OXSQL - Oxford Square Capital: Partial Redemption Of 2024 Bond Highlights Resilience Of RIC Debt

2023-07-14 06:18:44 ET

Summary

- BDC OXSQ 2024 bonds are being partially redeemed.

- We take a look at some of the dynamics of redemption.

- We discuss why bonds issued by registered investment companies or RICs deserve a place in income portfolios.

In this article we highlight the recent partial redemption of the 6.5% 2024 bonds from the BDC Oxford Square Capital Corp. (OXSQ). We also discuss why bonds issued by registered investment companies like BDCs and CEFs deserve a place in investor portfolios.

What Happened

On 22-Jun Business Development Company OXSQ OXSQL)%20(NasdaqGS%3A%20OXSQZ)%20(NasdaqGS%3A%20OXSQG)%20(the%20%E2%80%9CCompany%2C%E2%80%9D%20%E2%80%9Cwe%2C%E2%80%9D%20%E2%80%9Cus%E2%80%9D%20or%20%E2%80%9Cour%E2%80%9D)%20announced%20today%20that%20it%20intends%20to%20redeem%20a%20portion%20of%20its%206.50%25%20Notes%20due%202024" > announced it was redeeming most of its 6.5% bonds ( OXSQL ). An interesting element here is that OXSQ did a rights offering in May. The rights offering raised around $40m and, what a coincidence, the partial call of OXSQL was also for $40m. The company clearly didn't want to sell any assets to fund the redemption so they raised a bunch of equity instead.

This is all very good news for debt asset coverage since a redemption using current assets would have been worse. In the end we are going to see asset coverage rise from around 170% to 220% - a very good result.

The prompt for the redemption was very likely the fact that asset coverage has been moving lower over the last couple of years and was getting uncomfortably close to the 150% regulatory level which, if breached, would have required the company to do a number of things it clearly wasn't willing to do like suspend common dividends.

This tendency to buy back the bonds is something we have seen for CLO Equity CEFs as well. For instance, CEFs like Oxford Lane Capital (OXLC) and ECC repurchased their senior securities in previous market downturns to ensure they are still in compliance. This was a good result for senior holders as it not only improved asset coverage but also supported the price.

Occasionally, RICs retire their debt in order to refinance it. However, this wasn't the case this time as the 6.5% coupon is on par with where BBB- (i.e. investment-grade) bonds trade now. OXSQ debt is not at that rating level even if they were rated.

This highlights that the built-in protections of RIC bonds are pretty strong even if the issuers themselves are not of pristine quality.

Some Of The Key Mechanics

There are a couple of mechanics to be aware of for investors going through rights offerings and partial redemptions.

Many investors are worried about RICs like BDCs issuing shares below the NAV and they often vote no when asked by the companies, even if the companies don't have any plans to do so. However, what they often don't realize is that companies don't need shareholder approval to do rights offerings and these are typically executed with a subscription price well below the NAV.

In theory, a rights offering does not have to be dilutive to the NAV even if the subscription price is below the NAV. However, in practice it often is dilutive to many shareholders, particularly for those who do not fully exercise their rights and/or those who do not get a good price on selling transferrable rights (as there is often an asymmetry between sellers and buyers of rights in the secondary market).

As far as the partial redemptions are concerned, what happens there is a proportion of investors' shares are locked in their accounts. Investors are not allowed to sell these shares as they may end up with not enough shares to deliver into the redemption. These shares often get a different ticker in the account for clarity. The shares to be redeemed are allocated in a pro-rata fashion for each investor.

Why We Like OXSQ Bonds

We have been holders of OXSQ bonds since 2020. It's important to say at the outset that we like OXSQ bonds not because we like OXSQ itself. This distinction often confuses investors. After all, how in the world can it make sense to like the bonds of an issuer when you don't particularly like the issuer itself and wouldn't hold its common shares?

In an ideal world we would buy bonds of fantastic issuers at great yields. That reality sadly doesn't exist for the simple reason that 1) the sheer quantity of highest-quality issuers is very limited and 2) the bonds of those issuers trade at unexciting yields.

This means that we can expand the potential pool of issuers from highest-quality to what we call decent-quality. These issuers are not going to qualify for the usual investment-grade credit ratings from the major agencies however they are also not exactly dumpster diving material.

