PGPHF - Partners Group: Future Claims On Past Performance

2023-04-28 07:30:00 ET

Summary

- Partners Group reiterates interesting narratives in the private equity space that investors should be aware of.

- They claim that there is a megatrend in institutional money coming into private markets essentially because they believe public markets have become frivolous.

- They also claim that their active private approach, and determination for portfolio value creation, is going to be a less competitive area in markets.

- We think private markets may hold an increasing role in debt, but this isn't a particularly auspicious moment for private markets in general considering economic conditions.

- Slow transaction rates in PE demonstrate this, and terrible performance from an overzealous allocation year in 2021 just means that the sector will be weighed down.

Published on the Value Lab 04/25/23

Partners Group ( OTCPK:PGPHF ) is not doing well in the performance fee department. They allocated heavily in 2021 at high multiples, and for the first time in a long time, private equity ((PE)) is actually performing badly and LPs are surely very annoyed, especially with still so much dry powder to allocate currently committed to these funds which are doing nothing in terms of allocating as of now. Yet in the Q4, Partners Group makes some grand arguments about PE megatrends as if some great shift has happened that favors PE. We think that like in any recessionary capital market environment, PE will do badly, especially big ticket PE which like to have cheap debt. We actually think that the current macroeconomic and geopolitical makeup create a secularly negative tailwind for the industry, and are much more bullish on active public markets operations over private. While Partners Group is by no means doomed, and has a great history of actively improving portfolio companies' performance, we take their megatrend claims with a pretty big helping of salt, even though continuation of previously known trends such as pension funds getting into alternative assets remains at play. We don't think retail is going to take off that much, especially when we saw what happened with SPACs, and with the mid-market in public markets being similar profile (but also cheaper) that what you'd pay for indirectly in private markets but with no liquidity benefit.

Taking Apart the Q4 Comments

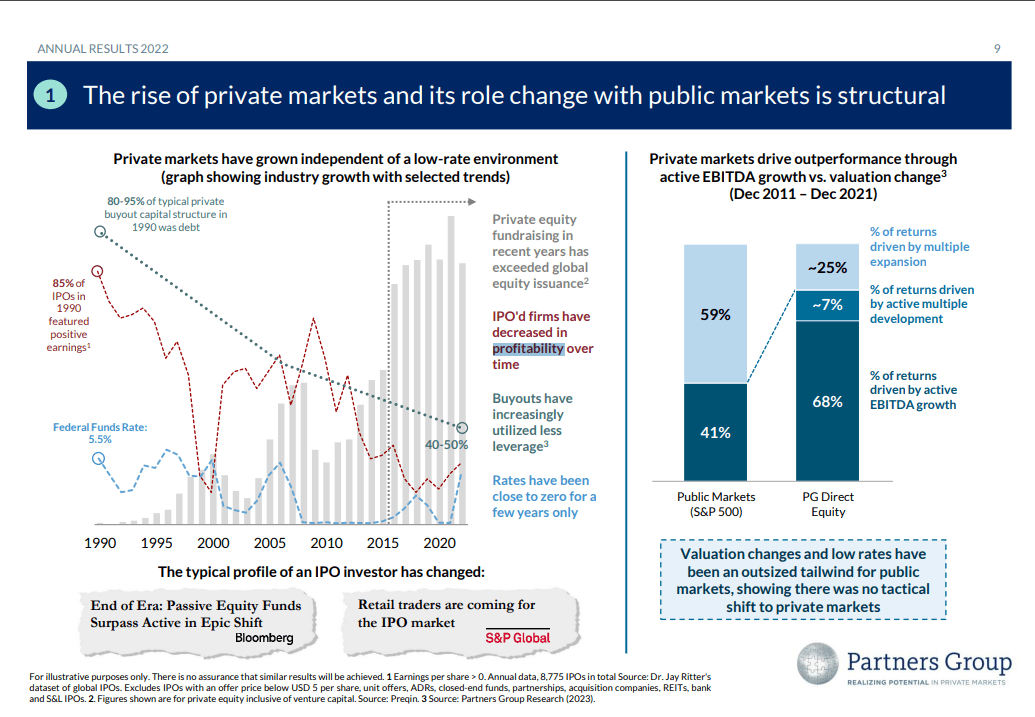

Some points are interesting . Multiple expansion has apparently driven returns in public markets (very conceivable considering the tech-driven dynamics of public markets), and IPOs, the gateway into public markets, include a greater proportion of unprofitable companies, where the return to IPOing a solid , profitable business is relatively less now than it was; in many cases not worth the higher reporting standards and implicit and explicit costs that come with that. We definitely believe it, and can see this as a good argument why take-privates had been so common prior to 2022. We also see it as a jab to public markets being more frivolous, and PG is pretty explicit in saying that public markets are of lesser importance to the real economy than they were before to private markets - that it's become more frivolous and speculative.

