PARXF - Parex Resources: Why The Exaggerated Fears Can't Compare To Its Growth Potential

2023-12-26 05:06:25 ET

Summary

- Parex Resources is the largest independent company in the oil and gas sector operating in Colombia.

- It is also one of the rare companies able to grow free cash flows above 40% while buying back 10% of its shares and providing a dividend yield above 5%.

- All the above, achieved debt-free.

- According to its 2P NAV value, Parex remains significantly undervalued.

- The company faces specific risks associated with its ground of operations, including political instability and security concerns. But once put into numbers, the risks seem overstated.

Editor's note: Seeking Alpha is proud to welcome Dannys Jorge Martinez Herrera as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Is There An Investment Thesis Here?

Parex Resources ( PXT:CA ) is a Canadian exploration and production (E&P) company that operates in Colombia. It is the largest independent land holder in the country, especially since 2021 when Parex quadrupled its acreage. This overlooked, mid-cap company has managed to outperform both the S&P500 ( SPY ) and the S&P/TSX Capped Energy Index ( XEG:CA ) since going public in November 2009:

Parex Resources stock price history compared to S&P500 (SPY) and S&P/TSX (XEG) (www.tikr.com)

Parex has maintained a pristine balance sheet, with zero debt in it. All its operations are funded by the company's cash flows, which are also the source for aggressive buybacks and for funding a high-yield dividend. In the last 10 years, Parex's diluted earnings per share have grown at a staggering 33.03% CAGR while CapEx increased at a 6.7% CAGR only. The company's free cash flow grew at a 44.7% CAGR since 2015 -it was negative before then- and the return on invested capital ((ROIC)) has been on average 25% through the last ten years. According to the net asset value of its proven and probable reserves (2P NAV), Parex remains deeply undervalued. Therefore, I am rating Parex as a Strong Buy.

In this article I will focus on the factors affecting Parex's operations through 2023. For the ease of the comparisons, I will represent the impact of every risk factor as a percentage of Parex's revenues of 2022 whenever possible.

The Elephants In The Room

Parex's impressive record of returning value to shareholders has been achieved under a major downward pressure on the share price. Conducting operations in Colombia scares investors to the bones. And we can imagine why: the country's history of political instability, social unrest and a long-lasting guerrilla activity are big enough concerns. However, none of it has stopped Parex from succeeding, suggesting that all those fears are probably overblown. But let's turn them into numbers and see what they are telling us.

First of all, investors panicked with the current Colombian president's plans for the oil & gas sector. Before swearing into office on August 7th, 2022, Gustavo Petro announced that his government would not sign new exploration contracts. That statement made international headlines, but in words of Parex's CEO Imad Mohsen, at the Capital Markets Day event of December 6, 2022:

I've not seen -- because we do our planning to apply for these licenses long in advance, we're not seeing any bottlenecks because of government actions.

(source: TIKR.com. Meeting transcript)

