ECCV - OXLC And ECC: Climbing Up The Capital Stack For Safe Income

2023-12-04 14:46:42 ET

Summary

- Oxford Lane Capital Corp. (OXLC) and Eagle Point Credit Co. (ECC) are popular income investments that invest in the lowest tranches of collateralized loan obligations (CLOs).

- OXLC and ECC leverage their portfolios to support high distribution yields, but this adds more risk and amplifies losses during downturns.

- Investing in the baby bonds and preferred offerings of OXLC and ECC, and the other CLO funds, can provide safer and steadier cash flow opportunities for conservative investors.

Written by Nick Ackerman, co-produced by Stanford Chemist.

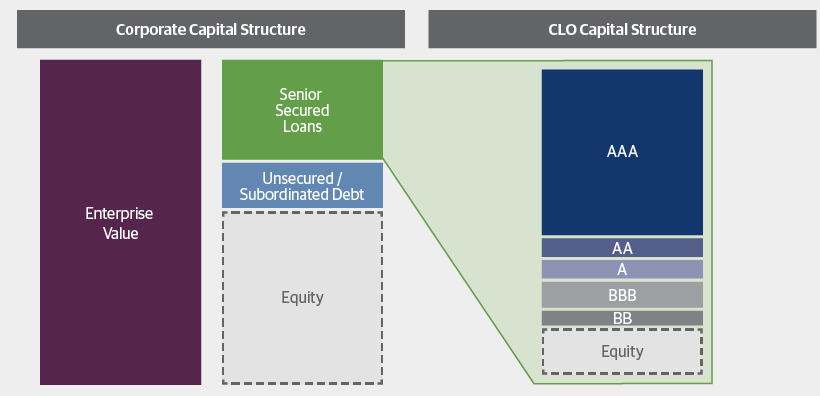

Oxford Lane Capital Corp. ( OXLC ) and Eagle Point Credit Co. ( ECC ) are highly popular income investments that often cause a flurry of passionate debates on whether they are worthwhile or not. They invest in the lowest tranches of the collateralized loan obligation ("CLO") structure, the equity portion and that means they are the last to receive any payments and the first to take losses.

That being said, the CLO structure is about what it sounds like. That is, it contains "loans," more specifically, senior secured loans pooled together. So, one is getting the bottom of the riskiest tranche in the CLO but near the top of the overall corporate capital structure.

{kind=link}

However, they then take a portfolio of these equity CO investments and leverage it up to the gills in an effort to support their massive distribution yields. Which, of course, adds more risk but delivers a result where OXLC is yielding around 19.5%, and ECC is pushing near 18%. Of course, leverage amplifies losses, so while historically, there has been a fairly low level of defaults, any defaults can be magnified. The net asset value per-share declines and share price declines that have followed over the years of market crashes are certainly the main arguments against these high-yielding investments.

With all that being said, I'm not focusing too much on OXLC and ECC commons specifically. I wanted to highlight several options for investors who want to climb up the capital stack of OXLC and ECC to invest in their baby bonds and preferred offerings. Essentially, investing in the leverage of these leveraged instruments.

What matters on those is less about what happens to the common and more about OXLC and ECC just having to survive. Historically speaking, no closed-end fund has ever gone "bust."

The share prices and NAV per share of both of these investments might look like they are racing to zero on a per-share basis. (Note: OXLC and ECC provide estimated NAV updates monthly, and those don't get reflected by YCharts. The chart is provided for a general idea of the direction of price/NAV over time.)

