WHGLY - Palm Valley Capital Fund Q4 2023 Commentary

2024-01-06 06:45:00 ET

Summary

- The Palm Valley Capital Fund invests in small cap stocks. While our Fund is new, its underlying absolute return-based investment strategy is not. We have practiced the same strategy throughout our careers in investment management.

- For the three months ending December 31, 2023, the Palm Valley Capital Fund increased 4.00% compared to 15.12% and 14.07% gains for the S&P SmallCap 600 and Morningstar Small Cap Total Return Indexes.

- For the year, the Fund rose 9.47% versus appreciation of 16.05% for the SmallCap 600 and 20.59% for the Morningstar Index.

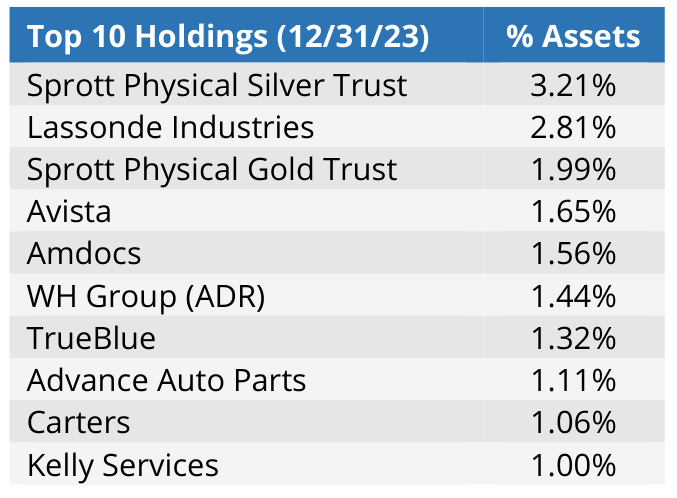

INVESTMENT PERFORMANCE (%) as of December 31, 2023

| Total Return |

| Annualized Return |

| Inception |

| Quarter |

| YTD |

| 1 Year |

| 3 Year |

| Inception |

| Palm Valley Capital Fund ( PVCMX ) |

| 4/30/19 |

| 4.00% |

| 9.47% |

| 9.47% |

| 5.42% |

| 7.72% |

| S&P SmallCap 600 Index ( SP600G ) |

| 15.12% |

| 16.05% |

| 16.05% |

| 7.30% |

| 8.37% |

| Morningstar Small Cap Index |

| 14.07% |

| 20.59% |

| 20.59% |

| 4.57% |

| 7.48% |

| Performance data quoted represents past performance of the Fund’s Investor Class ( PVCMX ) and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be higher or lower than the performance quoted. Performance of the Fund current to the most recent quarter-end can be obtained by calling 904-747-2345. As of the most recent prospectus, the Fund’s Investor class gross expense ratio is 1.53% and the net expense ratio is 1.28%. Palm Valley Capital Management has contractually agreed to waive its management fees and reimburse Fund operating expenses through at least April 30, 2024. |

The Leftovers

“Over here, we lost some of them. But over there, they lost all of us.”

—Nora Durst, The Leftovers

Dear Fellow Shareholders,

The Leftovers is a supernatural HBO drama that begins three years after the Sudden Departure, when 2% of the world’s population disappeared instantly on October 14, 2011. This event is captured in a touching montage during opening credits for the series, which explores how different families confront the grief of inexplicably losing their loved ones. One of the main characters, Nora, lost her husband and two children in the vanishing. The odds of that misfortune were 1 in 128,000. Like most of the Leftovers, Nora tried pressing on with life by landing a job interviewing potential beneficiaries for Departure Benefits. Several others in her Mapleton, New York, community followed a darker path, joining a nihilist cult of silent chainsmokers dressed in white called The Guilty Remnant. They aimed to be a living reminder that nothing is normal anymore.

