IHRTB - Palm Harbour Capital Q4 2022 Investor Letter

Summary

- Palm Harbour Capital LLP is a United Kingdom Limited Liability Partnership based in London. We scour the globe seeking undervalued securities in order to build a unique portfolio.

- During the fourth quarter the fund gained 9.7% gross of fees.

- We still believe there is a structural shortage after years of low capital expenditures and any economic upswing will cause significantly higher prices.

- We continue to believe this is a great time to be a value investor and are very excited about the medium-term prospects for the current portfolio.

Dear fellow investors and friends,

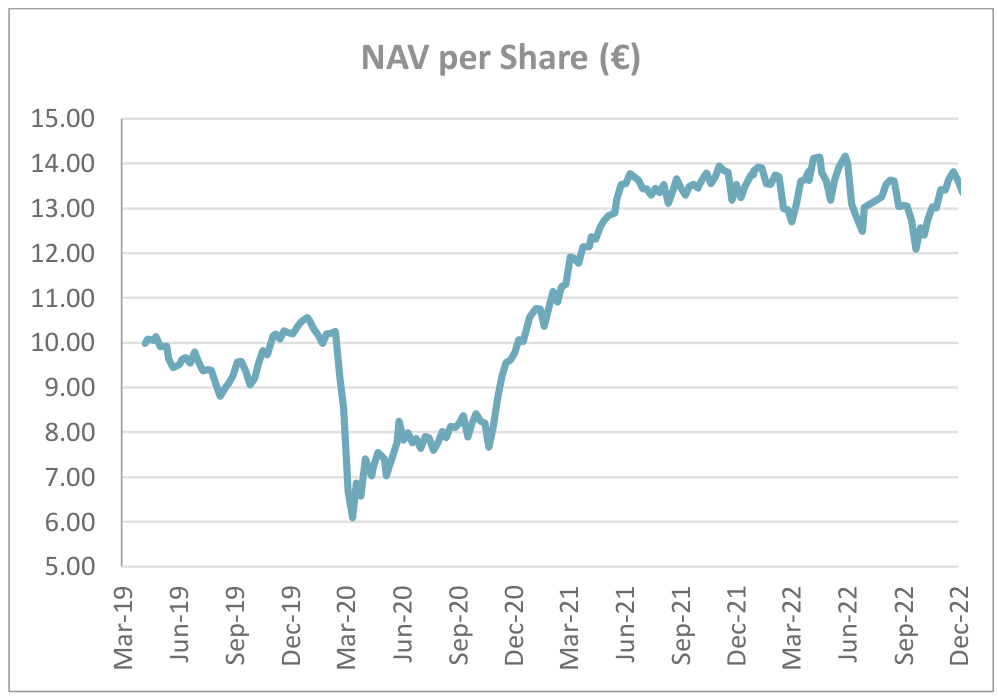

During the fourth quarter the fund gained 9.7% gross of fees [1] . We do not have a stated benchmark in our Key Investor Information Document (KIID) and therefore cannot comment on relative performance. We leave it up to you to decide. We note the above number appears in line with European benchmarks and significantly better than global benchmarks. We ended the quarter with a full year performance of -2.8% (-2.6% on a NAV basis 29 December 2022). Inception to quarter end return was 35.4% or 8.4% compounded annual return. Similarly, our last reported NAV at quarter-end was 13.39 (29/12/2022 +10.86% from the closest reported NAV at the third quarter end of 12.08 on 29/09/2022). We are extremely optimistic about our portfolio’s prospects and believe we will reach our compound return aspiration over time. Our fund’s composition is unlike any index, and we are unlikely to perform in a similar manner.

{kind=link}

The fourth quarter rhymed with the previous three quarters where the major themes remained inflation, interest rates, and recession. Similarly, our fund performed well, recovering from the previous quarter-end sell-off. However, we did suffer yet another late quarter-end sell-off, which prevented us from posting a positive year. Whilst not completely satisfied with our results (it is never pleasant to lose money if only on a mark-to-market basis rather than a permanent capital loss), we are glad to see some sanity return to the markets. We find it disheartening that it took war and run-away inflation for central banks to even start to normalize interest rate policy (let alone their balance sheets). Our philosophy precludes us from buying the speculative momentum stocks so popular in the past few years, let alone the parade of nonsense from profitless tech stocks, mega (overpriced) IPOs, cryptos, NFTs, SPACs, and meme stocks. We are glad that these bubbles have deflated, if not yet gone away and some market participants even discuss sensible valuation again. Even high-quality stocks that were trading on nosebleed valuations have somewhat corrected. However, there is still a long way to go to bring the economy back into balance.