YCharts

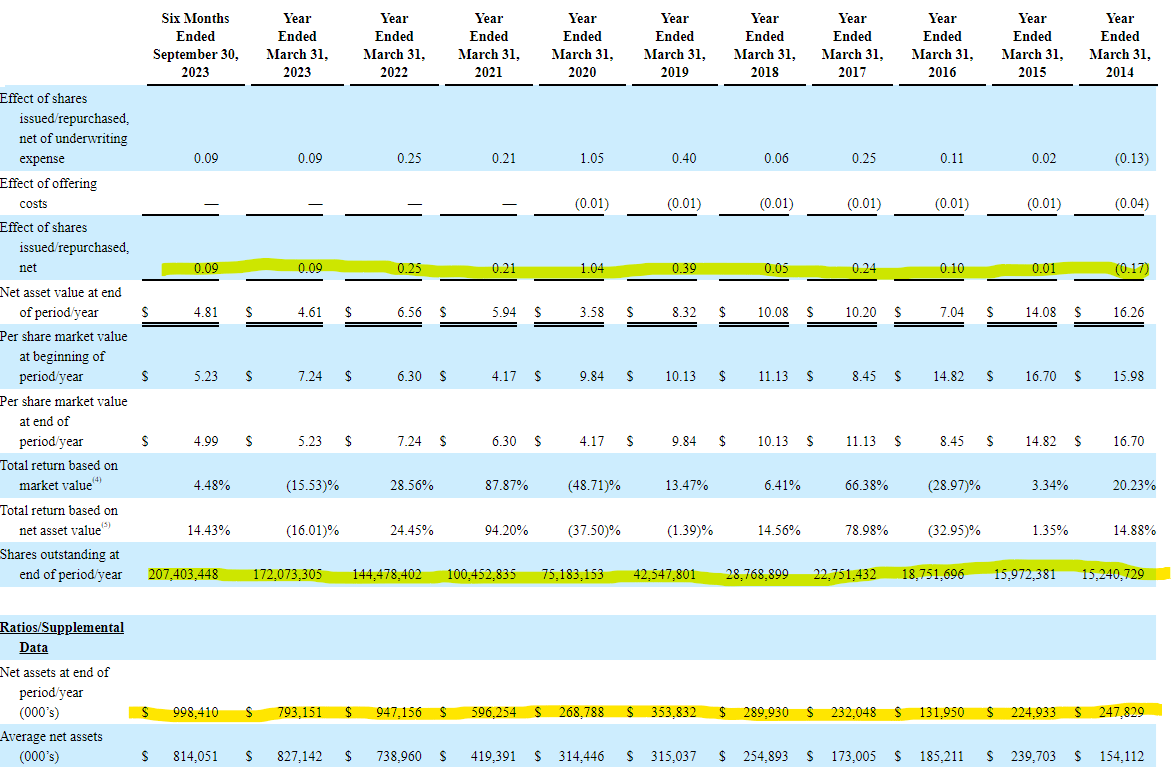

That isn't overly relevant for their underlying baby bonds and preferreds. This is because both of these funds issue shares like mad, and that actually isn't really a negative. In fact, it has often been accretive due to the premium to NAV that these investments trade at. For example, total shares for OXLC have exploded from March 31, 2019, to September 30, 2023, rising from 42.548 million to 207.403 million.

That is often another argument against the CLO funds, but it's actually a positive. During that time, the accretive effect on NAV per share was $2.07. Still, NAV per share dropped from $9.84 to $4.99. So, the drop in NAV would have ultimately been even worse had it not been for these accretive share offerings.

On the other hand, the main point of this was that net assets rose from $354 million to nearly $1 billion ($998 million) during this time for OXLC, which is really what matters more for having coverage of their baby bonds and preferreds. The further back you go , the more you see more of the same. Issuing shares that ultimately are accretive to the NAV per share, but the total assets balloon even more.

{kind=link}

That is the same for ECC; going back to December 31, 2019 , shares outstanding more than doubled from 28.632 million to 62.831 million. However, that added $1.37 to their NAV per share, and net assets went from $302.273 million to $548.122 million. On a per-share NAV basis, that slipped from $10.59 to $8.72.

Corporate Vs. Closed-end Fund Baby Bonds and Preferred

Similar to any regular corporate structure, the CLO closed-end funds are no different in that baby bonds are going to be higher in the capital stack over preferred. That is to say, should a CEF go bust, the baby bonds would get preference over their preferred, and both are above the common shareholders.