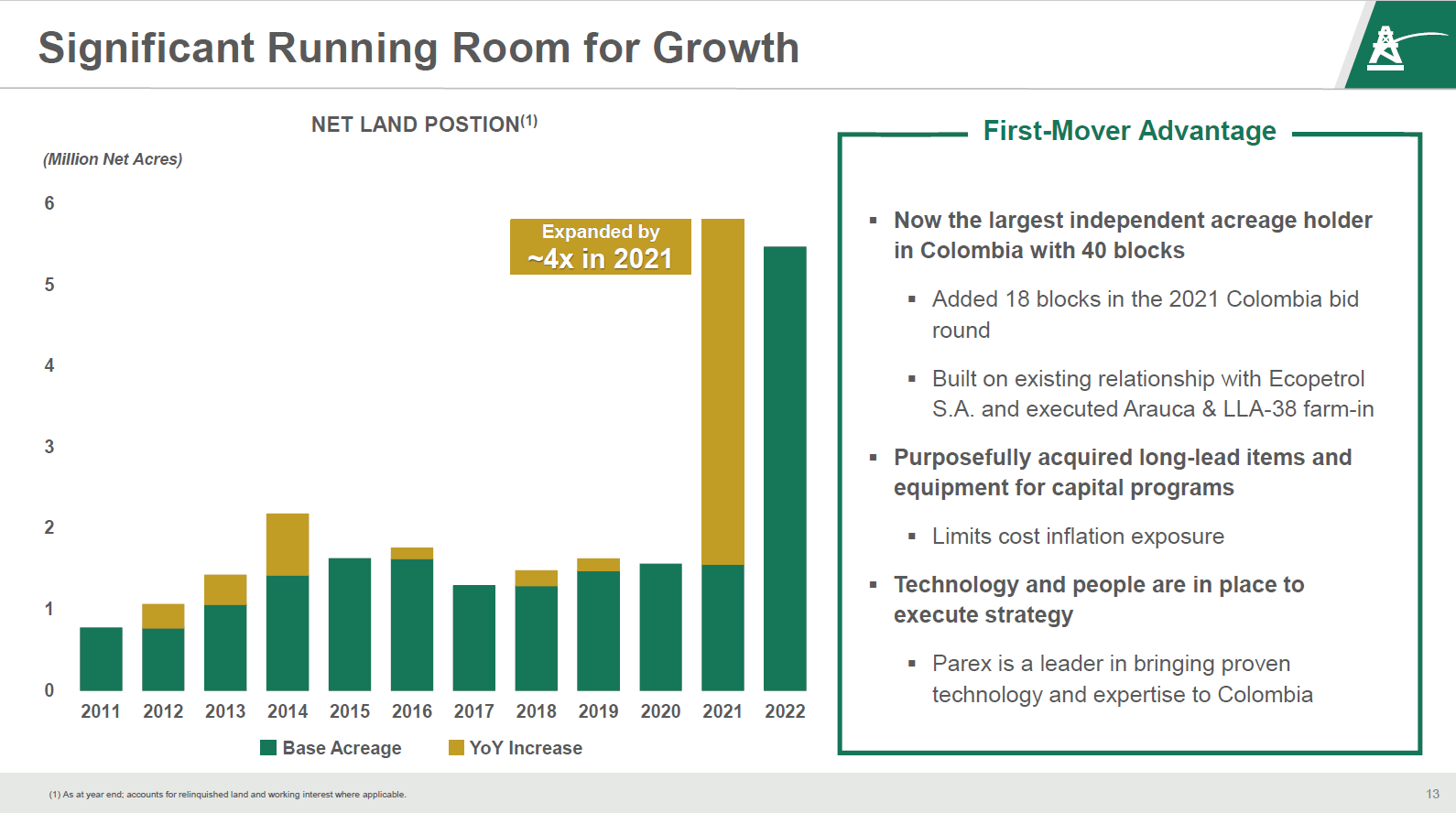

In the open bid round of 2021, Parex increased its land position in Colombia to approximately 5.9 million net acres, which is 3.7 times greater than the company's acreage by 2020 year end. Since then, Parex SG&A has increased 16%, mostly due to new personnel hired to start the production on new blocks. Therefore, this first risk factor should have a 0% impact on Parex's operations, and Imad Mohsen couldn't make it clearer at Parex's Q3 2022 Earnings Call:

So I'd like to highlight the fact that before this election last year, we managed to acquire 18 blocks, which has basically quadrupled our land area in Colombia. With that -- with a number of active licenses that we have in our portfolio, we don't see any constraints whatsoever for a decade plus on our running room in terms of exploration. So with that in mind, we are observing the new government's views on opening blocks or reactivating them or not, but we don't see any impact given that we are already -- that we have more than enough .

Parex Resources net land position since 2011 (Parex Resources Investor Presentation, April 2023)

{kind=link}

Now that the first fear has been addressed in depth, let's move on to the next one in the queue: the social unrest and security concerns. Sadly, illegal paramilitary groups continue extending a 50 year-long armed conflict in Colombia. Multiple peace agreements have been signed, the latest one with the FARC (Revolutionary Armed Forces of Colombia. Acronym in Spanish) in November 2016, leaving the ELN (National Liberation Army. Acronym in Spanish) as the last remaining operative guerrilla group. In August 2022, a 180-day cease fire was agreed between the Colombian government and the ELN as part of ongoing negotiations. Although frequent crossfire between rogue factions of these armed groups still occur, major achievements signal a clearer path for peace in the country.

On top of that, oil companies like Parex operate in rural areas in Colombia where basic infrastructure like roads, well-equipped schools and sometimes clean drinking water is lacking. Therefore, road blockades and other civil rights demonstrations are not infrequent. Parex has reported shut-ins due to social unrest or security concerns (guerilla activity) in 6 years since 2011. Correct, roughly once every two years. The shut-ins with the highest impact on Parex's operations happened in 2023. According to the press releases of April 17 and August 2 , the impact was of approximately 6,500 boe/d (barrels of oil equivalents per day) across Q1 and of 3,850 boe/d across Q2. If we translate that to dollars by using Parex's realized oil sell price in those two quarters, the losses caused by those shut-ins were in total $63,714,270 or the equivalent of 4.86% of 2022 revenues.