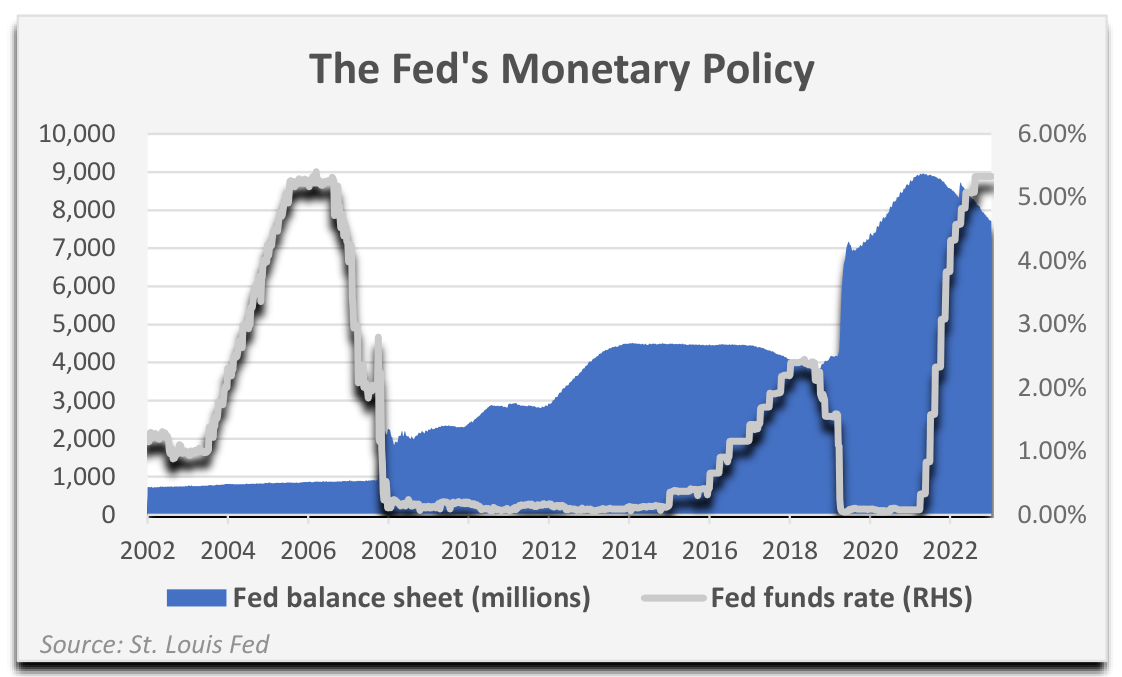

In a professional sense, we can relate. For the U.S. financial markets, the Sudden Departure transpired in Fall 2008, when the government and Federal Reserve tag teamed to “save humanity” from the unfolding credit crisis. In a sudden departure from historical precedent, the period that followed saw aggressive Quantitative Easing and the flooring of interest rates, which lasted for seven years. Many level-headed investors disappeared as asset prices skyrocketed. Others abandoned discipline to become a shadow of their former investment selves.

Nearly every money manager who didn’t participate in the bubble re-formation suffered professionally.

Politicians and the central bank delivered a monumental encore in 2020, doling out printed money at an unheard-of rate to counter the effects of COVID lockdowns…and then some. Just when things became interesting for value conscious investors in March 2020, stock prices mooned. And so did other prices. The culpable, yet outwardly overconfident, Fed attempted to slay the inflation dragon by unwinding the loose monetary policy they had normalized. While higher rates took the wind from the sails of speculative and long duration assets in 2022, the Great Asset Bubble of the 21 st Century came roaring back in 2023.

{kind=link}

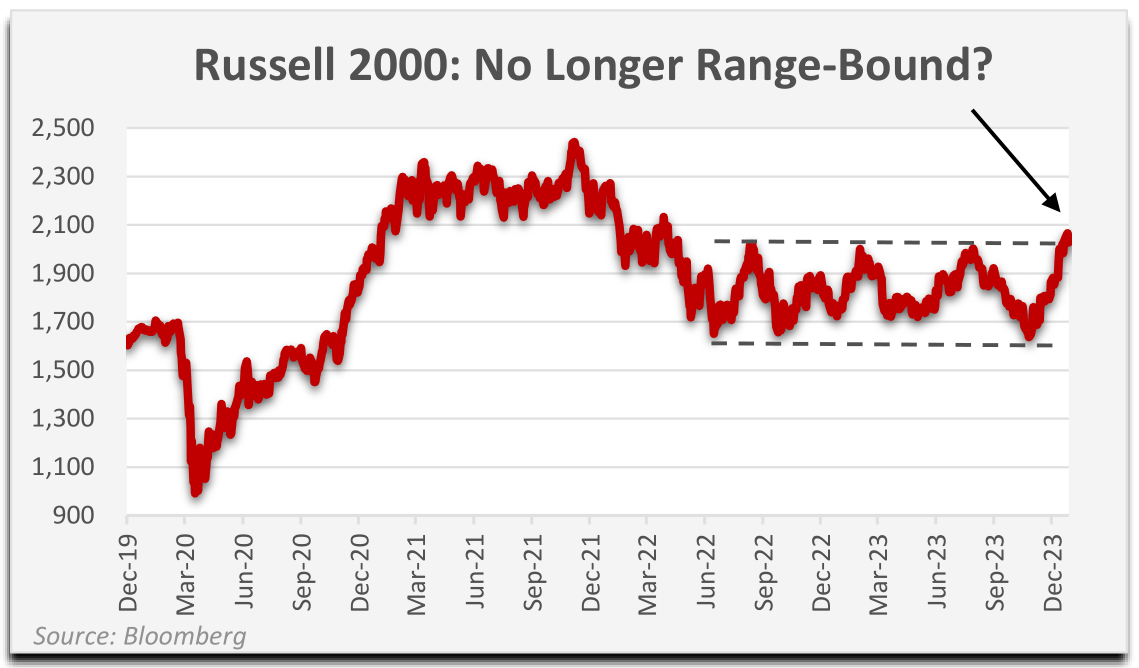

Stocks and home prices are at record highs, despite depression-worthy deficits and a 500 basis points move up in the Federal funds rate over 18 months, because investors expect the Fed to return to monetary easing in 2024. The only 2% that vanished last year was the Fed’s sanctified inflation target. Sign us up for Departure Benefits! Chairman Powell, in his December 13th press conference, gave the clearest indication yet that he won’t disappoint, promptly sending Russell 2000 small caps up almost 7% in 2.5 trading hours. Nothing is normal anymore.

If NASDAQ royalty has experienced a rapture-like event, then the average small cap was stuck in Leftovers purgatory. That changed suddenly in November, when the Wall Street bull machine went into overdrive rejoicing at an inflation print that was 0.1% below expectations. With the Magnificent Seven trade long in the tooth and investors eager to embrace a new story, small caps surged 26% from their October bottom.

{kind=link}

The Russell 2000 Index is now higher than any time except 2021. It still sits 16% below its all- time peak, which was a period when many idiotic things were happening, in our opinion. The NASDAQ and NYSE exchanges are littered with hundreds of stocks trading for below $1 per share, a vestige of the pandemic’s SPAC tsunami.

In our view, the sluggish trajectory of small caps over the last two years, until November, was an overdue and insufficient reckoning of valuations that went haywire after the credit crisis. Prices ran far ahead of earnings. In some cases where bottom lines seem to have caught up, the durability of underlying fundamentals is tenuous. Furthermore, while we hate to disappoint those embracing an Argentinian argument for stock prices, the U.S. economy’s recent bout of inflation has not nominally cured preexisting equity overvaluation. That bill is too steep, and that’s a devil’s bargain anyway.