A distinction between regular corporations and CEFs though is that CEFs are more strictly regulated. According to the Investment Company Act of 1940 , any public preferred is limited to 100% of net assets, or in other words, a 50% leverage ratio. It gets even more strict with public debt that is limited to 50% of net assets or a ~33.3% leverage ratio.

According to CEFConnect, the effective leverage for OXLC currently comes to 33.18%, and ECC is at 28.96%. XAI Octagon Floating Rate & Alternative Income Term Trust ( XFLT ) is another CLO fund, but they are more of a hybrid with CLO debt and equity, as well as incorporating individual senior loan investments. XFLT's effective leverage comes up to 40.17%, but they don't have public debt, only public preferred.

If these levels are breached, the funds must rectify the situation by reducing debt. One of the ways to do that would be to reduce borrowings on a credit facility; that would be the easiest, but OXLC and ECC don't have any borrowings through a credit facility.

That is one way that XFLT is in a bit better position, as they also have withdrawn on their leverage facility. While it means they are exposed to floating rates, it puts them in a situation where they could cure their leverage faster and easier. Otherwise, ECC and OXLC would have to redeem some of their notes or preferreds. Additionally, issuing shares would cure being overleveraged as total assets would rise and reduce the leverage ratio.

Should they not take care of being overleveraged, then the common distributions would be suspended, and that protects the baby bonds and preferreds further by retaining assets. One reason a fund may not take down its leverage is if it believes it is a short-lived dip, which would put it in a situation where they are firing off assets at sale prices that would bounce back in a month or two.

Of course, there is a strong incentive for curing leverage levels because if they are suspending their distribution, then there is less incentive for investors to buy shares. That would mean the funds issuing shares wouldn't be as lucrative, and that would hurt management's pockets as they get paid on the total assets. So rather than suspend distributions, we'd see the funds take down their leverage and reduce common distributions, which is what we saw in 2020.

OXLC was also hit similarly with having to deleverage and reduce the payout of the common in 2016. ECC, on the other hand, appears to have been able to take leverage up during this period rather than reduce it, and it also did not have to reduce its distribution to common shareholders. Presumably, this was because they had more recently launched in late 2014 and hadn't been fully ramped up, whereas OXLC launched in early 2011.

A downside to these baby bonds and preferred offerings is that investment volume is light. Extremely light would be more appropriate - perhaps even prohibitively light for some larger investors. That could be more incentive to spread out through the various holdings, which would essentially set up a ladder of maturities, which isn't necessarily a bad thing. Just keep in mind that if you are buying into these instruments, don't expect a swift exit - particularly if we are in a panic. Think of investing in these for the long term/maturity if entering into these securities, in my opinion.

