PTSI - P.A.M. Transportation: Mixed Results But Trading Too Cheap With Fleet Modernization Efforts

2024-01-06 02:57:28 ET

Summary

- P.A.M. Transportation Services delivered mixed quarter results, but the market's reaction was too severe.

- Analysts expect beneficial net sales growth from 2025, and the company's recent fleet renovation and manufacturing techniques could increase future FCF.

- Risks include fuel price changes and strikes, but the stock could trade at higher price marks.

P.A.M. Transportation Services, Inc. (PTSI) recently delivered mixed results. However, I believe that the reaction of the market was too severe. Other market analysts are expecting beneficial net sales growth from 2025. Besides, with recent renovation of the fleet, modern manufacturing and assembly techniques, and potential development of better relationships with drivers, I think that future FCF could increase. There are obvious risks from fuel price changes or strikes. However, I think that PTSI could trade at higher price marks.

P.A.M. Transportation's Business Model

P.A.M. Transportation is a dry freight trucking company that transports general merchandise. Its cargoes consist primarily of automotive parts, expedited merchandise, consumer goods, and manufactured goods. Its trucks have real-time location and data transmission systems.

Its headquarters, principal terminal facilities, maintenance facilities as well as corporate and administrative offices are located in Tontitown, Arkansas, which is a major center for the trucking industry. In addition, support services for most leading manufacturers of truck and trailer equipment are readily available in Tontitown, Arkansas.

The company has a single reportable segment that groups all operations: the road transportation segment. These operations are classified as full load services or brokerage and logistics services. This designation is based primarily on ownership of the asset that performs the freight transportation service.

Truckload services are performed by company divisions that generally use company-owned trucks, long-term contractors, or single-trip contractors to transport freight shipments for customers. Brokerage and logistics services use third-party equipment, and typically involve the use of single-trip contractors. Both truckload and brokerage and logistics operations have similar economic characteristics, and are affected by virtually the same economic factors.

Recent Earnings Report, And Expectations From Other Analysts

In the last quarterly report, P.A.M. Transportation noted better than expected EPS GAAP figures, but more quarterly revenue growth than expected. EPS GAAP stood at $0.28, with quarterly revenue of $201 million.

I believe that the numbers were not perfect. However, the current valuation and recent decline in the stock price seem too large. In 2022, the company traded at close to $40 per share, and it is now selling at close to $19 per share.

Source: SA Source: SA

If we look at the trading multiples, I believe that P.A.M. Transportation Services appears a bit cheap. The company trades at close to 0.54x net sales, with an EV/EBITDA not larger than 4x. It is also worth noting that investors out there are expecting net sales growth and EBITDA growth in 2025.

Source: S&P

Stable Balance Sheet

P.A.M. Transportation Services receives payments a bit late from clients, and reports a considerable amount of property and equipment. With a significant amount of cash in hand, P.A.M. Transportation does use some debt. However, I believe that most financing comes from equity investors. In sum, I am not concerned about the total amount of debt.

As of September 30, 2023, P.A.M. Transportation Services reported cash and cash equivalents worth $102 million, accounts receivable close to $96 million, and marketable equity securities worth $41 million. Total current assets stand at close to $269 million, implying a current ratio larger than 2x. Liquidity does not seem a problem here. The largest asset is revenue equipment worth $634 million, and total assets stand at close to $731 million. The asset/liability ratio is between 1x and 2x, so I would say that the balance sheet is stable.

Source: 10-Q

The list of liabilities does not seem worrying at all. Accounts payable stands at close to $57 million, with accrued expenses and other liabilities of about $22 million and current maturities of long-term debt worth $56 million. Finally, with long-term debt of $171 million, total liabilities are equal to $415 million.

Source: 10-Q

I carefully reviewed the interest rate paid by P.A.M. Transportation, which stands at close to 3.62% and interest rate of Term SOFR as of the first day of the month plus 1.35%. With these figures in mind, I believe that assuming a cost of capital between 5% and 10% would be conservative.

Real estate financing consisting of an installment obligation for the purchase of real estate in Laredo, TX, payable in 120 installments at an interest rate of 3.02% and maturing in August 2030, and an installment obligation for the financing of various company-owned terminals and office buildings payable in 120 installments at an interest rate of 3.62% and maturing in March 2032.

