IGT - Palm Harbour Capital Q1 2023 Investor Letter

2023-04-25 20:15:00 ET

Summary

- Palm Harbour Capital LLP is a United Kingdom Limited Liability Partnership based in London. We scour the globe seeking undervalued securities in order to build a unique portfolio.

- During the first quarter the fund gained 7.2% gross of fees.

- We are extremely optimistic about our portfolio’s prospects and believe we will reach our compound return aspiration over time.

- We continue to believe this is a great time to be a value investor and are very excited about the medium-term prospects for the current portfolio.

Dear fellow investors and friends,

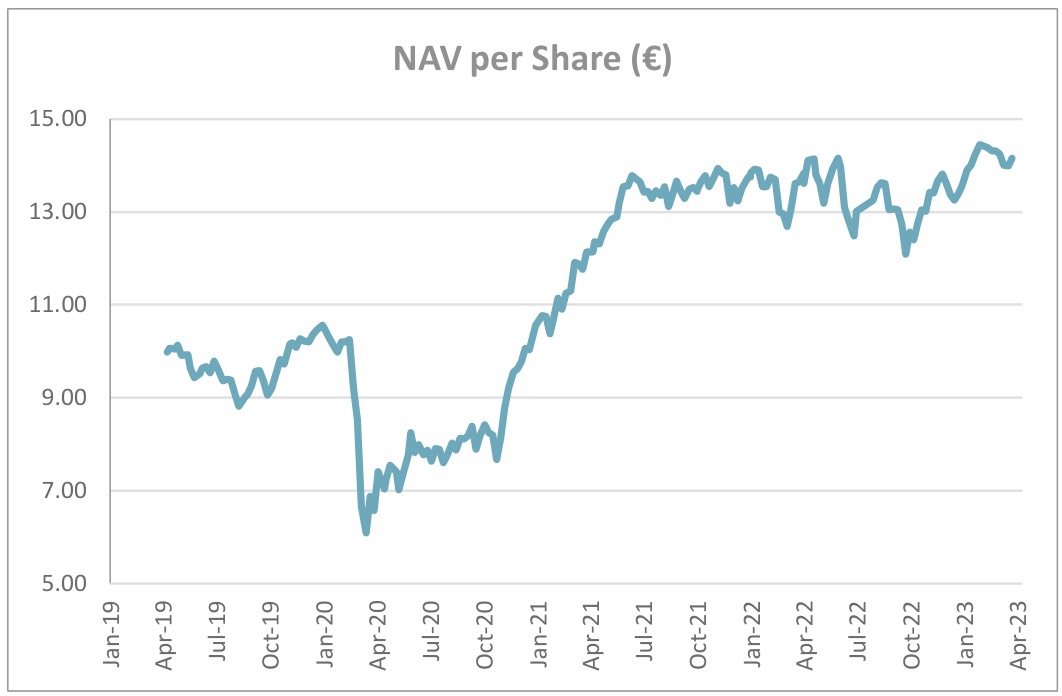

During the first quarter the fund gained 7.2% gross of fees [1] . We do not have a stated benchmark in our Key Investor Information Document ((KIID)) and therefore cannot comment on relative performance. We leave it up to you to decide. We note the above number appears a bit below European benchmarks and slightly better than global benchmarks. Inception to quarter end return was 45.2% or 9.8% compounded annual return. Our last reported NAV at quarter-end was 14.16 (30/03/2023 +5.8% from the closest reported NAV at the fourth quarter end of 13.39 on 29/12/2022). We are extremely optimistic about our portfolio’s prospects and believe we will reach our compound return aspiration over time. Our fund’s composition is unlike any index, and we are unlikely to perform in a similar manner.

