BANC - PacWest Bancorp: M&A Validates Our Bullish Call On The Preferred

2023-07-26 11:20:29 ET

Summary

- US regional bank stocks have been heavily shorted since the collapse of Silicon Valley Bank, with PacWest Bancorp being a prime target. However, stabilizing deposits have helped share prices recover.

- PacWest Bancorp announced its agreement to merge with Banc of California in an all-stock deal, which saw both companies' share prices increase. The combined entity will operate under the Banc of California banner.

- I maintain my BUY rating on PACWP as I expect price to converge to $25 within the next few months. Investors can still expect a 17% upside and a 9%yield.

Since the collapse of Silicon Valley Bank in March, US regional bank stocks have been targeted by speculators trying to predict which institution would be the next to fall in a proverbial domino. Despite an enormous negative potential impact on society and the broader economy, shorting stocks such as PacWest Bancorp ( PACW ) went through the roof in Q2 2023 without any intervention from the SEC.

The vicious cycle of customers losing confidence, deposits evaporating, and increased imbalance in the LDR (loan-to-deposits ratio) attracted more and more short selling, posing an existential threat to these smaller lenders. Fortunately, with the deposits' levels stabilizing in June, so did the share price. I reiterated my BUY rating for PacWest Bancorp 7.75% non-cumulative perpetual preferred stock series A ( PACWP ) at the end of last month when PACWP shares were trading at around $15.

Are they still a buy today? July was an eventful month, and PacWest Bancorp reported its Q2 results on July 25 th after the market close, hence the need to review what happened and share my updated view on PACW and PACWP.

PacWest reports 2Q23 earnings

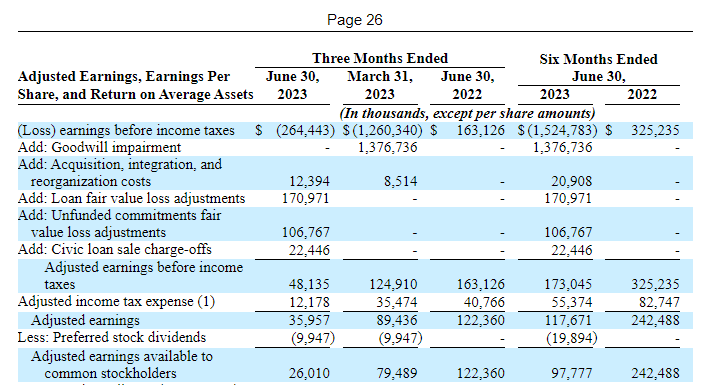

The adjusted EPS results were for $0.22 per share, a beat of $0.03, vs. the latest consensus of $0.19. However, analysts repeatedly revised the consensus estimate downward during the quarter, so I do not think this should count as a beat. When I published my analysis on June 3 rd , I called for $0.25 EPS at the midpoint of my forecast, and at that time, the figure aligned with the consensus. Even though I could think PACW earnings missed the target by $0.03 on my account, the truth is that many moving parts made the early estimation likely to be off, so I preferred to guide for a range of $0.10 - $0.40 instead.

The deals closed by PACW with Kennedy-Wilson ( KW ) and Ares Corporation ( ARES ) allowed PACW to sell substantial loan portfolios, replenish its cash depleted by fleeing depositors, and rebalance its LDR but, on the other side, hurt NII badly. Net interest income decreased by $137.8 million or 42.5% to $186.1 million for Q2 of 2023 vs. $323.9 million for Q2 of 2022. Because PACW sold these at a loss to book value, it also had to write down the assets taking a non-interest income hit of almost $171 million, which pushed the GAAP EPS to ($1.75).

