PANL - Pangaea Logistics: Curios Shipping Stock With An Attractive Yield

2024-01-05 22:38:25 ET

Summary

- Pangaea Logistics is a curious shipping company. It has 26 vessels, 12 of which are ice-class, and operates primarily on voyage charters and contracts of affreightment.

- PANL has 73% total debt to equity and 48.2% total liabilities to total assets. The company has maintained EBITDA/Interest Expense above 5.0 since 2018.

- The company has lower but stable margins due to the focus on voyage charters and COA. PANL pays dividends with attractive yields that are sufficiently covered.

- Except for the P/TBV ratio, PANL trades in the lower percentile than its peers. Looking at the historical multiple, PANL is undervalued compared to 10Y peaks; however, it trades close to its 5Y average figures.

- I give PANL a buy rating.

Introduction

Pangaea Logistics ( PANL ) is a curious shipping company. It has 26 vessels, 12 of which are ice class, and operates primarily on voyage charters and contracts of affreightment ((COA)). On top of that, the company owns stevedoring services in a few locations in North America and Greenland.

PANL has a solid balance sheet with $87 million cash, $275 million total debt, and a 0.31 cash-to-total debt ratio. Owning ice-class ships gives an advantage over the other bulker companies, reflected in the company's average rates. 3Q23 , the company realized 49% higher day rates than the Baltic Panamax and Baltic Supramax indexes.

The profit margins are lower than other bulkers due to the revenue composition. PANL prioritizes voyage charters and COA over time charters. This means the company has to cover all expenses: operational costs (crew, repair and maintenance, lube oil, spares) and voyage costs (bunkering fuel, port charges, canal transit dues). However, PANL maintains a healthy return comparable with its peers operating time-chartered vessels. PANL stock trades at lower multiples (except P/TBV) over its competitors. I give PANL a buy rating.

Bulkers recap

Let's quickly recap the bulk shipping market before proceeding with the PANL fleet and financials.

Tankers and bulkers share more similarities than differences in the current bull cycle. The supply-side catalysts are global fleet age, low order book figures, and limited shipyard capacity. The demand side is pushed by higher iron ore, coal, and agricultural commodities demand by developing countries, especially China and India.

The Chinese government plans to keep fiscal stimulus for the economy, boosting productivity and resulting in a growing demand for metals. In the coming quarters, we might see a recovery in the Chinese economy, pushing the development of new projects across industries. That means enhanced demand for iron ore, coal, and aluminum in the coming quarters. China announced 60% higher import quotas for crude oil in 2024 than in 2023. That fact will not directly impact the bulkers. However, I believe this is a sign of Chinese economic recovery.

In the long term, I expect the demand for iron to continue to grow, especially in India and China, the largest steel makers globally; apart from that, the demand for metallurgical coal used in steel production will continue to rise, too. A similar situation exists with the thermal coal used in coal power plants. Even Germany restarted its coal plants; countries like India and China are not planning to give up coal-fired plants soon.

PANL overview

As I mentioned in the intro, PANL is not the typical ship owner focused on time charters and the spot market. The table below from the last corporate presentation shows the company's business model.

{kind=link}

The company owns 25 vessels and one barge. Twelve of the ships are ice class. This means they can sail in polar water due to their purposefully designed hull and power plant. The price of a new build or at the second-hand market is higher. However, the supply of such vessels is relatively limited, and they command higher charter rates than the standard vessels, compensating for the higher capital costs. PANL ice-class vessels are operated under a voyage charter. That means the rates are contracted in the long term. This means the downside risk of declining day rates is capped. However, the company will miss the upside growth if we have a strong bull market. In my opinion, considering the peculiarities of the company, the fleet PANL management made a wise decision to use voyage charters.

PANL has 26 chartered vessels, which are given under COA. This type of freeing agreement is similar to the voyage charter, with a few distinct characteristics. The contract stipulates the shipowner’s obligation to carry specific cargoes in a fixed time frame and specified route. The charterer (cargo owner) is not responsible for delays during the cargo handling operations in the port, meaning he is not obliged to pay demurrage to the ship owner.

The chart below shows that PANL outperformed Baltic Panamax and Baltic Supramax benchmark indexes by 49%.

{kind=link}

Over 90% of the company`s revenue comes from 10 years of contracts. As I pointed out earlier, such long contracts mitigate the risk inherent in the shipping industry.

PANL offers stevedoring services in a few locations in North America and Greenland. They generate 2.8% of the company`s revenue.