{kind=link}

The first quarter of 2023 continued the themes of 2022, namely inflation, interest rates and what happened to that recession? Towards the end of the quarter, we also had a good old-fashioned bank run to spice up the headlines. Inflation trends slowly declined as we lapped last year’s very strong spike and non-headline energy, and food prices lapped the start of the Ukraine war (though they were elevated before the war lest we forget). The endless debate on when central banks will stop raising rates (and the speculators praying for cuts) continued until banks began to fail - then the debate intensified.

By design, we have no direct exposure to banks and the failures seen in that sector in the first quarter remind us why. By their nature, banks have highly levered business models, ultimately backed by trust. Normally, we like it when stock prices fall, assuming nothing has changed fundamentally, and we can buy them on the cheap. This is not the case with banks. Falling share prices alone could cause worry and can start a bank run, regardless of whether the bank is actually facing significant impairments. Banks have a fundamental duration mismatch between short-term liabilities, customer deposits, and assets, customer loans. Deposits are often instant access especially in today’s age of mobile apps. Loans on the other hand are usually held for years. If scared depositors want their money back and the bank does not have enough liquidity, end of bank.

Worse, bank balance sheets are illegible. While there is often massive amounts of required disclosure, it is usually provided in aggregate and therefore it is difficult to know the actual credit risk being taken. Prudent risk management is not rewarded. Regulation often shifts and is generally focused on the previous crisis whilst risk flows to where regulators are not currently looking. Management receives stock options which make them very rich if things go well; if things go bad, nothing happens. The incentive is to grow recklessly during good times and inevitably underwriting standards plummet. Bank managers have also learnt over the past decades that the central bank will always bail them out so why not gamble the house?

Generally, large banks are usually just considered macro calls on a country or interest rate policy whilst regional banks are usually a call on local commercial real estate. Trillions of bonds were once issued or traded with negative yields and trillions of debts were issued at very low rates to buy real estate and other assets at very elevated levels. One only needs to look at the private equity industry to see how loan covenants, used to protect creditors, were eroded until they were nearly non-existent. There are most likely more losses to be found in the coming years. All in all, there are definitely better places to fish.

We wrote in our previous letter, “Almost all bubbles have ended in a period of below average valuation where most speculators exit the market. Now, they appear merely to be on the sidelines.” We find it ironic that the failure of the largest bank involved with crypto firms and the largest bank banking to profitless tech companies have led to a massive rally in crypto and profitless tech at the end of the first quarter. Sadly, the animal spirits of rampant speculation have not yet met their end in this cycle.

Investment theses predicated on low interest rates or finding a greater fool to hop on the bandwagon are unlikely to be consistent winners, in our view. We do not think it is all that important to our portfolio of companies if interest rates rise or fall by a couple of per cent. For the most part they will continue making their products, satisfying their customers and most importantly, earning cash for their endeavors.

In the first quarter we added a significant position in Telekom Austria ( TKAGY ) which we outline later in this letter, a mid-sized position which we are still building and improving our knowledge on, and two small positions we added to our oil and gas basket. We sold our stake in Premia, a Greek Real Estate company and our stake in an American furniture company as we found better prospects for the capital.

We tendered our shares of South African conglomerate Grand Parade. We entered the position as a liquidation play. The company successfully sold their Burger King franchise, spun-off their stake in listed Spur corporation, closed and liquidated an unprofitable business and made other changes. All in all, we received two dividends for a total of ZAR 1.0 (ZAR0.7 after tax), sold our Spur shares worth ZAR0.37 and then the shares were tendered for by South African GMB Liquidity Corporation for ZAR3.33 a share leaving us with a total return of approximately 60% in two years.