But in spite of the largest shut-ins in the company's history, Parex has managed to increase oil production year-over-year: in-line in Q1, 7% increase in Q2 and 6% increase in Q3. And three new wells are expected to start producing in Q4. At this point, I can only think where Parex's production levels would be had the shut-ins not happened. But we won't have to wait much to see it, if the company continues increasing production at its current rate.

Commodity prices fluctuate following their cyclic nature, and oil prices have been lower in 2023 than in 2022. Certainly, the FFO (funds flow by operations) has been hit, but in the last decade it grew at a strong 12.5% CAGR in a per share basis:

Parex Resources average production and FFO since 2010 (Parex Resources Annual General Meeting 2023 Presentation)

According to the International Energy Agency ((IEA)), the oil demand will continue to grow at least until 2028. In my opinion, Parex's fundamentals show an impressive historical performance. Since it is nearly impossible to consistently predict where oil prices will go, I will be cautious and call it a draw between the positive and negative consequences of oil prices to the company's future business.

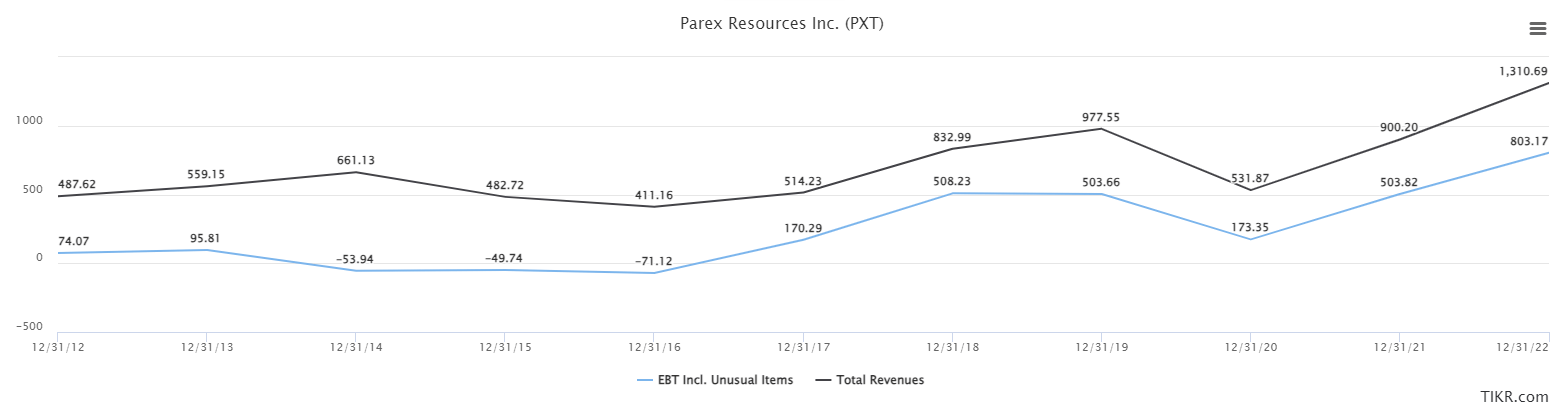

In November 2022 the Colombian Congress approved a tax reform that increases the max income surtax from 10% to 15% when Brent oil prices surpass $80/bbl. It also prevents the deduction of base royalties paid to the Colombian government. As the dear reader can imagine, that law caused a lot of panic among companies and investors. In 2022 Parex paid $17.68M in royalties, almost twice as much as in 2021 and more than five-fold 2020 royalties. From 2012 to 2022, the amount of taxable earnings (EBT, earnings before taxes) as a percentage of total revenues has expanded from 15.19% to 61.27%. Of course, with some bad years in between such as 2014-2016 due to a depressed oil market and 2020 due to the COVID-19 pandemic. But note also Parex's resilience and how the company managed to come out of those bad years stronger:

Parex Resources EBT and Revenues since 2012. Numbers in millions USD (www.tikr.com)

{kind=link}

Now, assuming future oil prices will always remain above $80/bbl as in 2022, the impact of the tax reform should be approximately an extra 3.89% of revenues (5% increased surtax plus 1.35% of revenues in royalties non deductible from EBT, which were 61.27% of revenues). But Parex revenues have a long history of growth, 10.39% CAGR since 2012 to be exact.