The company carries various bulk commodities. Iron ore, coal, and bauxite represent over 55% of PANL cargo. The remaining is distributed between pet coke, cement, and clinker.

PANL balance sheet

It isn't easy to find a company with the same profile as PANL, which owns ice-class ships and operates port facilities. To compare its financials, I choose similar size bulker companies:

- Pangaea Logistics ( PANL ) $87 million cash; $275 million total debt; 0.31 cash to total debt ratio, total debt to equity 73%

- Diana Shipping ( DSX ) $173 million cash; $657 million total debt; 0.26 cash to total debt ratio, total debt to equity 135%

- Grindrod Shipping ( GRIN ) $71 million cash; $168 million total debt; 0.42 cash to total debt ratio, total debt to equity 60%

- Safe Bulkers ( SB ) $74 million cash; $440 million total debt; 0.17 cash to total debt ratio, total debt to equity 57%

- Genco Shipping ( GNK ) $48 million cash; $141 million total debt; 0.33 cash to total debt ratio, total debt to equity 15%

The company has a 0.31 cash-to-total debt ratio, ranking in the middle of its peer group. Debt to equity is 73%, comparable with GRIN and SB. GNK is the top performer with 15%, while DSX has the highest ratio of 135%.

Let`s see how PANL capital structure has developed over the years.