{kind=link}

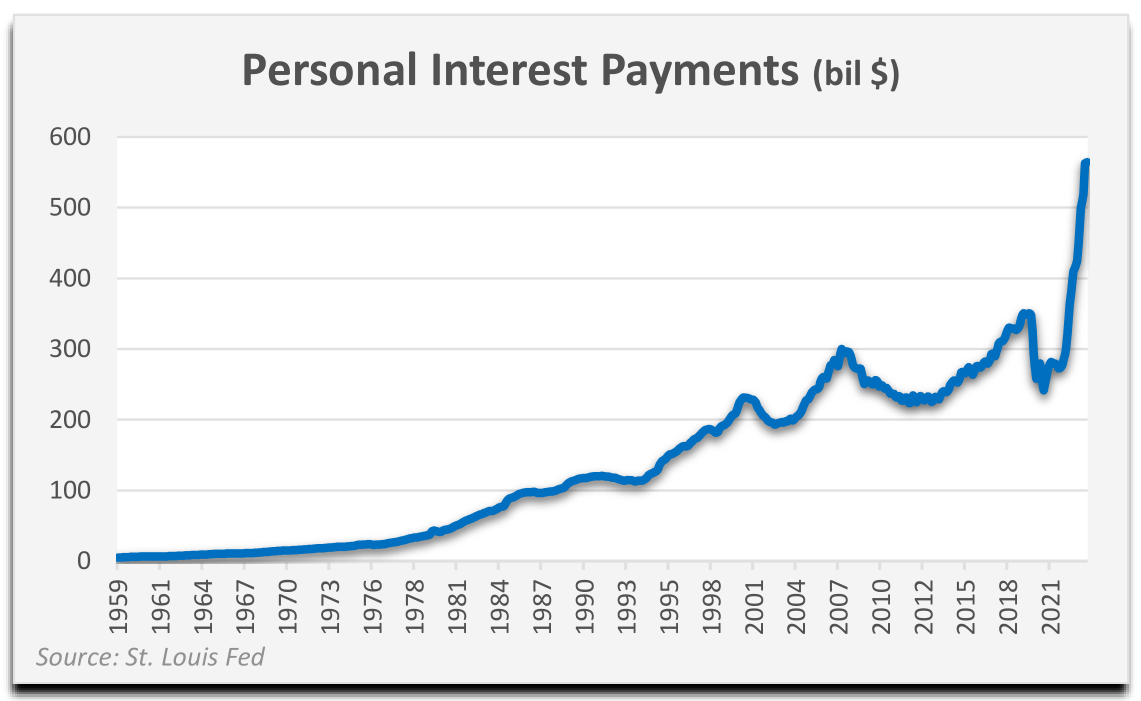

Although stocks may have escaped the full corrective response typically delivered by inflation and higher interest rates, the half of Americans without significant assets have become more financially strained. Higher prices don’t make things better for them. Forget buying a home, just renting an average apartment consumes almost half the U.S. median wage of $41k. Forty percent of Federal student loan borrowers failed to make their payment when collections resumed in October. Walmart now offers a Buy Now, Pay Later option on self-checkout kiosks. Even Chairman Powell acknowledged the dilemma: “A common theme is that while inflation is coming down, and that’s very good news, the price level is not coming down…So people are still living with high prices. And that’s not—that is something that people don’t like.”

While equities are often viewed as inflation hedges, that argument weakens when costs exceed revenues.

{kind=link}

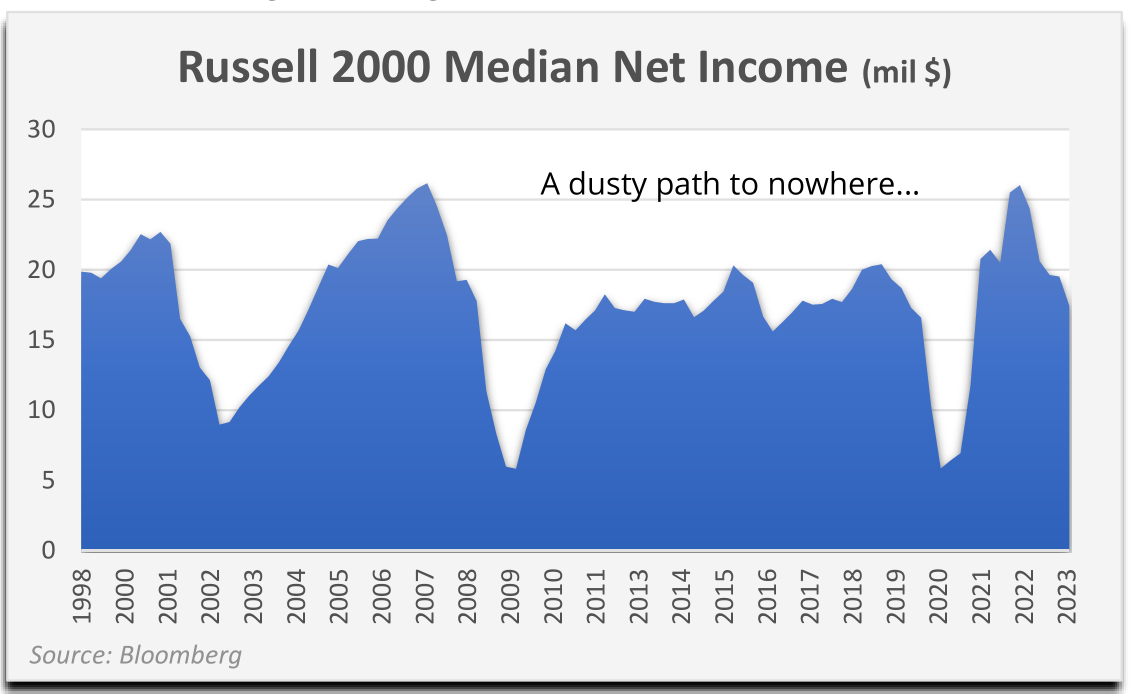

Throughout this cycle, it was hopes and dreams, not cash flows, that propelled the share prices of the expanding proportion of unprofitable Russell 2000 constituents. Before the credit crisis, 20% of Russell members didn’t make money. Today, it’s 40%. Median net income for small cap public companies is basically the same place it was 25 years ago, in nominal dollars.