Parex production expenses increased by $0.59/boe in Q3 2023 mainly because of two elements: increased electricity costs and well workovers and maintenance on two production blocks. The latter is part of the CapEx within Parex's capital allocation, which we will park for now since this article intends to delve deep into the risks, not the growth drivers. Electricity costs increased due to a drought caused by the meteorological phenomenon El Niño . Colombia relies mostly on hydropower to produce electricity (73.37% share of production in 2022: Statista ), so a drought can increase the electricity production costs. Parex's production of the first 9 months of 2023 was 53,567 boe/d and if that rate is maintained, the company should produce a total of 19,551,955 boe in 2023. Assuming both El Niño and those $0.59/boe of increased electricity costs keep coming every year, Parex will see $11,535,653 extra costs per year, or 0.88% of 2022 revenues. Nothing that would make a dent in the company's earnings.

Giving Back

It is notable how much the company gives back not only to shareholders, but to the communities where Parex operates. Parex's ESG Strategy includes investing 1-2% of the yearly capital in community initiatives. Since 2017 the company has invested more than $14M in the Works For Taxes program, benefiting over 68,000 community members in conflict-affected zones. In 2022, Parex was awarded five projects under the program, representing a historic $23 million investment. Through Parex-owned Energy for All program, the company has already provided 1,035 community members lacking power sources with access to solar energy. Since 2018, through the Water for All program, Parex has improved access to clean drinking water to over 33,000 locals in communities surrounding Parex's operation fields. Parex also aims to eliminate routine flaring by the end of 2025 (gas flaring is the burning of the natural gas associated with oil extraction) and to achieve net zero greenhouse gas emissions by 2050. In 2022, Parex launched its first solar farm with 7,200 panels that will replace approximately 10% of all field energy requirements. And those are only a few examples of Parex's major achievements in reforestation, biodiversity preservation, humanitarian aid and other initiatives detailed in Parex's 2022 Sustainability Report .

Valuation

A common way to value upstream companies is by means of the net asset value of its proven and probable reserves (2P NAV). Oil and gas reserves are classed as proven, probable or possible. Proven reserves are also known as 1P and many analysts refer to them as P90, or having 90% certainty of being produced. Probable reserves are known as P50 or having a 50% probability of production. Together, they are referred to as 2P.

In the press release of February 3, 2023, the company 2P NAV is calculated as follows:

2P NAV valuation formula (Parex's press release)

where:

- NPV10 (after tax) : present value of estimated future oil and gas revenues, net of forecasted direct expenses, and discounted at an annual rate of 10%.

- Working capital : current assets minus current liabilities.

Parex reported NPV10 after tax of 2P reserves valued in $3,435,562,000 as of December 31, 2022. Working capital was $84.99M and there were 109.112M basic shares outstanding by year end. Using those values in the formula, we will arrive at a 2P NAV for Parex of $32.26 per share or CAD 42.88 (USD/CAD exchange rate as of December 23, 2023). Considering Parex' shares are trading at CAD 25.40 at the moment of writing this article, the company is approximately 41% undervalued by its 2P NAV valuation.

Conclusion

Every business faces risks and Parex Resources certainly has some of its own. For starters, the inherent volatility of oil prices might scare some investors away from a long-term story of success. The fact that Parex's operations are conducted in Colombia naturally raises questions about the political instability, security concerns and social unrest problems the country faces. These risks deserved a dedicated analysis, and after quantifying their impact on the company's operations, the fears do not seem that daunting anymore. Surely, they do not justify a potential 41% undervaluation, as shown by Parex's 2P NAV value.

That becomes even more evident when considering Parex's multiple growth engines, some of which were mentioned earlier. Parex's three-year plan includes a 5% growth in oil production per year, which has already been surpassed in Q2 and Q3 (on a per-quarter basis). The long-term capital allocation plan intends to return at least 1/3 of total FFO and 100% of free funds flow to shareholders. Parex's share buyback program has cancelled the maximum allowed number of outstanding shares (10% of total) in each of the last four years. Add that to an annualized $3.50 dividend in 2023, and there is no doubt that shareholders are being well rewarded. Remember: Parex manages to do all this without tapping into its $200 million bank credit. And the list goes on, but I hope that Parex's enormous growth potential is clearer by now. It has overcome fears and risks in the past and will likely do so in the future.

For further details see:

Parex Resources: Why The Exaggerated Fears Can't Compare To Its Growth Potential