At quarter-end our portfolio had more than 105% upside to our estimated NAV and was trading at a weighted average P/E of 8.5x, FCF/EV yield of 19% and a return on tangible capital of 30%.

| Contributors |

| Detractors |

| Ginebra San Miguel ( GBSMF ) |

| +204 bps |

| Var Energi ( VARRY ) |

| -68bps |

| Danieli Savers |

| +113 bps |

| iHeartmedia ( IHRT ) |

| -58 bps |

| Esprinet |

| +109 bps |

| CIR SpA |

| -53 bps |

| Caltagirone |

| +88 bps |

| Tessenderlo ( TSDOF ) |

| -29 bps |

| International Game Technology ( IGT ) |

| +85 bps |

| OCI ( OCINF ) |

| -27 bps |

The top contributor during the first quarter was Ginebra San Miguel (+53.9% +204 bps), the Filipino gin and spirits company which we introduced in our second quarter 2021 letter. The company reported full year 2022 earnings with sales +11% (7% volume and 4% pricing – note they raise prices only once a year during the first quarter so were a bit behind given inflation. They raised prices by around 8% during the first quarter of 2023.) and operating income was +13% year over year. What we believe drove the share price, however, was the large dividend boost. The company has been net cash for some time now and they do not have large capital expenditure needs currently. The company paid a quarterly dividend of 0.25 PHP in 2020 (1 PHP full year), adding a quarterly special dividend of 1 PHP (5 PHP full year) in 2021. They increased the regular quarterly to 0.375 in 2022 (5.5 PHP full year) and have now announced 0.75 regular quarterly and 1.75 special quarterly (forecast of 10 PHP for full year 2023). The company ended 2022 with a share price of PHP 105. Given the new payout it implies a nearly 10% dividend yield for what is perceived as a consumer staples business. Thus, the shares re-rated ending the quarter at PHP 159 for a 6.3% dividend yield.

The second largest contributor was Danieli (+27.4% +123 bps), the Italian steel plant maker and steel producer, which we introduced in our third quarter 2020 letter. The EBITDA for the six-month period ended in December 2022, increased by 25% compared to the same period last year, driven by the steel segment due to favourable combination of prices, volumes and energy subsidies. Despite macro-uncertainty, management maintained a positive outlook for the steel market for 2023, with prices and volumes holding steady compared to 2022, thanks to a more receptive end-market and the expectation of a gradual normalisation of the energy market. Looking forward, the EU’s decision to levy a carbon tax from 2026 on non-green imported steel is also a moderate positive in our view. It should also drive other steelmakers to buy their green technologies boosting their plant-making division. Despite the great results, Danieli still trades at only a modest premium to its net cash position.

The third largest contributor was Esprinet (+37.1% +109 bps), the Italian electronics distributor, which we introduced in our fourth quarter 2019 letter. Against inflation pressures and consumer pessimism, Esprinet managed to increase margins on flat sales, thanks to the focus on higher profit margin product categories. Working capital remained elevated but we expect it to decline in the second half of 2023. Despite the increased working capital, improved profitability reversed the declining trend of return on capital employed for the fourth quarter. The strategy is broadly focused on expanding the group’s presence in high value-added products that could further improve margins. Overall, despite the short-term uncertainty, management continues to prove its ability to execute. We remain very positive about the mid-to-long term prospects of the company powered by strong trends in IT spending in Italy helped by EU subsidies.

The fourth significant contributor was Caltagirone (+31% +88 bps), the Italian holding company whose major asset is an approximately 45% stake in the white cement producer Cementir, which we introduced in the first quarter of 2021 letter. The shares were undeservingly weak in the fourth quarter and as its major holding, Cementir, increased 28.5% in the first quarter following excellent results. The holding company shares followed suit. However, the discount remains extraordinarily wide at c. 54%, which leaves Caltagirone massively undervalued on a NAV basis and even more so using our target prices for the major holdings.

The fifth largest contributor was International Game Technology (+16.8% +85 bps), the Italian-American lottery and gaming machine technology provider, which we introduced in our first quarter 2020 letter. Revenue and profit exceeded the high-end of management’s outlook for both the fourth quarter and the full year of 2022. Strong cashflows allowed for meaningful debt reduction as they ended the year 3.1x levered, ahead of guidance and in the mid-range of their 2025 target range, with 80% of the debt being fixed rate. Management guided for further margin improvement and $500-600 million in free cash flow for 2023. The defensive characteristics of the business model, deleveraging and attractive valuation continue to support a strong investment thesis.