{kind=link}

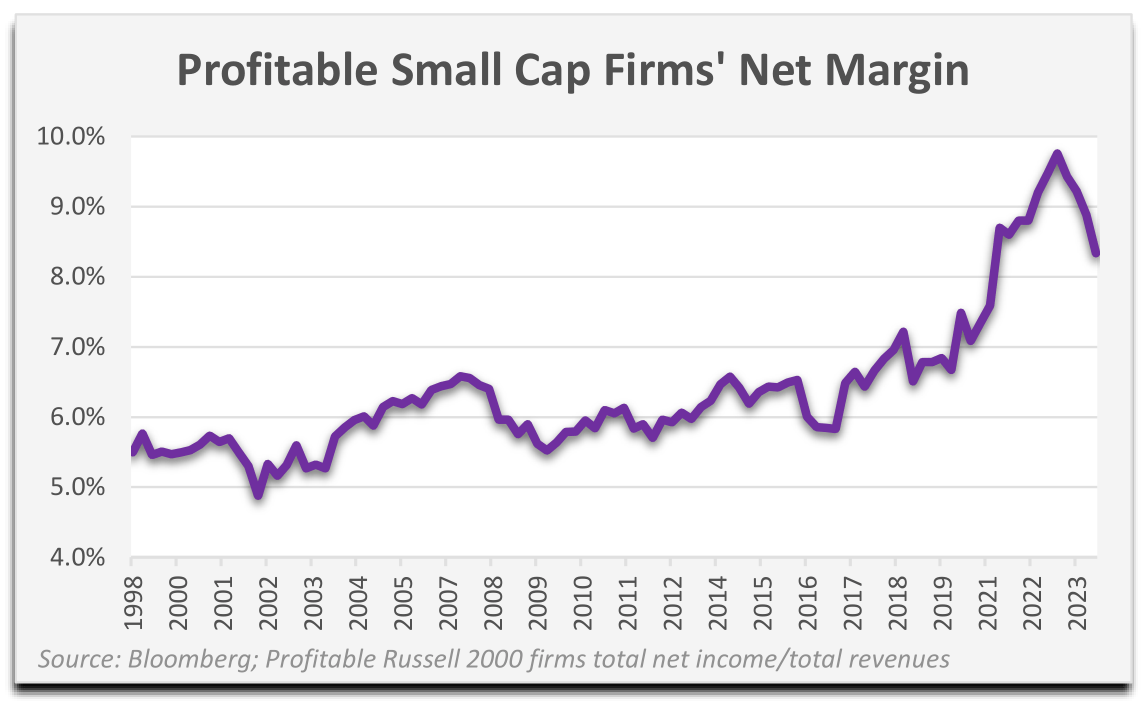

While the overall quality of the small cap universe has declined, profits for good businesses marched forward at an impressive rate after 2010. The aggregate net profit margin for profitable Russell 2000 small caps is approximately 40% higher than it was before 2018, reflecting corporate tax cuts and a pandemic boost. The expansion in the median profitable company margin is not as dramatic, which demonstrates a growing influence of larger firms on Index profitability. The contraction in margins from their 2022 record is due to financial company pressure from higher interest rates, as well as lower nonfinancial margins due to a reduced stimulus impact. We think the profit descent has a long way to go.

Even after the recent surge, the collective market capitalization of the ~2,000 companies in the Russell Index is scarcely more than the size of the biggest company alone (Apple), so small caps aren’t a focus for many investors. Compared to the megacaps that power the S&P 500, the lifespan of many small caps as public firms is fleeting. Only 37% of the companies comprising the Russell ten years ago remain in the Index today. Another 37% of the 2013 members were subsequently acquired. That’s normally an exciting event, but over one-third of the targets were bought for less than where they traded on the start date of our analysis (December 31, 2013). While most received a higher deal value, the median acquisition premium to the start date market cap was only in the mid 20% range. Also, it took over three and a half years for the average transaction to materialize, so the median IRR from the end of 2013 to the announcement date was 8%—not exactly exceptional for a takeover. Seven percent of the 2013 constituents eventually graduated to the Russell 1000, while a low double-digit percentage left the index for another reason, such as a demotion due to a falling market cap or from failing some other requirement (e.g., minimum closing price, float, voting rights). Eight percent of the year 2013 Index members later went bankrupt, and this happened during a period of below average corporate distress. We’d wager that the 2023 cohort will fare worse.