Line of credit agreement with a bank provides for maximum borrowings of $60.0 million and contains certain restrictive covenants that must be maintained by the Company on a consolidated basis. Borrowings on the line of credit are at an interest rate of Term SOFR as of the first day of the month plus 1.35%, (5.65% at December 31, 2022) and are secured by our trade accounts receivable. An "unused fee" of 0.25% is charged if average daily borrowings are less than $18.0 million in a given month. Source: 10-k

Further Development Of Relationships With Clients And Drivers Will Most Likely Bring Economies Of Scale And FCF Margin Growth

The company has set a goal of developing relationships with customers in high-density traffic lanes. In this sense, it seeks to provide equipment to its customers in defined regions and disciplined traffic lanes. I believe that this strategy will allow it to maintain more consistent equipment capacity, provide a high level of service to its customers, attract and retain drivers, and maintain a strong safety record as drivers travel familiar routes.

It is also worth noting that the marketing approach is aimed at clients who are sensitive to the quality of service and not only to price. With these assumptions, I believe that economies of scale could bring FCF margin growth and increase in the stock valuation.

Modern Manufacturing And Assembly Methods Will Most Likely Continue To Decrease Inventory Levels

I believe that P.A.M. Transportation Services studies carefully the needs of clients, and offers shipments when necessary. Management tries to lower the amount of inventory. With these techniques, I believe that we could see a decrease in working capital and perhaps increases in FCF margin.

Many of our customers depend on us to deliver shipments on a time-definite basis, meaning that parts or raw materials are scheduled for delivery as they are needed on a manufacturer's production line. The need for this service is a product of modern manufacturing and assembly methods that are designed to decrease inventory levels and handling costs. Such requirements place a premium on our delivery performance and reliability. Source: 10-k

Recent Reduction In the Number Of Trucks Operating Could Lead To Future Flexibility And A Decrease In Costs

In the last quarter, P.A.M. Transportation noted a decrease in the number of trucks operating. If the company correctly assesses future demand from customers, I believe that we could see future improvements in the free cash flow. In this regard, I think that investors may want to have a look at the lines below.

Also contributing to the revenue reduction was a 150 truck decrease in the average number of trucks operated by the Company during the third quarter 2023 compared to the third quarter 2022 as the company aligned fleet size to decreased demand from customers. Source: 10-Q

P.A.M. Transportation Sells Old Trucks, And Buys New Trucks

The company noted that capex would stand at close to $90 million in 2023. From the quarterly report, I concluded that P.A.M. does not seem to lower the acquisition of trucks in the near future, which I believe is a great sign. With management trying to lower the age of the fleet, in my view, the company expects the business model to perform in the incoming years.

During the remainder of 2023, we expect to purchase approximately 330 trucks and 1,130 trailers while continuing to sell or trade older equipment, which we expect to result in net capital expenditures of approximately $90.8 million. Source: 10-Q