The top detractor was Var Energi (-27.2% -68 bps), one of the largest independent oil and gas producers in Norway. Var’s net production was flat for the year but 18% down compared to the fourth quarter 2021, negatively impacted by the fire at Åsgard B site in November 2022. Var reported a volume-weighted average price of $115 per barrel of oil equivalent (“boe”) in a continued strong commodity price environment. Despite announcing higher than expected production costs, due to increased maintenance activity, inflation pressure and cost overruns on new projects, management reported profits in line with consensus post the revised guidance. Management expects production cost to increase to $14.5-15.5 per boe in 2023 but remains confident about its mid-term target of $8 per boe as production from new projects picks up. Lower oil and gas prices due to a temporarily over-supplied market also weighed on the share price. We believe there has been structural underinvestment in the oil and gas industry and companies are much more focused on capital allocation than they have historically been. We note there has been increasing insider buying activity which further builds confidence.

The second largest detractor was iHeartMedia (-37.5% -58 bps), the American radio and podcasting company. The company suffered two self-inflicted wounds, which will impact the first quarter. The first, which the company flagged as temporary was a change in sales incentives. Apparently, they changed their sales force behaviour to sell more lower margin products at the expense of higher margin products (where management believed it should have been incremental volumes of lower margin not a switch). The second was their guidance for interest rate expense. The company did not hedge their floating term loan and is suffering from the higher interest rate environment, something you do not want to see in a highly levered company. Their debt maturities are years out, but every quarter that passes where free cashflow is low will make refinancing more difficult. Up until now, the company has been executing well, and their podcast business is growing strongly. Management has also been buying shares and we believe their major shareholder, if allowed by the Federal Trade Commission, is potentially interested in owning the business.

The third largest detractor was CIR (-11.3% -53 bps), the Italian holding company which owns nursing homes and rehabilitation centres in Italy and Germany and a stake in listed auto parts supplier Sogefi, which we introduced in the fourth quarter 2019 letter. Management expects a full recovery to pre-Covid activity in 2023 for Acute and Rehab and in 2024 for nursing homes . Margins increased in 2022, but management expects a slow recovery as tariff resets lag inflation.Sogefi expects mid-single digit market and revenue growth and stable to growing margins in a volatile environment. Absent new adverse events, both companies expect profits in line with or slightly above last year. The company continues to buy back shares and we believe there will be a change to the group structure in the coming years.

The fourth largest detractor was Tessenderlo (-13.6% -29 bps), the Belgian conglomerate with businesses in agriculture chemicals, bio-valorization, and weaving machine products. After the merger of Tessenderlo with Picanol, Luc Tack succeeded in fully combining the two entities into one group and controls 54% of the shares. The combined company offers additional diversification which should lead to more stable cash flows albeit with a more complicated structure. The management’s reputation and their shareholder unfriendly approach was a major overhang to the share price, but we believe now that he has completed this merger on his terms perhaps, he will focus more on the share price. We have already seen changes with the initiation of both a €0.75 per share dividend and a share buyback, which does make us more optimistic about share price development going forward.

The fifth largest detractor was OCI (-6.5% -27 bps), the Dutch nitrogen fertilizer and methanol producer, which we introduced in our second quarter 2019 letter and further updated in our fourth quarter 2021 letter. OCI posted dull fourth quarter results, in a seasonally low quarter, but management sees a high farmer profitability and decades low grain stocks providing a healthy backdrop heading into the 2023 Northern hemisphere application season. We are bit more bearish on the short-term but believe in the longer-term fundamentals especially in the emerging uses of ammonia and methanol. The company plans to pay a €3.5 per share dividend in April, which will bring distributions in the last twelve months to €8.5 per share. At quarter end, Inclusive Capital Partners [2] , an activist fund run by Jeff Ubben (formerly of ValueAct Capital), has sent a letter to OCI’s Chairman arguing that OCI is undervalued, and that management should explore strategic initiatives to unlock value. Management wrote a public reply and seemed receptive to their input.