{kind=link}

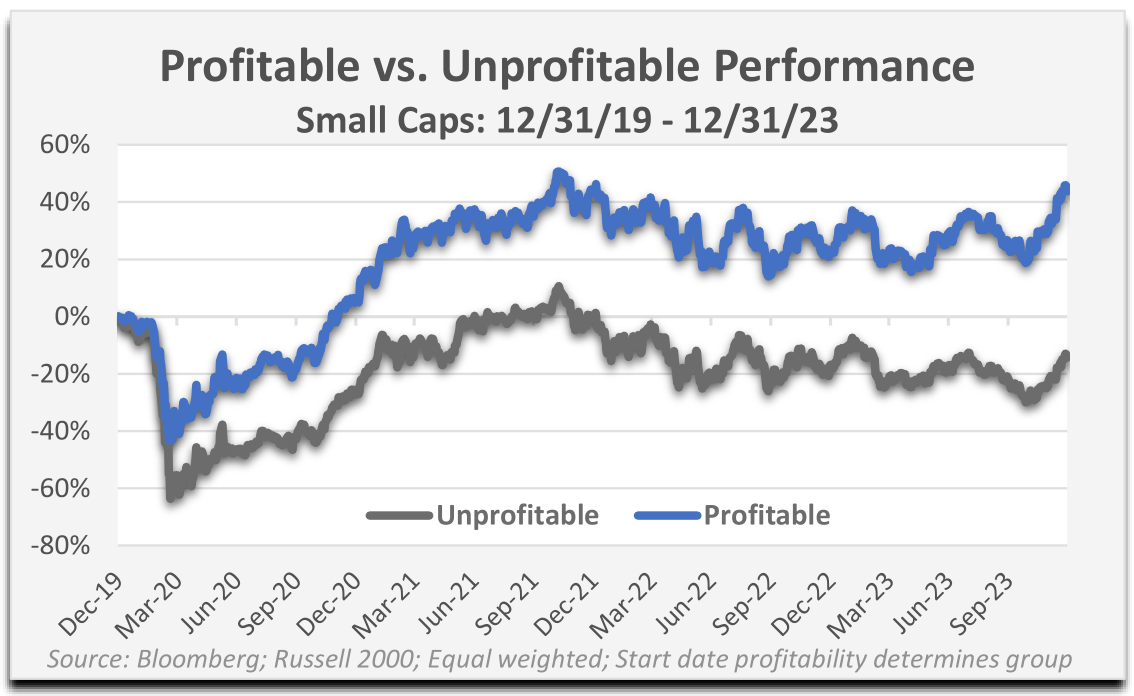

Over the past four years, the Russell 2000 has underperformed the S&P 500 by 29.5%. The Russell is up 28%, while the S&P gained 57.5%. Ignoring for a moment the heavy influence of the Magnificent Seven stocks, the large cap benchmark has few unprofitable firms and even fewer consistently unprofitable ones. The Russell has 800! The equal weighted return of only the unprofitable Russell small caps over the period was a loss of 14%, but the profitable basket appreciated 44%. The equal weighted S&P was up 47% over the same stretch. In other words, small cap returns have not been dramatically different from large caps when you eliminate the junk. Our ability to find attractive discounts has been constrained because most quality small caps never became cheap, in our opinion.

We believe we can add more value by investing in smaller companies, but we don’t view it as our role to promote an asset class. Although many small caps have been treated like the market’s unwanted leftovers in recent years, their relative performance wasn’t a mystery. Loose money produced speculative business models that don’t work, even in a fair-weather economy. The shares of more durable companies have held up, but in many cases, their profit growth is linked to reckless deficit spending. Perhaps the specter of a renewed acceleration of inflation will dissuade the government from more gigantic money drops. Or it may not. If Washington can convert a current problem into a future crisis for someone who isn’t voting for them, they’ll do it. In today’s America, the real Leftovers aren’t underperforming small caps or value investors that failed to thrive in the ZIRP/QE regime, they’re the coming generations that will be left holding the bag when we’re gone.

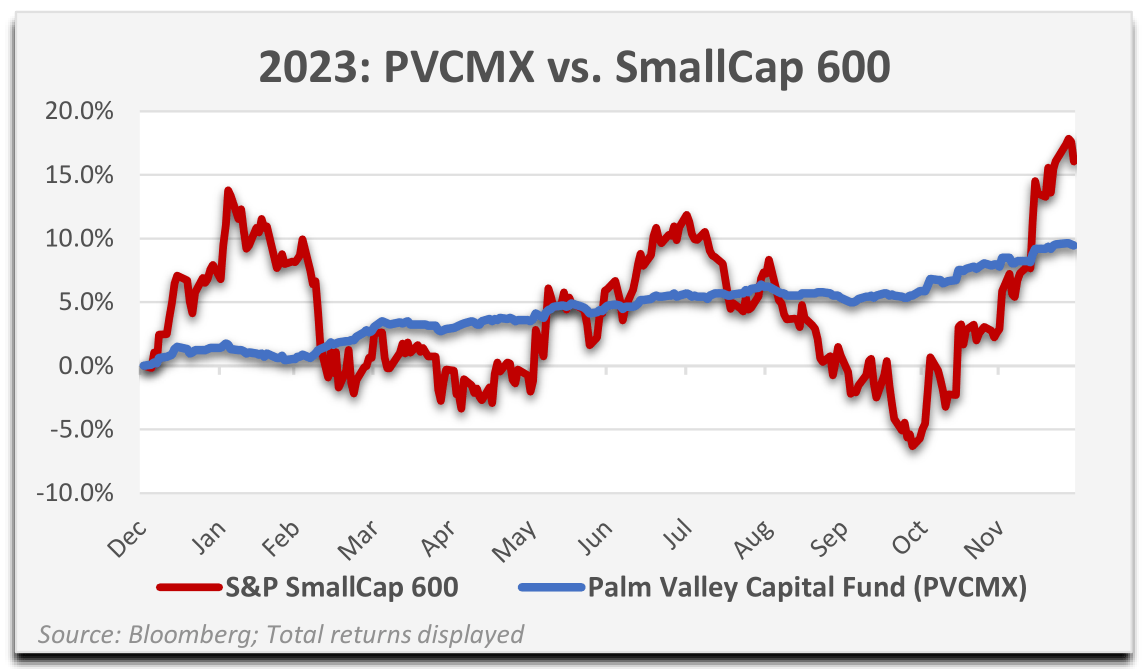

For the three months ending December 31, 2023, the Palm Valley Capital Fund increased 4.00% compared to 15.12% and 14.07% gains for the S&P SmallCap 600 and Morningstar Small Cap Total Return Indexes. For the year, the Fund rose 9.47% versus appreciation of 16.05% for the SmallCap 600 and 20.59% for the Morningstar Index. The Fund’s performance in 2023 was less volatile than our benchmarks due to our heavy weighting in Treasury bills. This positioning helped contribute to the Fund’s outperformance during the July to October market decline, but it led to significant underperformance during the November and December rally.