The US stock market is merely trading around its standard long-term multiple and we have yet to see much in the way of earnings downgrades. In reality, the magnitude of the recent correction isn’t fierce: the S&P500 is where it was in 2021. Almost all bubbles have ended in a period of below average valuation where most speculators exit the market. Now, they appear merely to be on the sidelines.

During the fourth quarter consumer price index measurement of inflation began to come in below expectations after several months of above expectation readings. The current narrative is that we are past peak inflation and that the long-sought “Fed pivot” will occur in the second half of this year. That is to say that not only will the Fed not continue to increase but indeed even start to decrease the Fed funds rate. Thus, the market can go back to party mode, fueling asset price inflation (think real estate and stock market valuation multiples) and easing the pain of over-leveraged players dependent on easy money to make a profit. Many winners in the previous bubble are praying daily for this but we are skeptical.

In previous letters we argued that inflation is quite complex and current inflation has many causes, some of which were temporary in nature and some that might be more permanent. For example, housing had skyrocketed on the back of record lower interest rates at the same time as there was post-Covid pent up demand (i.e., this inflation input was almost solely caused by central banks poor timing). But with higher interest rates, the affordability of mortgages declines, and this leads to lower prices. This has started to come through in countries with adjustable mortgages, but is just beginning in those with more fixed term mortgages such as the USA (housing also is a lagging indicator in CPI). We think this is good for society. Housing should not change in value by 50% in two years (nor should single-family housing be an “asset” traded by private equity firms - but that is another rant). Food inflation will only significantly reduce after a year or two of bumper growing seasons. Oil and gas are a function of the economy on the demand side yet supply remains constrained. As many expect a global recession and China is in the middle of a COVID reset oil has been on the back foot. We still believe there is a structural shortage after years of low capital expenditures and any economic upswing will cause significantly higher prices. We called out supply chain issues and freight to be temporary in nature and this has turned out to be mostly correct.

On the other hand, corporations have learned that being completely dependent on just in time inventories, single suppliers or single countries is a bad idea. Resulting nearshoring and strengthening of supply chains requires higher working capital and this is inflationary. The green energy transition is very inflationary as we completely change the way we produce electricity, build cars, make cement, fertilizers, steel, and other inputs. The massive demand for batteries will continue to buoy many commodity prices as we replace the global fleet of cars. The monetary aspect of inflation is also far from recovering. Central bank balance sheets (Fed holds $8.6 trillion of interest-bearing assets versus <$1 trillion before Lehman Brothers collapse in 2008) remain swollen and have barely begun to unwind. This deluge of debt that must be digested by markets will keep pressure on rates unless the central banks reverse course – which would likely lead us back to asset inflation and other significant distortions to the economy as it has for the past decade.

A newer inflation topic that we are just developing a view on is wage inflation. We are incredulous that many central bankers believe they need to raise the unemployment rate to stifle inflation by causing job losses and loosening the labor market (i.e., destroying employees current bargaining power against capital). We understand the concept of the wage inflation spiral of the 1970s (when unions were significantly stronger than they are today) but we simply do not believe we are in such a situation and the backdrop is completely different. There are many reasons to raise interest rates and keep them high but rising wages for low-paid workers so that they can eat and stay warm in winter isn’t one of them in our view. Perhaps this is a topic for another letter.

Luckily, forecasting inflation that has very little to do with our investing strategy. The market’s preoccupation with the topics is a sideshow for us, however it does create volatility and volatility creates opportunities to buy high quality companies at bargain prices. We are heartened that more market participants are looking at valuation again, although for how long is anyone’s guess.

Timing investments is always tricky, as noted in our previous letter we sold Brazilian credit rating agency Boa Vista as we thought an irrational player was damaging the market and we wanted some evidence that they returned to the normal behavior of an oligopoly. This proved to be ill-timed as Equifax made a bid for the company shortly after. Our other sale of the third quarter was the Greek refiner Motor Oil, which we sold after the government-imposed an irrational “windfall” tax on them based on their “normal” profitability using COVID years as the base. We were disgusted but the stock nevertheless went on to perform exceptionally during the fourth quarter.

In the fourth quarter we added one significant position outlined later in this letter and two starter positions and sold our long-term holding in Ringmetall as we believed we were at peak earnings for this cycle.

Our top performers of 2022 include OCI ( OCINF , see our fourth quarter 2021 letter for why we thought 2022 would be great), H&T (UK cost of living crisis) and Verallia ( VRLAF , a new position taking advantage of the markets short-termism on energy prices and pricing power). Our top detractors were iHeartMedia ( IHRT ), a levered radio and podcaster, RHI Magnesita ( RMGNF ), which had a large working capital build and Esprinet, which suffered from a slowdown in IT spending in Italy.