{kind=link}

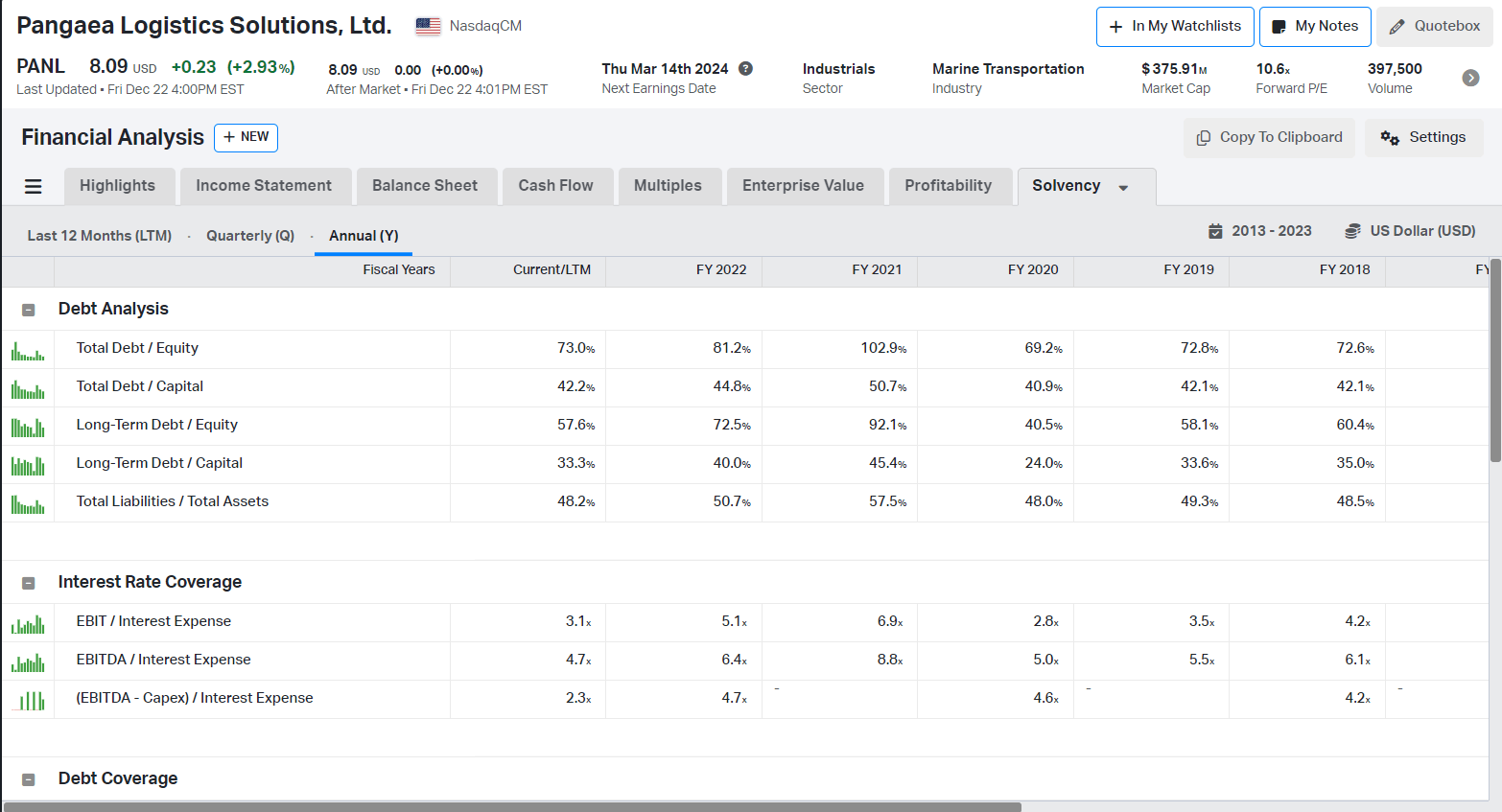

In 2021, the company had 103% total debt to equity and 57.5% total liabilities to total assets ratios. PANL management reduced the company’s debt by more than 25% in two years. It`s worth mentioning the company has bought seven vessels in 2021 at bottom prices. This is the reason for the higher leverage in that year.

Now, PANL has 73% total debt to equity and 48.2% total liabilities to total assets. PANL has $275 million total debt. Capital leases ($146.5 million) are a significant portion of the debt. In 2024, the company has to repay $20 million of its debt.

Interest coverage had declined due to lower revenues caused by declining day rates in 2023. Despite that, PANL has maintained EBITDA/Interest Expense above 5.0 since 2018. Such consistency is impressive in a volatile shipping market.

PANL profitability

Let`s compare how PANL performs against similar sized bakeries companies:

- Pangaea Logistics 21% gross margin, 17% EBITDA margin, 11.4% ROE, 5.2% ROTC

- Diana Shipping 65% gross margin, 49% EBITDA margin, 14.4% ROE, 6.0% ROTC

- Grindrod Shipping 29% gross margin, 7.8% EBITDA margin, (3.5)% ROE, 1.0% ROTC

- Safe Bulkers 62% gross margin, 52% EBITDA margin, 11.1% ROE, 5.1% ROTC

- Genco Shipping 36.5% gross margin, 26.3% EBITDA margin, 1.2% ROE, 3.71% ROTC

PANL has significantly lower margins than its peers because of the company`s preference for voyage charters and COA. Both types of freight agreements oblige the shipowner to cover all costs: capital, operation, and voyage. Under a time charter, the ship owner covers capital and operation costs, and the charter pays the voyage costs. While under the bareboat charter, the owner covers only capital costs, the reaming costs are on the cargo owner. All options have their pros and cons. The other company in the group operates their ships mainly under time charters, resulting in lower costs and higher profit margins. However, the trade-off is the assumed risk in case of day rates decline.

PANL management skillfully utilizes its fleet. Proof of that is the relatively stable margins and returns over the years.

{kind=link}

If the company chooses time charters instead of voyage charters, COA can utilize the peaks in the spot market (and the bottoms, too). Day rate volatility will generate erratic revenue, resulting in fluctuating margins.

Of course, that does not mean investing in companies operating time-chartered ships is wrong. It is the opposite. Owning PANL stocks is a smart way to diversify the shipping part of my portfolio, mitigating the risk inherent in the freight rate spot market.