Nevertheless, the company provided a reasonable reconciliation between GAAP and non-GAAP adjusted earnings, purging the costs associated with the loan portfolio sales. The just-mentioned fair value loss, plus unfunded commitments for fair value loss of another $106.7 million, accounted for almost 90% of the total reconciliation, with sold loans charge-offs for $22.4 million and restructuring costs for $12.4 million being the rest of it. Once removing these effects, adjusted after-tax earnings totaled roughly $36 million, which puts the $10 million quarterly payout on PACWP at about 28% of the available profits. Assuming that Q2 is the trough of PACW's earnings, the preferred dividend would be safe and vindicate my April's bullish call.

{kind=link}

However, the earnings call results were entirely overshadowed by another news, which made it look like all the above has no meaning: PacWest announced its agreement to merge with Banc of California ( BANC ) in an all-stock deal.

The combination

Under the terms of the deal, PacWest shareholders will receive 0.6569 of a share of Banc of California. BANC closed at $14.6 yesterday, but the news of the merger pushed the stock even higher toward $15.9, which equates to approximately $10.4 for PACW. Unsurprisingly, PACW edged 30% higher in its post-market session and breached $10 per share, fully recovering and surpassing a 27% drop during the last regular trading. It is rare to see mergers where both the acquirer and the acquired experience a meaningful share price gain, but this is one such case. After all, the combined entity, operating under the Banc of California banner, will have a larger footprint, minimal exposure left to uninsured deposits, and the ability to raise further capital (20% of the combined total equity), something PACW could not do during the crisis.

The $400 million equity raise from Warburg Pincus and Centerbridge seems like a good deal for the PE firms, which get exposure to a solid combined entity with 10%+ pro forma CET1. Despite the capital raise, the merger is expected to be 20% accretive to 2024 EPS and immediately 3% accretive to TBVPS.

Following closing and the asset sales, the company will have approximately $36.1 billion in assets, $25.3 billion in total loans, and $30.5 billion in total deposits, fully rebalancing PACW's problematic LDR and bringing it down to 85%. Wholesale funding will remain but at a minimum of approximately 8%.

Now, the essential news about PACWP is that, under the terms of the merger agreement, outstanding shares of preferred Series A issue will be converted into the right to receive one share of a newly created series of substantially identical preferred stock of BANC (for convenience from now referred as BANCP), which will keep the same T&C and 7.75% yield of PACWP. It is excellent news for PACWP holders, and I expect further recovery toward face value, even if the stock jumped 18% and trades now above $21.

Rating update and final remarks

There is no reason for BANCP to trade substantially lower than face value. However, it is crucial to recognize that achieving face value could also be an unlikely scenario now that interest rates have increased considerably. Many preferred issues have devalued over the past months, and for a good reason, since preferreds should carry a healthy spread against risk-free alternatives.

However, the exact size of this spread can't be mathematically determined. It is still a function of investors' preferences. Preferreds in the regional banks' space that could be somewhat comparable to BANCP include KeyCorp Series G ( KEY.PK ), which carries a coupon of 5.625%. Now trading at $20.6, it yields about 6.8%. Western Alliance Bancorporation ( WAL ), another bank severely hit by the crisis, also has a preferred issue ( WAL.PA ) with a similar yield since it trades at about 63% of its face value but carries a 4.25% interest at par. Considering the coupon on peers' offerings, I think it is reasonable to maintain my BUY rating on PACWP at this time. With the merger happening and PE's support, it would make sense that a good part of the premium assigned to the preferreds of these larger institutions dissipates. And even when trading at par, PACWP/BANCP would yield about 1% higher. I expect PACWP to converge to $25 within the next few months, meaning investors can still expect a 17% upside and cash in a 9% yield while waiting.

Regarding the common stock PACW/BANC, the initial guidance calls for 2024 earnings in the $1.65–$1.80 range, meaning shares are effectively changing hands at 9x fwd earnings. While I think such a valuation is reasonable, it is more or less in line with the peers mentioned above, KeyCorp ( KEY ) and Western Alliance. With PACW revaluing above $10 per share, I have a neutral view of its shares and see better value elsewhere in the banking space.

For further details see:

PacWest Bancorp: M&A Validates Our Bullish Call On The Preferred