At quarter-end our portfolio had more than 117% upside to our estimated NAV and was trading at a weighted average P/E of 6x, FCF/EV yield of 20% and a return on tangible capital of 29%.

| Contributors |

| Detractors |

| Jost Werke |

| +160 bps |

| IHeartMedia ( IHRT ) |

| -45 bps |

| International Game Technology ( IG ) |

| +141 bps |

| [Undisclosed Position] |

| -19 bps |

| Verallia ( VRLAF ) |

| +104 bps |

| [Undisclosed Position] |

| -17 bps |

| RHI Magnesita ( RMGNF ) |

| +101 bps |

| Caltagirone |

| -17 bps |

| MTU Aero Engines ( MTUAF ) |

| +79 bps |

| Ibstock ( IBJHF ) |

| -14 bps |

The top contributor during the fourth quarter was JOST Werke (+47% +160 bps), the German truck and agricultural machinery supplier, which we introduced in our fourth quarter 2019 letter. JOST reported 22.8% sales growth for the first nine months which was translated into 15.4% growth in operating profits. Apparently, the company was able to compensate a weaker development in Europe, mainly due to raw materials inflation, energy costs and supply bottlenecks, with a strong operating performance in North America and Asia-Pacific. Following the strong performance, management raised its sales and earnings forecast for 2022, with sales expected to exceed the €1.2 billion mark for the first time.

The second largest contributor was International Game Technology (+32.3% +141 bps), the Italian-American lottery and gaming machine technology provider, which we introduced in our first quarter 2020 letter. The Company posted a sales increase of 8% and profit contribution from all operating segments, primarily driven by global gaming. Although the margin was 2% lower versus the second quarter of 2022, it remained above the last 15 quarters average. Market concerns about the debt level should abate on improved operating performance and as the already announced disposals reduced leverage to 3.1x. It is worth noting that management hit their 2025 leverage target more than two years in advance, while returning $224 million to shareholders through midOctober 2022. Management confirmed the upper half of their fiscal year 2022 guidance which combined with an improved credit profile drove the share price higher. We still find the steady cashflows and low valuation very compelling.

The third largest contributor was Verallia (+36.8% +104 bps), a leading French glass packaging manufacturer, which we introduced in our second quarter 2022 letter. Following their second quarter guidance increase, they increase guidance again in the third quarter (Full year EBITDA guidance started at €700 million and moved to €750800 million after the second quarter and now sits at greater than €820 million at the third quarter release) on the back of stellar earnings. They demonstrated their pricing power and highlighted the shortage of glass packaging in Europe. Furthermore, the company announced the purchase of Allied Glass in the UK, which gives them a beachhead to expand in the region. Verallia has almost fully recovered from the sell-off caused by the energy crisis and war in Ukraine but we still believe there is significant upside as its quality and growing cashflows are clearly underestimated.

The fourth largest contributor was RHI Magnesita (+33.5% +101 bps), the AustrianBrazilian refractories company, which we introduced in our second quarter 2019 letter. According to management, customer demand remains strong with price increases offsetting cost increases. Management also reported market share gains in the steel segment and stable market share in the industrial segment. Increasing net debt linked to the working capital remains a point of concern, especially given their use of working capital finance lines, but an expected cash release should normalize both over the coming quarters. Our thesis was predicated on the company having pricing power and not beholden solely to commodity prices as well as being linked to rather stable steel volumes versus highly cyclical steel pricing. Although they were a bit slow adjusting prices early on in this inflation cycle, they seem to have returned to normal margins and are maintaining them now. While we expect European steel volumes to perform poorly during this winter, other geographies such as India should partially offset this. We still believe the company is well positioned and poorly misunderstood by the market despite the stock being the largest inception to date detractor for the fund.

The fifth significant contributor was MTU Aero Engines (+31.1% +79 bps), the German aircraft engine manufacturer, which we introduced in our second quarter 2020 letter. The company reported solid third quarter earnings, held a capital markets day which surprised the market positively, brought forward the recovery to 2023 from 2024 and benefited at the end of the quarter from the Chinese government dropping its zero COVID policy which will inevitably help global air traffic.

The top detractor was iHeartMedia (-24.3% -45 bps), the American radio and podcasting company. The company is the highest levered business in our portfolio and has suffered on fears of an advertisement slowdown. Company insiders continue to buy stock in the market and the company as of yet, has not seen the drastic slow-down the market is predicting. With long debt maturities and a growing podcasting business, as well as likely interest from a major shareholder, we think the company can survive all but the harshest of recessions. If, on the other hand, there is even a couple years of moderate growth, the company could be worth many multiples of the current share price.