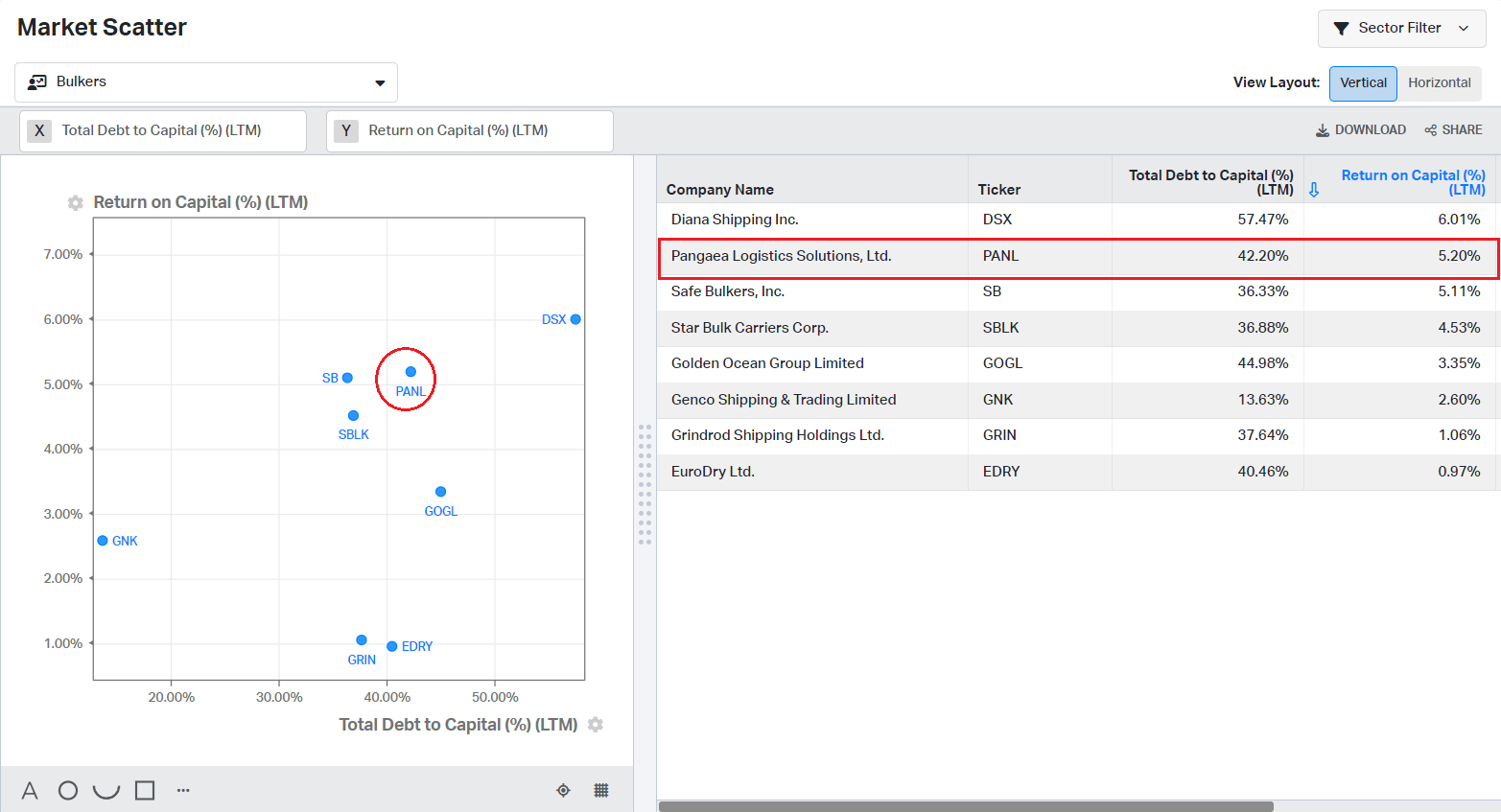

Let`s see how PANL allocates capital compared to the companies mentioned above.

{kind=link}

DSX and PANL share the first two places. With 5.2% ROTC and 42.2% total debt/total capital, PANL management has shown its capabilities to invest prudently in the company's capital.