Telekom Austria ( TKAGY )

The combination of a defensive business model, growing free cashflow and low leverage creates a particularly attractive investment thesis around Austria’s largest telecommunications provider. Additionally, the spin-off of its tower assets is expected to unlock value and potentially allow them to re-lever with a special dividend or M&A.

Telekom Austria (TKA) is a leading Austrian telecommunication provider with growing business in Central and Eastern Europe. The company splits operations geographically with Austria representing 55% of sales, followed by Bulgaria (13%), Croatia (9%), Belarus (9%), Serbia (7%), Slovenia (4%) and North Macedonia (3%). TKA operates in oligopolistic markets being the incumbent in Austria and number two or three in all other jurisdictions. While telcos are perceived as mature businesses, TKA has managed to grow top line at 2.7% pa over the last five years mainly due to the growth of its international activities, which benefit from price increases, a post-covid recovery, convergence, and rising penetration rates. Moreover, the group is not suffering from changes in consumer behavior or increased churn, and it continues to benefit from strong demand for highbandwidth products and successful upselling.

TKA has more pricing power than most European peers, with inflation-linked tariffs in the two key jurisdictions, Austria and Bulgaria, and price increases in most other markets, protecting profitability in a particularly challenging macro environment. Simultaneously, the ongoing restructuring program combined with the main shareholder’s focus on financial performance has already borne fruit with the EBITDA margin increasing from 32.5% in 2016 to 36.7% in 2022 to grow EBITDA at 5.0% per annum over the last five years. Finally, the lowly-levered balance sheet (<1.0x excluding leases) offers ample space for management to execute a 5G and fiber investment program without adding debt risk. It is worth noting that the United Group, the main competitor in Bulgaria, Croatia, Slovenia and Serbia has a similar investment program but it is 5.0x levered.

The most interesting part of the story is the announced spin-off of the tower business and its listing on the Vienna stock exchange. While public markets are unlikely to pay recent private market multiples for this business, publicly traded peers are still highly appreciated by the market. Apart from the value recognition of the tower company asset, currently ignored by the market, the spin-off is expected to benefit the thesis in multiple ways. As an independent entity, the tower company could expand its strategy by signing agreements with other telecom operators and tower companies, hence increasing the tenancy ratio, which is the main driver of profitability. Moreover, TKA will transfer approximately 50% of their leases and we estimate 200-250 million of financial debt to the tower company, reducing lease (IFRS 16) and financial debt and their linked lease and interest expense cash outflows.

Exposure to Belarus, roughly 10% of the business, weighs negatively on investor sentiment. Thus far they have been able to extract dividends and the currency has been remarkably stable, however this could change at any time. Even in the most pessimistic scenario, the thesis remains attractive. Low liquidity of the share and the required investment in 5G and fiber are probably two other reasons for the discount. We don’t see them as a concern since the first has nothing to do with the value of the company and the second is a market-wide trend which probably affects the levered peers more. The major shareholders have already agreed to a capital expenditure plan so the risk that the government forces uneconomic 5G/fiber rollout is limited.

Excluding any value realization from the tower business divestment, we estimate that Telekom Austria trades at a 12% free cash flow yield, which for a stable and growing business with improving margins should be considered a bargain. Although the details of the spin-off haven’t been released yet, the tower company should add an extra €2.53.0 per share value to our thesis. The spin-off is also expected to further reduce leverage, which could give room for a special dividend. Overall, we see this as a classic value play with an interesting upside potential without taking significant risk.

As stated in our previous letter, we are currently not charging a management fee until the fund reaches a larger size. The founder’s class management fee will then be only 1% of assets. We do not charge entry or exit commissions despite our KIID saying it is theoretically possible.