The second largest detractor was a new undisclosed position (-5.5% -19 bps) in the fertilizer industry. We will likely discuss this position in future letters.

The third largest detractor (-17 bps) was an undisclosed American furniture manufacturer. The loss is largely result of the decline in the US dollar. The company had been on our watch list for a couple of years. We seemed to have missed a decent COVID induced rally but as the stock retreated this year, a bid became public as the bidder said that the board would not engage with them and wanted to go to the shareholders. We decided to initiate a small position as we felt the company was trading at a large discount to intrinsic value and either the bidder would go hostile or the board would have to do something significant to realize value for shareholders. Quite bafflingly, the CEO has been buying stock both before the bid became public (but after the board was approached) and after the bid was made public. Time will tell, though a possible recession might push back this opportunity. We decided to build a small position.

The fourth largest detractor was Caltagirone (-6.2% -17 bps), the Italian holding company. We do not believe there was any significant news as both its major holdings Cementir and Generali reported decent earnings given the current situation. The minor loss is more likely due to the illiquidity of the stock in the illiquid month of December despite an increase in the sum-of-the-parts valuation discount.

The fifth largest detractor was Ibstock (-6.9% -14 bps), the British brick and concrete product manufacturer, which we introduced in our third quarter 2019 letter. In October

2022 trading statement, the company reported trading ahead of expectations with robust demand patterns and strong operational performance supported by cost management initiatives and dynamic pricing to counter cost inflation. Management completed the share buyback program and increased full-year guidance. Despite positive update, the market remained concerned about the property market slowdown with home builders reporting drastic slowdown in bookings.

LNA Santé (LNA FP)

“Throwing out the baby with the bathwater” whilst a cliché, aptly describes the current share price of LNA Santé following a scandal at their much larger peer Orpea. Orpea’s wrongdoings and alleged wrongdoings were exposed in the book Les Fossoyeurs (The Gravediggers), and led to a 93% share price decline during 2022 and will result in a complete financial restructuring. We believe LNA’s situation to be completely different and thus its share price reaction irrational.

Le Noble Age (LNA) was established in 1990 with its first nursing home in France. Today, it is one of the leading care home operators in France, with activity in Belgium and Poland, with an authorized base of 9,996 beds. The company splits operations into Nursing Home (44% 2021 sales, 5,033 operating beds, 177 under transformation), Medical & Rehabilitation, Psychiatric and Surgery (38% sales, 2,688 operating, 757 under transformation) and Home Care (9% Sales, 580 operating, 100 under transformation). On the Real Estate side, the company carries real estate assets on its balance sheet on a transitional basis until completion of a redevelopment and subsequently sells them to real estate investors. This strategy significantly differentiates the business model from that of peers Orpea and Korian. LNA’s in-house development team saves development money, allows the Group to transform the facility according to their own standards and offers them a discount on post-exit rent as they do not inflate the real estate values. Part of Orpea and Korian’s challenges, outside the book’s allegations, are their large portfolio holdings which are highly levered and whose values are being hit by higher interest rates.

While optically nursing homes and medical centres shouldn’t have high barriers to entry, this is in fact not true. In France, operators are required to gain prior approval from local authorities before they can build, open, or operate a new nursing home. Since 2012, regulators in France have authorized, extensions aside, very few openings of new nursing homes. Authorizing new licenses simply increases state’s healthcare budget, since the government covers the salary cost of medical professionals and parts of other costs such as medical equipment. The existing regulatory framework offers a growth avenue through acquisition of existing licenses, small private or state-owned, while it protects incumbents from new entrants through blocking an at-scale new entrant. The state is also incentivized to sell existing licenses to private operators since that reduces the healthcare budget and improves the quality of services.

While LNA looks like another levered nursing home operator, we don’t believe that the company faces the same credit risks as Orpea or Korian. In this case, real estate debt relates to properties bought for refurbishment and only stays for a short period of time on the balance sheet. Aside from that, the operating business is <2.0x levered. Management agrees and is buying back stock in the market. Regulatory risk is also less of a concern for LNA and management welcomed changes as they believe that any increase will allow the company to compete more efficiently and reduce budgeting discrepancies versus peers. Industry-wide staff shortages are a challenge for all operators. However, LNA’s reputation allows them to attract trained staff ahead of competition. Finally, inflation adjusted state funding, tariff renegotiations and minimal (<3% of sales and currently hedged) energy exposure will allow the company to navigate through inflationary headwinds.