Less Leverage in PE, IPOs are of Unprofitable Companies (Q4 2022 Pres)

{kind=link}

Still, linking the role of public markets as a market to create returns for clients is to IPOs is dubious. There are plenty of companies that now are mainstays in public market portfolios, have driven returns, and have been trading for years having been IPO'd decades ago. Using the last 7 years of IPOs is not a particularly informative, and the rise of tech is clearly the explanatory factor in the overall trend of lower profitability of IPO'd companies, and tech justifiably is valued highly by markets and society thanks to the secular impact and implicit pricing power, thinking about Amazon ( AMZN ) as a prime example.

While we don't like tech investing, and much prefer the profile of businesses in private portfolios, the argument that PG makes is odd, especially as they claim that the current state of affairs favors a tectonic shift of money from public markets to private markets by passive investment funds. While pension funds and some other quasi-indexers have certainly joined the fray, the shift has already been very meaningful in dry powder growth.

The argument in particular that we don't like is that leverage ratios having fallen in private transactions somehow makes private markets more suitable for allocators in the current environment, specifically around rate changes.

Firstly, we don't think there's been as much reason to use debt when there's so much dry powder from LPs, and with AUM over performance having been such a contributor in overall earnings for funds since the PE boom got going in the 2010s, it makes sense to use some of that up, even if you exchange some leverage-based returns. It makes sense that leverage has fallen with the excessive availability of dry powder from allocators, which ultimately comes from leverage elsewhere in the system i.e. the money printers. Moreover, the fact is that they didn't really exchange any leveraged based returns, because rates have been so low that the money has been free, and you couldn't exactly multiply a portfolio of private companies when it has been a seller's market for years. There's a reason they have all that dry powder: there's not enough opportunities, so even with all the debt-based cash that these managers could get, they couldn't keep up with growing their portfolio, otherwise they'd have already been bottlenecked by the LPs commitments.

PG extol their ability to raise portfolio company EBITDAs, but that is easier with smaller companies in the private market arena, and it's easier in a low-rate environment that supports the sort of spending cycles that are typical to clients of PE-style businesses. Tech is more secular and consistent, and probably a lot more rate resistant on the fundamentals side, even if not the valuation side due to horizon value effects.

While multiple contraction could be a big problem for equity markets, at least there's liquidity there. Liquidity premiums are likely to grow in a major recession. Indeed, PE data is much less frequent since it's illiquid, but we have seen low transaction velocities , which means there's not even a meaningful equilibrium price yet. Whatever that will be, it will be lower in private markets than before, just like public markets. Possibly it will be disproportionately lower, especially if things like geopolitical concerns becomes a secular problem in a deglobalizing world. Liquidity premiums will rise on a secular basis and this is very bad for PE. While active PE could be valuable in a more complex environment, liquidity is always the more important driver of value when there's volatility and complexity, not some vague value-add promises from the businessmen in charge at a PE fund.

Bottom Line

While it's true that a shift of institutional money into private markets could generate returns through more lazy mechanisms like multiple expansion, the same way that multiple expansion had for years now been driving public market returns, the matter of liquidity precludes this somewhat. Moreover, while active PE is more of the norm as far as funds in the private space go, activism is growing in public markets too. This could end up capping the relative benefits of active management in private funds. We argue there are also way fewer opportunities in private markets for PE funds than on public markets for the host of retail and institutional investors focused on that market. When a company is public, you don't have to deal with primary investment into a company owned by possessive founder-owners - you deal with owners who value the liquidity, and move around frequently. The reason transaction velocity has plummeted in private markets is exactly for that reason, owners of private businesses don't want to sell equity they still own, while equity already sold to investors on public markets is easy to exchange thanks to public markets' exploitation of the benefits of liquidity.

Private debt may have a secular moment now that banking has proven fragile, and that rates are coming up. Moreover, banks aren't as well set up for taking risks on specific businesses in an environment more prone to geopolitical considerations as well, where we think deglobalization is the biggest megatrend of all.

{kind=link}

The shortfall has come in performance fees, which considering the recent bloat in the AUM and portfolios, where AUM has come up by 14% YoY, is not particularly impressive. Underlying growth is there thanks to the higher AUM and management fees, but the poor transaction environment with all sponsors playing a wait and see approach in PE is not lending itself to high realizations and carries on investments. Also, the lacking debt financing is the main barrier to getting returns right now, not so much the explicit debt cost impact. This could be an ongoing issue, even after the rate volatility passes through secondary markets, because of the banking environment.

So a transaction that previously was underwritten to a 20% return, just isolating the rate factor alone would be 18.5%. Obviously, there's less leverage available today as well. That's got an additional impact also.

David Layton, Partners Group CEO

PG trades at 22x PE. It makes some sense. Even now the company is managing EBITDA growth in its underlying companies of around 15%, and they are getting some amazing multiples on investments in a couple of major category winners that have driven performance. In no way is Partners Group and PE doomed. In fact, Partners Group remains one of the more attractive names in the space. The key issue is that we don't think PE benefits particularly from the current economic environment, and in no way outcompetes public equity in the increment going forward, which is how management spent most of the Q4 call spinning it.

For further details see:

Partners Group: Future Claims On Past Performance