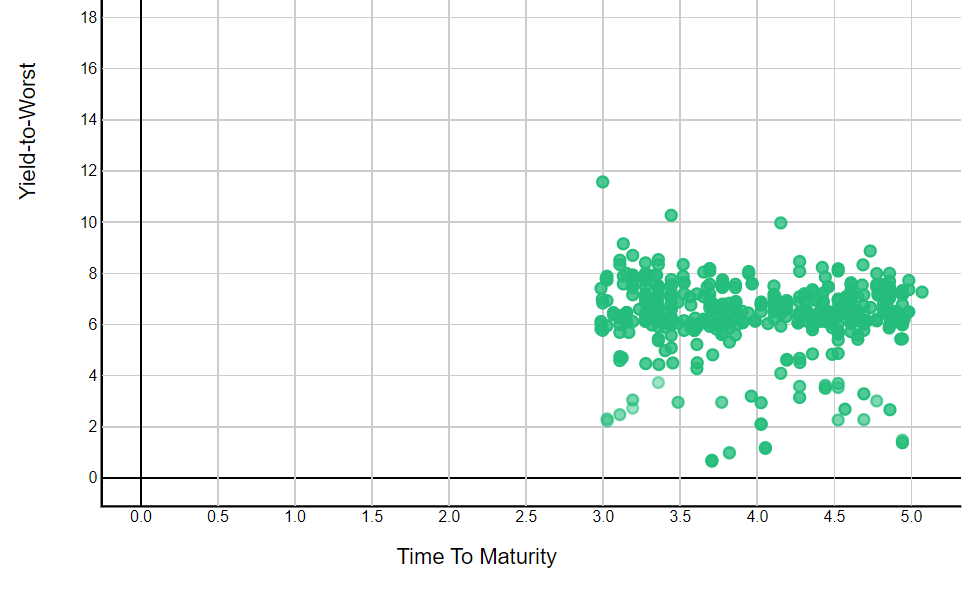

For all the reasons stated above about its safety, I would give this bond a BBB rating but we will compare it to BBB- rated bonds (1 notch lower) in order to be conservative. Here is a scatter plot of all BBB- baby bonds maturing in the 3 to 5 year range.

{kind=link}

Looking at the scatter plot, the average YTM on a 3 to 5 year BBB- bond tends to be around 7%. So the 8.93% YTM on OXLCZ is extremely good. After examining the safety of an unrated bond, putting your own rating on the bond is something I often do so that I can compare them to bonds that are rated. This is how to find mispricings. You can quibble with the rating I have given OXLCZ, but unrated bonds are generally the best bonds in the market. Institutions generally cannot buy them and retail investors tend to be very poor at pricing baby bonds. Doing your own homework on unrated bonds generally pays off big as does thinking outside the box.

Risks

In terms of risk, I see the risks here as primarily short term price risk. Prices could drop on OXLCZ and ECCV in an overall market sell off or if the common stocks of OXLC and ECC sell off. Longer term, they have their maturity dates which mitigate short term downward price moves.

For further details see:

Oxford Lane Baby Bond: A Misunderstood 8.93% YTM Bargain