Our focus is and remains on the portfolio, but we do need to grow our assets to a sustainable level. Please feel free to share this letter with any potential investors.

We now have a commercial agreement with Cobas Asset Management to distribute our fund in Spain. You can now open an account and place orders with them. For more information, please contact them via phone or email. In the future, we hope it will be possible via their website. You can reach the Cobas team at +34 91 755 68 00 or international@cobasam.com

Our fund can be invested through both European international central securities depositories: Euroclear and its FundSettle clearing platform and Clearstream through the Vestima fund clearing platform. Our fund is registered for distribution in the UK, Spain and Luxembourg including for retail distribution.

Currently the following financial institutions in Spain are distributors: Renta 4 (you may need to contact them – it is not offered on the website yet), Ironia, Lombard Odier, Banco Alcala as well as many other institutions working through the main platforms in which the fund is available upon request: Allfunds Bank and Inversis.

In the UK we are offered on the AJ Bell low-cost platform ajbell.co.uk and can be part of an ISA or pension.

Our fund is also available on SwissQuote swissquote.com where almost any nationality (ex-USA) can open an account without local Swiss taxes being an issue.

If you have any issues finding our fund or you wish to get more information about us and our process, please contact us at IR@palmharbourcapital.com

Our fund is being offered as part of a Spanish pension value-orientated fund of funds. If interested in investing in a Spanish pension scheme, please contact us.

We thank you for your ongoing support. We continue to believe this is a great time to be a value investor and are very excited about the medium-term prospects for the current portfolio.

Yours faithfully,

Palm Harbour Capital

Footnotes[1] Our NAV is calculated weekly by FundPartner Solutions, a subsidiary of Pictet & Cie and does not align with monthly or quarterly reporting. The gross return stated is net of taxes and fees but before fund expenses, which are currently running at approximately 15 bps per quarter at current AUM. We project this to decline significantly as AUM grows. Please see our comment on management fees. [2] https://www.cnbc.com/2023/04/08/how - inclusive - capital - could - boost - value - at - oci - and help - the - environment.html |

| This information is being communicated by Palm Harbour Capital LLP which is authorised and regulated by the Financial Conduct Authority. This material is for information only and does not constitute an offer or recommendation to buy or sell any investment or subscribe to any investment management or advisory service. In relation to the United Kingdom, this information is only directed at, and may only be distributed to, persons who are “investment professionals” (being persons having professional experience in matters relating to investments) defined under Articles 19 & 49 of Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 & Articles 14 & 22 of the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemption) Order 2001 and/or such other persons as are permitted to receive this document under The Financial Services and Markets Act 2000. Any investment, and investment activity or controlled activity, to which this information relates is available only to such persons and will be engaged in only with such persons. Persons that do not have professional experience should not rely or act upon this information unless they are persons to whom any of paragraphs (2)(a) to (d) of article 49 apply to whom distribution of this information may otherwise lawfully be made. With investment, your capital is at risk and the value of an investment and the income from it can go up as well as down, it may be affected by exchange rate variations and you may not get back the amount invested. Past performance is not necessarily a guide to future performance and where past performance is quoted gross then investment management charges as well as transaction charges should be taken into consideration, as these will affect your returns. Any tax allowances or thresholds mentioned are based on personal circumstances and current legislation, which is subject to change. We do not represent that this information, including any third-party information, is accurate or complete and it should not be relied upon as such. Opinions expressed herein reflect the opinion of Palm Harbour Capital LLP and are subject to change without notice. No part of this document may be reproduced in any manner without the written permission of Palm Harbour Capital LLP; however recipients may pass on this document but only to others falling within this category. This information should be read in conjunction with the relevant fund documentation which may include the fund’s prospectus, simplified prospectus or supplement documentation and if you are unsure if any of the products and portfolios featured are the right choice for you, please seek independent financial advice provided by regulated third parties. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Palm Harbour Capital Q1 2023 Investor Letter