Whilst LNA Santé may face stricter regulation and some higher costs, we do not believe this justifies the 41% fall in the share price during 2022. The company is family owned and operated and we believe to be of significantly higher quality (and have more integrity) than their larger peers evidenced by occupancy rate recovery post-Covid and post-scandal (versus Orpea’s and Korian, which have not recovered to pre-Covid levels). Trading at a free cash flow yield of above 12% on 2024 numbers with a strong pipeline of additional beds and a demographic tailwind (ageing population), we think the market will slowly recognize the value once the Orpea restructuring is past us and a few quarters of continued earnings resilience are achieved.

As stated in our previous letter, we are currently not charging a management fee until the fund reaches a larger size. The founder’s class management fee will then be only 1% of assets. We do not charge entry or exit commissions despite our KIID saying it is theoretically possible.

Our focus is and remains on the portfolio, but we do need to grow our assets to a sustainable level. Please feel free to share this letter with any potential investors.

We now have a commercial agreement with Cobas Asset Management to distribute our fund in Spain. You can now open an account and place orders with them. For more information please contact them via phone or email. In the future, we hope it will be possible via their website. You can reach the Cobas team at +34 91 755 68 00 or info@cobasam.com

Our fund can be invested through both European international central securities depositories: Euroclear and its FundSettle clearing platform and Clearstream through the Vestima fund clearing platform. Our fund is registered for distribution in the UK, Spain and Luxembourg including for retail distribution.

Currently the following financial institutions in Spain are distributors: Renta 4 (you need may need to contact them – it is not offered on the website yet), Ironia, Lombard Odier, Banco Alcala as well as many other institutions working through the main platforms in which the fund is available upon request: Allfunds Bank and Inversis.

In the UK we are offered on the AJ Bell low-cost platform ajbell.co.ukand can be part of an ISA or pension.

Our fund is also available on SwissQuote swissquote.comwhere almost any nationality (ex-USA) can open an account without local Swiss taxes being an issue.

If you have any issues finding our fund or you wish to get more information about us and our process, please contact us at IR@palmharbourcapital.com

Our fund is being offered as part of a Spanish pension value-orientated fund of funds. If interested in investing in a Spanish pension scheme, please contact us.

We thank you for your ongoing support. We continue to believe this is a great time to be a value investor and are very excited about the medium-term prospects for the current portfolio.

Yours faithfully,

Palm Harbour Capital

| This information is being communicated by Palm Harbour Capital LLP which is authorised and regulated by the Financial Conduct Authority. This material is for information only and does not constitute an offer or recommendation to buy or sell any investment or subscribe to any investment management or advisory service. In relation to the United Kingdom, this information is only directed at, and may only be distributed to, persons who are “investment professionals” (being persons having professional experience in matters relating to investments) defined under Articles 19 & 49 of Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 & Articles 14 & 22 of the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemption) Order 2001 and/or such other persons as are permitted to receive this document under The Financial Services and Markets Act 2000. Any investment, and investment activity or controlled activity, to which this information relates is available only to such persons and will be engaged in only with such persons. Persons that do not have professional experience should not rely or act upon this information unless they are persons to whom any of paragraphs (2)(a) to (d) of article 49 apply to whom distribution of this information may otherwise lawfully be made. With investment, your capital is at risk and the value of an investment and the income from it can go up as well as down, it may be affected by exchange rate variations and you may not get back the amount invested. Past performance is not necessarily a guide to future performance and where past performance is quoted gross then investment management charges as well as transaction charges should be taken into consideration, as these will affect your returns. Any tax allowances or thresholds mentioned are based on personal circumstances and current legislation, which is subject to change. We do not represent that this information, including any third-party information, is accurate or complete and it should not be relied upon as such. Opinions expressed herein reflect the opinion of Palm Harbour Capital LLP and are subject to change without notice. No part of this document may be reproduced in any manner without the written permission of Palm Harbour Capital LLP; however recipients may pass on this document but only to others falling within this category. This information should be read in conjunction with the relevant fund documentation which may include the fund’s prospectus, simplified prospectus or supplement documentation and if you are unsure if any of the products and portfolios featured are the right choice for you, please seek independent financial advice provided by regulated third parties. |

Footnotes[1] Our NAV is calculated weekly by FundPartner Solutions, a subsidiary of Pictet & Cie and does not align with monthly or quarterly reporting. The gross return stated is net of taxes and fees but before fund expenses, which are currently running at approximately 10 bps per quarter at current AUM. We project this to decline significantly as AUM grows. Please see our comment on management fees. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Palm Harbour Capital Q4 2022 Investor Letter