Highlighting Some Opportunities

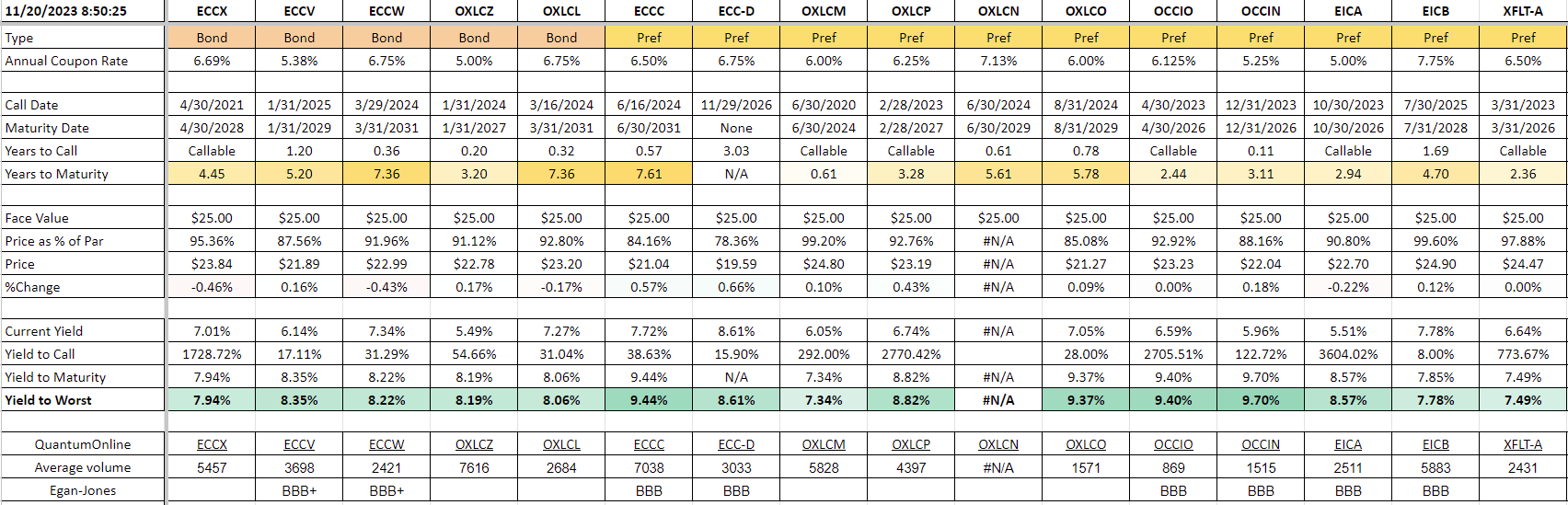

In looking at the options in the CLO baby bond and preferred space, we have many options to choose from. That includes other offerings from OXLC and ECC peer OFS Credit Company, Inc. ( OCCI ). In addition, their hybrid counterpart, XFLT, has their publicly traded ( XFLT.PR.A ) as well. Here's a breakdown of what's available, as well as the relevant data as of 11/20/2023.

CLO Fund Baby Bond and Preferred Overview (CEF/ETF Income Laboratory)

{kind=link}

The preferred I hold personally is OXLC's 6.25% Preferred Shares Series 2027 ( OXLCP ). This is one that I bought during the Covid crash, so I've been holding it for a while. Ironically, it was issued right before Covid really hit the market on 2/6/2020.

- callable date 2/28/2023 with maturity on 2/28/2027

- current yield: 6.74%

- yield to maturity 8.82%

- monthly pay $0.1302

The current yield might not be overly tempting for some investors, but if you have the patience to wait 3.28 years, you're looking at a YTM that is decent.

Alternatively, going higher in the capital stack offers a somewhat similar option. That is OXLC's 5% Notes due 1/31/2027 ( OXLCZ ).

- callable date 1/31/2024 with maturity on 1/31/2027

- current yield 5.49%

- yield to maturity 8.19%

- quarterly pay $0.3125

Despite being higher in the capital stack, the YTM here isn't all that much different when compared to OXLCP, with a difference of 63 basis points. It comes with a similar 3.2 years until maturity as well. However, I suspect that investors are willing to pay up a bit for OXLCP's monthly pay rather than quarterly. Additionally, the current yield is a 125 basis point difference, which is probably another factor with investors being able to invest in U.S. Treasuries of comparable current yields.

If you are simply looking for the highest current yield, that would be ECC's 6.75% Series D Preferred ( ECC.PR.D ). This is a perpetual preferred, meaning there is no date defined when investors will receive back the $25 face value. For that risk, investors are getting paid 8.62%. Though it does become callable on 11/29/2026, if rates are where they are now or even close, there is little chance that it gets redeemed. ECC was issued in 2021 when rates were at zero.

If you want something with a maturity date from ECC, then their 6.6875% Notes Due 2028 ( ECCX ) could be something that one finds appealing. It offers a respectable current yield and a decent YTM.

- callable date 4/30/2021 with maturity on 4/30/2028

- current yield 7.01%

- yield to maturity 7.94%

- quarterly pay $0.418

Conclusion

The CLO closed-end funds often get hotly debated between investors searching for income. Their searing yields offer a tempting opportunity for investors willing to incorporate these more volatile funds into their high-yield portfolios. Over the long term, OXLC and ECC have provided decent total return results.