An important caveat here is that we only really tend to do this for registered investment companies or RICs rather than traditional companies. This is for two reasons. One, the risk of RICs is much easier to gauge since RICs are just portfolios of securities and these securities tend to behave in much more predictable fashion than traditional companies. Unlike a traditional company, a RIC is not going to go bust because it loses a major client or because its supply costs explode or because it gets disrupted. This makes it less risky in our view and much more intuitive to think about across various market and macro scenarios.

And two, RIC bonds have a number of structural protections having to do with asset coverage, common share buybacks and dividends which ensure that companies support their bonds and prioritize the interests of bondholders.

Takeaways

As this article suggests we continue to find a lot of value in shorter-maturity baby bonds issued by RICs like BDCs, CEFs and mortgage REITs, particularly those that are currently callable (i.e. those whose first call date is in the past).

The bonds tend to offer both attractive yields and resilience. The chart below shows the performance of the two OXSQ bonds (blue and orange lines) since we last topped up our allocation to them in 2021 relative to OXSQ common shares as well as OXLC which is another vehicle managed by the advisor focusing on CLO Equity.

Systematic Income

If we expand our horizon and look at 5 different periods up to today (e.g. 2019+ means the period starting at the beginning of 2019 and ending today) we see that the bonds have outperformed in 4 of those periods except for the period starting from 2021.

Systematic Income

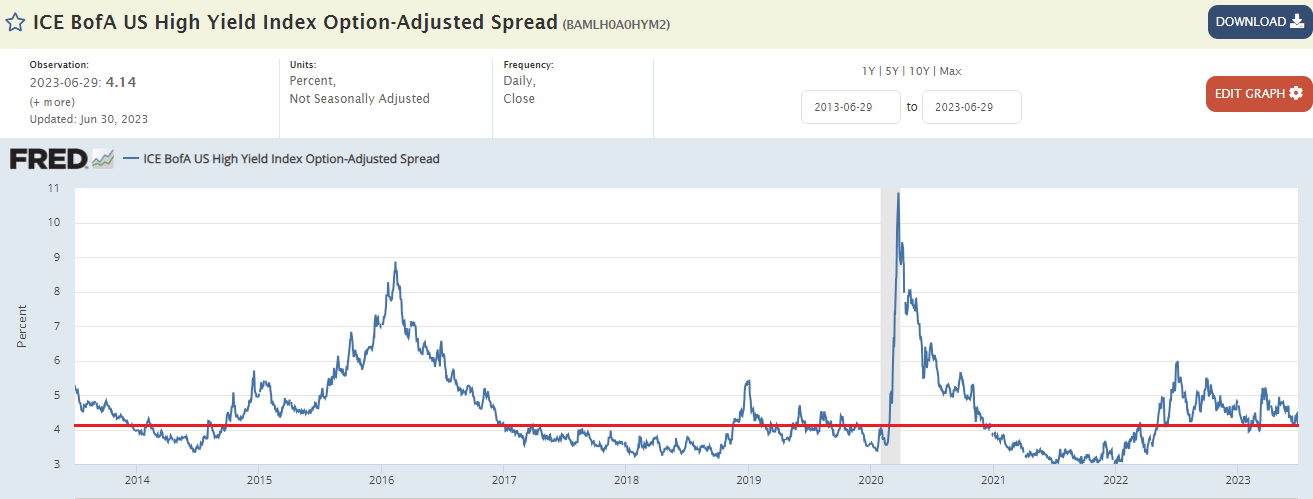

Often, lower-beta securities tend to end up outperformers after the market falls out of bed. However, the market today is quite strong with corporate bond credit spreads trading at very middling levels as seen below. Moreover both OXSQ and OXLC hold primarily floating-rate assets so they were not directly impacted by the backup in rates since 2022. All of this highlights that it's not a sure thing that higher-beta / higher-risk securities will outperform over longer-term periods.

{kind=link}

Our point in this article is not that investors should avoid common shares of BDCs or CEFs (such as OXSQ and OXLC). We certainly don't view the common stocks of the various RIC vehicles uninvestable, in fact we hold many BDCs and CEFs outright. Rather the important takeaway is that RIC bonds deserve a place in portfolios for several reasons. Not only can they perform well over the longer-term, across different market periods, but they can also offer investors drier-powder capital to put to work when the market falls out of bed. We continue to hold the company's other bonds like the 8.3%-yielding 2026 bonds ( OXSQZ ) in our Portfolios.

For further details see:

Oxford Square Capital: Partial Redemption Of 2024 Bond Highlights Resilience Of RIC Debt