{kind=link}

Cash equivalents began the fourth quarter at 81% of Fund assets, declined to 75% during October, and ended the period at 78%. For the year, cash averaged 80% of assets. The equities within the portfolio increased 14.25% during the fourth quarter and 33.30% during the full year. Although equity- only results are only one component of overall Fund performance, along with the yield on cash net of fees, we have been pleased with the beneficial impact of stock selection on our risk-adjusted returns. We look forward to a day when undervalued small caps will account for most of the portfolio.

Since the onset of QE, we have faced a very expensive small cap market a majority of the time. The Spring 2020 lockdowns presented the most favorable valuations since the credit crisis, enabling us to invest in several undervalued names before stocks were rescued. There were a handful of other periods when small cap valuations improved enough to lift our hopes that the market was on its way to making sense again. Late Summer 2011, the beginning of 2016, the end of 2018, and parts of 2022 and 2023 all qualify. However, from our perspective, each of these market declines was arrested before ever delivering meaningful value. The Fed has been keen to intervene, often encouraged and assisted by the executive and legislative branches. Interventions are usually paired with pledges to quickly unwind them. Mary Poppins called these “pie crust promises”: easily made, easily broken.

In our third quarter letter to you, we described improving small cap valuations but pointed out that these were mostly occurring in businesses with plenty of operational or financial risk. Still, we purchased a few undervalued stocks in Q3 that had responded negatively to rate hikes. This continued in October, when we acquired two new positions for the portfolio and also added to around half of our existing holdings.

The narrow window of opportunity for picking up value has mostly closed, in our opinion. A combination of strong earnings reports and the market’s winter ramp carried several Palm Valley holdings closer to our valuations. As a result, we reduced many names in the fourth quarter, including Crawford & Co. (ticker: CRD.A , CRD.B ), which had been one of the larger weightings in the Fund.

During the quarter we purchased Monro, Inc. (ticker: MNRO ). Founded in 1957, Monro is a leading auto repair and tire sales company in the U.S. The company’s stock declined throughout most of the year due to weaker than expected sales. As middle- and lower-income consumers struggled to make ends meet, many of Monro’s customers traded down to lower priced tires and delayed auto repairs. Due to these negative trends, the company’s stock traded below our valuation based on normalized free cash flow, so we started a position. Shortly after our purchase, the small cap market rose sharply and took Monro’s shares along for the ride! In an unusual occurrence for our strategy, we sold Monro’s stock during the same quarter it was purchased because its stock price exceeded our calculated valuation.

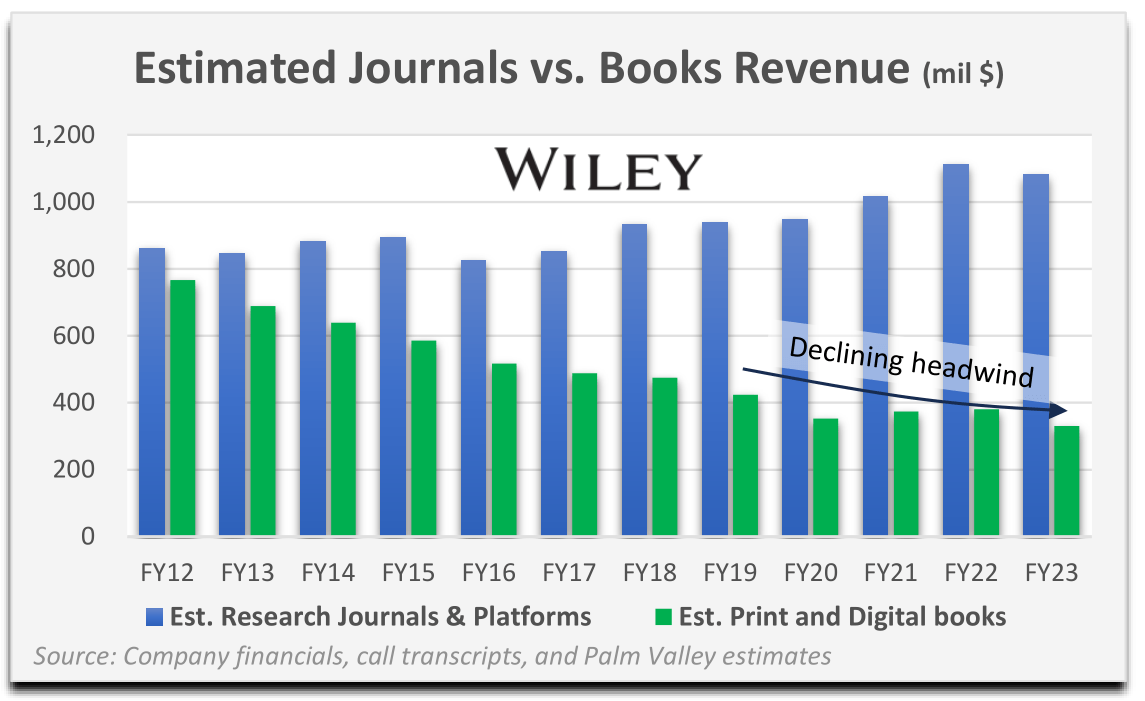

We also purchased John Wiley & Sons (ticker: WLY ), one of the world’s leading publishers of academic research. Founded in New York City as a small printing shop in 1807, Wiley is one of the oldest independent companies in the U.S. Early in its history, Wiley served legendary American writers including Herman Melville, Edgar Allen Poe, Nathaniel Hawthorne, and James Fenimore Cooper. The firm even supplied books to repopulate the Library of Congress after it was burned in the War of 1812. Today, Wiley is one of the leading global providers of academic journals, and it also sells books and courseware for higher education and professional roles.