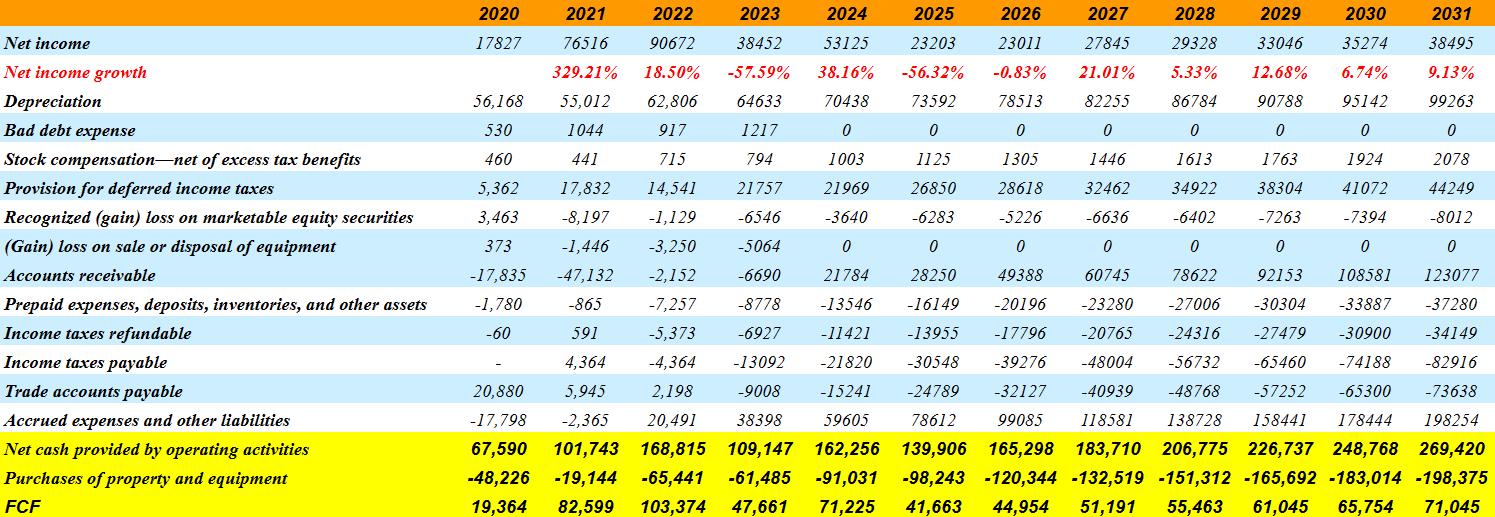

My FCF Expectations Based On Previous Assumptions And A Basic DCF Model Imply Certain Undervaluation In The Stock

My cash flow projections include 2031 net income close to $38 million, depreciation of about $99 million, and stock compensation of about $2 million. I did not include losses on sale or disposal of equipment, but I did assume 2031 changes in accounts receivable of about $123 million.

Additionally, with prepaid expenses, deposits, inventories, and other assets worth -$38 million and changes in trade accounts payable of close to -$74 million, accrued expenses and other liabilities would be close to $198 million.

Finally, 2031 CFO would be $269 million, and with 2031 purchases of property and equipment of close to -$199 million, 2031 FCF could be $71 million.

{kind=link}

P.A.M. Transportation Services reported EV/FCF close to 6x and 9x in the past. Moreover, the peers in the same sector trade at about 12x and 11x EBITDA. With these figures in mind, I assumed that an exit valuation of close to 6x-10x would make sense.

Source: Ycharts Source: SA

With FCF ranging between $42 million and $71 million, a WACC of 5%-10%, and EV/FCF close to 6x-10x, the implied valuation without net debt would range between $646 and $997 million.

Source: DCF Model

Besides, dividing by the share count, the implied median fair price would range between $33 and $41 per share. Finally, we would be talking about an internal rate of return close to 9% and 15%.

Source: DCF Model

Competitors

It is a highly fragmented industry, with thousands of competitors, none of which dominates the market. The current operating environment is characterized by a state of competition in relation to drivers and freight contracts. The market share of the P.A.M. Transportation is less than 1%, and it competes mainly with other medium and long-haul full-load carriers, with private transportation carried out by its current and potential customers, and to a lesser extent with railroads.

Competition occurs based on service quality, delivery performance, and price. Many of the carriers the company competes with have substantially greater financial resources, own more equipment, or transport a comparatively larger total volume of cargo.

Risks

The general state of the national and regional economy, along with equipment capacity levels, seriously conditions the transportation business. The volatility of various operating expenses, such as fuel and insurance, makes the predictability of profit levels uncertain. Additionally, driver availability, and compensation also affect operating costs.

It is also highlighted that the growth of the transportation business in Mexico entails risks associated with the relationship between the US and Mexican currencies, in relation to Mexican regulations and with regard to changes that may occur regarding trade and transportation between the United States and Mexico.

Revenue dependence on a few large customers is also a potential risk for the company. The five largest clients accounted for approximately 39%, 33%, and 35% of total revenues in 2022, 2021, and 2020 respectively. The majority of customers belong to the automotive industry segment.

Conclusion

P.A.M. Transportation Services delivered mixed quarter results, however I believe that the recent decrease in the stock price appears too severe. I think that modern manufacturing and assembly methods, renovation of the fleet, and further development of relationships with drivers could bring FCF growth. I did identify risks from fuel price changes, strikes, or dependence on a few clients, however the stock appears too cheap.

For further details see:

P.A.M. Transportation: Mixed Results, But Trading Too Cheap With Fleet Modernization Efforts