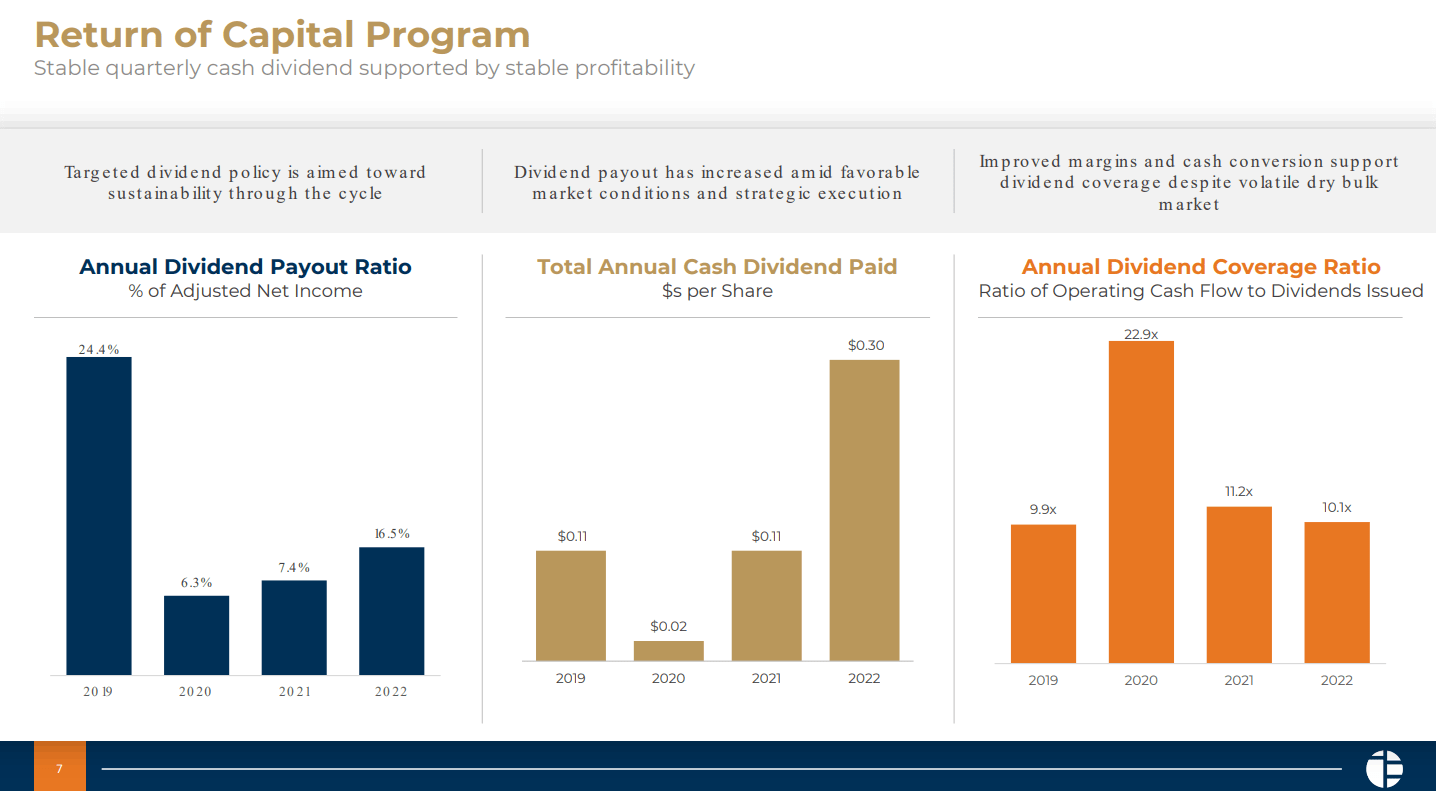

PANL pays dividends with an attractive yield of 5.09% ((TTM)).

{kind=link}

The chart above shows the company has excellent dividend coverage over the cycle. In 2022, the operating cash flow to dividends ratio is 10.1. The pay ratio for the same year is 16.5%.

PANL Valuation

First, I will compare PANL against the same companies from previous chapters:

- Pangaea Logistics 1.22 Ev/Sales, 7.15 EV/EBITDA, 1.12 P/BV

- Diana Shipping 2.83 EV/Sales, 5.72 EV/EBITDA, 0.62 P/BV

- Grindrod Shipping 0.73 EV/Sales, 9.34 EV/EBITDA, 0.57 P/BV

- Safe Bulkers 2.8 EV/Sales, 5.38 EV/EBITDA, 0.57 P/BV

- Genco Shipping 1.99 EV/Sales, 7.56 EV/EBITDA, 1.02 P/BV

PANL trades at the highest P/TBV, the second lowest EV/EBITDA, and the second lowest EV/Sales.