The company’s stock has suffered from quality control issues tied to a 2021 acquisition, and Wiley’s CEO was pushed out abruptly in September while the firm works to divest non-core operations. Furthermore, a long-term decline in sales of printed textbooks has weighed on results, but soon this should no longer be a material headwind.

{kind=link}

The academic journals business at the heart of Wiley has strong profitability and high barriers to entry. The company generates consistent cash flow, and new management may focus more on returning capital to shareholders than value-destructive M&A. We picked up Wiley’s stock near multiyear lows when it was selling for 10x trailing free cash flow and at a dividend yield exceeding 4.5%.

{kind=link}

There were no securities negatively impacting the Fund by at least 10 basis points in Q4. The three positions contributing most positively to the Fund’s fourth quarter performance were Crawford & Co., Lassonde Industries (ticker LAS.A:CA ) and WH Group (ticker: WHGLY ). Crawford recently delivered its highest quarterly operating profit in five years. While management cautioned that Q4 results wouldn’t be as strong because no major hurricanes hit the U.S. during the fall, we believe investors are rewarding Crawford for expanding margins in its business segments that aren’t dependent on the weather.

Lassonde’s profits increased far more than revenue in Q3, as pricing actions and reduced freight expenses are fully offsetting modest volume declines. Skyrocketing costs for orange concentrate will force the company to continue to take pricing on OJ, potentially impacting demand. However, Lassonde has a broad portfolio spanning branded and private label and including apple and other juices. The Canadian firm is also working to improve profitability in its U.S. business under a broad strategic plan.

{kind=link}

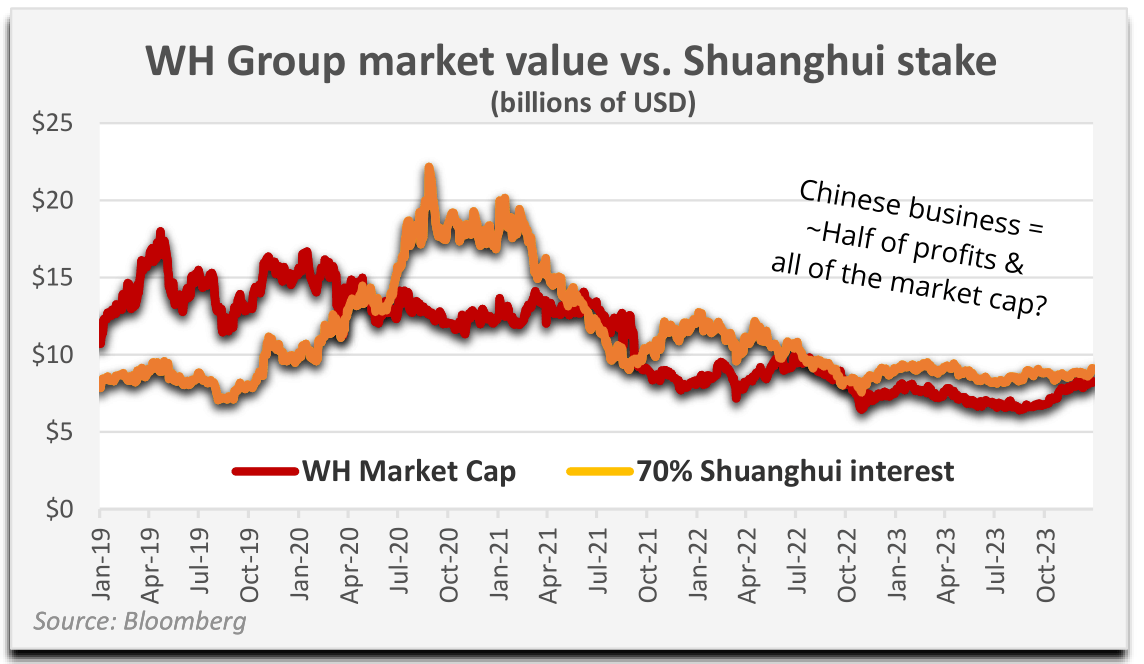

Despite continued weakness among Hong Kong stocks during the quarter, WH Group partly rebounded from its multiyear slog. The company’s third quarter performance improved markedly over the first half of the year as a result of significantly reduced losses in the U.S. Pork segment. On October 19th, The Wall Street Journal reported that WH Group is working with banks to take Smithfield public in the U.S. For several years the Hong Kong parent company has traded for less than the market value of its 70% stake in Henan Shuanghui, WH’s Chinese subsidiary. One could argue investors were assigning negative value to U.S.-based Smithfield and the European subsidiaries, which often account for half of WH’s profit. However, capital controls in China partially reduce the informational value of Shuanghui’s stock price. Nevertheless, a U.S. IPO of Smithfield should help resolve WH Group’s undervaluation.

The only position negatively impacting full year 2023 returns by at least 10 basis points was Natural Gas Services (ticker: NGS). We sold NGS earlier in the year after management laid out a growth plan that included meaningful new borrowings. This violated our internal policy of not holding companies with significant operating and financial risk.