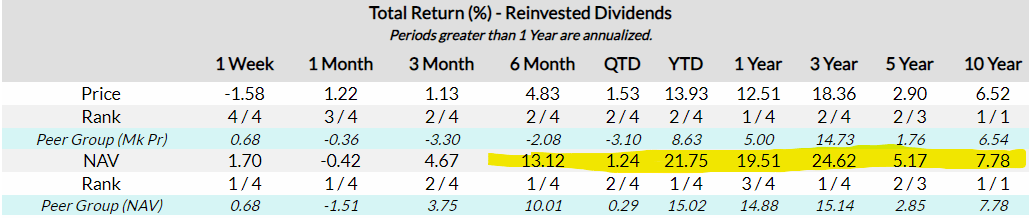

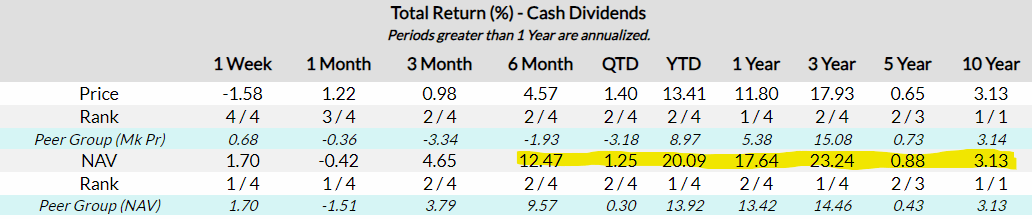

Here is a look at OXLC's performance and we can see that over the last decade, they provided around a 7.78% total NAV return. The last three years had been even more impressive, but that was coming out of Covid.

{kind=link}

Assuming one is taking the cash distributions and not reinvesting, the results are much more muted. Still, they have delivered positive results.

{kind=link}

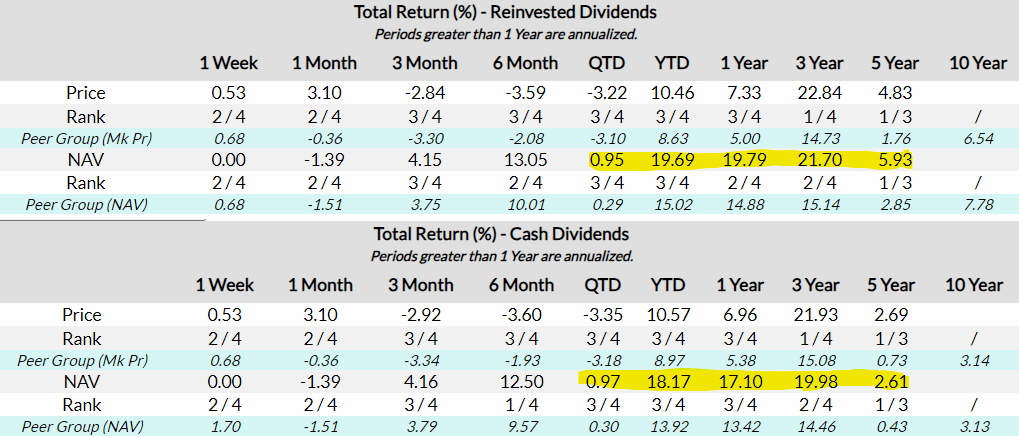

ECC shows a somewhat similar result, though we don't have the 10-year period to look at.

{kind=link}

Alternatively, for conservative investors who don't mind taking it down several notches but are getting significantly safer and steadier cash flows in return, the baby bonds and preferred CLO funds offer potential opportunities.

History doesn't guarantee future results. With that caveat said, should OXLC deliver the same ~8% total returns going forward for the common shareholders, then the 8-9% one could receive by climbing up their capital stack should certainly be a tempting offer. Additionally, a variety of maturity dates could provide a way to help ladder out one's fixed-income portfolio.

f

For further details see:

OXLC And ECC: Climbing Up The Capital Stack For Safe Income