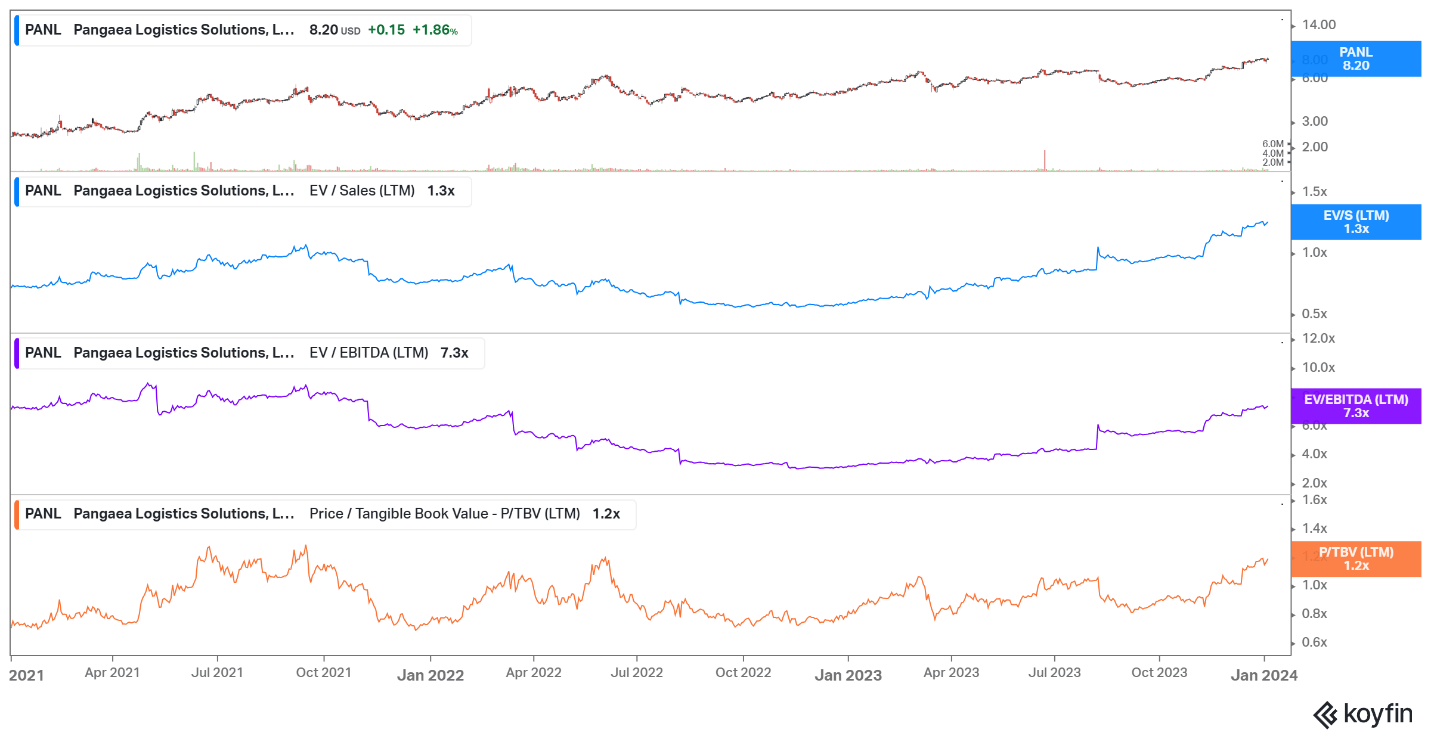

Let`s compare PANL against its past multiples.

{kind=link}

The company trades below 10Y peaks (1.4 EV/Sales, 17.9 EV/EBITDA, 1.5 P/BV). Compared to 5Y average multiples (0.81 EV/Sales, 9.23 EV/EBITDA, 1.28 P/BV), PANL stock trades erratically: much higher than EV/Sales, lower than EV/EBITDA and equal to P/TBV.

In conclusion, I assume PANL stock is relatively undervalued by the market. Due to the Red Sea crisis, the investors’ attention will focus on shipping stocks. PANL will hook entrepreneurial investors with its distinct fleet and business model.

Risks

PANL carries lower risks compared to its peers. The primary reason is the focus on voyage charter and COA. They cut the downside risk in the day rates bear market. Of course, the price is limited upside potential in a bull market. Considering the distinct fleet, including ice-class vessels, I assume using Voyage charters and COA is the better choice.

Financially, the company is sound, given its capital structure and interest rate coverage. The annual interest varies between $11.5 million-$21.5 million over the last five years. The operational cash flow varies between $20.8 million-$134 million for the same period. Besides that, the company has $87 million in cash.

Investors takeaway

PANL is a curious proposition for investors seeking exposure to the shipping industry. The company owns 25 vessels and one barge. Twelve of the ships are ice class. The company prioritizes voyage charters and COA over time charters, resulting in lower but stable margins. PANL has a healthy balance sheet with sufficient liquidity and a sound capital structure. The company distributes dividends with attractive yields. Except for the P/TBV ratio, the company trades in the lower percentile compared to its peers. Looking at the historical multiple, PANL is undervalued compared to 10Y peaks; however, it trades close to its 5Y average figures.

For further details see:

Pangaea Logistics: Curios Shipping Stock With An Attractive Yield