For the year, three holdings having the largest favorable impact on performance were Crawford & Co., Lassonde Industries, and Miller Industries (ticker: MLR). Crawford’s stock had materially underperformed the market before 2023, and improving fundamentals combined with an undemanding valuation led to significant appreciation during the year. Both Lassonde and Miller experienced substantial cost inflation throughout the pandemic, which negatively impacted profitability. However, the firms were able to pass through pricing, with a lag, and this was evident in their improved results during 2023.

“The world changed when Superman flew across the sky.

And then it changed again when he didn’t.”

—Amanda Waller, Suicide Squad

In 2009, author Tom Perrotta began writing The Leftovers—the novel on which the series was based. Although he never cited the economic downturn as an inspiration, the dour mood it cast couldn’t have hurt. Perrotta explained to a New York Times book reviewer, “I know that feeling of being left behind.”

{kind=link}

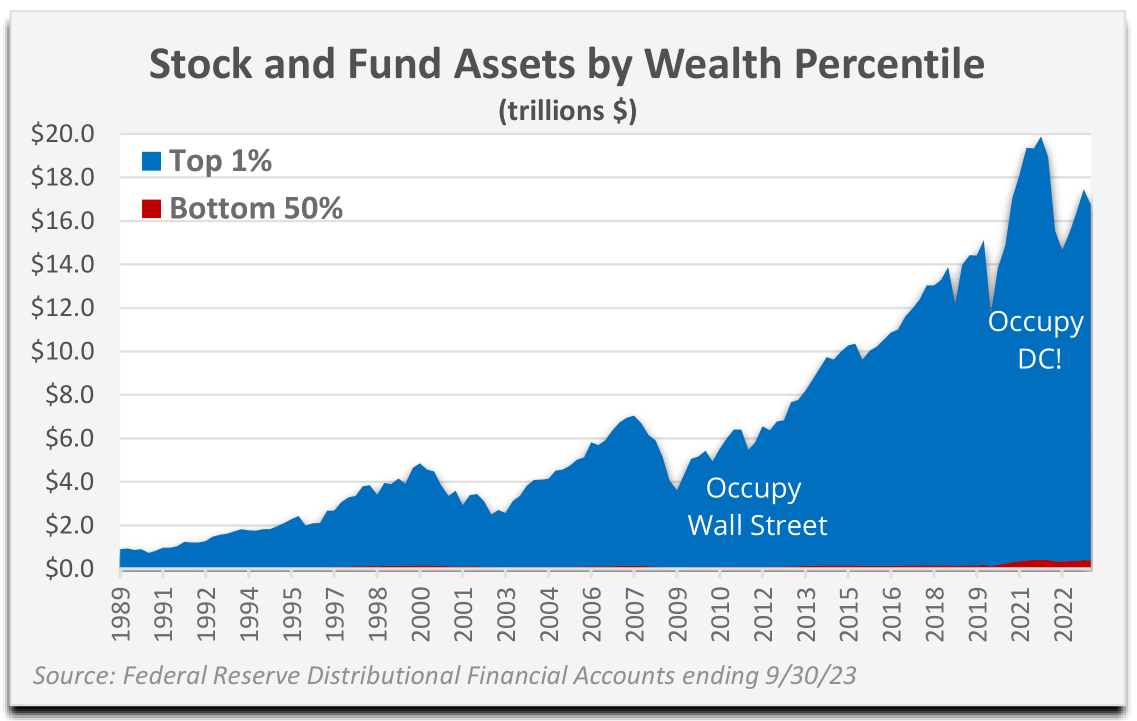

Since central banks began using asset prices to steer the economy, many have been enriched, but countless others haven’t benefited at all. Occupy Wall Street, a Fall 2011 economic analog of The Guilty Remnant, flamed out within months due to a lack of clarity about the goals of protestors. Nevertheless, “We are the 99%” became a rallying cry for identifying the class warfare that many feel is underway.

We believe rising economic inequality is the unappreciated nuclear risk for equity investors. Fed Chair Powell has remarked that the biggest contributor to inequality is losing your job. Yet, we have a massive wealth gap despite years of labor market strength. Many folks barely get by, and disinflation is a cold comfort when shelter, transportation, and healthcare costs are already breaking the bank. The Fed’s plan is to cut rates in 2024 to make it somewhat easier for people to finance all these overpriced necessities. While that may be the spoken reason, what goes unsaid usually drives the ship. The U.S. government’s annual interest tab is approaching $1 trillion, exacerbating alarming deficits. The Treasury Department, along with the wobbling commercial property market, could use a lifeline. The Fed also won’t readily surrender the spending boost associated with the wealth effect it ignited. Thus, instead of higher for longer, we have a quagmire for longer.

After a 40-year tailwind from lower interest rates culminating in the most extreme Fed policies ever implemented, the vested interests are unwilling to endure a normalization of financial conditions. Yield, we hardly knew ye. Nevertheless, we believe there is a limit to the asset inflation and wealth gap the middle and lower classes are willing to tolerate before they revolt against the entrenched system. Are housing prices going to soar again on top of current record levels? Is labor going to accept a further expansion in margins for large corporations? Will legislators attempt to square the circle by enacting huge tax hikes to fund universal basic income programs, bringing resentment from both sides? If Washington’s goal is to eliminate recessions by any means necessary, does that mean the business cycle will only end when society implodes?

Give us free markets—not risk-free markets. In the age of empty suits, papering over problems with cheap money is the hollowest of solutions.

Thank you for your investment.

Sincerely,

Jayme Wiggins Eric Cinnamond

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Palm Valley Capital Fund Q4 2023 Commentary